CHAPTER 12

Planning for Capital Investments

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe capital budgeting

inputs and apply the cash

payback technique.

1, 2, 3

1

1

1, 2, 6, 9,

10, 11

1A, 2A

2. Use the net present value

method.

4, 5, 6, 7

2, 3, 4, 5

2

1, 2, 3, 4

10, 11

1A, 2A, 3A,

4A, 5A

3. Identify capital budgeting

challenges and

refinements.

8, 9, 10, 11

4, 5, 6

3

4

3A , 4A, 5A

4. Use the internal rate of

return method.

12, 13, 16

7, 8

4

5, 6, 7

3A, 5A

5. Use the annual rate of

return method.

3, 14, 15

9

5

8, 9, 10, 11

1A, 2A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Compute annual rate of return, cash payback, and net

present value.

Moderate

30–40

2A

Compute annual rate of return, cash payback, and net

present value.

Complex

30–40

3A

Compute net present value, profitability index, and

internal rate of return.

Moderate

20–30

4A

Compute net present value considering intangible

benefits.

Moderate

20–30

5A

Compute net present value and internal rate of return

with sensitivity analysis.

Moderate

30–40

ANSWERS TO QUESTIONS

1. The screening of proposed capital expenditures may be done by a capital budgeting committee

which submits its findings to the officers of the company. The officers, in turn, select the

projects they believe to be the most worthy of funding and submit them to the board of directors.

The directors ultimately approve the capital expenditure budget for the year.

2. The cash payback technique is relatively easy to compute and understand. However, it should

4. The two tables are:

(1) The present value of a single future amount (Table 3 in Appendix A). This table is used

when a project has uneven cash payments over its useful life and to compute the present

value of the salvage value of the project.

5. The decision rule is: Accept the project when net present value is zero or positive; reject the

project when net present value is negative.

6. The discount rate has two elements, a cost of capital element and a risk element. Many times

companies set the risk element equal to zero; thus, they are setting the discount rate equal to the

8. Examples of intangible benefits of investment projects would be increased product quality,

improved safety, and enhanced employee loyalty. Intangible benefits often complicate the capital

budgeting process because their value can be difficult to quantify. Ignoring intangible benefits

may result in rejecting projects that would be financially beneficial to the company.

Questions Chapter 12 (Continued)

10. When trying to choose between competing proposals, simply comparing the net present value of

the competing proposals ignores the fact that one proposal may require a considerably larger

investment. The profitability index is useful because it incorporates the required initial investment

into the evaluation.

11. A post-audit is a thorough evaluation of how well a project’s actual performance matches the

original projections. Performing post-audits can be valuable because:

(1) managers are more likely to submit reasonable and accurate data if they know that their

13. Under the internal rate of return method, the objective is to find the rate that will make the present

value of the expected net annual cash flows equal the present value of the proposed capital

expenditure. The decision rule under the internal rate of return method is: Accept the project

when the internal rate of return is equal to or greater than the required rate of return, and reject

the project when the internal rate of return is less than the required rate.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 12-1

$450,000 ÷ $60,000 = 7.5 years

BRIEF EXERCISE 12-2

Present Value

Less: Capital investment

Net annual cash flows – $40,000 X 5.65

$226,000

BRIEF EXERCISE 12-3

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

$25,000

X

3.79079

=

$ 94,770

BRIEF EXERCISE 12-4

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Less: Capital investment

Net present value

BRIEF EXERCISE 12-5

Project A

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$70,000

X

6.41766

=

$449,236

Project B

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

$55,000

X

6.41766

=

$352,971

Project B has a lower net present value than Project A, but because of its

BRIEF EXERCISE 12-6

Original estimate

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Less: Capital investment

250,000

Present value of net annual cash flows

$46,000

X

5.75902

=

$264,915

Less: Capital investment

400,000

BRIEF EXERCISE 12-6 (Continued)

Revised estimate

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$39,000

X

6.49506

=

($253,307)

BRIEF EXERCISE 12-7

When net annual cash flows are expected to be equal, the internal rate of

return can be approximated by dividing the capital investment by the net

annual cash flows to determine the discount factor, and then locating this

discount factor on the present value of an annuity table.

BRIEF EXERCISE 12-8

When net annual cash flows are expected to be equal, the internal rate of

return can be approximated by dividing the capital investment by the net

annual cash flows to determine the discount factor, and then locating this

BRIEF EXERCISE 12-8 (Continued)

Net annual cash flows = $400,000 – $150,000 = $250,000

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$250,000

X

7.16073

=

$1,790,183

BRIEF EXERCISE 12-9

The annual rate of return is calculated by dividing expected annual income

by the average investment. The company’s expected annual income is:

$130,000 – $70,000 = $60,000

Its average investment is:

flows

Less: Capital investment

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 12-1

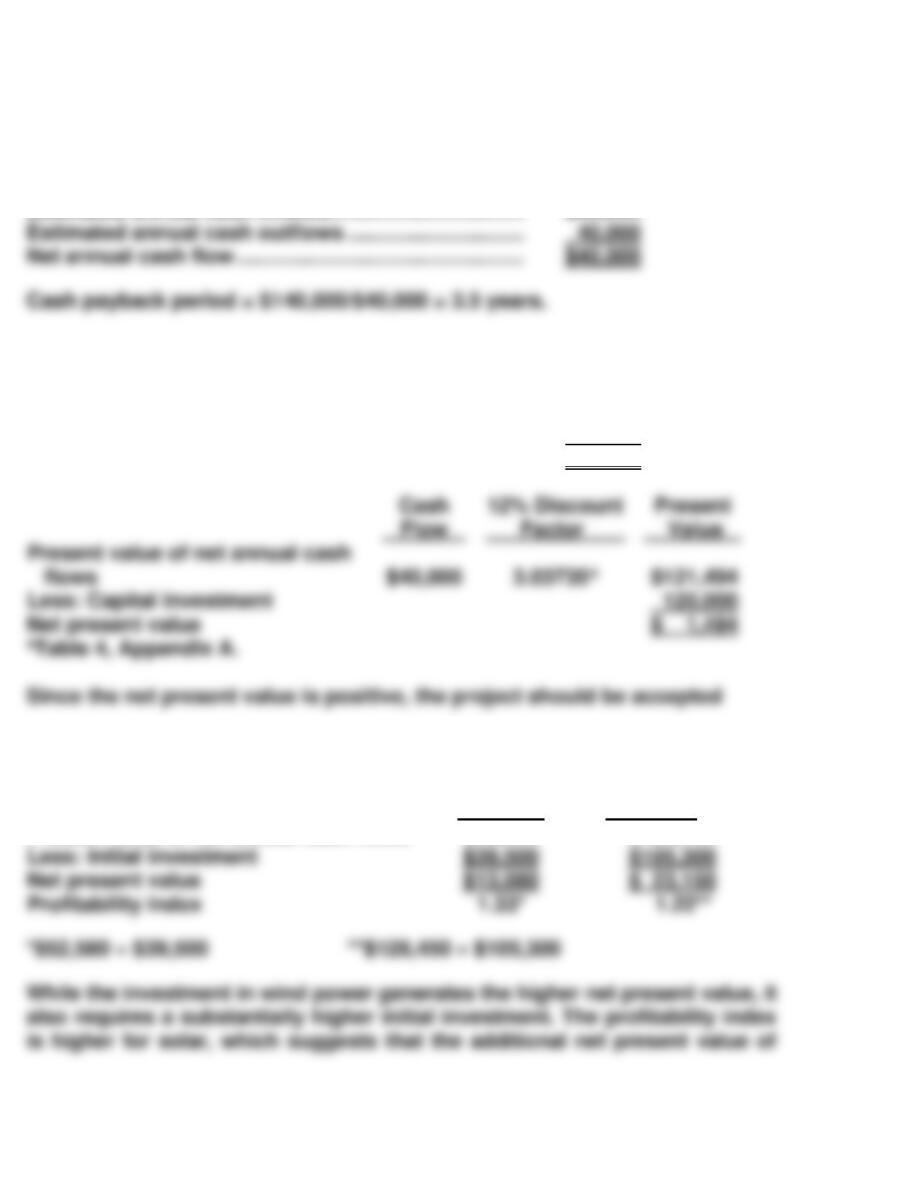

Estimated annual cash inflows…………………………... $80,000

DO IT! 12-2

Estimated annual cash inflows…………………………... $80,000

Estimated annual cash outflows ………………………… 40,000

Net annual cash flow …………………………………………. $40,000

DO IT! 12-3

Solar

Wind

Present value of net annual cash flows

$52,580

$128,450

Less: Initial investment

$39,500

$105,300

Profitability index

wind is outweighed by the cost of the initial investment. The company should

choose solar.

DO IT! 12-4

Estimated annual cash inflows…………………………... $80,000

Estimated annual cash outflows ………………………… 40,000

DO IT! 12-5

Revenues ………………………………………………………….. $80,000

Less:

Expenses (excluding depreciation) ………………… $41,000

SOLUTIONS TO EXERCISES

EXERCISE 12-1

(a) The cash payback period is:

$56,000 ÷ $8,000 = 7 years

The net present value is:

8%

(b) In order to meet the cash payback criteria, the project would have to

have a cash payback period of less than 4 years (8 ÷ 2). It does not

EXERCISE 12-2

(a)

AA

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

2

$ 7,000

9,000

$ 7,000

16,000

EXERCISE 12-2 (Continued)

BB

22,000 ÷ 10,000 = 2.2 years

CC

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

$13,000

$13,000

The most desirable project is CC because it has the shortest payback

period. The least desirable project is AA because it has the longest

payback period. As indicated, only CC is acceptable because its cash

payback is 1.75 years.

(b)

AA

BB

CC

Year

Discount

Factor

Cash

Flow

Present

Value

Cash

Flow

Present

Value

Cash

Flow

Present

Value

.71178

12,000

10,000

11,000

Total present value

Less: Investment

Net present value

21,966

(22,000

)

24,019

(1)

29,003

(22,000

1

2

.89286

.79719

$ 7,000

9,000

$ 6,250

7,175

$10,000

10,000

$ 8,929

7,972

$13,000

12,000

$11,607

9,566

EXERCISE 12-3

Investment in new equipment …………. $2,450,000

Disposal of old equipment ………………. (250,000)

Calculation of net present value:

Year

Discount

Factor, 9%

Amount

Present

Value

Cash flows 1 0.91743 $ 390,000 $ 357,798

2 0.84168 400,000 336,672

3 0.77218 411,000 317,366

Maintenance 5 0.64993 (100,000) (64,993)

Net cash flows from

operations: 2,028,586

EXERCISE 12-4

Machine A

Cash

Flows

X

9% Discount

Factor

=

Present

Value

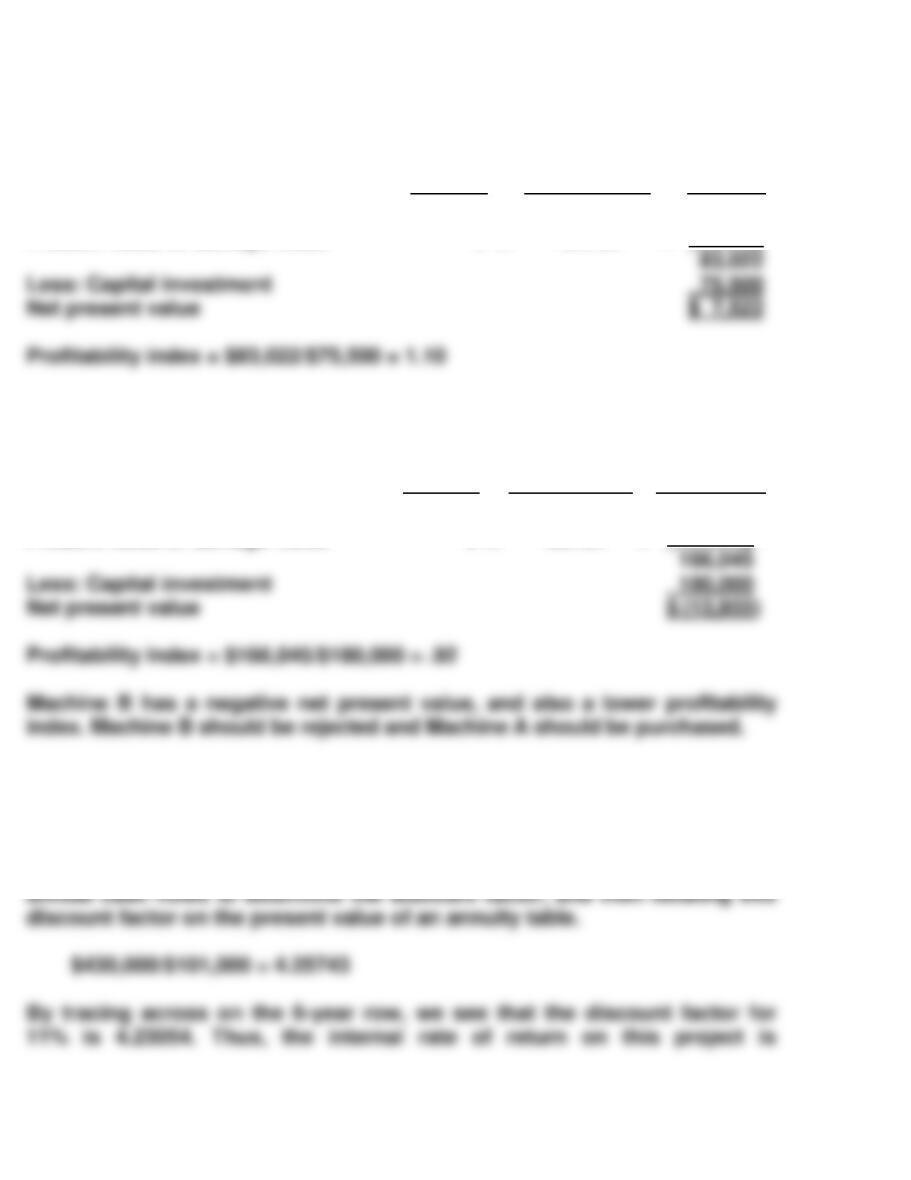

Present value of net annual cash flows

Present value of salvage value

$15,000

0

X

X

5.53482

.50187

=

=

$83,022

0

Machine B

Cash

Flows

X

9%

Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of salvage value

$30,000

0

X

X

5.53482

.50187

=

=

($166,045)

( 0)

EXERCISE 12-5

When net annual cash flows are expected to be equal, the internal rate of

return can be approximated by dividing the capital investment by the net

83,022

EXERCISE 12-6

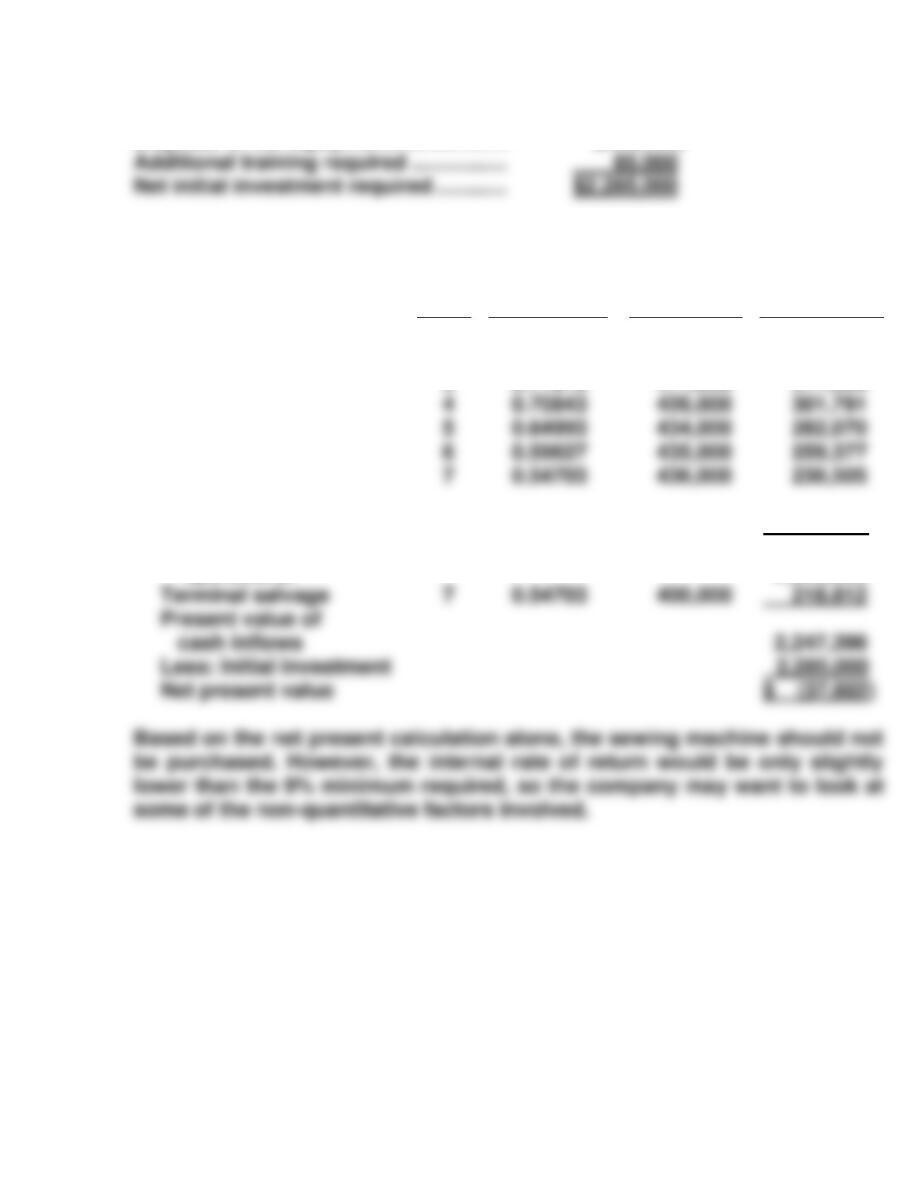

(a) Total net investment = $29,300 + $1,500 – $2,000 = $28,800

(b) Net present value approximates zero when discount rate is 12%.

Item

Amount

Years

PV Factor

Present

Value

EXERCISE 12-7

(a)

Project

Capital

Investment

÷

Net Annual Cash

Flows*

=

Internal

Rate of

Return

Factor

Closest

Discount

Factor

Internal

Rate of

Return

÷

=

EXERCISE 12-8

The annual rate of return is calculated by dividing expected annual income

by the average investment. The company’s expected annual income is:

$70,000 – $41,500 = $28,500

Its average investment is:

EXERCISE 12-9

(a) Cost of hoist: $32,400 + $3,300 + $700 = $36,400.

Net annual cash flows:

Number of extra mufflers 5 X 52 weeks (a) 260

EXERCISE 12-10

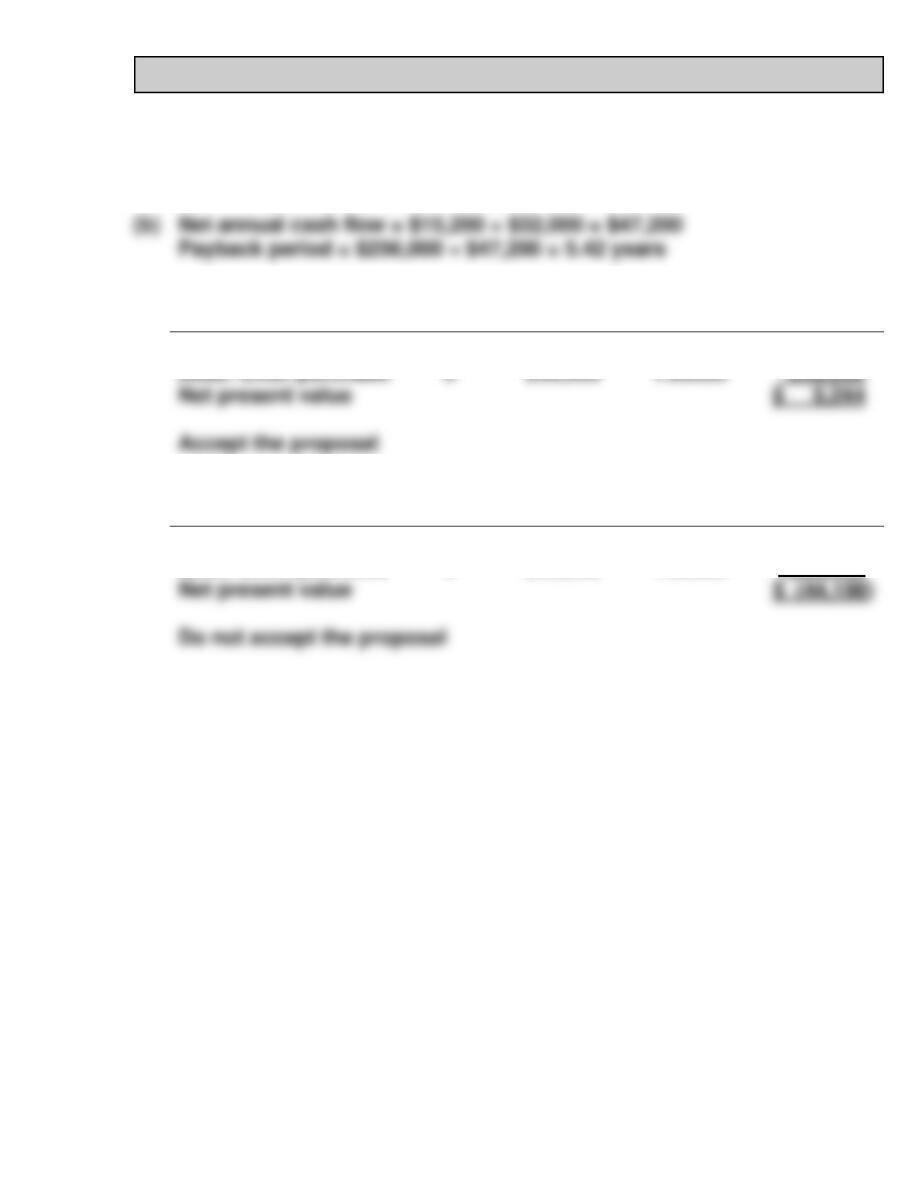

(a) 1. Cash payback period: $190,000 ÷ $50,000 = 3.8 years.

2. Annual rate of return: $12,000 ÷ [($190,000 + $0) ÷ 2] = 12.63%.

EXERCISE 12-11

(a)

Year

Net Annual Cash Flow

Cumulative Net Cash Flow

1

2

3

$45,000

40,000

35,000

$ 45,000

85,000

120,000

(c) Discount Present

Year Factor, 11% Amount Value

Net cash flows 1 0.90090 $45,000 $ 40,541

2 0.81162 40,000 32,465

SOLUTIONS TO PROBLEMS

PROBLEM 12-1A

(a) Project Bono $160,000 ÷ ($14,000 + $32,000) = 3.48 years

Project Edge

Year

Cash Flow

Cumulative Cash Flow

1

2

$53,000 ($18,000 + $35,000)

$52,000 ($17,000 + $35,000)

$ 53,000

$105,000

Project Clayton

Year

Cash Flow

Cumulative Cash Flow

1

2

$67,000 ($27,000 + $40,000)

$63,000 ($23,000 + $40,000)

$ 67,000

$130,000

PROBLEM 12-1A (Continued)

(b) Project Bono

Item

Amount

Years

PV Factor

Present

Value

Net annual cash flows

Less: Capital investment

Negative net present value

$46,000

1–5

3.35216

$154,199

160,000

$ (5,801)

Project Edge

Project Clayton

Year

Discount

Factor

Cash

Flow

PV

Cash

Flow

PV

1

2

.86957

.75614

$ 53,000

52,000

$ 46,087

39,319

$ 67,000

63,000

$ 58,261

47,637

(c) Project Bono = $14,000 ÷ [($160,000 + $0) ÷ 2] = 17.5%.

Project Edge = $14,400 ÷ [($175,000 + $0) ÷ 2] = 16.5%.

Project Clayton = $19,200 ÷ [($200,000 + $0) ÷ 2] = 19.2%.

(d)

Project

Cash Payback

Net

Present Value

Annual

Rate of Return

Clayton

Bono

3

2

2

$237,000

PROBLEM 12-2A

(a)

(1)

Annual

Net Income

(2)

Annual

Cash Inflow

Sales

Expenses

Drivers’ salaries

Out-of-pocket expenses

*$108,000*

* 48,000*

* 30,000*

$108,000

48,000

30,000

(c) Present value of annual cash inflows ($30,000 X 2.28323*) = $68,497

Less: Capital investment = 75,000

Net present value = $ (6,503 )

*3 years at 15%, PV of annuity of 1.

PROBLEM 12-3A

(a)

(1) Option A

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Less: Capital investment

a$41,000a

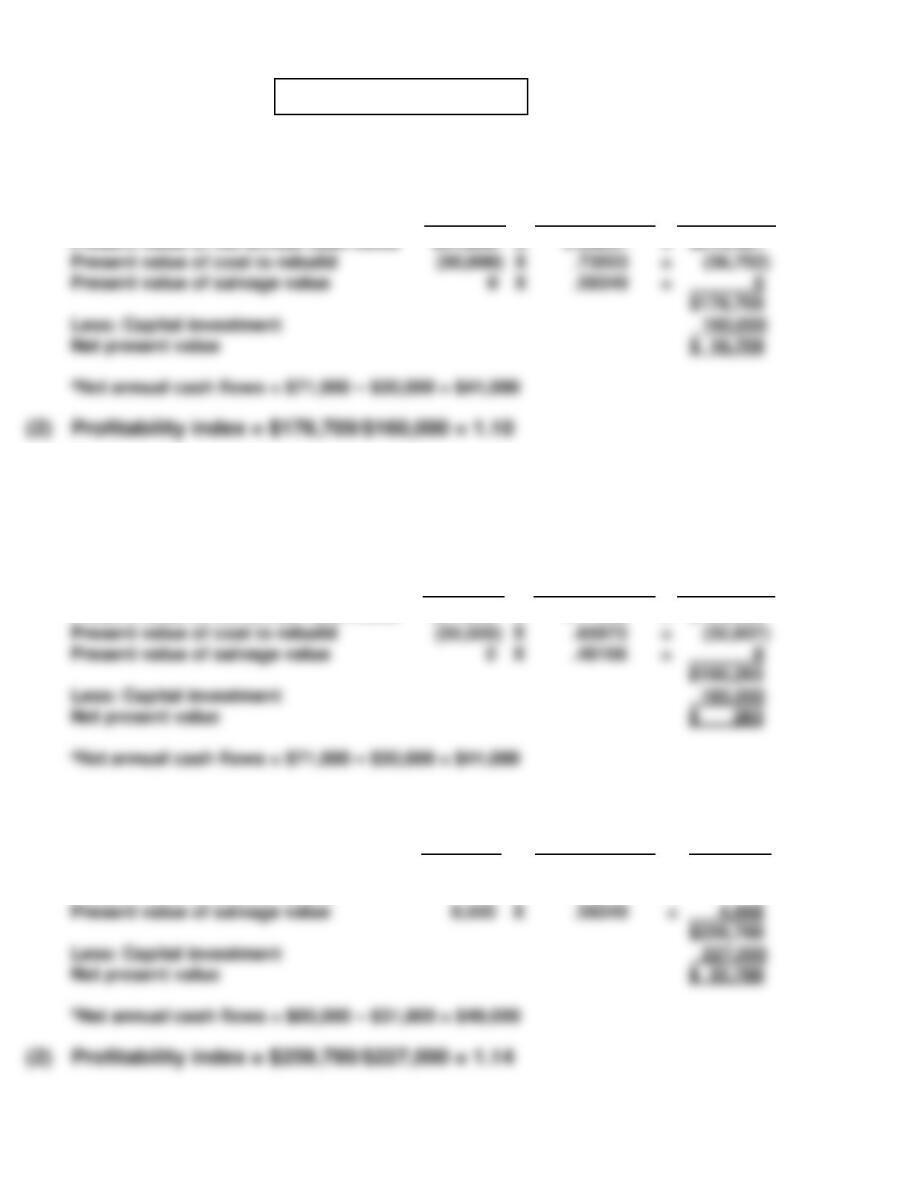

(3) The internal rate of return can be approximated by finding the discount

rate that results in a net present value of approximately zero. This is

accomplished with a 11% discount rate.

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

a$41,000a

X

4.71220

=

($193,200)

(1) Option B

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of cost to rebuild

b$49,000b

0

X

X

5.20637

.73503

=

=

$255,112

0

Less: Capital investment

PROBLEM 12-3A (Continued)

(3) Internal rate of return on Option B is 12%, as calculated below:

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of cost to rebuild

Present value of salvage value

b$49,000b

0

8,000

X

X

X

4.56376

.63552

.45235

=

=

=

$223,624

0

3,619

Less: Capital investment

PROBLEM 12-4A

(a) The net present value based on the original estimates is as follows:

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$ 8,000

X

5.53482

=

($ 44,279

(b) The net present value based on the revised estimates is as follows:

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

$13,500*

X

5.53482

=

($74,720)

(c) The present value of the intangible benefits was $30,441 (the increase

in the net present value from a negative $13,950 to a positive $16,491).

Rick’s estimates of the value of these intangible benefits may be overly

PROBLEM 12-5A

(a) Using the original estimates, the net present value is calculated as

follows:

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of salvage value

a$ 80,000a

1,500,000

X

X

9.81815

.21455

=

=

$ 785,452

321,825

1,107,277

(b) Using the revised estimates, the net present value is calculated as

follows:

Cash

Flows

X

8% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

Present value of salvage value

b$ 55,000b

1,500,000

X

X

9.81815

.21455

=

=

$(539,998)

(321,825)

$(861,823)

$ 207,277

PROBLEM 12-5A (Continued)

(c) Using the original estimates, but an 10% discount rate, the net present

value is calculated as follows:

Cash

Flows

X

10% Discount

Factor

=

Present

Value

Present value of net annual cash flows

Present value of salvage value

Less: Capital investment

c$ 80,000c

1,500,000

X

X

8.51356

.14864

=

=

$ 681,085

222,960

$ 904,045

900,000

(d) The internal rate of return can be determined by calculating the discount

rate that results in a net present value of approximately zero. In this

case the internal rate of return was approximately 12%.

Cash

Flows

X

12% Discount

Factor

=

Present

Value

Less: Capital investment

Present value of net annual cash flows

Present value of salvage value

$ 40,000

1,332,000

X

X

3.60478

.56743

=

=

$144,191

755,817

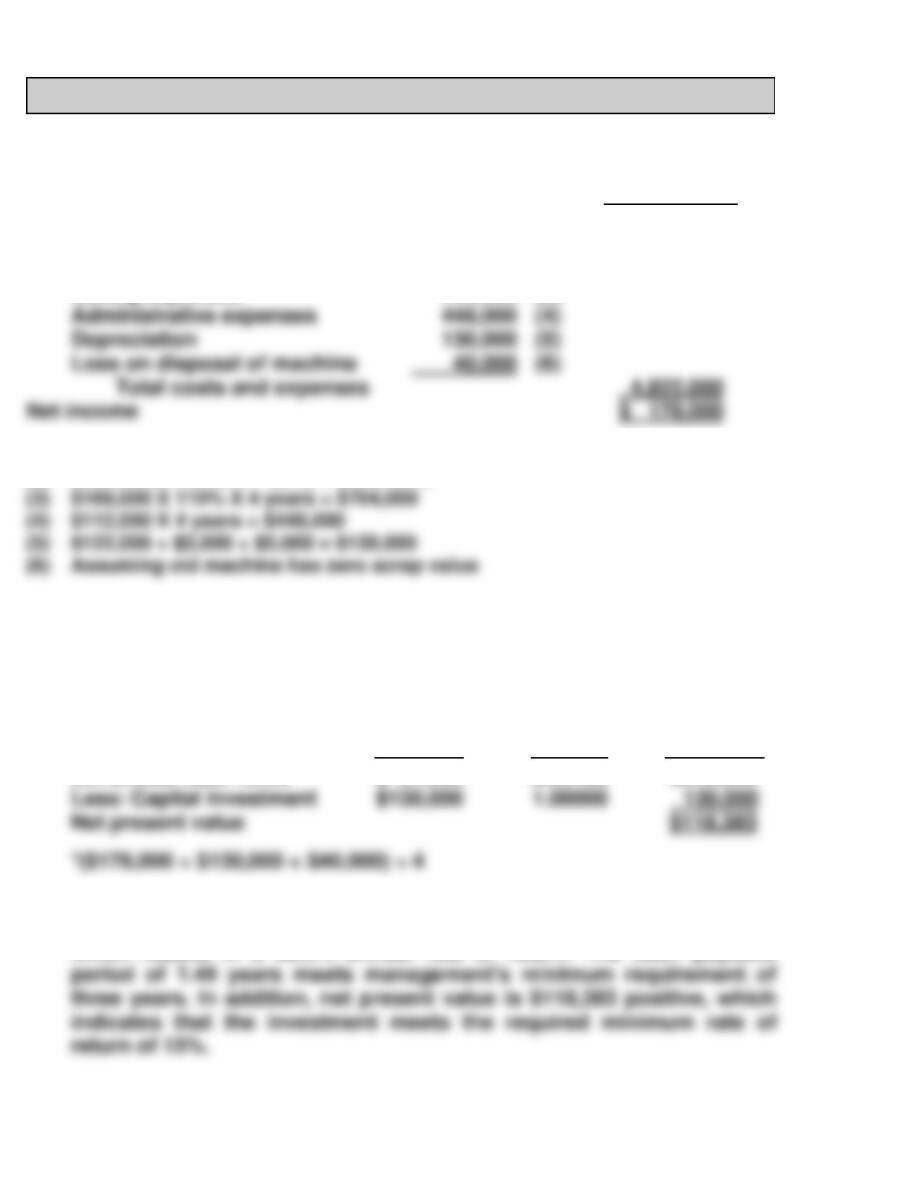

CD12 CURRENT DESIGNS

(a) Average investment = ($256,000 + 0) ÷ 2 = $128,000

Annual rate of return = $15,200 ÷ $128,000 = 11.88%

(c)

Event

Time

Period

Cash

Flows

9% Discount

Factor

Present

Value

Net annual cash flow

1-8

$ 47,200

5.53482

$ 261,244

Less: Oven purchase

0

256,000

1.00000

256,000

Net present value

$ 5,244

(d)

Event

Time

Period

Cash

Flows

15% Discount

Factor

Present

Value

Net annual cash flow

1-8

$ 47,200

4.48732

$ 211,802

Less: Oven purchase

0

256,000

1.00000

256,000

Net present value

BYP 12-1 DECISION-MAKING ACROSS THE ORGANIZATION

Purchase

New Machine

Sales

Costs and expenses

Cost of goods sold

Selling expenses

$3,500,000

704,000

(2)

(3)

$5,000,000

(1)

(1) 10,000 X $100 X 4 years = $4,000,000 X 125% = $5,000,000

(2) $5,000,000 X (100% – 30%) = $3,500,000

(a) Annual rate of return = 68.5%; ($178,000 ÷ 4) ÷ [($130,000 + $0) ÷ 2]

(b) Cash payback period = 1.49 yrs.; $130,000 ÷ [($178,000 + $130,000 +

$40,000) ÷ 4]

(c)

Net present value =

Amount

Factor

Present

Value

Net annual cash flows

$ 87,000

*

2.85498

$248,383

(d) The new machine should be purchased. The analysis shows that net

income will be $178,000 over the four years with the new machine,

which results in a 68.5% annual rate of return. The cash payback

BYP 12-2 MANAGERIAL ANALYSIS

(a) Using the original estimates, the present value is calculated as follows:

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Present value of net annual cash flows

$ 460,000a

X

7.19087

=

($3,307,800)

(b) Using the revised estimates, the net present value is calculated as

follows:

Cash

Flows

X

11% Discount

Factor

=

Present

Value

Present value of net annual cash flows

b$ 720,000b

X

7.19087

=

$5,177,426

BYP 12-2 (Continued)

(c) Using the original estimates, but a 9% discount rate, the net present

value is calculated as follows:

Cash

Flows

X

9% Discount

Factor

=

Present

Value

Present value of net annual cash flows

c$ 460,000c

X

8.06069

=

$3,707,917

Using the original estimates, but the lower discount rate, the net present

value is positive, suggesting the project should be accepted.

Less: Capital investment

$ 256,997

BYP 12-3 REAL-WORLD FOCUS

This disclosure, provided by the company’s management in its annual

report, suggests that the scroll compressor project has not achieved the

goals originally hoped for. In deciding whether to continue with this project,

management should undertake a post-audit. This would involve collecting

data on results obtained thus far and comparing those results with original

BYP 12-4 REAL-WORLD FOCUS

Answers to this problem will vary depending on the year chosen by the

student. The following solution is provided for the year ended July 28, 2013.

(a) The statement of cash flows indicates that capital expenditures

(purchase of plant assets) were $336 million in 2013, an increase of $13

million from the prior year.

BYP 12-5 COMMUNICATION ACTIVITY

To: Maria Fierro, Supervisor

From: , Assistant Chief Accountant

Subject: Recommendation for New Hoist

The quantitative analysis pertaining to this management decision is as

follows:

Cost of hoist: $32,400 + $3,300 + $700 = $36,400.

Net annual cash flows:

Average investment: ($36,400 + $3,000) ÷ 2 = $19,700.

Annual depreciation: ($36,400 – $3,000) ÷ 8 = $4,175.

Annual net income: $5,200 – $4,175 = $1,025.

Annual rate of return = $1,025 ÷ $19,700 = 5.2% (rounded).

BYP 12-6 ETHICS CASE

(a) The stakeholders are:

• Yourself.

• Your spouse and children.

• Employees of NuComp Company.

• Citizens of the town where the company is presently located.

• The stockholders of NuComp Company.

(b) The ethical issue is:

BYP 12-7 ALL ABOUT YOU

Results will vary depending on article selected by the student. Some

common signals identified in articles are: bills more than two months in

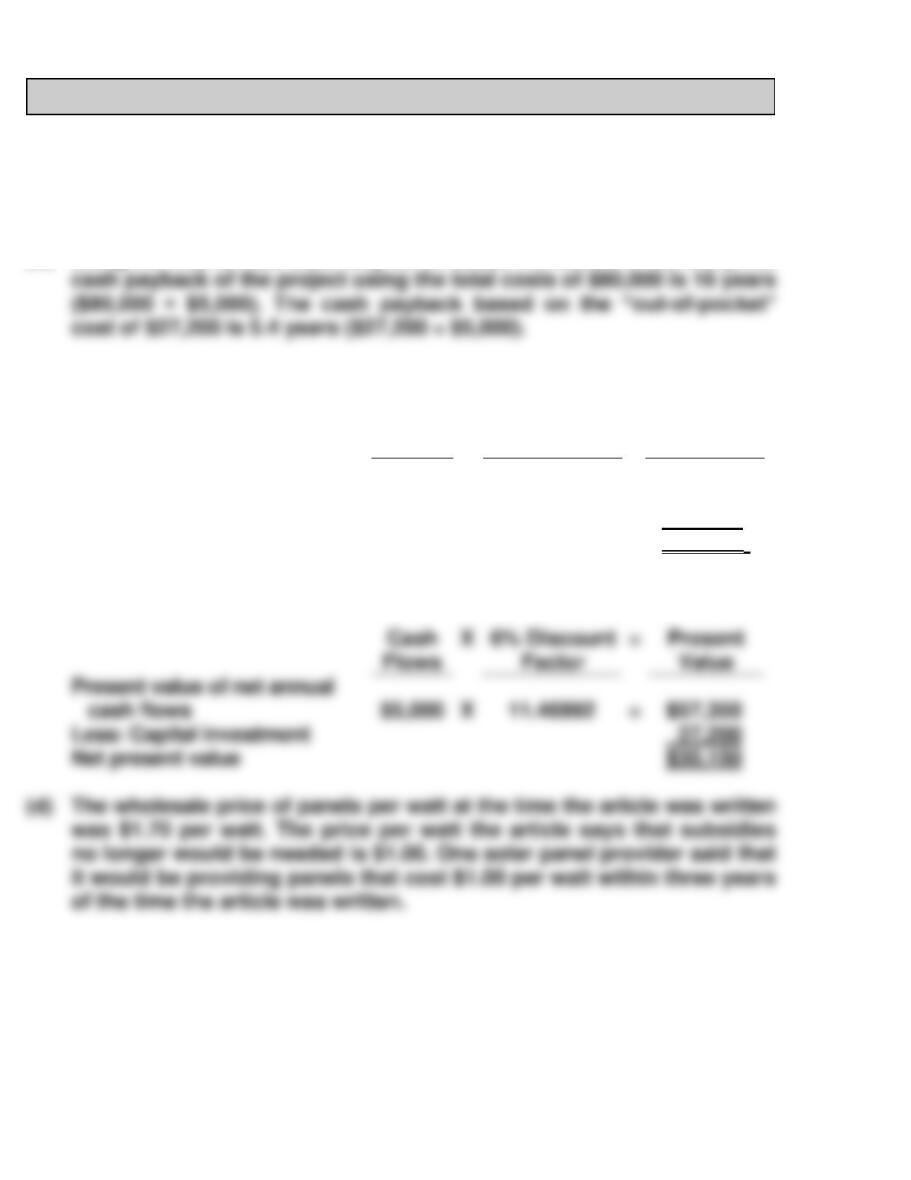

BYP 12-8 CONSIDERING YOUR COSTS AND BENEFITS

(a) The total cost of the installed solar panels was $80,000. The “out–of–

pocket” cost to the couple was $27,200.

(b) Using the total annual electricity bill of $5,000 mentioned in the story, the

(c) The net present value of the project using the total cost is:

Cash

Flows

X

6% Discount

Factor

=

Present

Value

Present value of net annual

cash flows

$5,000

X

11.46992

=

$ 57,350

Less: Capital investment

80,000

Net present value

$(22,650)

X

6% Discount

=

Present value of net annual

cash flows

$5,000

X

11.46992

=

Less: Capital investment

Net present value

The net present value of the project using the out–of–pocket cost is: