*EXERCISE 12-14

1. N. Rice, Capital …………………………………………………. 60,000

B. Higgins, Capital ……………………………………………. 2,500

J. Mayo, Capital ………………………………………………… 1,500

Cash …………………………………………………………. 64,000

2. N. Rice, Capital …………………………………………………. 60,000

B. Higgins, Capital ……………………………………… 5,000

J. Mayo, Capital …………………………………………. 3,000

Cash …………………………………………………………. 52,000

*EXERCISE 12-15

(a) Cash ……………………………………………………………. 88,000

Garrett, Capital ($288,000a X 25%) ………….. 72,000

Foss, Capital ($16,000 X 50%) ………………… 8,000

(b) Foss, Capital ……………………………………………….. 100,000

Albertson, Capital ($10,000 X 3/5) ………………….. 6,000

SOLUTIONS TO PROBLEMS

PROBLEM 12-1A

(a) Jan. 1 Cash …………………………………………………… 14,000

Accounts Receivable …………………………... 17,500

Inventory ……………………………………………. 28,000

Equipment ………………………………………….. 25,000

1 Cash …………………………………………………… 12,000

Accounts Receivable …………………………... 26,000

Inventory ……………………………………………. 20,000

Equipment ………………………………………….. 15,000

(b) Jan. 1 Cash …………………………………………………… 5,000

Sorensen, Capital …………………………. 5,000

PROBLEM 12-1A (Continued)

(c) SOLU COMPANY

Balance Sheet

January 1, 2017

Assets

Current assets

Cash

($14,000 + $12,000 + $5,000 + $19,000) …. $ 50,000

Accounts receivable

($17,500 + $26,000) ……………………………… $43,500

Less: Allowance for doubtful accounts

Liabilities and Owners’ Equity

Current liabilities

Notes payable ($18,000 + $15,000) …………. $ 33,000

Accounts payable ($22,000 + $31,000) …… 53,000

Total current liabilities …………………… 86,000

Owners’ equity

PROBLEM 12-2A

(a) (1) Income Summary ………………………………………….. 30,000

(2) Income Summary ………………………………………….. 40,000

A. Niensted, Capital ($15,000 + $5,000) …….. 20,000

G. Bolen, Capital ($10,000 + $5,000) …………. 15,000

K. Sayler, Capital ($0 + $5,000) ………………… 5,000

(3) Income Summary ………………………………………….. 19,000

A. Niensted, Capital

($4,800 + $15,000 – $2,100) …………………. 17,700

G. Bolen, Capital ($3,000 – $2,100) …………… 900

K. Sayler, Capital ($2,500 – $2,100) ………….. 400

Net income ………………………. $19,000

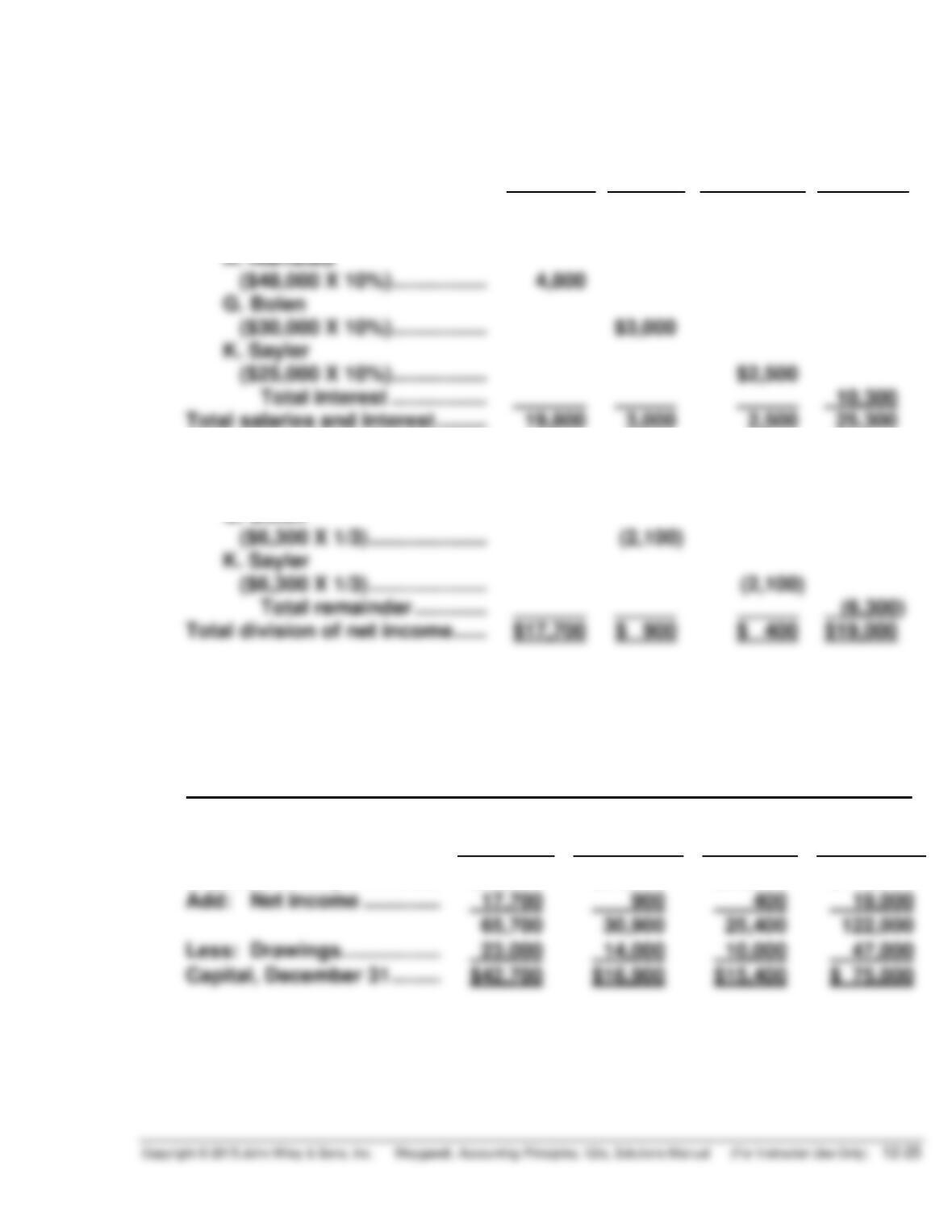

Interest allowance

Niensted ($48,000 X 10%) . (4,800)

PROBLEM 12-2A (Continued)

(b)

DIVISION OF NET INCOME

Art

Niensted

Greg

Bolen

Krista

Sayler

Total

Salary allowance ……………………

Interest allowance on capital

A. Niensted

($48,000 X 10%)……………..

G. Bolen

Remaining deficiency, ($6,300)

A. Niensted

($6,300 X 1/3) …………………

G. Bolen

$15,000

4,800

(

(2,100)

(

$15,000

(

(c) NBS COMPANY

Partners’ Capital Statement

For the Year Ended December 31, 2017

Art

Niensted

Greg

Bolen

Krista

Sayler

Total

Capital, January 1 ……………

$48,000

$30,000

$25,000

$103,000

PROBLEM 12-3A

(a) (1)

Cash ………………………………………………………………… 51,000

Allowance for Doubtful Accounts ………………………. 1,000

Accumulated Depreciation—Equipment …………….. 5,500

(2)

A. Jamison, Capital ($23,000 X 5/10) ………………….. 11,500

(3)

Notes Payable ………………………………………………….. 13,500

Accounts Payable …………………………………………….. 27,000

(4)

Cash ………………………………………………………………… 1,600

P. Roper, Capital ($4,600 – $3,000) ………………. 1,600

(5)

A. Jamison, Capital ($33,000 – $11,500) ……………… 21,500

PROBLEM 12-3A (Continued)

(b)

Cash

A. Jamision, Capital

Bal. –0–

Bal. –0–

Bal. 27,500

(3) 44,500

(2) 11,500

Bal. 33,000

S. Moyer, Capital

P. Roper, Capital

(2) 6,900

Bal. 21,000

(2) 4,600

Bal. 3,000

(c) (1) A. Jamison, Capital ($1,600 X 5/8) ……………….. 1,000

(2) A. Jamison, Capital ($21,500 – $1,000) ………… 20,500

*PROBLEM 12-4A

(a) (1) J. Pinkston, Capital ……………………………………. 9,000

J. Terrell, Capital …………………………………. 9,000

(2) C. Lamar, Capital ……………………………………….. 16,000

J. Terrell, Capital …………………………………. 16,000

(3) Cash …………………………………………………………. 62,000

G. Donley, Capital (50% X $8,000) ………… 4,000

(4) Cash …………………………………………………………. 42,000

G. Donley, Capital ($6,000 X 50%) ……………….. 3,000

C. Lamar, Capital ($6,000 X 40%) ………………… 2,400

*PROBLEM 12-4A (Continued)

Terrell’s capital credit

($160,000 X 30%) ………….. $48,000

(b) (1) Total capital after admission ($32,000 ÷ 20%) ………….. $160,000

Total capital before admission …………………………..…… 118,000

(2) Decrease in Lamar’s equity ($48,000 – $32,000) ………… $ 16,000

*PROBLEM 12-5A

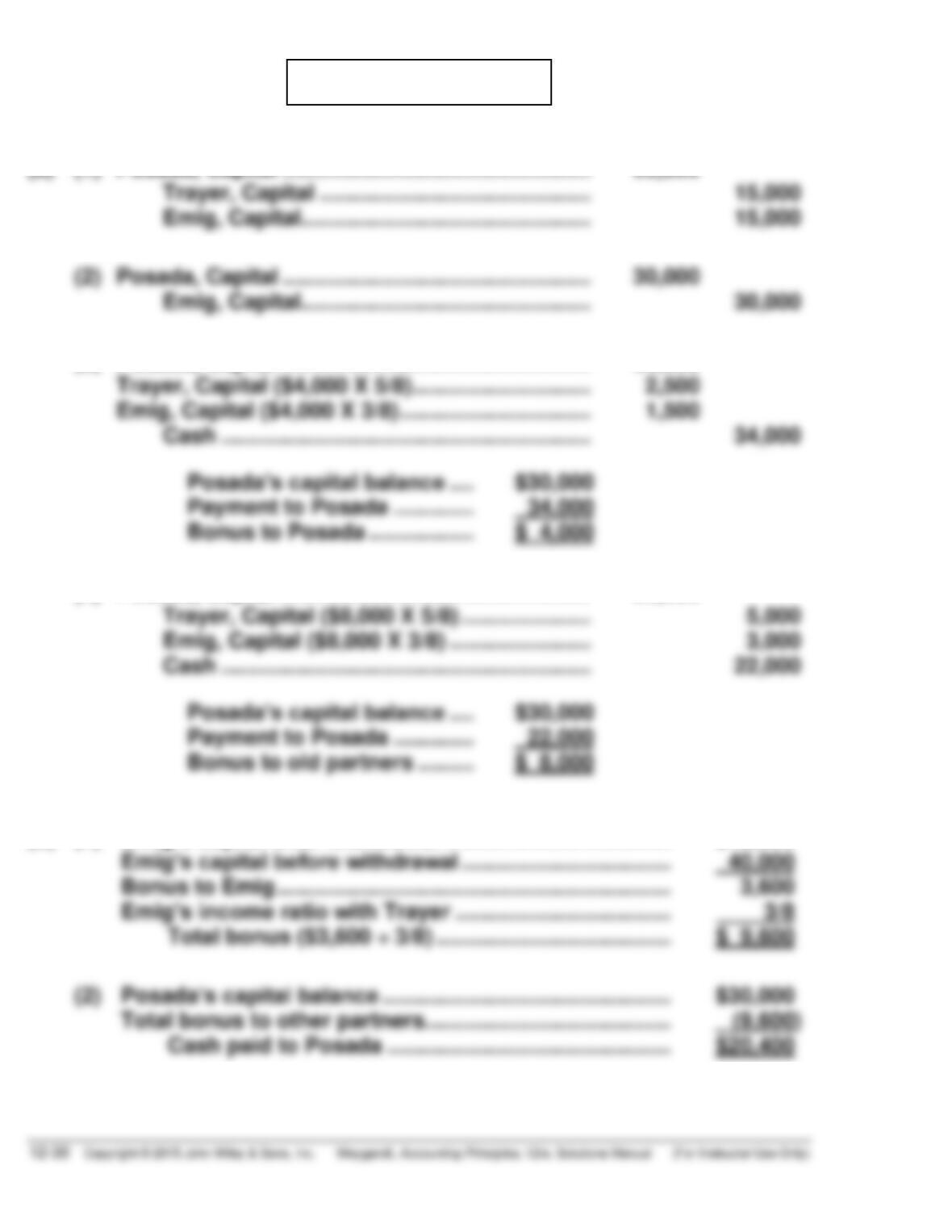

(a) (1) Posada, Capital ………………………………………….. 30,000

Trayer, Capital …………………………………….. 15,000

Emig, Capital ……………………………………….. 15,000

(3) Posada, Capital ………………………………………….. 30,000

Trayer, Capital ($4,000 X 5/8) ……………………….. 2,500

Emig, Capital ($4,000 X 3/8) …………………………. 1,500

Cash …………………………………………………… 34,000

(4) Posada, Capital ………………………………………….. 30,000

Trayer, Capital ($8,000 X 5/8) ………………… 5,000

Emig, Capital ($8,000 X 3/8) ………………….. 3,000

Cash …………………………………………………… 22,000

(b) (1) Emig’s capital after withdrawal ………………………………. $43,600

Emig’s capital before withdrawal ……………………………. 40,000

BYP 12-1 REAL-WORLD FOCUS

Students’ answers will depend upon the firm selected and the timing of

their exploration.

BYP 12-2 DECISION MAKING ACROSS THE ORGANIZATION

(a) The major disadvantages of a partnership are mutual agency, limited

life, and unlimited liability. Mutual agency means that each partner acts on

behalf of the partnership when engaging in partnership business. The act

of any partner is binding on all other partners, even when the partners

act beyond the scope of their authority, so long as the act appears to be

(b) The written partnership agreement, often referred to as the articles of

co-partnership, is needed. It should contain such basic information as

the name and principal location of the firm, the purpose of the business,

(c) The best approach would be to give Stephen an interest allowance for

(d) The computer equipment should be depreciated on the books of

the partnership, not on Stephen’s personal tax return. The computer is

owned by the partnership, and only Stephen’s share of net income

should be reported on his tax return. The computer would be reported

at its fair value when invested in the partnership, less the accumulated

depreciation as of the end of the taxable year.

BYP 12-2 (Continued)

(e) To facilitate the payment from partnership assets of the deceased

partner’s equity, some companies obtain life insurance policies on

BYP 12-3 COMMUNICATION ACTIVITY

To: Ronald Hrabik

Meg Percival

From: Your Accountant

Subject: Partnership Agreement for Pasta Shop

There are many important issues that should be included in your partnership

agreement. Prior to our meeting next Tuesday, in my office, it would be helpful

for you to consider the following matters.

1. Facts about the business; i.e., name, location, purpose, and date of

inception.

2. Facts about the partners; i.e., the name and address of each partner,

the beginning capital contribution of each partner, and the rights and

duties of partners with respect to: (a) making business decisions, (b) active

participation in the partnership (full/part-time), and (c) allowances for

vacations and sick leave.

BYP 12-3 (Continued)

5. Procedures for submitting disputes to arbitration. Inevitably, disagreements

will occur between partners. The partnership contract should provide a

framework for resolving them. You may want to include some or all of the

outside parties mentioned above in an arbitration committee.

7. Rights and duties of surviving partners. The death of a partner is often a

traumatic experience. Thus, it is advisable that the partnership agreement

specify the responsibilities of the surviving partners, assuming the

business is continued, or if the business is terminated. Also, procedures

should be included for determining the deceased partner’s equity in the

firm. The procedures might include an audit of the financial statements

and a revaluation of assets by an independent appraisal firm.

BYP 12-4 ETHICS CASE

(a) The stakeholders in this situation are Alexandra and Kellie.

(b) The consequences of Alexandra’s actions are that they cause significant

differences in the time worked between the partners and in the amount

of drawings made by each partner. Sooner or later, Kellie is going to

become annoyed with Alexandra’s actions and this could cause

friction between the partners.

(c) For the differences in time worked, two changes in the partnership

agreement should be considered. First, Kellie could be given a higher

salary allowance than Alexandra. Second, because Kellie is

contributing more to net income than Alexandra, she could be given a

higher percentage of net income after deducting salary allowances.

BYP 12-5 ALL ABOUT YOU

Given that the students may come up with variety of answers that are

correct, there is no single correct solution to this problem. You may wish to

have a show of hands on each question to see whether any consensus has

developed on any of the questions.