CHAPTER 12

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 12-1B

(a) Jan. 1 Cash …………………………………………………… 10,000

Accounts Receivable …………………………... 18,000

Inventory …………………………………………….. 38,000

Equipment …………………………………………… 35,000

Allowance for Doubtful

(b) Jan. 1 Cash …………………………………………………… 3,500

Utech, Capital ……………………………….. 3,500

PROBLEM 12-1B (Continued)

(c) COMMANDER COMPANY

Balance Sheet

January 1, 2017

Assets

Current assets

Cash

($10,000 + $8,000 + $3,500 + $16,000) … $ 37,500

Accounts receivable

Property, plant, and equipment

Equipment ($35,000 + $18,000) ……………… 53,000

Total assets ……………………………………………….. $195,000

Liabilities and Owners’ Equity

Current liabilities

Notes payable ……………………………………… $ 20,000

Accounts payable ($30,000 + $40,000) …… 70,000

PROBLEM 12-2B

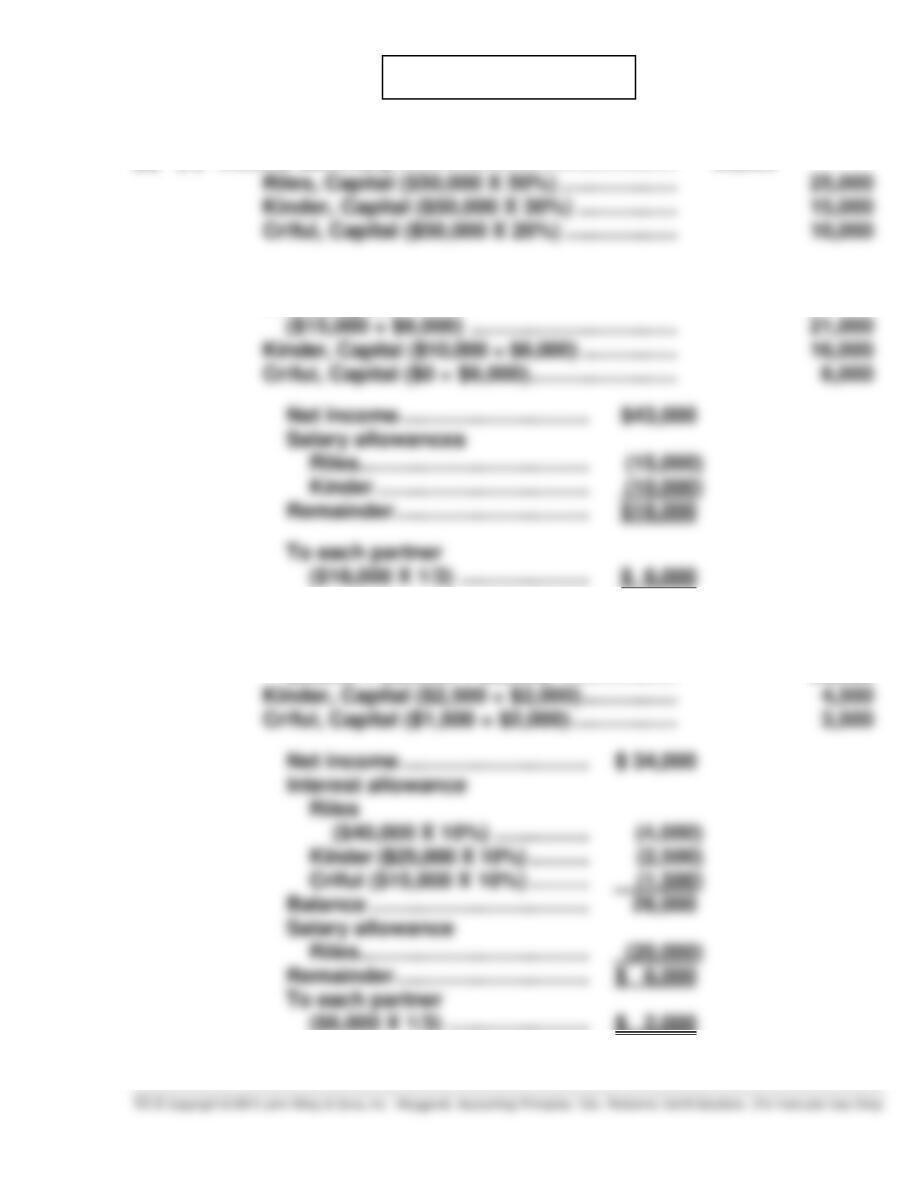

(a) (1) Income Summary ………………………………………… 50,000

Riles, Capital ($50,000 X 50%) ……………….. 25,000

Kinder, Capital ($50,000 X 30%) …………….. 15,000

Crifui, Capital ($50,000 X 20%) ………………. 10,000

(2) Income Summary ………………………………………… 43,000

Riles, Capital

(3) Income Summary ………………………………………… 34,000

Riles, Capital

($4,000 + $20,000 + $2,000) ……………….. 26,000

Kinder, Capital ($2,500 + $2,000) ……………. 4,500

Crifui, Capital ($1,500 + $2,000) ……………… 3,500

Net income ………………………….. $ 34,000

Interest allowance

PROBLEM 12-2B (Continued)

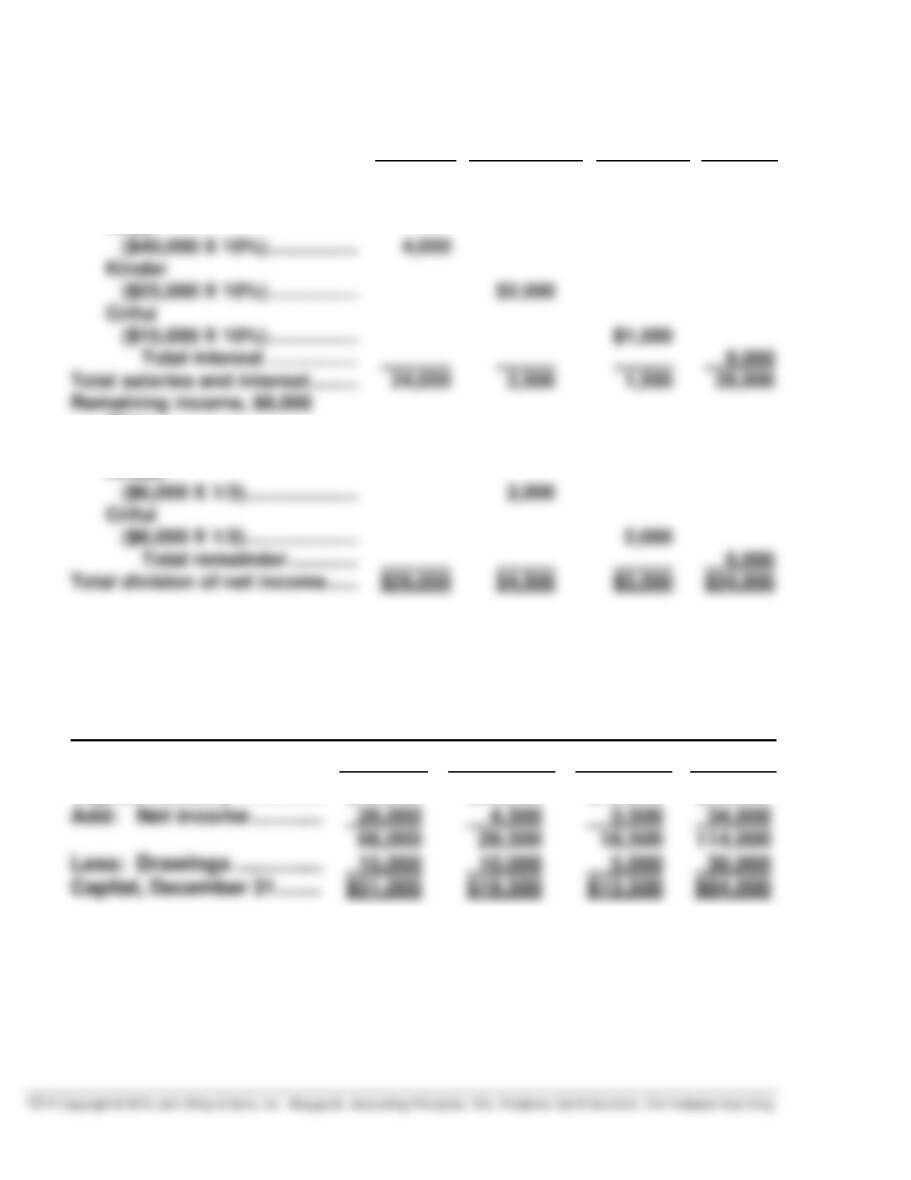

(b)

DIVISION OF NET INCOME

Riles

Kinder

Crifui

Total

Salary allowance ……………………

Interest allowance on capital

Total salaries and interest ………

Remaining income, $6,000

Riles

($6,000 X 1/3) …………………

Kinder

($6,000 X 1/3) …………………

$20,000

24,000

2,000

2,500

2,000

(

1,500

$20,000

28,000

(c) RKC COMPANY

Partners’ Capital Statement

For the Year Ended December 31, 2017

Riles

Kinder

Crifui

Total

Capital, January 1 …………..

Add: Net income …………..

$40,000

26,000

$25,000

4,500

$15,000

3,500

$80,000

34,000

PROBLEM 12–3B

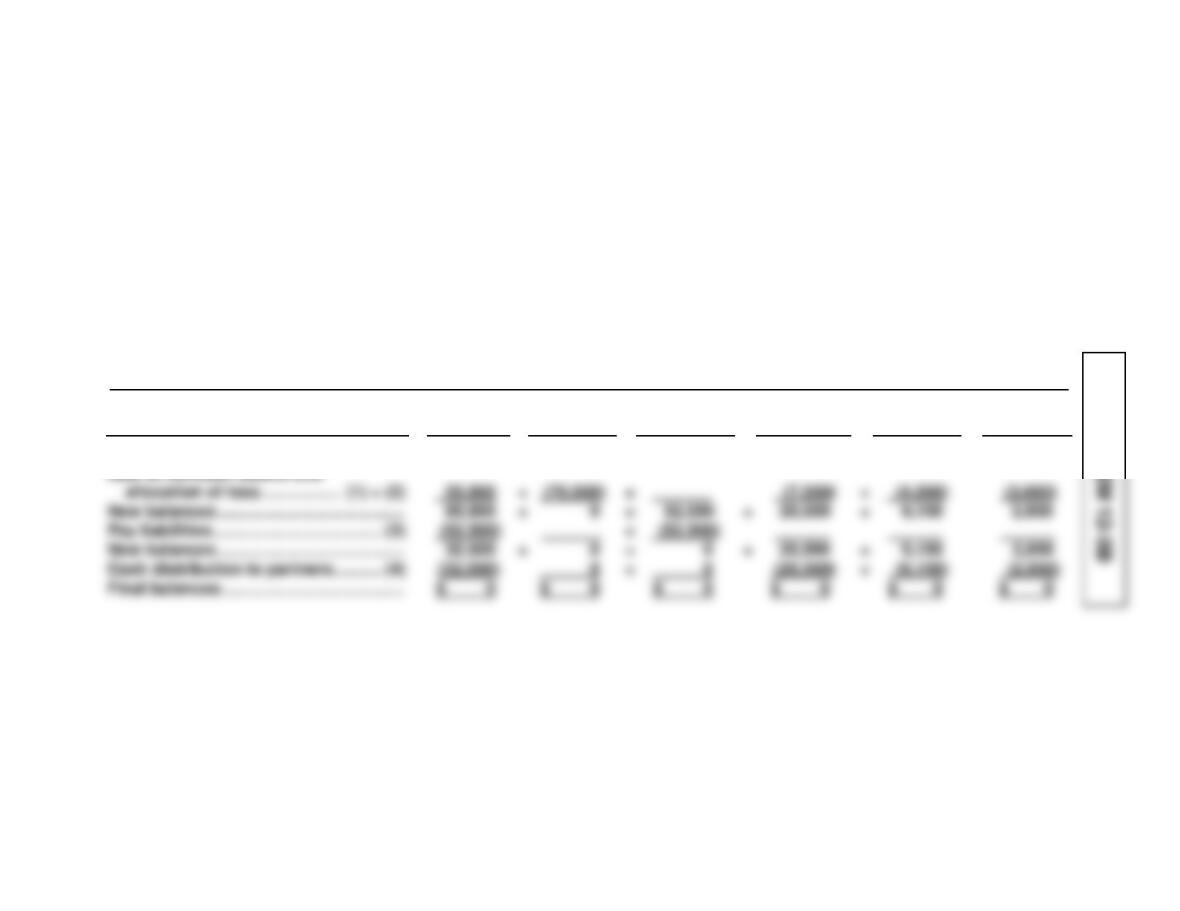

(a) NEWMAN COMPANY

Schedule of Cash Payments

Item

Cash

+

Noncash

Assets

=

Liabilities

+

Mallory,

Capital

+

Bosco,

Capital

+

Renteria,

Capital

Balances before liquidation ……………..

Sale of noncash assets and

allocation of loss …………….. (1) + (2)

$30,000)

55,000)

+

+

$70,000)

(70,000)

=

=

$52,500)

+

$28,000)

(7,500)

+

+

$13,650)

(4,500)

$5,850)

(3,000)

PROBLEM 12-3B (Continued)

(b) (1)

Apr. 30 Cash …………………………………………………. 55,000

Allowance for Doubtful Accounts ………. 2,000

Accumulated Depreciation …………………. 8,000

Noncash assets (net) ………… $70,000

Sale proceeds ………………….. 55,000

(2)

30 Mallory, Capital ($15,000 X 50%) …………. 7,500

Bosco, Capital ($15,000 X 30%) ………….. 4,500

(3)

30 Notes Payable …………………………………… 20,000

Accounts Payable ……………………………… 30,000

(4)

30 Mallory, Capital ($28,000 – $7,500) ……… 20,500

Bosco, Capital ($13,650 – $4,500) ……….. 9,150

PROBLEM 12-3B (Continued)

(c)

Cash

Bosco, Capital

Bal. 30,000

4/30 (1) 55,000

4/30 (3) 52,500

4/30 (4) 32,500

4/30 (2) 4,500

4/30 (4) 9,150

Bal. 13,650

Bal. –0–

Bal. –0–

Mallory, Capital

Renteria, Capital

Bal. –0–

Bal. –0–

4/30 (2) 7,500

Bal. 28,000

4/30 (2) 3,000

Bal. 5,850

*PROBLEM 12-4B

(a) (1) Giger, Capital …………………………………………….. 5,000

Edelman, Capital …………………………………. 5,000

(3) Cash …………………………………………………………. 29,000

Younger, Capital ($5,000 X 5/10) …………………. 2,500

Beyer, Capital ($5,000 X 3/10) ……………………… 1,500

Giger, Capital ($5,000 X 2/10) ……………………… 1,000

Edelman, Capital …………………………………. 34,000

Total capital of existing

partnership ……………….. $56,000

Investment by Edelman …. 29,000

Total capital of new

partnership ……………….. $85,000

(4) Cash …………………………………………………………. 24,000

Younger, Capital ($8,000 X 5/10) …………… 4,000

Beyer, Capital ($8,000 X 3/10) ………………. 2,400

*PROBLEM 12-4B (Continued)

Edelman’s capital credit

($80,000 X 20%) ……………. $16,000

(b) Total capital after admission ($25,000 ÷ 25%) ………………… $100,000

Total capital before admission ……………………………………… 56,000

*PROBLEM 12-5B

(a) (1) Piper, Capital …………………………………………….. 28,000

Dunlap, Capital……………………………………. 14,000

Yevak, Capital …………………………………….. 14,000

(2) Piper, Capital …………………………………………….. 28,000

Yevak, Capital …………………………………….. 28,000

(4) Piper, Capital …………………………………………….. 28,000

Dunlap, Capital ($9,000 X 6/9) ………………. 6,000

Yevak, Capital ($9,000 X 3/9) ………………… 3,000

Cash …………………………………………………… 19,000

(b) (1) Yevak capital after withdrawal………………………………… $57,000

Yevak capital before withdrawal …………………………….. 51,000

Bonus to Yevak …………………………………………………….. $ 6,000