Chapter 12 – Financial Statement Analysis

Chapter 12

Financial Statement Analysis

REVIEW QUESTIONS

Question 12-1 (LO 12.1, 12.2)

The three types of comparisons commonly used in financial statement analysis are comparisons

Question 12-2 (LO 12.1, 12.2)

For vertical analysis, we express each item as a percentage of the same base amount, such as a

Question 12-3 (LO 12.1)

Question 12-4 (LO 12.1)

The company that has most of its equity balance in retained earnings is likely an older and more

Question 12-5 (LO 12.2)

Question 12-6 (LO 12.3)

We measure income statement accounts over a period of time (like a video), while we measure

Question 12-7 (LO 12.3)

Liquidity refers to a company’s ability to pay its current liabilities. The accounts used to

Question 12-8 (LO 12.3)

Question 12-9 (LO 12.3)

(a) Good news.

Question 12-10 (LO 12.3)

Question 12-11 (LO 12.4)

Question 12-12 (LO 12.4)

(a) Good news.

Question 12-13 (LO 12.4)

The return on assets and the return on equity differ due to financial leverage – the amount of debt

Question 12-14 (LO 12.5)

Question 12-15 (LO 12.6)

The trend in earnings per share is favorable. Companies report discontinued operations

Question 12–16 (LO 12.6)

Question 12–17 (LO 12.6)

A larger estimation of the allowance for uncollectible accounts, the write-down of overvalued

Question 12-18 (LO 12.6)

A lower estimation of the allowance for uncollectible accounts, waiting to report an inventory

Question 12–20 (LO 12.6)

All of the changes proposed near the end of the chapter improve the income statement and the

Chapter 12 – Financial Statement Analysis

BRIEF EXERCISES

Brief Exercise 12-1 (LO 12.1)

2018

2017

Amount

%

Amount

%

Cash

$ 420,000

7.0

$ 1,050,000

21.0

Inventory

18.5

Long-term assets

3,900,000

65.0

54.5

$6,000,000

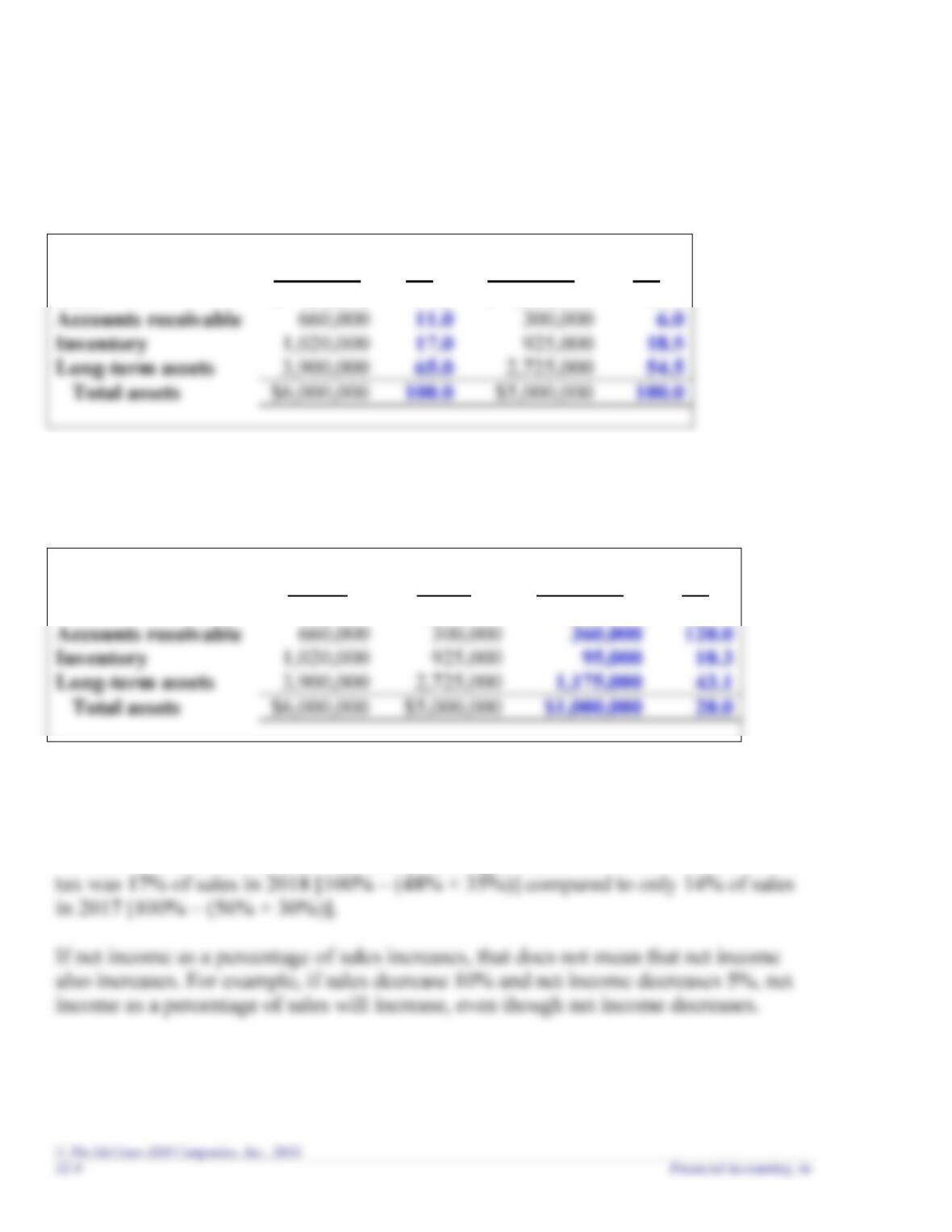

Brief Exercise 12-2 (LO 12.2)

Year

Increase (Decrease)

2018

2017

Amount

%

Cash

$ 420,000

$ 1,050,000

$ (630,000)

(60.0)

Accounts receivable

Inventory

$6,000,000

20.0

Brief Exercise 12-3 (LO 12.1)

Athletic World’s income before tax as a percentage of sales increased. Income before

Chapter 12 – Financial Statement Analysis

Brief Exercise 12-4 (LO 12.2)

Brief Exercise 12-5 (LO 12.2)

Brief Exercise 12-6 (LO 12.3)

Brief Exercise 12-7 (LO12.3)

Chapter 12 – Financial Statement Analysis

Brief Exercise 12-8 (LO12.3)

COGS must equal $980,000 to complete the inventory turnover ratio.

Inventory turnover ratio

COGS

$200,000

= 4.9 times

Brief Exercise 12-9 (LO12.3)

Current ratio before purchase of inventory

= 0.70 to 1

= 0.70 to 1

= 0.75 to 1

Chapter 12 – Financial Statement Analysis

Brief Exercise 12-10 (LO12.4)

Return on assets

= 15.0%

Profit margin

= 11.5%

Asset turnover

= 1.3 times

Brief Exercise 12-11 (LO12.4)

Return on assets

$130,000

$700,000

= 18.6%

Return on equity

= 36.1%

Brief Exercise 12-12 (LO12.5)

Income from continuing operations

$32,000,000

Discontinued operation:

Brief Exercise 12-13 (LO12.5)

12-8 Financial Accounting, 4e

1. Other expenses

2. Other expenses

Brief Exercise 12-14 (LO12.6)

1. Conservative

2. Aggressive

3. Aggressive

Brief Exercise 12-15 (LO12.6)

1. Conservative

2. Conservative

3. Conservative

Chapter 12 – Financial Statement Analysis

EXERCISES

Exercise 12-1 (LO12.1, 12.2, 12.3, 12.4, 12.5, 12.6)

Items

g

1. Vertical analysis

e

2. Horizontal analysis

a

3. Liquidity

h

4. Solvency

5. Discontinued operation

d

6. Quality of earnings

b

7. Conservative accounting practices

Descriptions

a. A company’s ability to pay its current liabilities.

b. Accounting choices that result in reporting lower income, lower assets, and

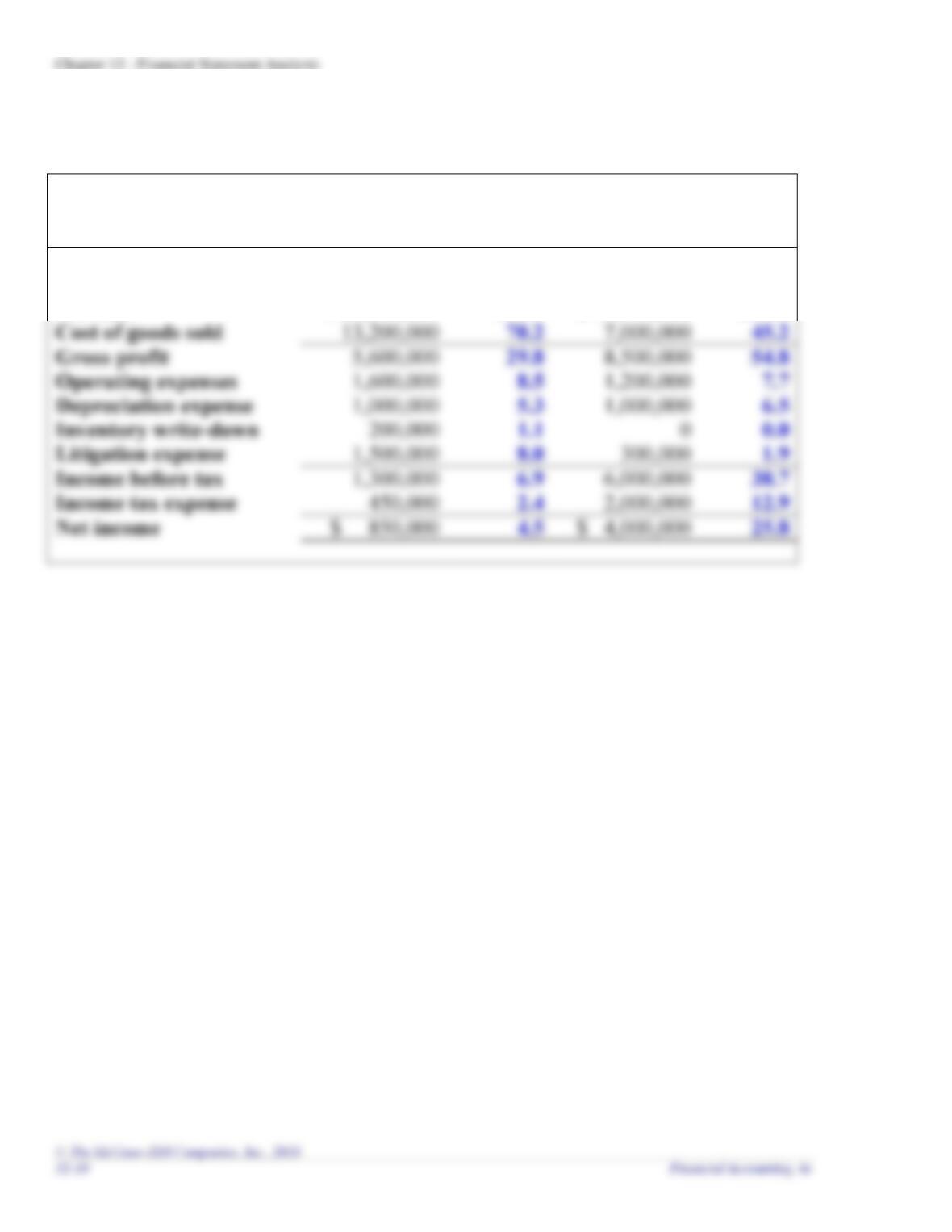

Exercise 12-2 (LO12.1)

Federer Sports Apparel

Income Statement

For the Years Ended December 31

2019

2018

Amount

%

Amount

%

Net sales

$ 18,800,000

100.0

$ 15,500,000

100.0

Cost of goods sold

Gross profit

Depreciation expense

Inventory write-down

Litigation expense

Income before tax

Income tax expense

Net income

$ 4,000,000

Chapter 12 – Financial Statement Analysis

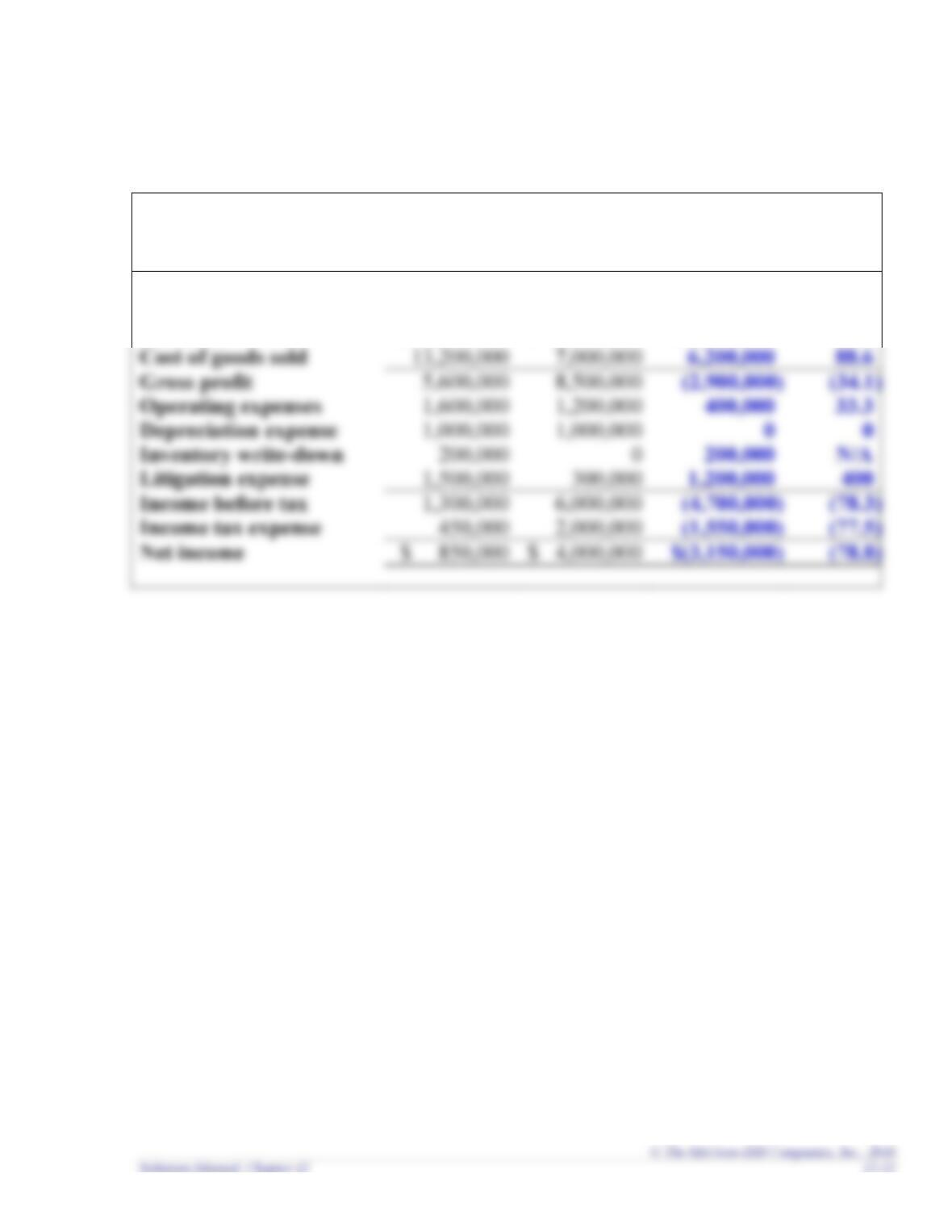

Exercise 12-3 (LO12.2)

Federer Sports Apparel

Income Statement

For the Years Ended December 31

Year

Increase (Decrease)

2019

2018

Amount

%

Revenues

$ 18,800,000

$ 15,500,000

$3,300,000

21.3

Cost of goods sold

88.6

Operating expenses

Depreciation expense

Inventory write-down

N/A

Litigation expense

Income before tax

Income tax expense

Net income

$ 4,000,000

Exercise 12-4 (LO12.1, 12.2)

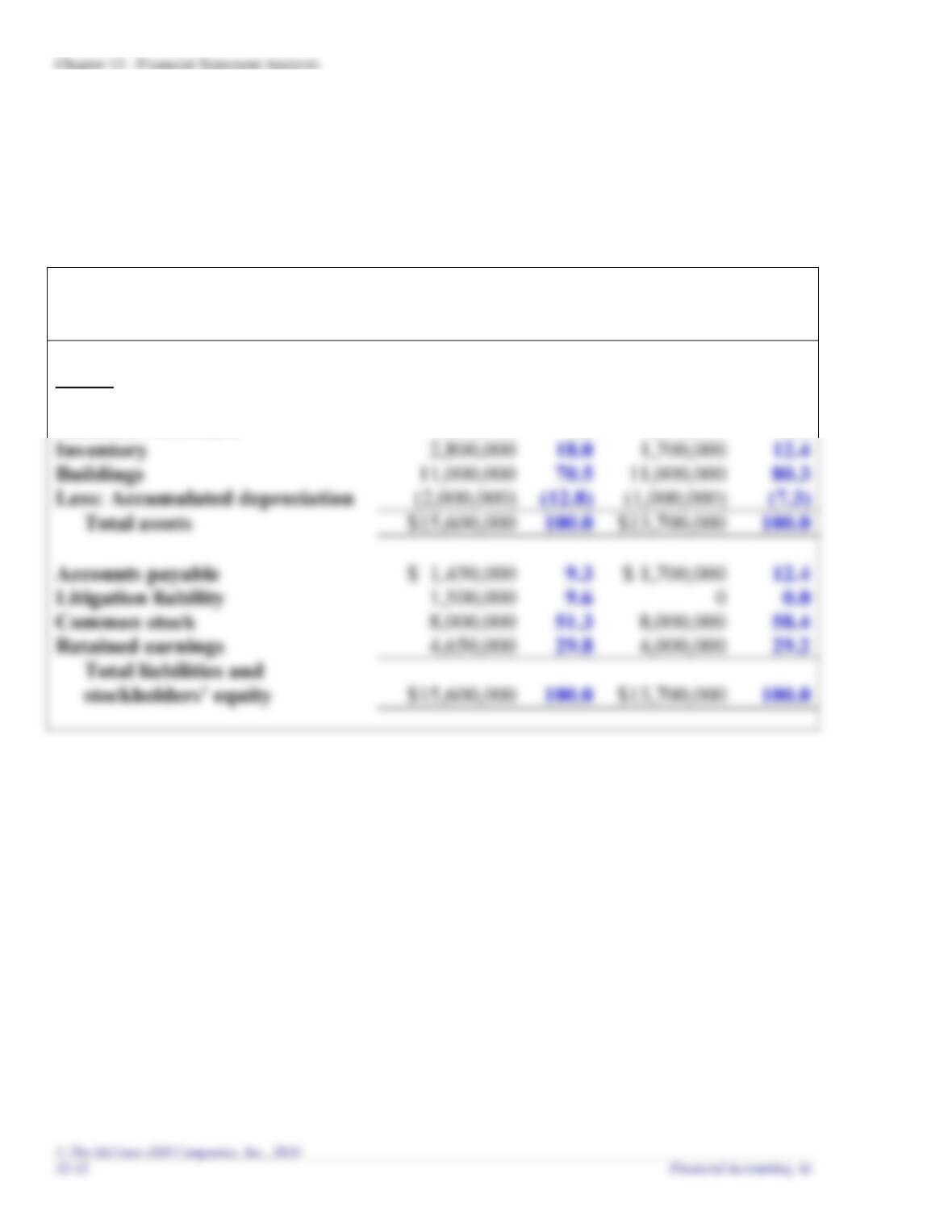

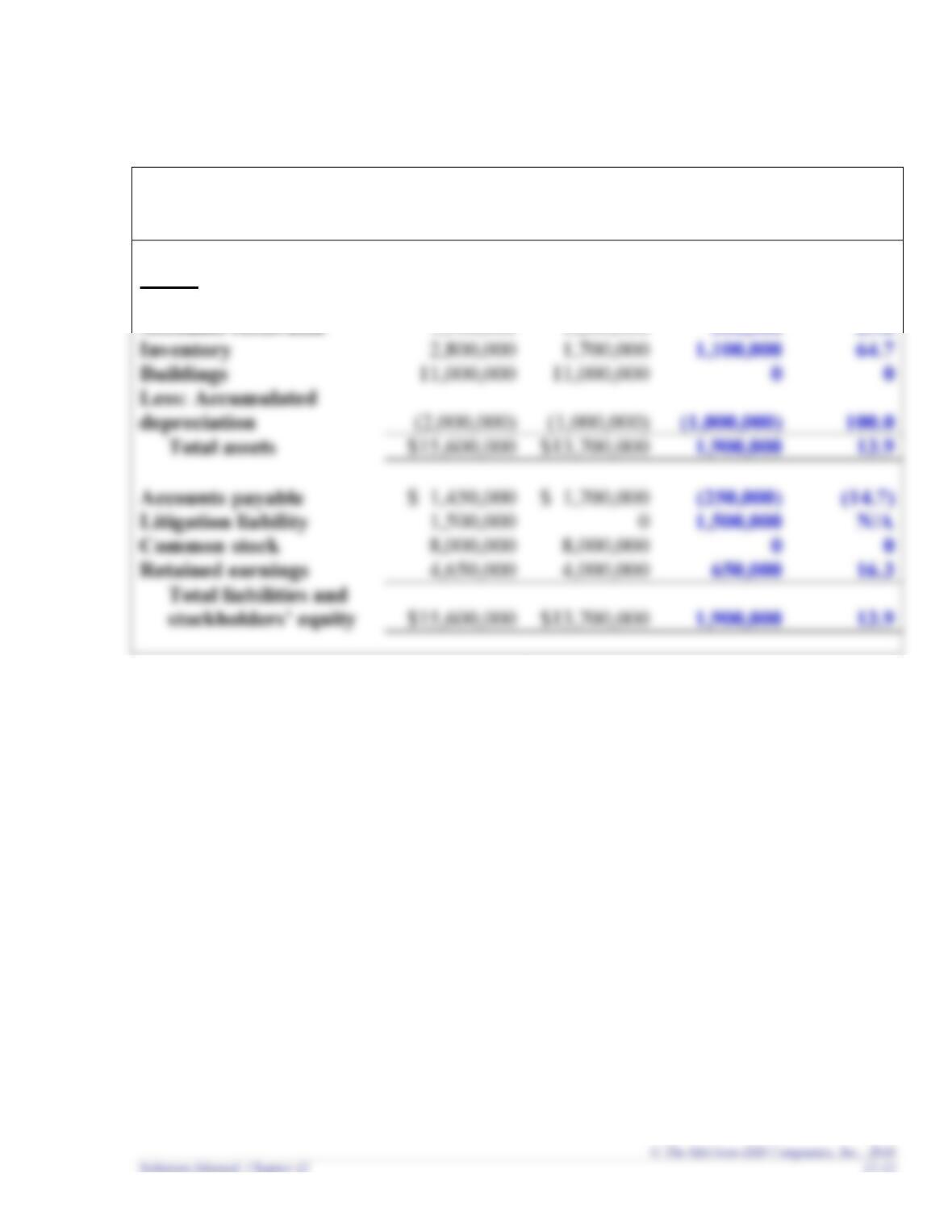

Requirement 1

Federer Sports Apparel

Balance Sheet

December 31

2019

2018

Assets

Amount

%

Amount

%

Cash

$ 2,300,000

14.7

$ 800,000

5.8

Accounts receivable

1,500,000

9.6

1,200,000

8.8

Inventory

2,800,000

18.0

1,700,000

Buildings

70.5

Less: Accumulated depreciation

Accounts payable

9.3

Litigation liability

1,500,000

9.6

0.0

Common stock

8,000,000

51.3

8,000,000

Retained earnings

4,650,000

29.8

4,000,000

Chapter 12 – Financial Statement Analysis

Requirement 2

Federer Sports Apparel

Balance Sheet

December 31

Year

Increase (Decrease)

Assets

2019

2018

Amount

%

Cash

$ 2,300,000

$ 800,000

$1,500,000

187.5

Accounts receivable

Inventory

Buildings

depreciation

100.0

Accounts payable

Litigation liability

Common stock

Retained earnings

650,000

Exercise 12-5 (LO12.3)

Requirement 1

Risk Ratios

Calculations

Receivables turnover ratio

$19,310,000

($1,100,000 + $1,600,000) / 2

= 14.3 times

Average collection period

= 25.5 days

Inventory turnover ratio

($1,500,000 + $2,000,000) / 2

= 7.0 times

Average days in inventory

= 52.1 days

Debt to equity ratio

= 88.5%

Requirement 2

Based on the above ratios, Adrian Express is more risky than the industry average.

Exercise 12-6 (LO12.4)

Requirement 1

Profitability Ratios

Calculations

Gross profit ratio

($19,310,000 – $12,250,000)

$19,310,000

= 36.6%

Return on assets

= 20.0%

$19,310,000

Asset turnover

= 2.3 times

Return on equity

= 40.4%

Requirement 2

Adrian Express is less profitable than the industry average. The gross profit ratio,

Exercise 12-7 (LO12.3)

Requirement 1

Risk Ratios

Calculations

a. Receivables turnover ratio

$1,890,000

($102,000 + $98,000) / 2

= 18.9 times

b. Inventory turnover ratio

= 14.3 times

d. Acid-test ratio

= 2.8 to 1

e. Debt to equity ratio

= 20.3%

Requirement 2

One company can have a higher current ratio while the other has a higher acid-test

ratio. The company may have a higher current ratio due to higher inventory and

Chapter 12 – Financial Statement Analysis

Exercise 12-8 (LO12.4)

Requirement 1

<

Profitability Ratios

Calculations

a. Gross profit ratio

$495,750

$1,890,000

= 26.2%

c. Profit margin

= 9.7%

d. Asset turnover

= 1.4 times

e. Return on equity

= 17.3%

Requirement 2

One company can have a higher return on assets while the other company has a higher

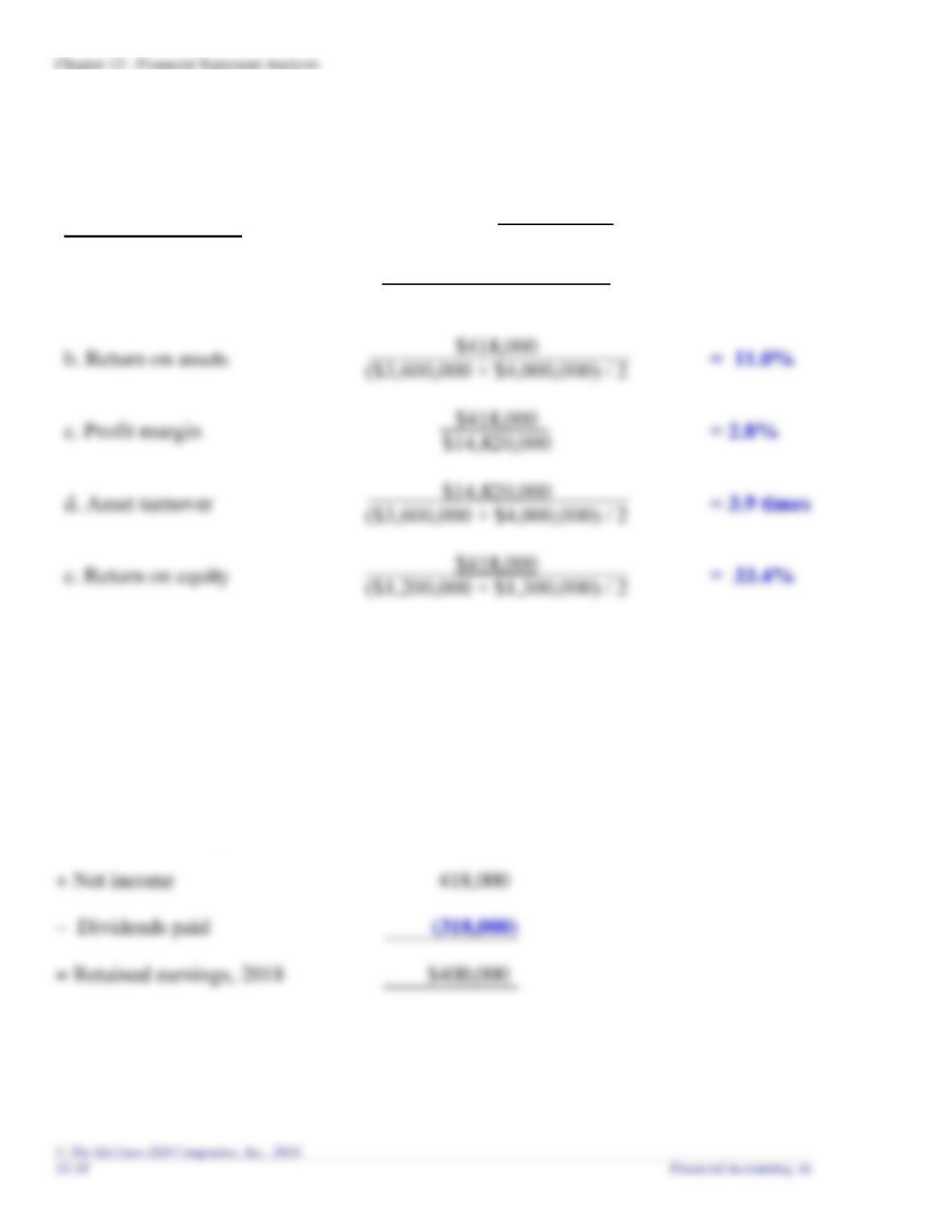

Exercise 12-9 (LO12.4)

Requirement 1

Profitability Ratios

Calculations

a. Gross profit ratio

$14,820,000 – $9,544,080

$14,820,000

= 35.6%

b. Return on assets

= 11.0%

d. Asset turnover

= 3.9 times

e. Return on equity

= 33.4%

Requirement 2

Dividends paid to shareholders in 2018 were $318,000. This amount can be

determined by analyzing the changes to retained earnings as follows:

Retained earnings, 2017

$300,000

$400,000

Exercise 12-10 (LO12.4)

Profitability Ratios

Calculations

Return on assets

$65,700

$900,000

= 7.3%

Profit margin

= 12.2%

Return on equity

$65,700

= 10.6%

Stockholders’ equity, beginning

$600,000

Exercise 12-11 (LO12.5)

a. Other expenses

b. Discontinued operations

c. Other expenses

d. Other expenses

e. Other revenues