CHAPTER 12

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 12-1B

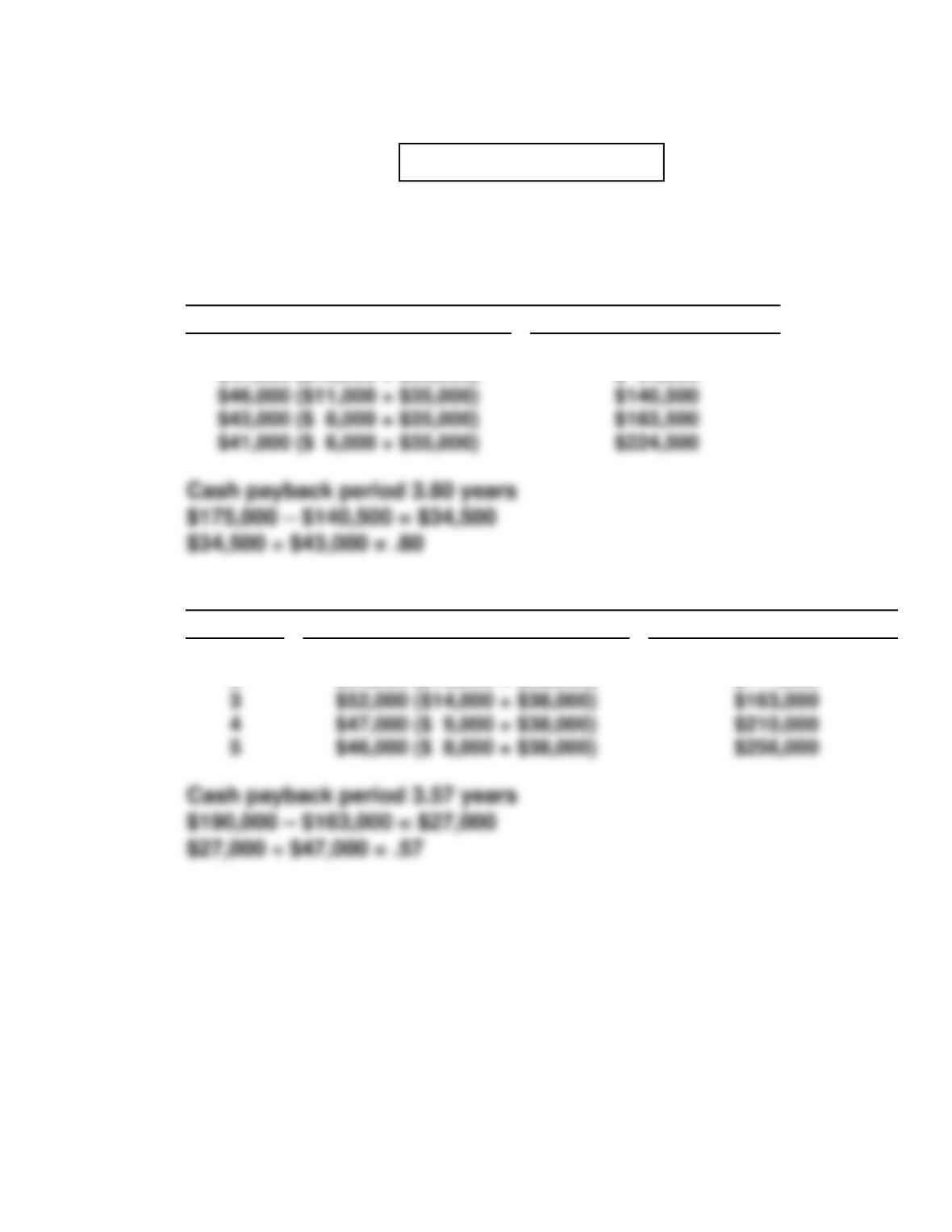

(a) Project Mary $140,000 ÷ [($10,000 + $28,000)] = 3.68 years

Project Winnie

Cash Flow

Cumulative Cash Flow

$47,500 ($12,500 + $35,000)

$47,000 ($12,000 + $35,000)

$ 47,500

$ 94,500

Project Sarah

Year

Cash Flow

Cumulative Cash Flow

1

2

$57,000 ($19,000 + $38,000)

$54,000 ($16,000 + $38,000)

$ 57,000

$111,000

PROBLEM 12-1B (Continued)

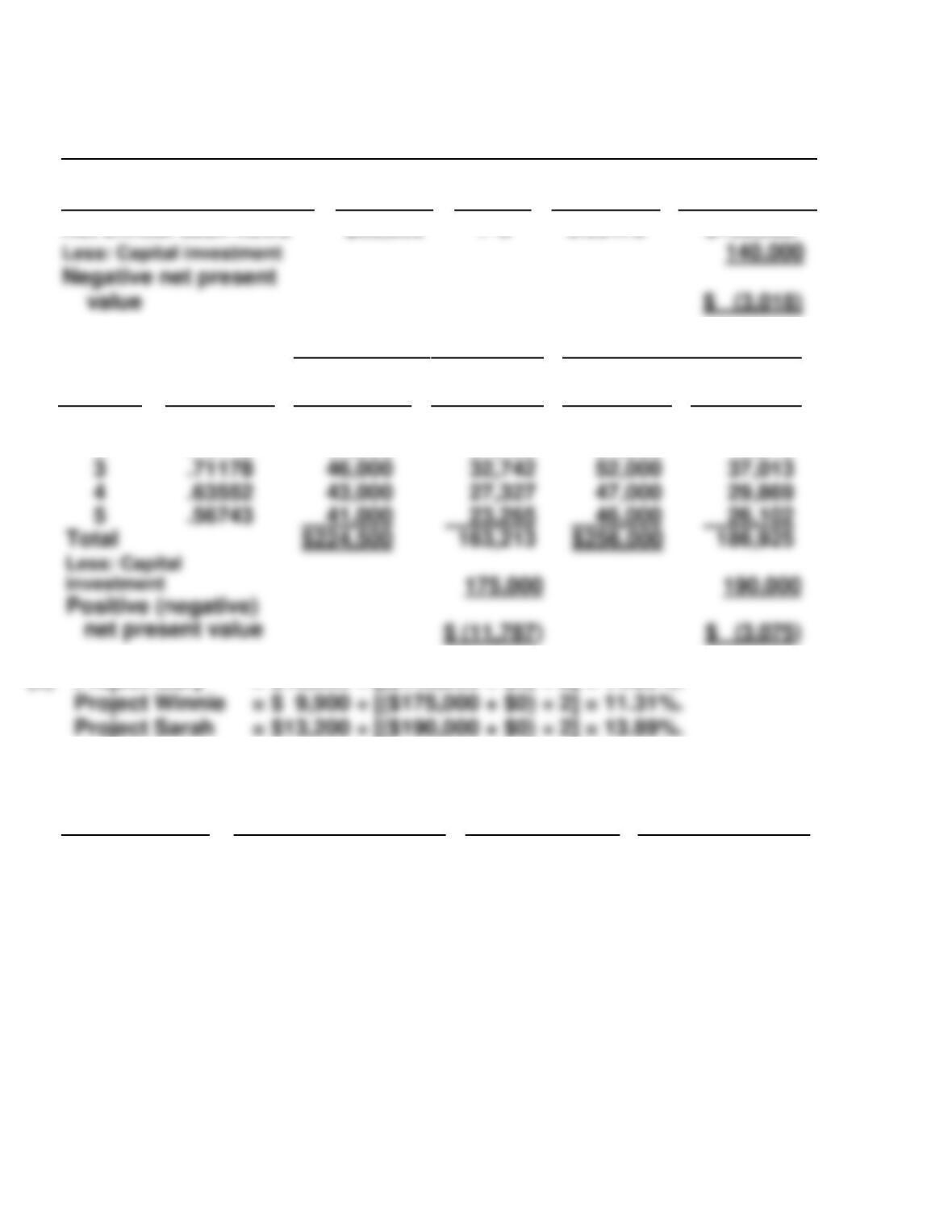

(b) Project Mary

Item

Amount

Years

PV Factor

Present

Value

Net annual cash flows

$38,000

1–5

3.60478

$136,982

Project Winnie

Project Sarah

Year

Discount

Factor

Cash

Flow

PV

Cash

Flow

PV

Total

$224,500

46,000

1

2

.89286

.79719

$ 47,500

47,000

$ 42,411

37,468

$ 57,000

54,000

$ 50,893

43,048

(c) Project Mary = $10,000 ÷ [($140,000 + $0) ÷ 2] = 14.29%.

(d)

Project

Cash Payback

Net

Present Value

Annual

Rate of Return

Mary

Winnie

Sarah

2

3

1

1

3

2

1

3

2

The best project is Mary, but even Mary should not be recommended,

because the net present value is negative.

PROBLEM 12-2B

(a)

(1)

Annual

Net Income

(2)

Annual

Cash Inflow

Sales

Expenses

Drivers’ salaries

*$144,000*

43,000

$144,000

43,000

(b) 1. Cash payback period = $90,000 ÷ $59,000 = 1.53 years.

(c) Present value of annual cash inflows ($59,000 X 2.28323*) = $134,711

Capital investment = (90,000)

Net present value = $ 44,711

(d) The computations show that the commuter service is a good

investment for these reasons: (1) annual net income will be $29,000,

PROBLEM 12-3B

(a)

(1) Option A

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

a$32,000a

X

4.23054

=

($135,377)

(2) Profitability index = $96,624/$100,000 = .97

(3) The internal rate of return can be approximated by finding the discount

rate that results in a net present value of approximately zero. This is

accomplished with a 10% discount rate.

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

Les: Capital investment

(1) Option B

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Less: Capital investment

160,000

Present value of net annual cash inflows

b$36,000b

X

4.23054

=

$152,299

(2) Profitability index = $165,130/$160,000 = 1.03

PROBLEM 12-3B (Continued)

(3) Internal rate of return on Option B is 12%, as calculated below:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

b$36,000b

X

4.11141

=

$148,011

(b) Option A has a lower net present value than Option B, and also a lower

profitability index and internal rate of return. Therefore, Option B is the

Less: Capital investment

PROBLEM 12-4B

(a) The net present value based on the original estimates is as follows:

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

$ 9,600

X

5.33493

=

($ 51,215

(b) The net present value based on the revised estimates is as follows:

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash inflows

$14,500*

X

5.33493

=

($77,356)

(c) The present value of the intangible benefits was $26,141 (the increase

in the net present value from a negative $11,102 to a positive $15,039).

Brad’s estimates of the value of these intangible benefits may be

PROBLEM 12-5B

(a) Using the original estimates, the net present value is calculated as

follows:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

Present value of salvage value

a$130,000a

700,000

X

X

7.46944

.10367

=

=

$ 971,027

72,569

1,043,596

(b) Using the revised estimates, the net present value is calculated as

follows:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Less: Capital investment

Net present value

Present value of net annual cash inflows

b$ 62,000b

X

7.46944

=

$463,105

Net present value

$ 493,596

PROBLEM 12-5B (Continued)

(c) Using the original estimates, but a 15% discount rate, the net present

value is calculated as follows:

Cash

Flows

X

15% Discount

Factor

=

Present

Value

Present value of net annual cash inflows

Present value of salvage value

c$130,000c

700,000

X

X

6.25933

.06110

=

=

$813,713

42,770

(d) The internal rate of return can be determined by calculating the discount

rate that results in a net present value of approximately zero. In this

case the internal rate of return was approximately 15%.

Cash

Flows

X

15% Discount

Factor

=

Present

Value

Present value of salvage value

Less: Capital investment

=

Present value of net annual cash inflows

$ 65,000

X

3.35216

=

$217,890

Less: Capital investment