CHAPTER 12

THE REVENUE CYCLE: SALES AND CASH COLLECTIONS

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

12.1 Customer relationship management systems hold great promise, but their usefulness

is determined by the amount of personal data customers are willing to divulge. To

what extent do you think concerns about privacy-related issues affect the use of

CRM systems?

The basic issue concerns the willingness of consumers to divulge the kind of information

12.2 Some products, like music and software, can be digitized. How does this affect each

of the four main activities in the revenue cycle?

Digitized products do not change the four basic business activities of the revenue cycle.

For all products, whether digitized or not, an order must be taken, the product shipped,

the customer billed, and cash collected.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

12.3 Many companies use accounts receivable aging schedules to project future cash

inflows and bad-debt expense. Review the information typically presented in such a

report (see Figure 12-8). Which specific metrics can be calculated from those data

that might be especially useful in providing early warning about looming cash flow

or bad-debt problems?

The accounts receivable aging report shows dollar amounts outstanding by number of

days past due by customer and by invoice. The following metrics can provide useful

early warnings about looming cash flow or bad-debt problems.

• The percentage of total accounts receivable categorized by days past due would alert

management of categories that are increasing. This could also be reported by

12.4 Table 12-1 suggests that restricting physical access to inventory is one way to reduce

the threat of theft. How can information technology help accomplish that objective?

Possibilities include:

• Electronic locks on all entrances and exits to the inventory area.

Accounting Information Systems

12-3

12.5 Invoiceless pricing has been adopted by some large businesses for B2B transactions.

What are the barriers, if any, to its use in B2C commerce?

Many companies are trying to incent their customers to sign up for automatic bill-pay.

12.6 The use of some form of electronic “cash” that would provide the same kind of

anonymity for e-commerce that cash provides for traditional physical business

transactions has been discussed for a long time. What are the advantages and

disadvantages of electronic cash to customers? To businesses? What are some of the

accounting implications of using electronic cash?

Any form of electronic or digital cash has the same audit risks as physical cash:

susceptibility to theft and loss of an audit trail. In addition, digital “cash” also has risks

associated with the durability of the store of value – to what extent can the cash be

recovered if the storage media becomes defective?

Ch. 12: The Revenue Cycle: Sales and Cash Collections

SUGGESTED ANSWERS TO THE PROBLEMS

12.1 Match the term in the left column with its definition in the right column.

1. __d__ CRM system

a. Document used to authorize reducing the balance in a customer

6. __c___ FEDI

f. Method of maintaining accounts receivable that generates one

payments for all sales made the previous month

7. _n__ Remittance advice

g. Method of maintaining customer accounts that generates

payments for each individual sales transaction

8. _j__ Lockbox

h. Maximum possible account balance for a customer

9. _k__ Back order

i. Electronic invoicing

10. _m__ Picking ticket

j. Post office box to which customers send payments

11. _l__ Bill of lading

k. Document used to indicate stock outs exist

l. Document used to establish responsibility for shipping goods via

a third party

n. Turnaround document returned by customers with payments

account

2. __g_ Open-invoice

b. Process of dividing customer account master file into subsets

3. __a__ Credit memo

c. System that integrates EFT and EDI information

4. __h__ Credit limit

d. System that contains customer-related data organized in a

manner to facilitate customer service, sales, and retention

Accounting Information Systems

12-5

12.2 What internal control procedure(s) would provide protection against the following

threats?

a. Theft of goods by the shipping dock workers, who claim that the inventory

shortages reflect errors in the inventory records.

Inventory clerks should count and document goods (on paper or by computer) as they

leave inventory storage. Shipping personnel should be required to count and

b. Posting the sales amount to the wrong customer account because a customer

account number was incorrectly keyed into the system.

If the transactions are being entered online, closed loop verification could be used.

The system could respond to the operator entering the account number by retrieving

and displaying the customer’s name for the operator to review.

c. Making a credit sale to a customer who is already four months behind in making

payments on his account.

Up–to-date credit records must be maintained to control this problem. During the

credit approval process, the credit manager should review the accounts receivable

Ch. 12: The Revenue Cycle: Sales and Cash Collections

d. Authorizing a credit memo for a sales return when the goods were never actually

returned.

A receiving report should be required before a credit for sales returns is issued. The

e. Writing off a customer’s accounts receivable balance as uncollectible to conceal

the theft of subsequent cash payments from that customer.

The problem usually occurs because the same individual writes off accounts and

f. Billing customers for the quantity ordered when the quantity shipped was

actually less due to back ordering of some items.

Shipping personnel should be required to record the actual quantity shipped on the

g. Theft of checks by the mailroom clerk, who then endorsed the checks for deposit

into the clerk’s personal bank account.

In order to cover up this theft, the mailroom clerk has to be able to alter the accounts

receivable records. Otherwise, a customer who is subsequently notified that they are

Accounting Information Systems

12-7

h. Theft of funds by the cashier, who cashed several checks from customers.

In order to cover up this theft, the cashier has to be able to alter the accounts

receivable records. Otherwise, a customer who is subsequently notified that they are

past due will complain and provide proof that they sent in payment. Therefore, the

critical control is to segregate the duties of handling cash and making deposits from

the maintenance of accounts receivable records.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

i. Theft of cash by a waiter who destroyed the customer sales ticket for customers

who paid cash.

In a manual system, all sales tickets should be prenumbered and accounted for so

management can detect missing sales tickets.

j. Shipping goods to a customer but then failing to bill that customer.

To prevent this from occurring deliberately, it is necessary to segregate the shipping

and billing functions.

k. Lost sales because of stockouts of several products for which the computer

records indicated there was adequate quantity on hand.

Regular physical inventory counts need to be made, the results compared to recorded

amounts on hand, and needed adjustments to inventory quantities made.

l. Unauthorized disclosure of buying habits of several well-known customers.

Access to customer information should be restricted using User IDs, passwords, and

an access control matrix.

Accounting Information Systems

12-9

m. Loss of all information about amounts owed by customers in New York City

because the master database for that office was destroyed in a fire.

Data: Regular backups with copies being stored off-site.

n. The company’s Web site was unavailable for seven hours because of a power

outage.

A UPS can power a system for a time, but most are unlikely to be able to power a

system for seven hours.

o. Interception and theft of customers’ credit card numbers while being sent to the

company’s Web site.

Encryption of credit card information prior to transmitting over the Internet. Typically

this involves using SSL.

p. A sales clerk sold a $7,000 wide-screen TV to a friend and altered the price to

$700.

All product prices and sales discounts maintained in the system

Ch. 12: The Revenue Cycle: Sales and Cash Collections

q. A shipping clerk who was quitting to start a competing business copied the

names of the company’s 500 largest customers and offered them lower prices

and better terms if they purchased the same product from the clerk’s new

company.

Shipping clerks should not have access to customer account information.

r. A fire in the office next door damaged the company’s servers and all optical and

magnetic media in the server room. The company immediately implemented its

disaster recovery procedures and shifted to a backup center several miles away.

The company had made full daily backups of all files and stored a copy at the

backup center. However, none of the backup copies were readable.

Periodically practicing and testing the backup and restoration process would verify its

effectiveness.

Accounting Information Systems

12-11

12.3 For good internal control, which of the following duties can be performed by the

same individual?

1. Approve changes to customer credit limits

2. Sales order entry

3. Shipping merchandise

Cells with an “X” indicate duties that can be performed by the same individual:

Duty

1

2

3

4

5

6

7

8

9

1

2

3

4

5

6

7

8

9

For sound internal control, most of these duties need to be performed by different people.

There are two exceptions:

• The same person can take customer orders and check inventory availability because

this combination does not provide any way to commit and conceal a theft.

Key duties to segregate include:

• Approving changes to customer credit and sales order entry. If both duties are

performed by the same person, they could authorize sales to friends that are

subsequently not paid.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

• Depositing customer payments and maintaining accounts receivable. If the same

person performs both duties, they could commit the fraud known as lapping (stealing

payments and covering it up by adjusting the accounts so that the customer does not

complain about a missing credit).

Accounting Information Systems

12-13

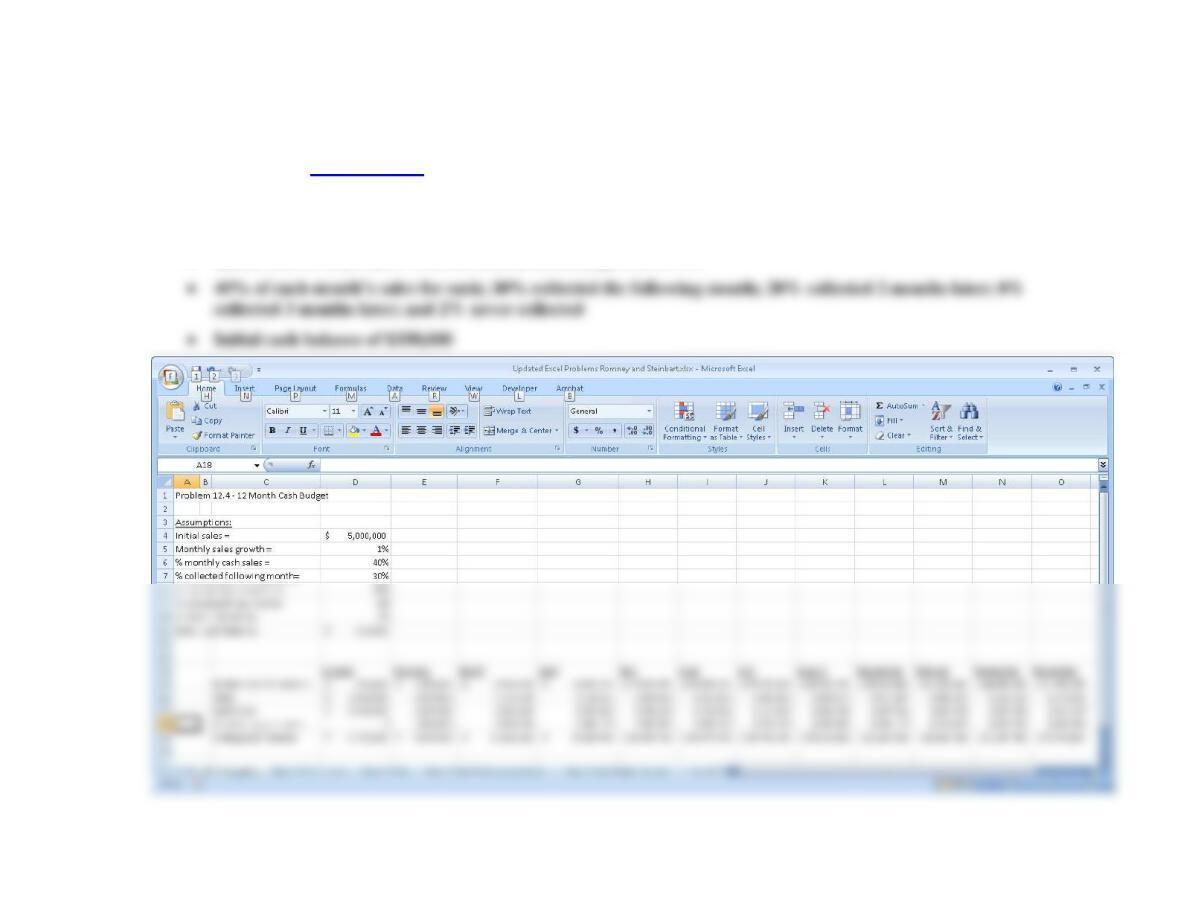

12.4 EXCEL PROJECT. (Hint: For help on steps b and c, see the article “Dial a Forecast,” by James A. Weisel, in the

December 2006 issue of the Journal of Accountancy. The Journal of Accountancy is available in print or online at the

AICPA’s Web site: www.aicpa.org

Required:

a. Create a 12-month cash flow budget in Excel using the following assumptions:

• Initial sales of $5,000,000 with forecasted monthly growth of 1%

Accounting Information Systems

12-15

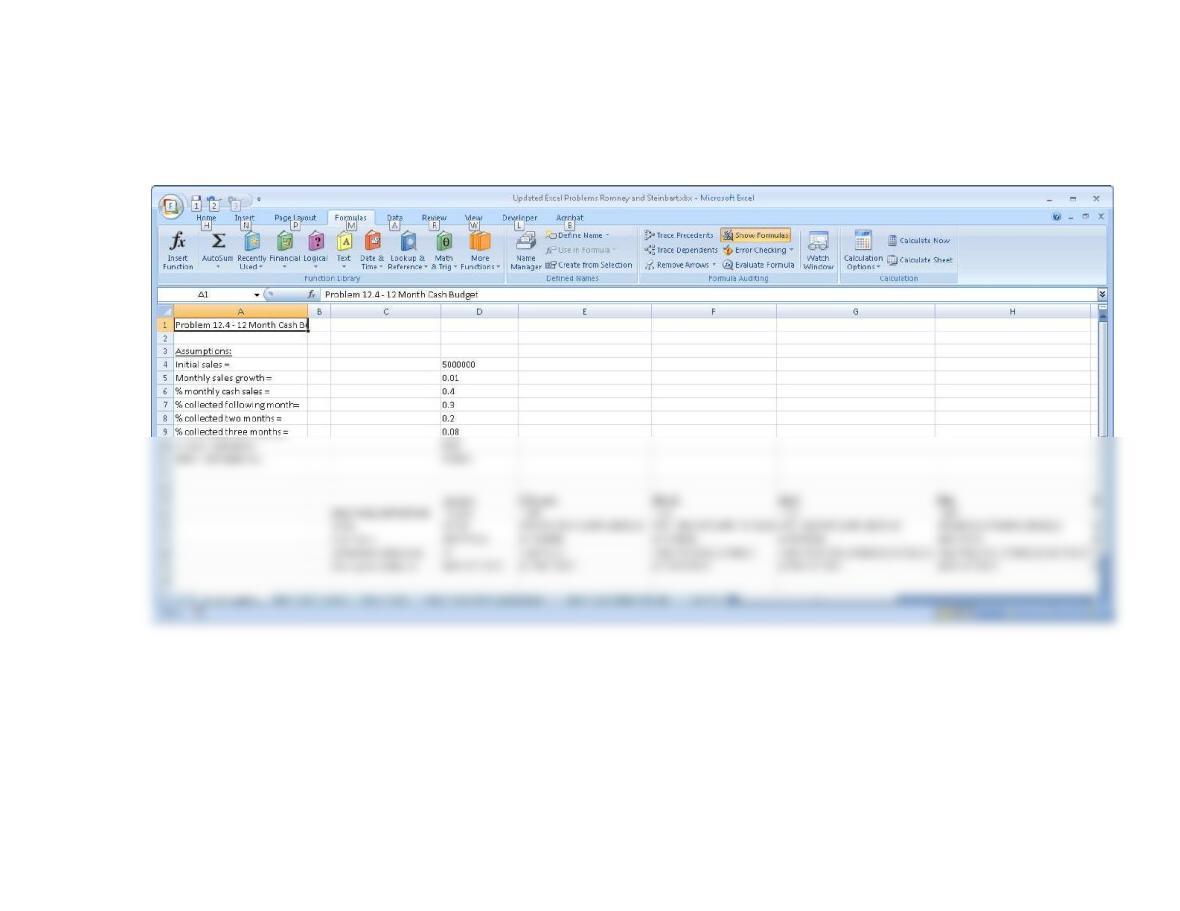

Formulas (the formulas for June – December are similar to those shown in the column for April and May)

Ch. 12: The Revenue Cycle: Sales and Cash Collections

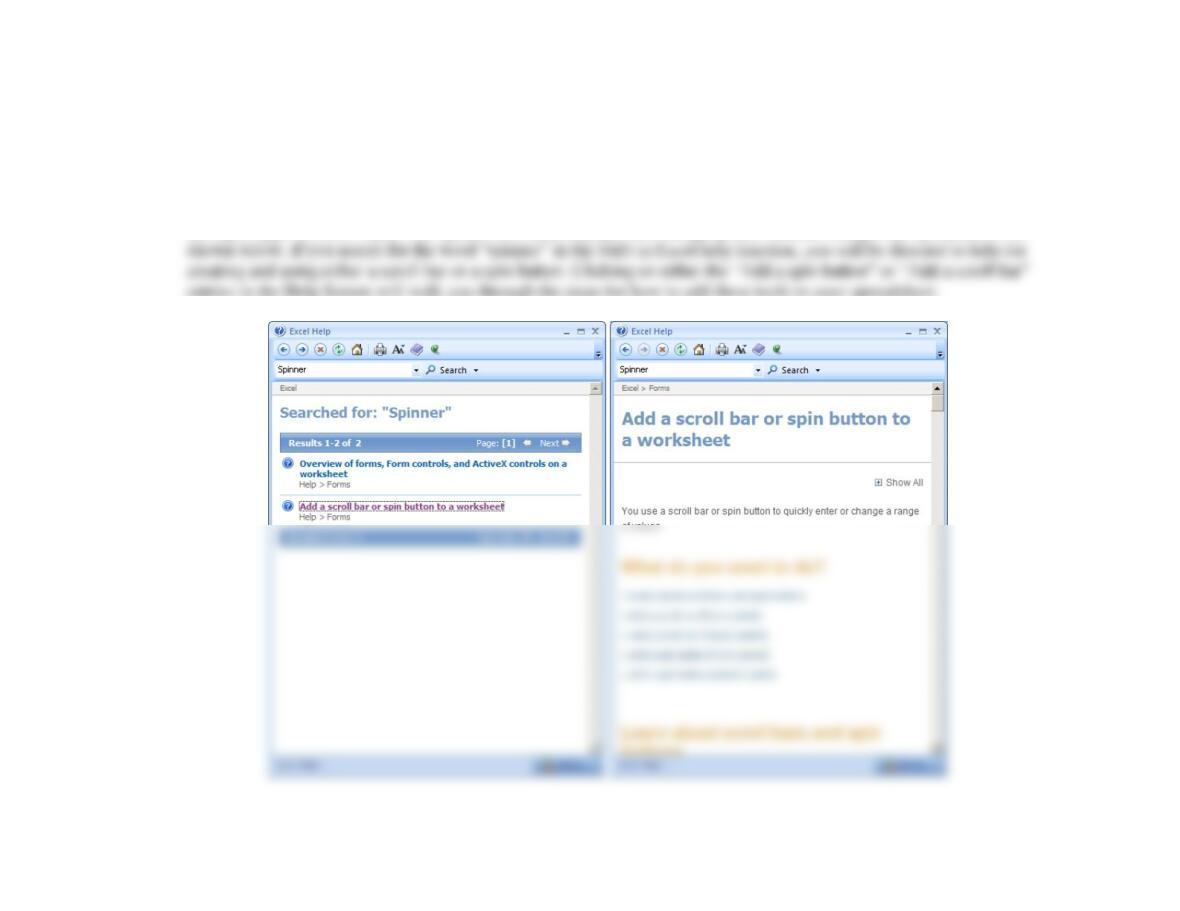

b. Add a “spinner” to your spreadsheet that will enable you to easily change forecasted monthly sales growth to range

from 0.5% to 1.5% in increments of 0.1%.

A “spinner” is a tool that enables the user to easily alter the values of a variable by clicking on the “spinner” rather than

having to type in a new value. The spinner tool then displays how changing that variable changes the spreadsheet. As

Accounting Information Systems

12-17

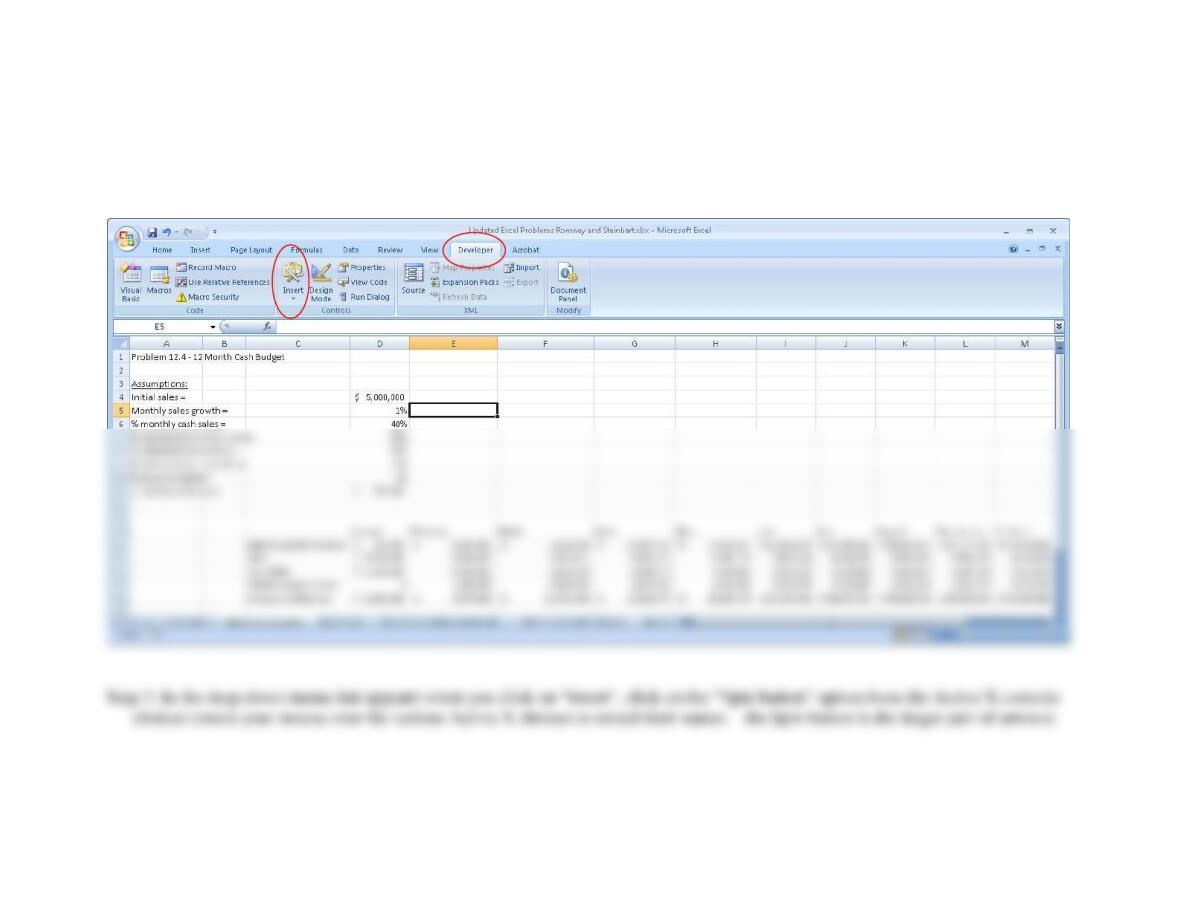

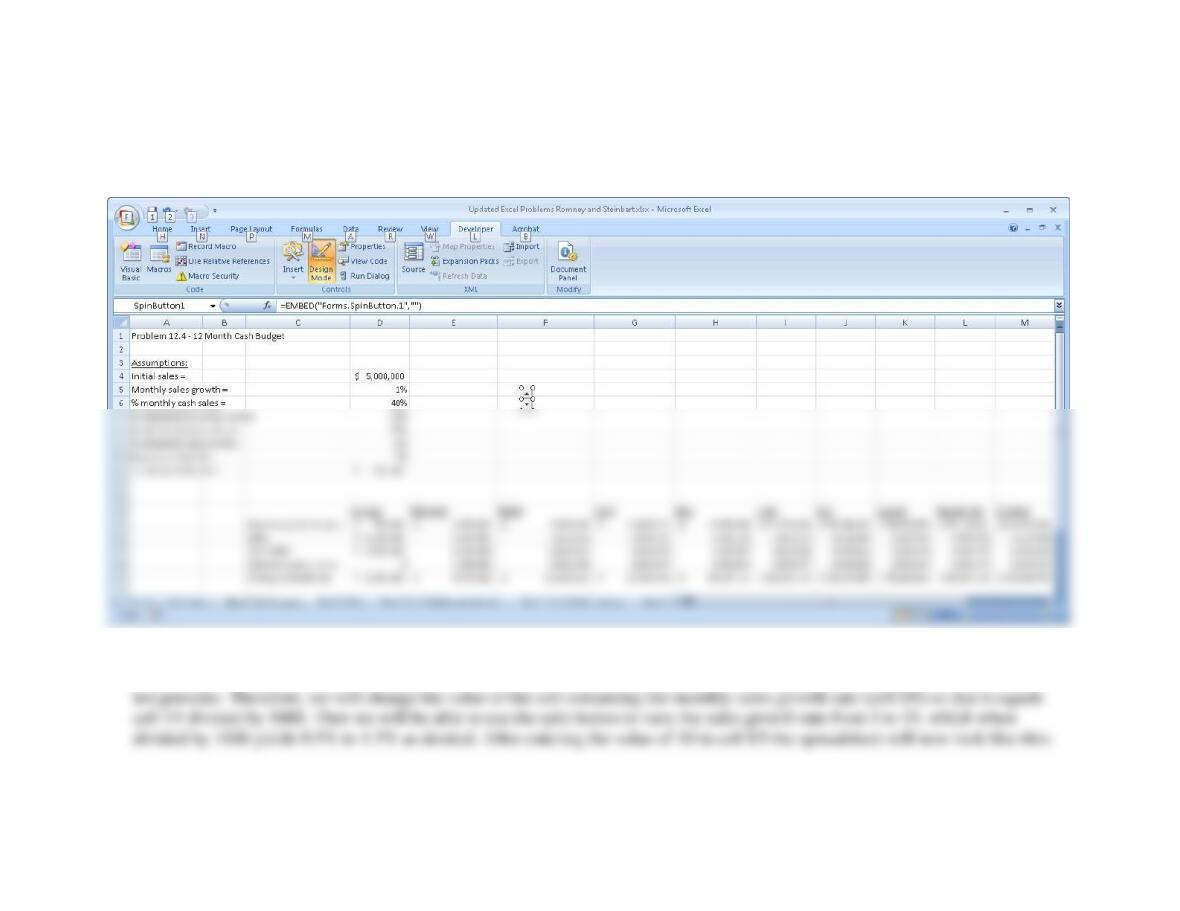

In part b, we will create a spin button to change the assumed sales growth rate.

Step 1: Click on the “Developer” tab and then click on the “Insert” button as shown:

Ch. 12: The Revenue Cycle: Sales and Cash Collections

Then click on a cell that is two cells to the right of the one that contains your initial assumption for the sales growth rate (i.e., cell F5)

which will result in the following:

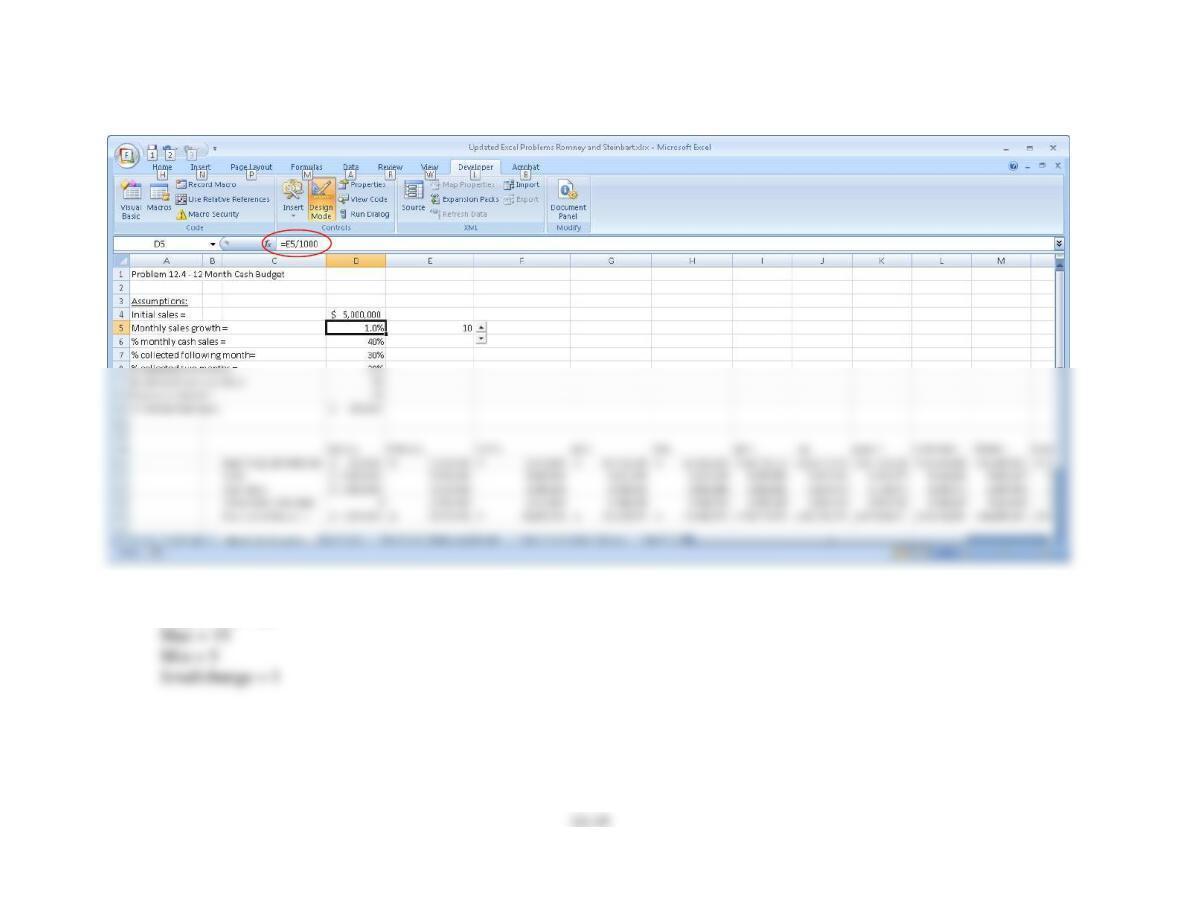

Step 3: Now we have to link the spin button tool to the cell that we wish to manipulate. In this case, the objective is to be able to vary

the sales growth rate (in cell D5) from 0.5% to 1.5%. However, the spin button tool can only increment variables in whole units,

Accounting Information Systems

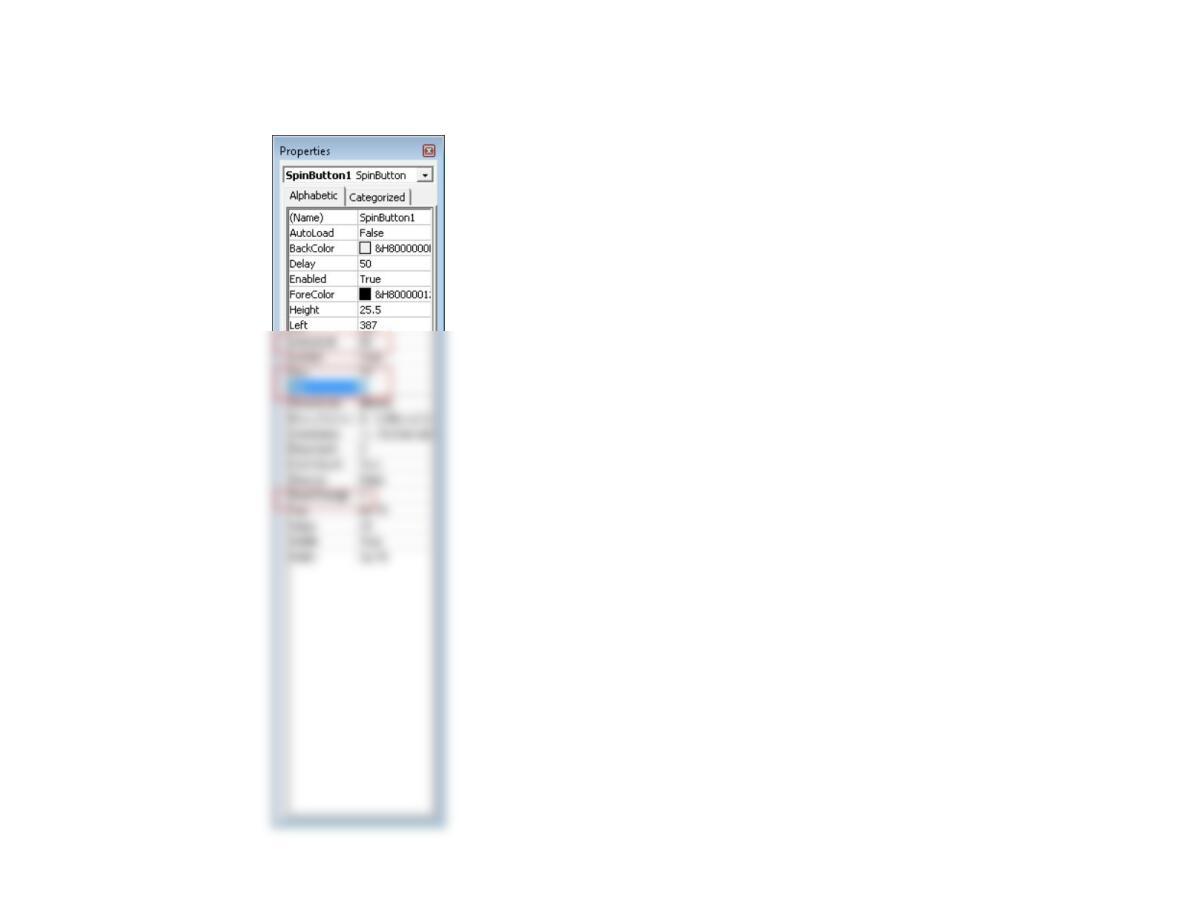

Step 4: Now right-click on the spin button, then select “Properties” and enter the following values:

Linked cell = E5

Ch. 12: The Revenue Cycle: Sales and Cash Collections