*EXERCISE 12-12

(a) Cash payments to suppliers

Cost of goods sold ……………………. $5,178.0 million

Deduct: Decrease in inventory …. 5.3

(b) Cash payments for operating expenses

Operating expenses exclusive

of depreciation

*EXERCISE 12-13

Cash flows from operating activities

Cash receipts from

Customers …………………………………………. $243,000*

Dividend revenue ……………………………….. 18,000*

261,000*

*EXERCISE 12-14

TALIAFERRO CORP.

Statement of Cash Flows—Direct Method

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ……………………… $566,100

Less: Cash payments:

Cash flows from investing activities

Sale of building ……………………………………… 197,600

Cash flows from financing activities

Issuance of common stock …………………….. 355,000

Payment of cash dividend ………………………. (21,800)

Net increase in cash ………………………………………….. 258,100

*EXERCISE 12-15

Cash payments for rent

Rent expense ……………………………………………………… $ 30,000*

Cash payments for salaries

Salaries and wages expense ……………………………….. $ 54,000*

Cash receipts from customers

Revenue from sales …………………………………………….. $160,000*

SOLUTIONS TO PROBLEMS

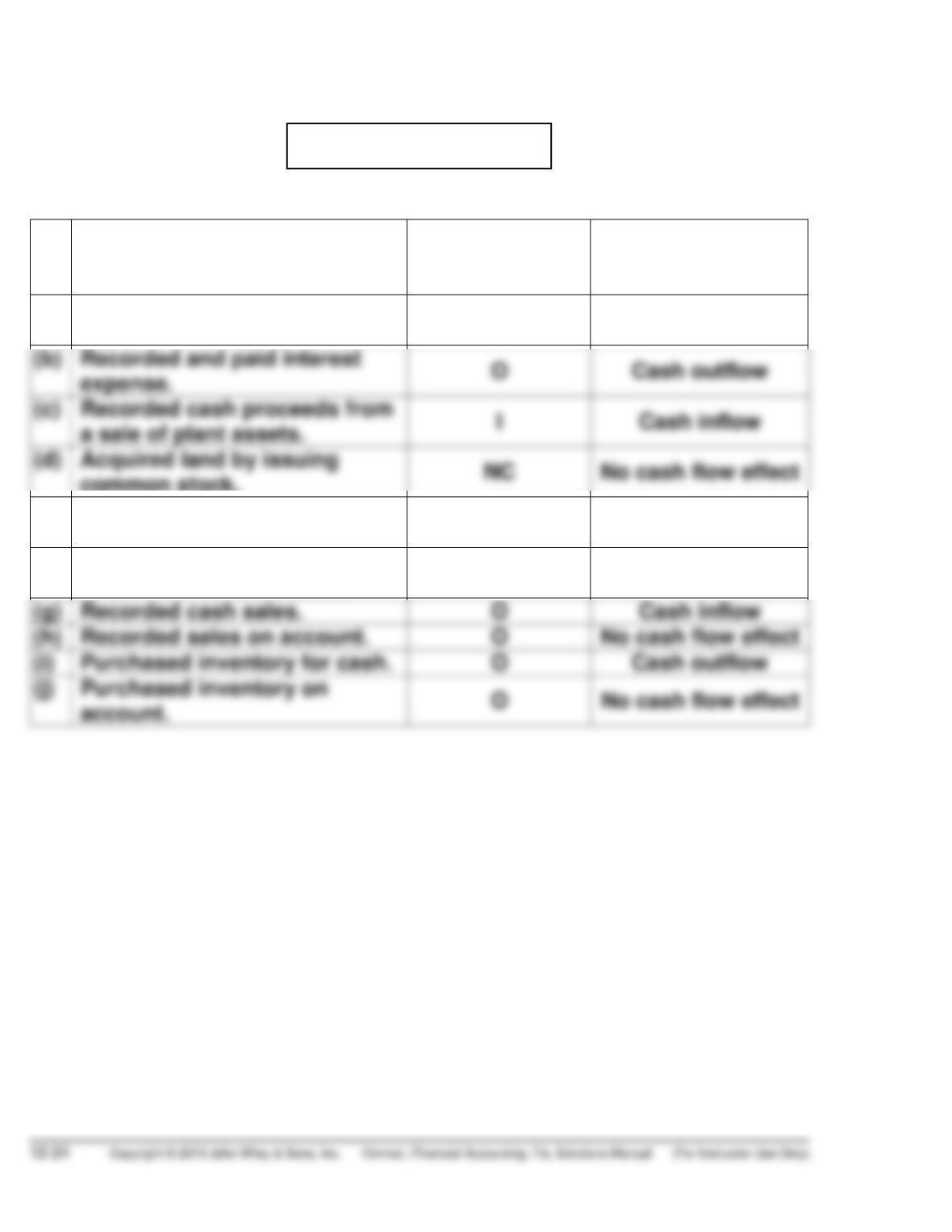

PROBLEM 12-1A

Transaction

SCF Activity

Affected

Cash Inflow,

Outflow, or No

Effect?

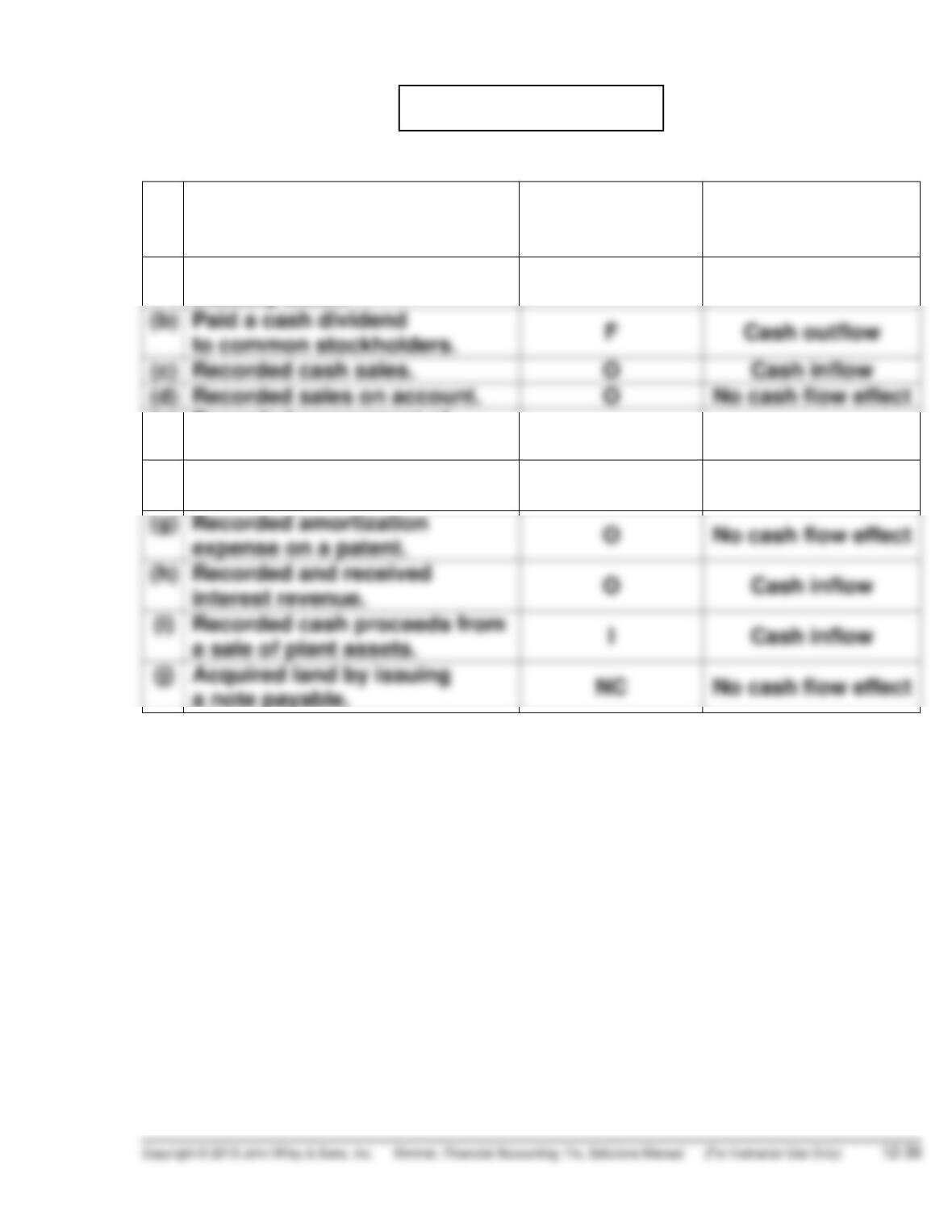

(a) Recorded depreciation

expense on the plant assets. O No cash flow effect

common stock. NC No cash flow effect

(e) Paid a cash dividend

to preferred stockholders. F Cash outflow

(f) Paid a cash dividend

to common stockholders. F Cash outflow

PROBLEM 12-2A

(a) Net income can be determined by analyzing the retained earnings

account.

Retained earnings beginning of year ……………………… $270,000

Add: Net income (plug) …………………………………………. 58,800*

(b) Cash inflow from the issue of stock was $12,000 ($160,800 – $140,000 –

$8,800).

Common Stock

140,000

(c) Both of the above activities (issue of common stock and payment of

PROBLEM 12-3A

PAXSON COMPANY

Partial Statement of Cash Flows

For the Year Ended November 30, 2014

Cash flows from operating activities

Net income ……………………………………………………. $1,750,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………… $ 110,000

Decrease in accounts receivable …………… 380,000

*PROBLEM 12-4A

PAXSON COMPANY

Partial Statement of Cash Flows

For the Year Ended November 30, 2014

Cash flows from operating activities

Cash receipts from customers ……… $7,980,000 (1)

Less cash payments:

Computations:

(1) Cash receipts from customers

Sales …………………………………………………………. $7,600,000

Add: Decrease in accounts receivable ………. 380,000

(3) Cash payments for operating expenses

Operating expenses, exclusive

of depreciation …………………………. $1,040,000*

Add: Increase in prepaid

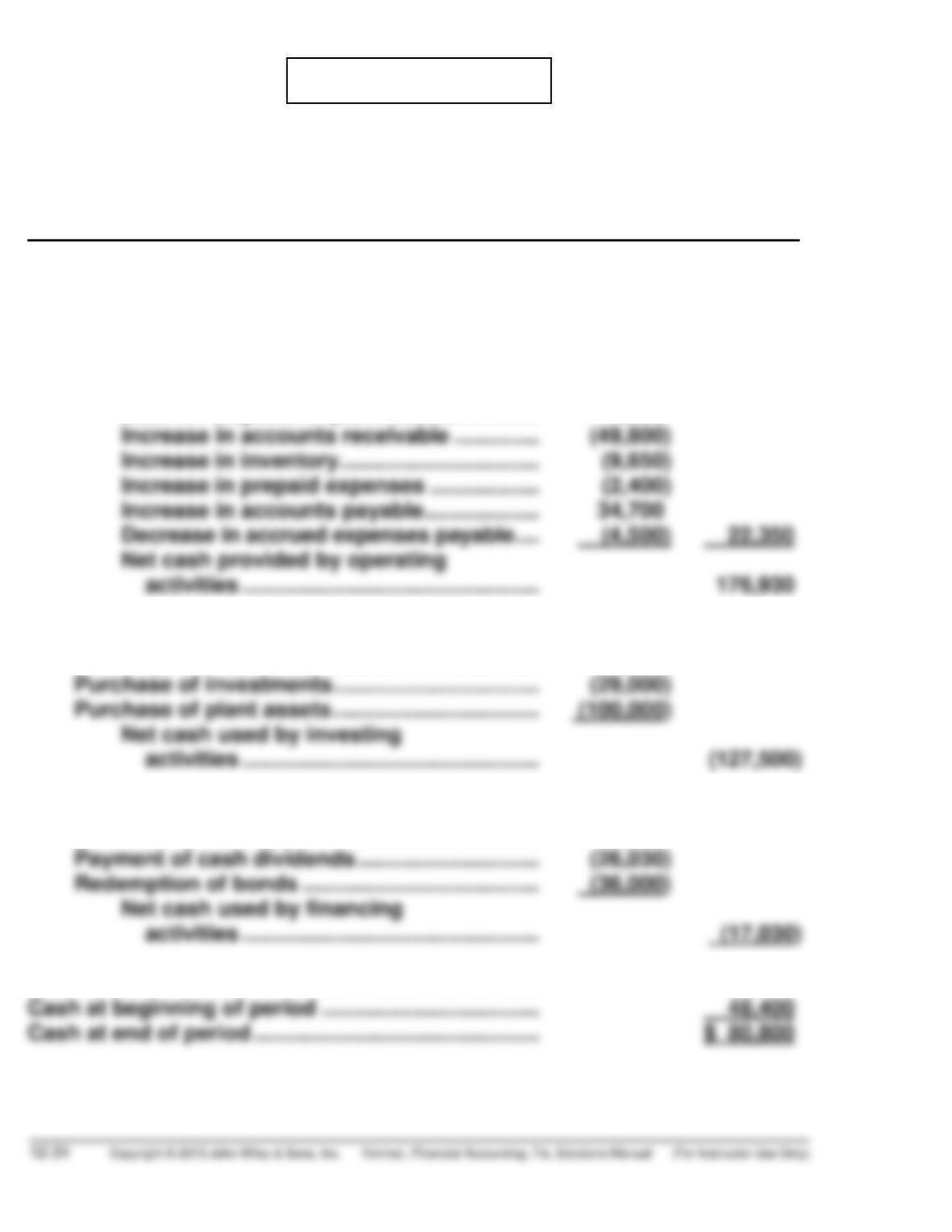

PROBLEM 12-5A

THORNTON COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………… $229,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

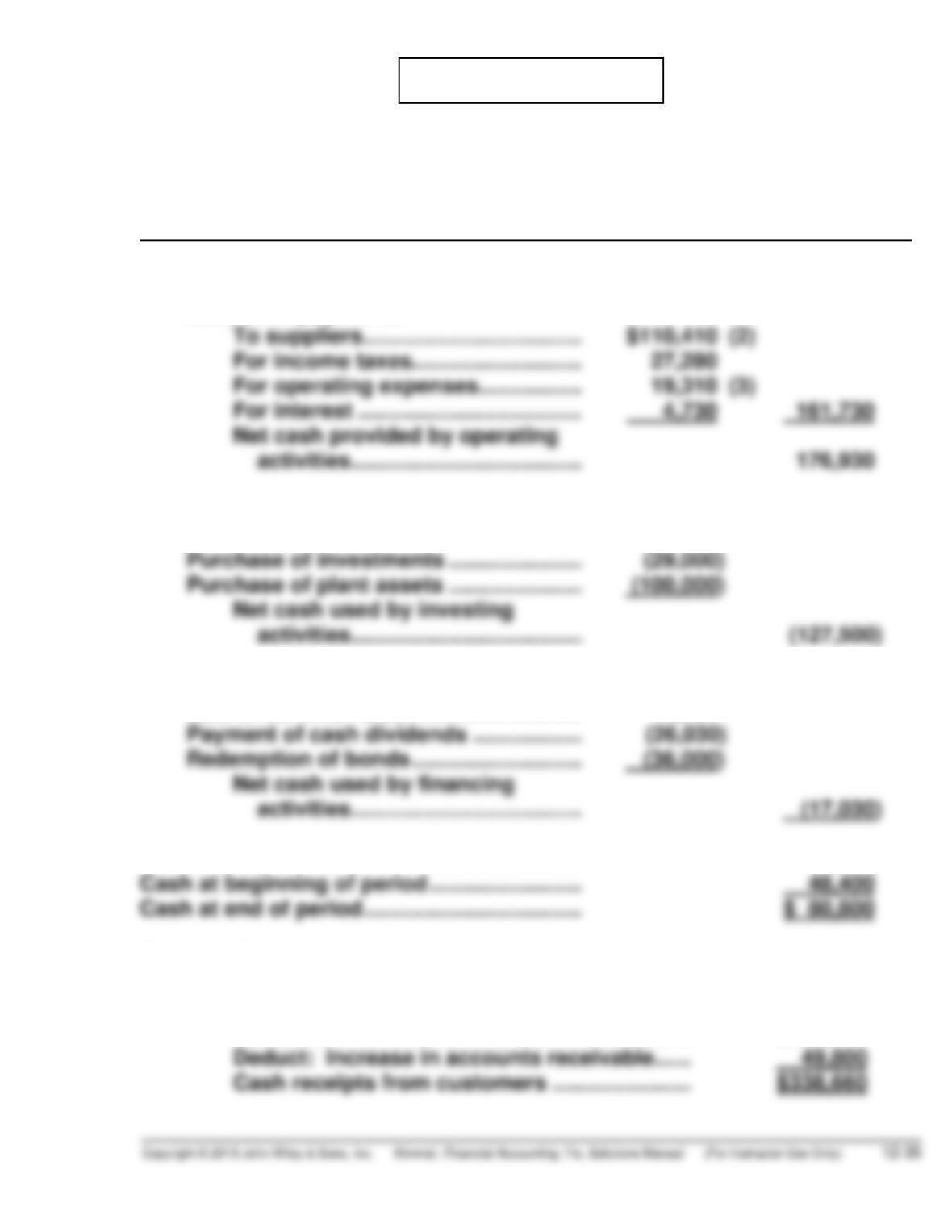

*PROBLEM 12-6A

THORNTON COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ……… $960,000 (1)

Less cash payments:

(1) Cash receipts from customers

Revenues ………………………………………………………………. $970,000

Deduct: Increase in accounts receivable

(2) Cash payments for operating expenses

Operating expenses per income statement …………….. $614,000

(3) Cash payments for income taxes

Income tax expense per income statement……………… $ 56,000

Deduct: Increase in income taxes payable

PROBLEM 12-7A

(a) KURTZEL COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………… $32,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ……………………… $17,500

Cash flows from investing activities

Sale of equipment ………………………………… 8,500

Cash flows from financing activities

Issuance of common stock …………………… 4,000

Net increase in cash …………………………………… 15,000

PROBLEM 12-7A (Continued)

(b) 1. $38,500

[Per Part (a)] ÷$23,000* + $ 26,000**

2 = 1.57 times

*$15,000 + $8,000 **$19,000 + $7,000

*PROBLEM 12-8A

(a) KURTZEL COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers …… $236,000 (1)

Less cash payments:

To suppliers ………………………. $179,000 (2)

Cash flows from investing activities

Sale of equipment ……………………… 8,500

Cash flows from financing activities

Net increase in cash ………………………… 15,000

Computations:

(1) Cash receipts from customers

Sales ………………………………………………………………. $242,000

*PROBLEM 12-8A (Continued)

(2) Cash payments to suppliers

Cost of goods sold ……………………………………………….. $175,000

(3) Cash payments for operating expenses

Operating expenses ……………………………………………… $ 24,000

(4) Cash payments for income taxes

Income tax expense ……………………………………………… $ 8,000

(b) 1. $38,500

[Per Part (a)] ÷$23,000**+ $26,000***

2 = 1.57 times

PROBLEM 12-9A

ODGERS INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………… $154,580

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………. $46,500

Loss on disposal of plant assets …………. 7,500

Cash flows from investing activities

Sale of plant assets ……………………………………. 1,500

Cash flows from financing activities

Sale of common stock ……………………………….. 45,000

Net increase in cash …………………………………………. 32,400

*PROBLEM 12-10A

ODGERS INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers …………. $338,660 (1)

Less cash payments:

Cash flows from investing activities

Sale of plant assets …………………………. 1,500

Cash flows from financing activities

Sale of common stock ……………………… 45,000

Net increase in cash ……………………………….. 32,400

Computations:

(1) Cash receipts from customers

Sales ………………………………………………………… $388,460

*PROBLEM 12-10A (Continued)

(2) Cash payments to suppliers

Cost of goods sold ………………………………………………… $135,460

Add: Increase in inventory ……………………………………. 9,650

(3) Cash payments for operating expenses

Operating expenses exclusive of

depreciation ………………………………………. $12,410

Add: Increase in prepaid expenses …………… $2,400

Decrease in accrued expenses

PROBLEM 12-11A

YANIK COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………… $ 37,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………….. $42,000

Loss on disposal of plant assets …………….. 2,000

Cash flows from investing activities

Sale of land ($130,000 + $40,000 – $145,000) ….. 25,000

Net increase in cash …………………………………………….. 23,000

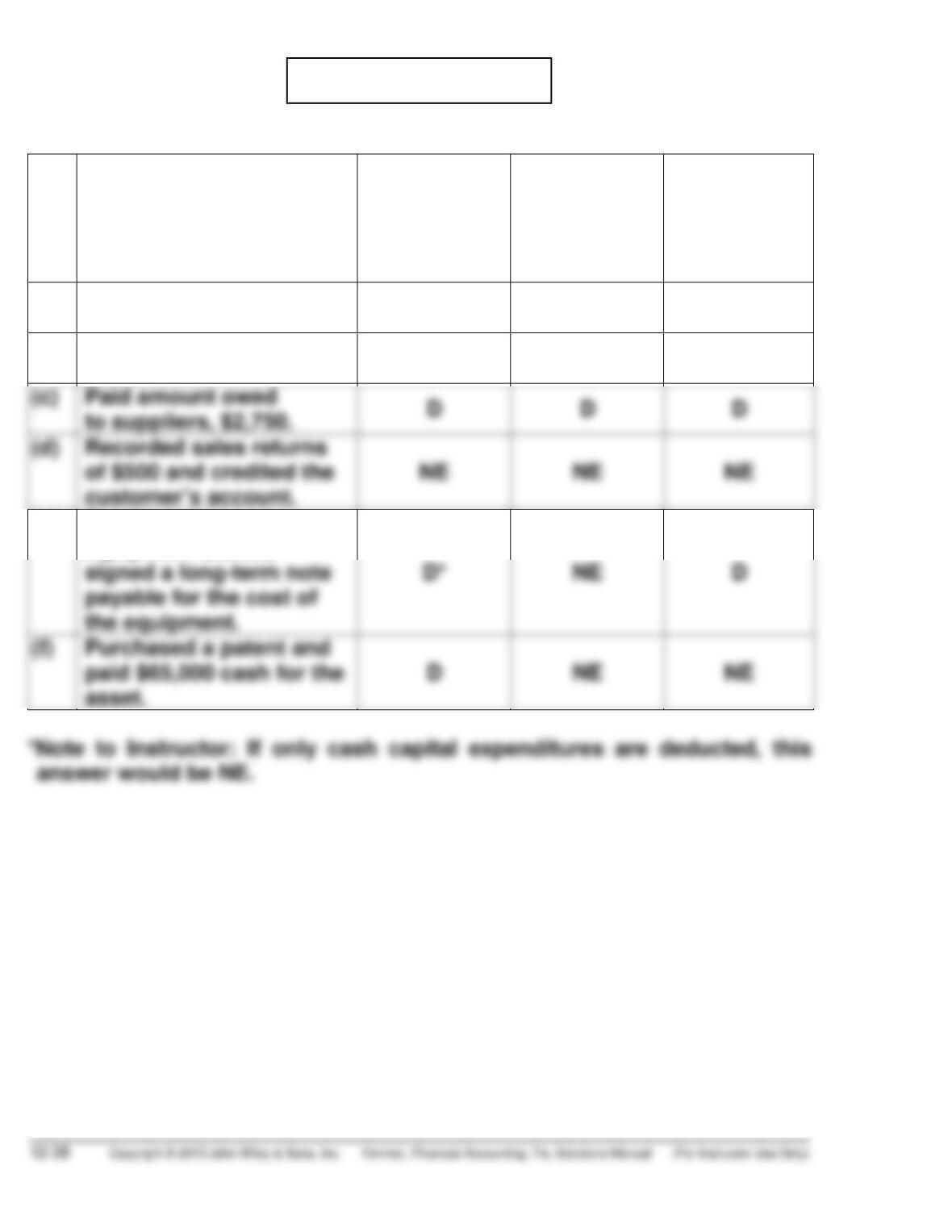

PROBLEM 12-12A

Transaction

Free Cash

Flow

($125,000)

Current

Cash Debt

Coverage

Ratio

(0.5 times)

Cash Debt

Coverage

Ratio

(0.3 times)

(a) Recorded credit sales

$2,500. NE NE NE

(b) Collected $1,900 owed by

customers. I I I

(e) Purchased new

equipment $5,000;

PROBLEM 12-1B

Transaction SCF Activity

Affected

Cash Inflow,

Outflow, or No

Effect?

(a) Purchased shares of common

treasury stock. F Cash outflow

(e) Recorded prepayment of

insurance expense. O Cash outflow

(f) Purchased supplies on

account. O No cash flow effect

a note payable. NC No cash flow effect

PROBLEM 12-2B

(a) Cash inflows (outflows) related to plant assets 2014:

Equipment purchase ……………………… ($85,000)

Accumulated depreciation removed from accounts for sale of equipment

Accumulated Depreciation—

Equipment

96,000

Note to instructor—some students may find journal entries helpful in under-

standing this exercise.

Equipment ……………………………………………………………. 85,000

Cash ……………………………………………………………… 85,000

(b) Equipment purchase Investing activities (outflow)