CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-6A (Concluded)

1. b.

Noncash Bowes Simmons Ahmed

Cash Assets Liabilities (2/5) (2/5) (1/5)

Balances before realization $ 38,000 $ 152,000 $ 24,000 $ 69,000 $ 85,000 $ 12,000

Sale of assets and division of loss 65,000 (152,000) —(34,800) (34,800) (17,400)

Balances after realization $103,000 $0

$ 24,000 $ 34,200 $ 50,200 $ (5,400)

The $5,400 deficiency of Ahmed would be divided between the other partners, Bowes and Simmons, in their income-

sharing ratio (1:1, respectively). Therefore, Bowes would absorb one-half of the $5,400 deficiency, or $2,700, and

Simmons would absorb one-half of the $5,400 deficiency, or $2,700.

* $34,200 – $2,700

** $50,200 – $2,700

Bowes, Simmons, and Ahmed

Statement of Partnership Liquidation

Capital

For Period November 1–30

++

+

=+

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

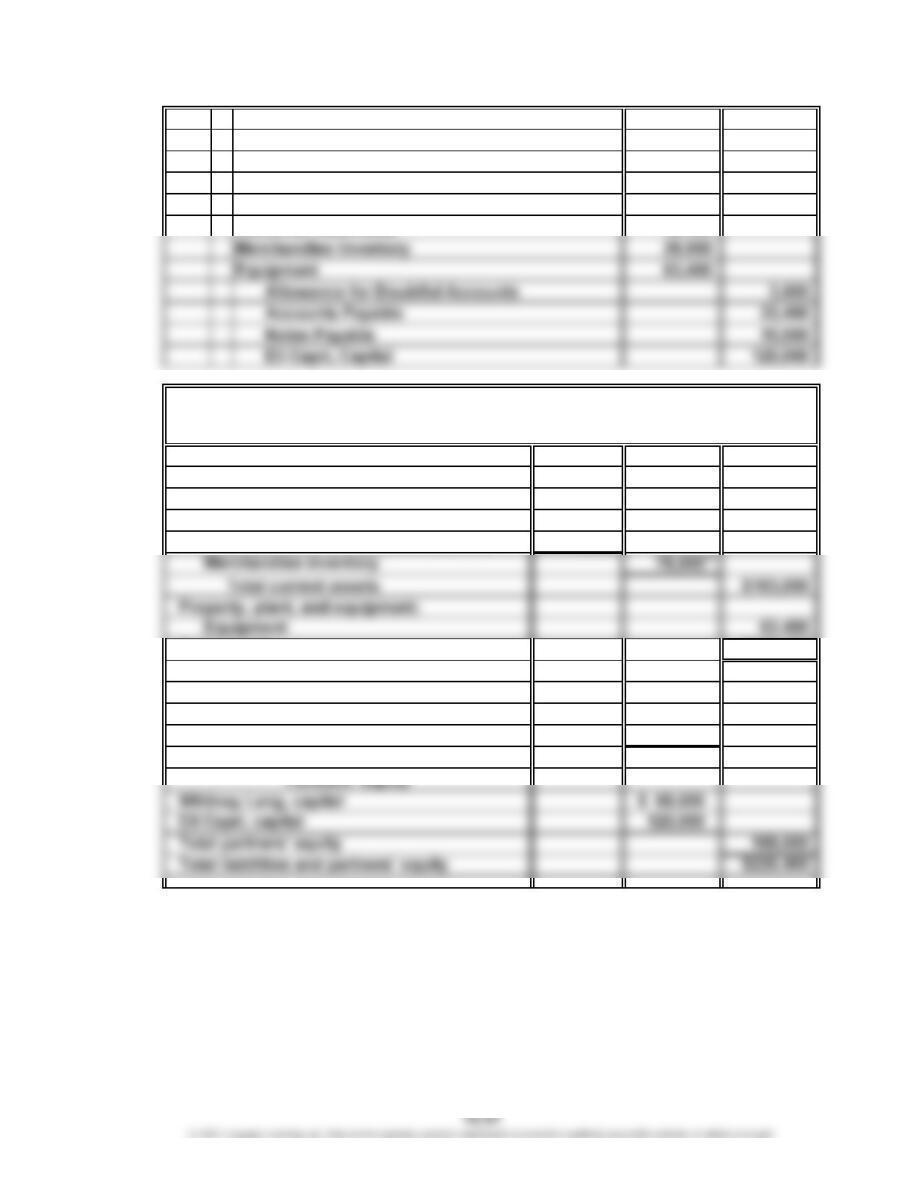

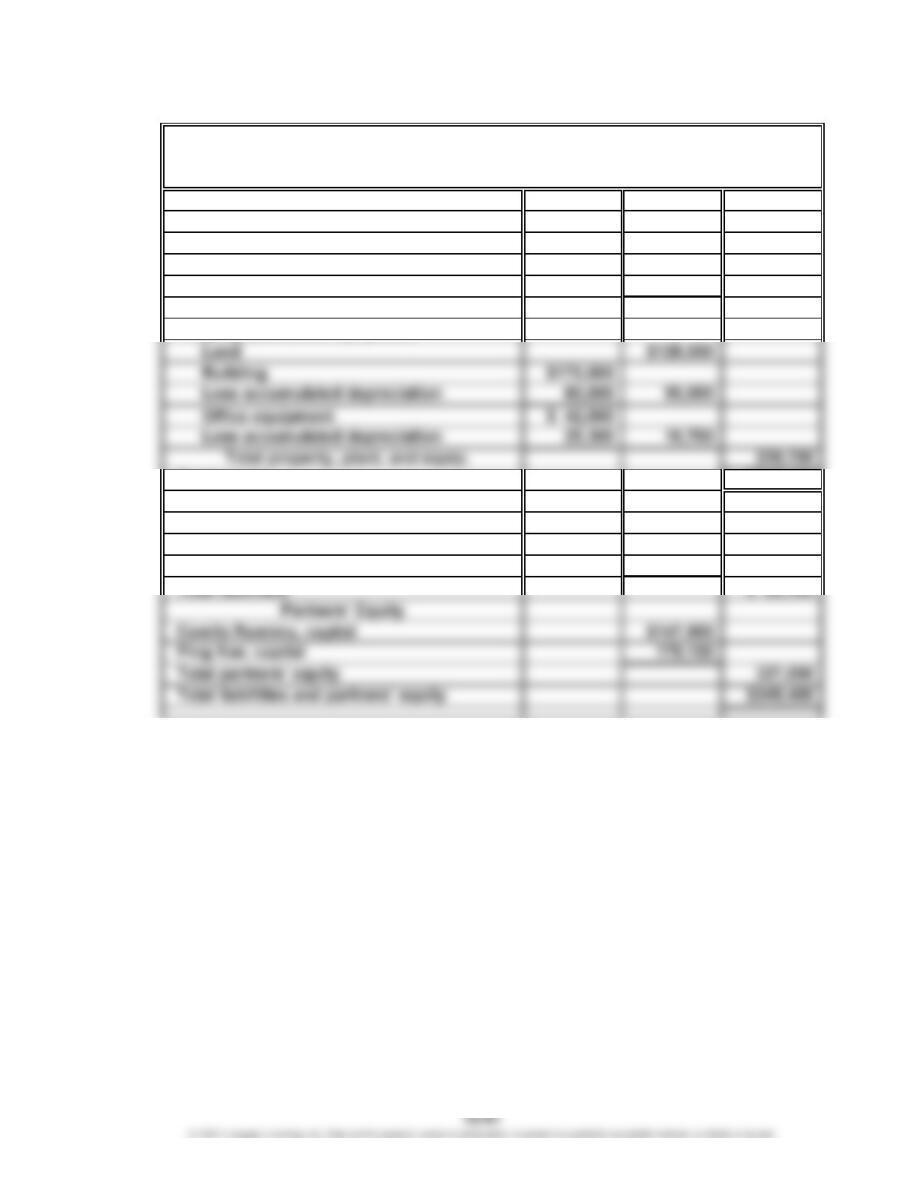

Prob. 12-1B

1. Apr. 1 Cash 18,000

Merchandise Inventory 50,000

Whitney Lang, Capital 68,000

1 Cash 26,200

2.

Current assets:

Cash $ 44,200

Accounts receivable $43,400

Less allowance for doubtful accounts 3,500 39,900

Total assets $226,400

Current liabilities:

Accounts payable $ 23,400

Notes payable 15,000

Total liabilities $ 38,400

*

$18,000 + $26,200

**

$28,900 + $50,000

Liabilities

Lang and Capri

Balance Sheet

April 1, 20Y1

Assets

*

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-1B (Concluded)

31 Whitney Lang, Capital 40,000

Eli Capri, Capital 30,000

Whitney Lang, Drawing 40,000

Eli Capri, Drawing 30,000

* Computations:

Total

Interest allowance…………………………

…

$ 6,800 $12,000 $ 18,800

Salary allowance……………………………

…

36,000 22,000 58,000

Lang Capri

12

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-2B

Plan Howell Nickles Howell Nickles

a. …………………………………

…

$210,000 $210,000 $ 75,000 $75,000

b. …………………………………

…

168,000 252,000 60,000 90,000

Details:

Nickles

a. Net income (1:1)……………

…

$210,000 $210,000 $ 75,000 $75,000

b. Net income (2:3)……………

…

$168,000 $252,000 $ 60,000 $90,000

…

…

…

…

…

…

…

…

f. Interest allowance…………

…

$ 5,000 $ 7,500 $ 5,000 $ 7,500

Salary allowance……………

…

38,000 19,000 38,000 19,000

Bonus allowance……………

…

72,600 18,600

Remaining income (1:1)……

…

138,950 138,950 30,950 30,950

Net income……………………

…

$254,550 $165,450 $ 92,550 $57,450

(1) (2)

$420,000 $150,000

Nickles HowellHowell

$420,000 $150,000

23

…

…

…

…

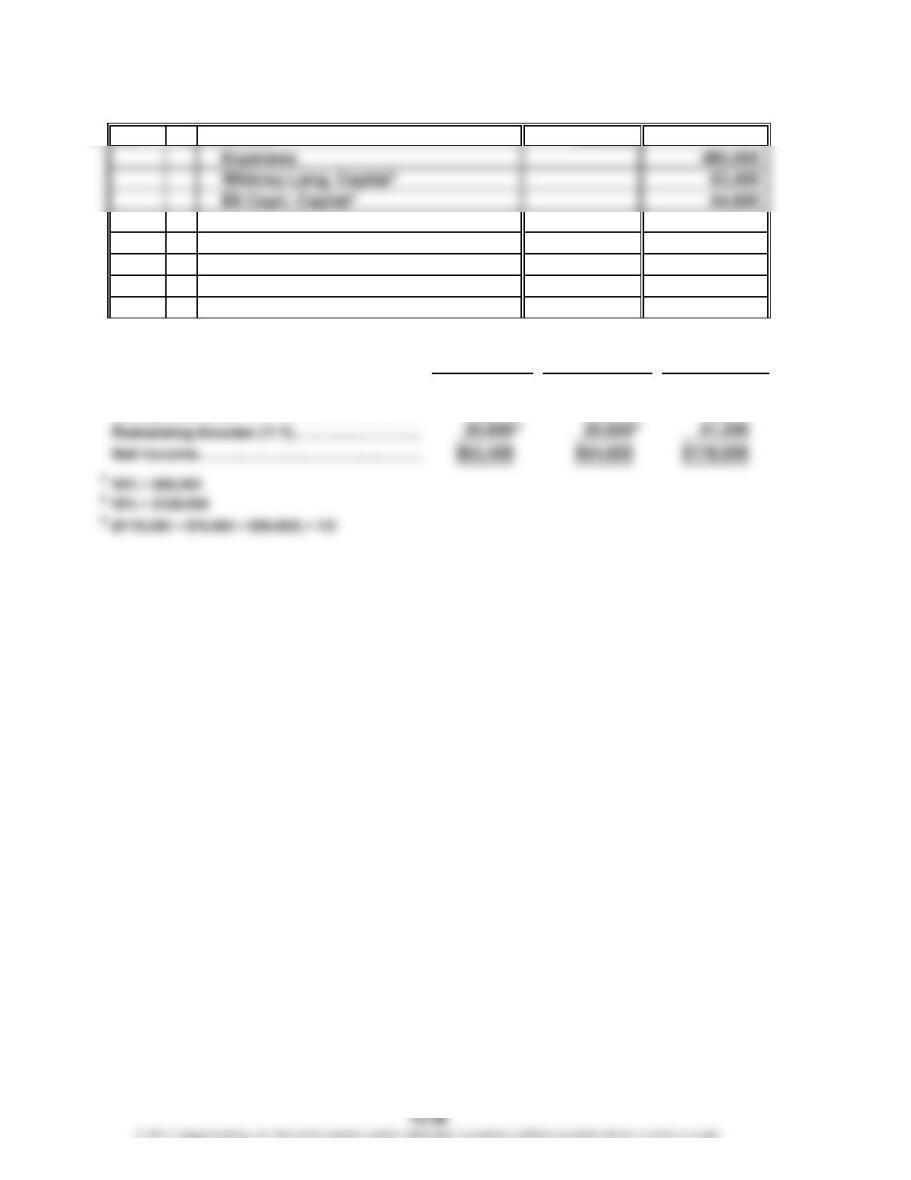

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-3B

1.

Professional fees

Operating expenses:

Salary expense

Depreciation expense—building

Heating and lighting expense

Division of net income:

Total

Salary allowance…………………………

…

$50,000 $65,000 $115,000

Interest allowance………………………… 15,000 16,200 31,200

Remaining income (loss) (1:1)…………

…

(7,100) (7,100) (14,200)

$57,900 $74,100 $132,000

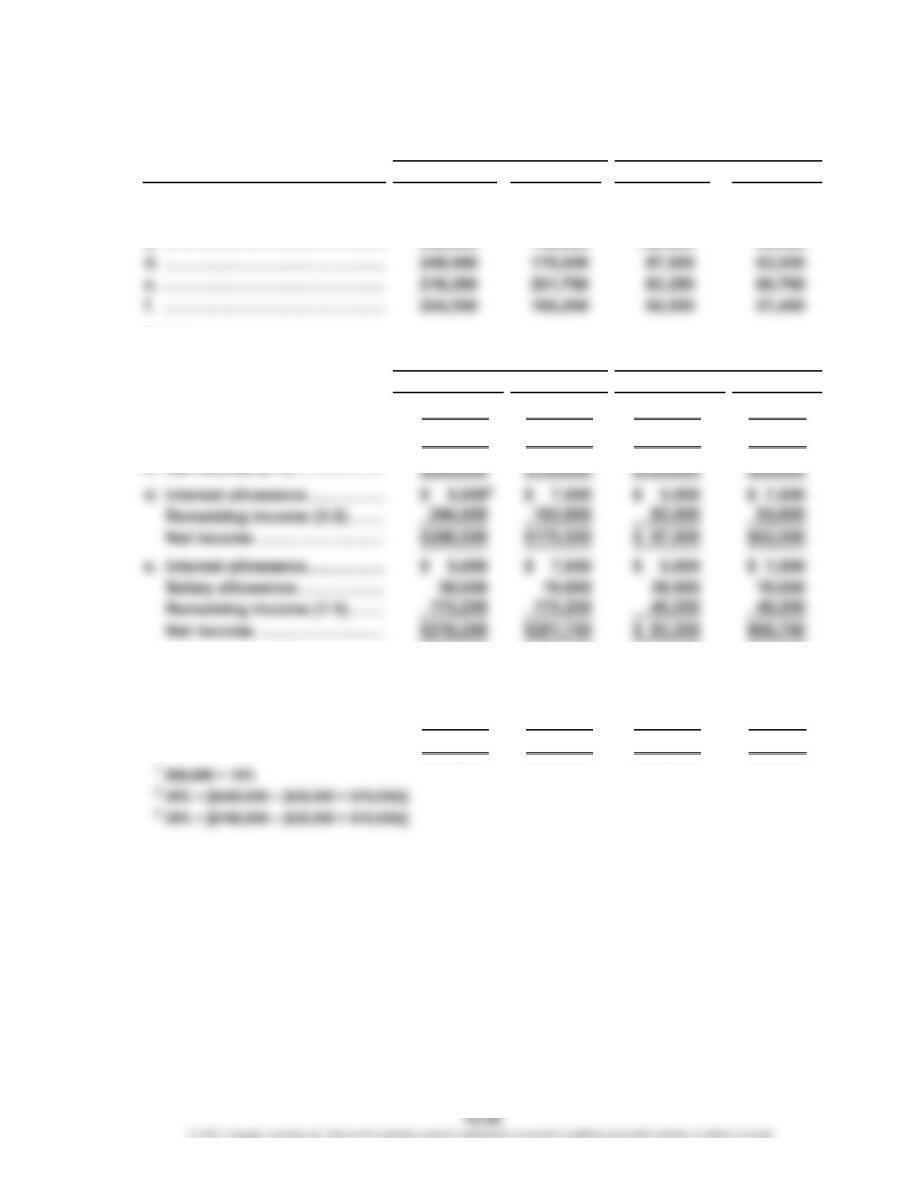

2.

Total

Balances, Januar

y

1, 20Y2

Ca

p

ital additions

20,000

$125,000

—20,000

Xue

$135,000

Ramirez

Ping

Ramirez and Xue

Camila

$260,000

Camila

Ramirez Xue

Ping

Statement of Partnership Equity

For the Year Ended December 31, 20Y2

10,500

Ramirez and Xue

Income Statement

For the Year Ended December 31, 20Y2

$555,300

$384,900

12,900

**

*

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

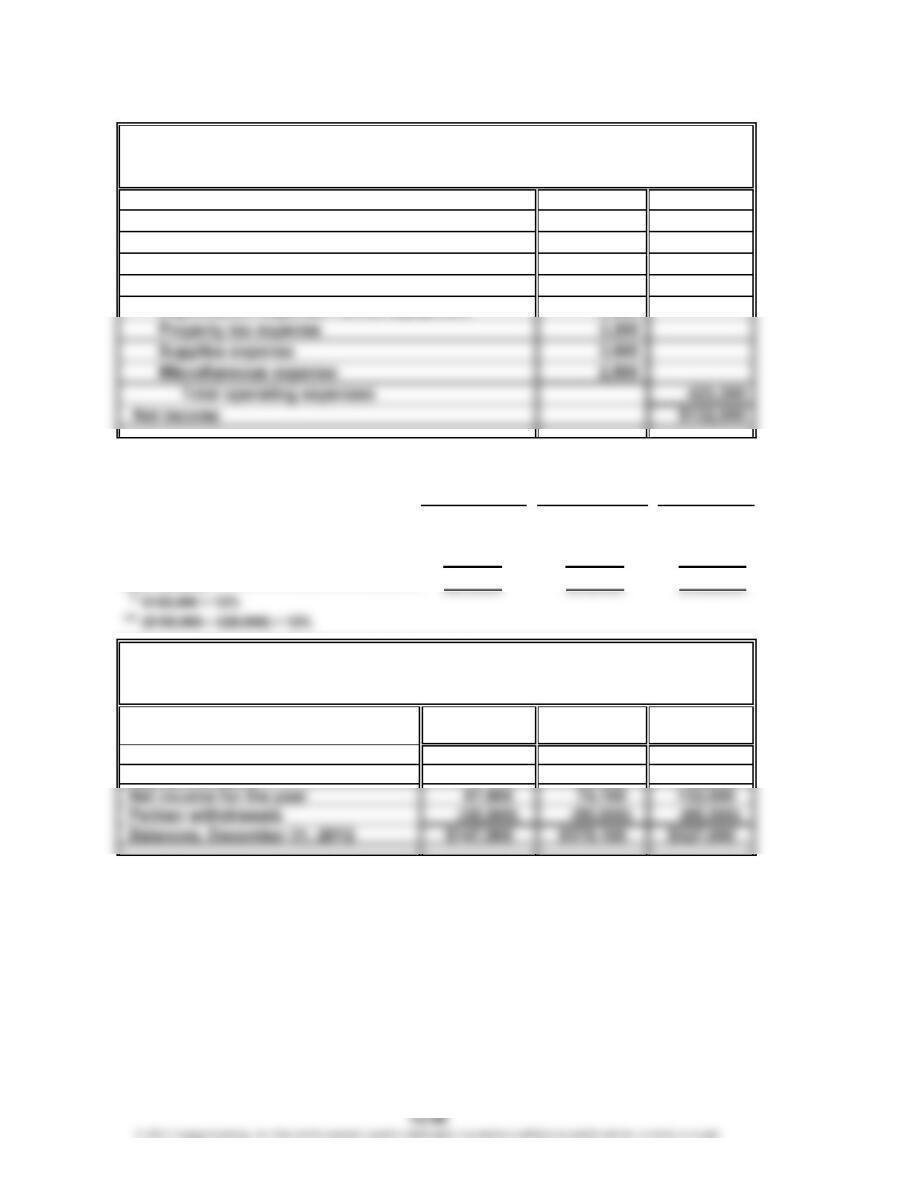

Prob. 12-3B (Concluded)

3.

Current assets:

Cash $ 70,300

Accounts receivable 33,600

Supplies 5,800

Total current assets $109,700

Property, plant, and equipment:

Total assets $349,400

Current liabilities:

Accounts payable $ 12,400

Salaries payable 10,000

Ramirez and Xue

Balance Sheet

December 31, 20Y2

Assets

Liabilities

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

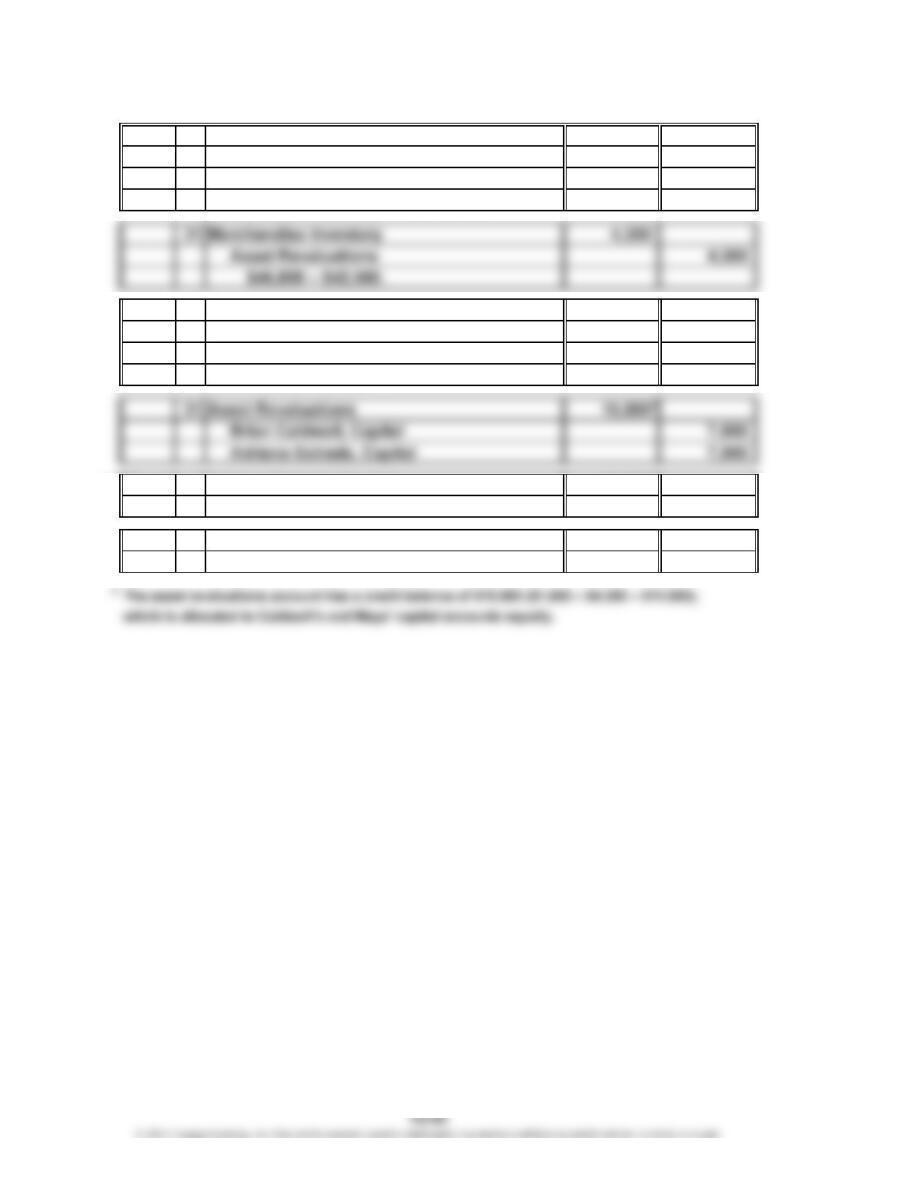

Prob. 12-4B

1. Aug. 31 Asset Revaluations 1,800

Accounts Receivable 1,500

Allowance for Doubtful Accounts 300

[($19,500 – $1,500) × 5%] – $600.

31 Accumulated Depreciation—Equipment 15,500

Equipment 3,000

Asset Revaluations 12,500

$64,500 – $67,500.

2. Sept. 1 Adriana Estrada, Capital 26,000

Kris Mays, Capital 26,000

1 Cash 32,000

Kris Mays, Capital 32,000

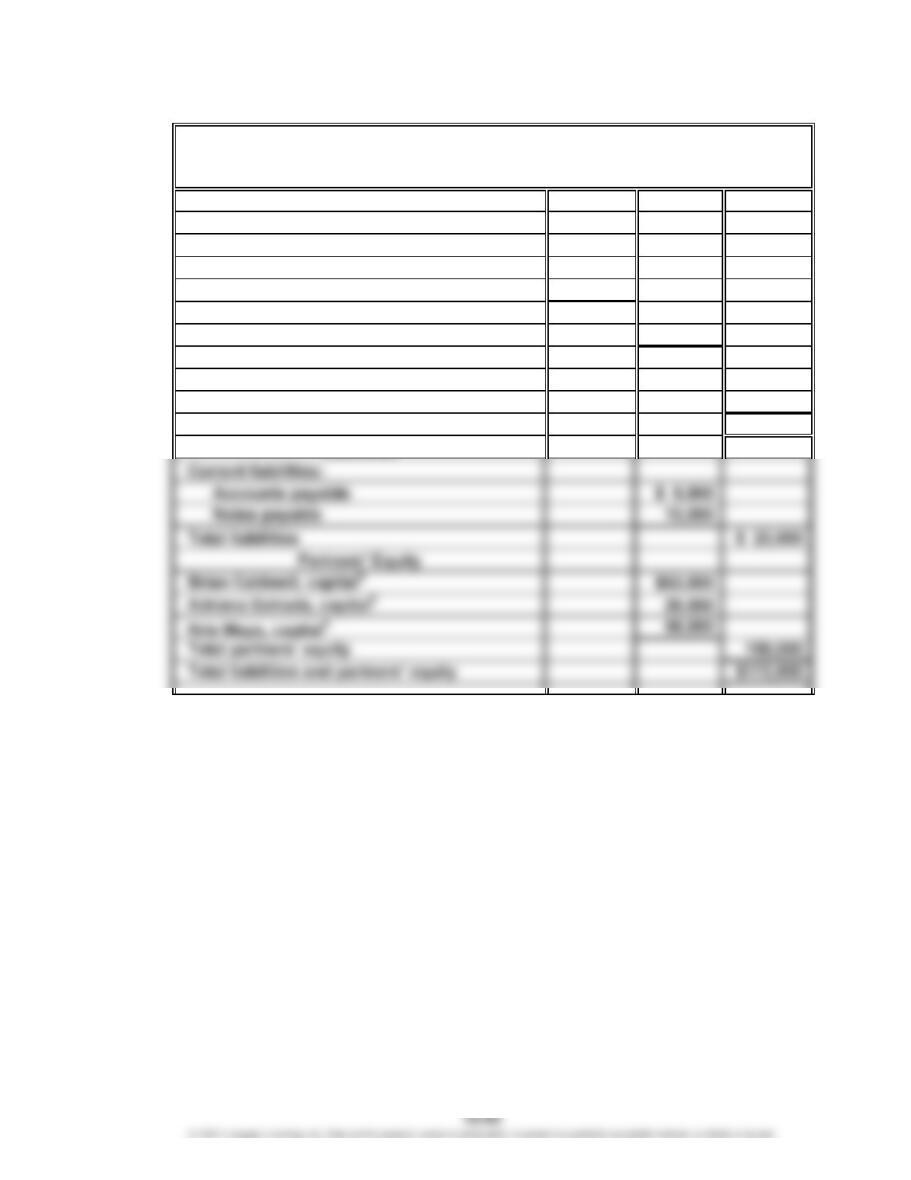

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-4B (Concluded)

3.

Current assets:

Cash1$44,300

Accounts receivable $18,000

Less allowance for doubtful accounts 900 17,100

Merchandise inventory 46,800

Prepaid insurance 1,200

Total current assets $109,400

Property, plant, and equipment:

Equipment 64,500

Total assets $173,900

1$12,300 + $32,000

2$55,000 + $7,500

3$48,000 + $7,500 – $26,000

4$26,000 + $32,000

Caldwell, Estrada, and Mays

Balance Sheet

September 1, 20Y9

Assets

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-5B

1.

Noncash Fairchild Lowes Howard

Cash Assets Liabilities (1/4) (1/4) (2/4)

Balances before realization $ 23,500 $ 84,500 $ 22,000 $ 42,000 $ 7,500 $ 36,500

a. Sale of assets and division of loss 48,500 (84,500) — (9,000) (9,000) (18,000)

Balances after realization $ 72,000 $ 0 $ 22,000 $ 33,000 $(1,500) $ 18,500

b. Payment of liabilities (22,000) — (22,000) — — —

2. a. Zach Fairchild, Capital

Amber Howard, Capital

Austin Lowes, Capital

The $1,500 deficiency of Lowes would be divided between the other partners, Fairchild and Howard, in their income-

sharing ratio (1:2, respectively). Therefore, Fairchild would absorb one-third of the $1,500 deficiency, or $500, and

Howard would absorb two-thirds of the $1,500 deficiency, or $1,000.

+++

Fairchild, Lowes, and Howard

Statement of Partnership Liquidation

For Period April 10–30

Capital

+=

1,500

500

1,000

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-6B

1. a.

Noncash Chapelle Rock Pryor

Cash Assets Liabilities (1/5) (2/5) (2/5)

Balances before realization $ 65,000 $ 167,000 $ 30,000 $ 14,000 $ 102,000 $ 86,000

Sale of assets and division of gain 217,000 (167,000) — 10,000 20,000 20,000

Balances after realization $ 282,000 $ 0 $ 30,000 $ 24,000 $ 122,000 $ 106,000

++=++

Chapelle, Rock, and Pryor

Statement of Partnership Liquidation

For Period August 3–29

Capital

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-6B (Concluded)

1. b.

Noncash Chapelle Rock Pryor

Cash Assets Liabilities (1/5) (2/5) (2/5)

Balances before realization $ 65,000 $ 167,000 $ 30,000 $ 14,000 $102,000 $ 86,000

Sale of assets and division of loss 72,000 (167,000) —(19,000) (38,000) (38,000)

Balances after realization $ 137,000 $ 0 $ 30,000 $ (5,000) $ 64,000 $ 48,000

2. a. Rock, Capital

Pryor, Capital

Chapelle, Capital

The $5,000 deficiency of Chapelle would be divided between the other partners, Rock and Pryor, in their income-

sharing ratio (1:1, respectively). Therefore, Rock would absorb one-half of the $5,000 deficiency, or $2,500, and Pryor

would absorb one-half of the $5,000 deficiency, or $2,500.

Chapelle, Rock, and Pryor

Statement of Partnership Liquidation

Capital

For Period August 3–29

2,500

2,500

+=+++

5,000

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

CP 12-1

This scenario highlights one of the problems that arises in partnerships:

attempting to align contribution with income division. Often, disagreements

are based on honest differences of opinion. However, in this scenario, there is

evidence that Robbins was acting unethically. Robbins apparently made no

mention of his plans to “scale back” once the partnership was consummated.

As a result, Barrow agreed to an equal division of income based on the

that way.

Barrow could respond to this situation by either withdrawing from the

partnership or changing the partnership agreement. One possible change

would be to provide a partner salary based on the amount of patient billings.

CASES & PROJECTS

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

CP 12-2

a. and b.

This table is from the 2018 “Accounting Today Top 100 Firms.”

Total Revenues Revenues

(in millions) per Partner*

Deloitte & Touche………………… $18,551 $5,917,384

PwC…………………………………

…

15,620 4,694,920

Ernst & Young……………………

…

13,000 4,062,500

KPMG………………………………

…

8,960 4,113,866

c.

Percent of

Revenue per Deloitte &

Partner Touche

Deloitte & Touche…………………

…

$5,917,384 100%

PwC…………………………………… 4,694,920 79%

KPMG…………………………………

…

4,113,866 70%

Ernst & Young………………………

…

4,062,500 69%

*

$4,694,920 ÷ $5,917,384

d. As can be seen, Deloitte & Touche has the highest revenue per partner relative to

Partners

3,135

3,327

3,200

2,178

Total

**

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

CP 12-3

When developing an LLC (or partnership), the operating (or partnership)

agreement is a critical part of establishing a business. Each party must consider

the various incentives of each individual in the LLC. For example, in this case,

one party, Lindsey Wilson, is providing all of the funding, while the other two

parties are providing expertise and talent. This type of arrangement can create

some natural conflicts because the interests of an investor might not be

the same as those operating the LLC. Specifically, you would want to advise

A second issue is the division of partnership income. The suggested agreement

is for all the partners to share the remaining income, after the 10% preferred return,

equally. Wilson should be counseled to consider all aspects of the LLC contribution

to determine whether this division is equitable. There are many considerations,

including the amount of investment, risk of the venture, degree of expertise of

noninvesting partners, and degree of exclusivity of noninvesting members’ effort

contribution (unique skills or business connections, for example). Often, the simple

assumption of equal division is not appropriate.

CP 12-4

A good solution to this problem would be to divide income into three steps:

1. Provide interest on each partner’s capital balance.

2. Provide a monthly salary for each partner.

3. Divide the remainder according to a partnership formula.

With this approach, the return on capital and effort will be calculated

separately in the income division formula before applying the percentage

formula. Thus, Willard will receive a large interest distribution based on the