Chapter 12 – Financial Statement Analysis

12-1

Chapter 12

Financial Statement Analysis

INSTRUCTOR’S MANUAL

Learning Objectives

LO12-1 Perform vertical analysis.

LO12-2 Perform horizontal analysis.

LO12-3 Use ratios to analyze a company’s risk.

LO12-4 Use ratios to analyze a company’s profitability.

LO12-5 Distinguish persistent earnings from one-time items.

LO12-6 Distinguish between conservative and aggressive accounting practices.

Chapter 12 – Financial Statement Analysis

12-2

Teaching Suggestions

Chapter 12 adopts an underlying sports theme to demonstrate the basic tools used in financial

statement analysis.

Part A introduces vertical and horizontal analysis using actual financial statements from

Under Armour and Nike. Vertical analysis controls for differences in company size, making

comparisons among companies of different size possible. Horizontal analysis allows users to

analyze trends in financial statement data for a single company over time. The horizontal

analysis of Under Armour’s financial statements demonstrates the large growth in company

operations during the year. The horizontal analysis of Nike’s financial statements is included in a

Let’s Review problem at the end of this section.

Part B uses ratio analysis to provide a detailed assessment of risk and profitability for Under

Armour, comparing the results to the sports apparel industry leader, Nike. We review 14 ratios

separated into two categories: risk ratios and profitability ratios. Ratio analysis is presented in a

separate section at the end of each chapter, beginning in Chapter 5. These same ratios are

included in a comprehensive example here in Chapter 12 to give instructors maximum flexibility

in the coverage of ratios. Instructors can cover ratios chapter by chapter, save the coverage of

ratios until the final chapter, or combine these two approaches by introducing the ratios in each

chapter and then bringing all of the ratios together in this final chapter. Some instructors even

save this chapter for the next semester to include it in the managerial accounting class.

Part C addresses earnings persistence and earnings quality. Discontinued operations are part

of net income in the current year but are not expected to persist beyond the current year. The

decision maker’s perspective near the end of this section, titled “Does Location in the Income

Statement Matter?,” helps students see that sometimes it’s not just the final net income number

that’s important—the location of the item in the income statement matters as well. The final

section on earnings quality was written based on reviewer feedback regarding the need to help

students better recognize conservative versus aggressive accounting practices. Major topics from

Chapters 5, 6, 7, and 8 are used as examples of both conservative accounting practices (as

prepared by Mr. Nadal) and aggressive accounting practices (as prepared by Mr. Djokovic) to

help students better understand the subjectivity inherent within accounting standards.

Chapter 12 – Financial Statement Analysis

12-3

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO12-1, 12-2

Identify types of comparisons commonly used in

financial statement analysis

5

2

LO12-1, 12-2

Explain the difference between vertical and

horizontal analysis

5

3

LO12-1

Describe the base amounts commonly used in

vertical analysis

5

4

LO12-1

Identify the relative age of a company based on the

size of its common stock and retained earnings

balances

5

5

LO12-2

Explain why it is important to look at both the

amount and percentage change in horizontal

analysis

5

6

LO12-3

Explain why some ratios use average rather than

ending balance sheet amounts

5

7

LO12-3

Describe the difference between liquidity and

solvency

5

8

LO12-3

Relate risk ratios with financial questions

5

9

LO12-3

Determine whether each of the following changes in

risk ratios is good news or bad news about a

company

5

10

LO12-3

Describe the effect of a transaction on the current

ratio

5

11

LO12-4

Relate profitability ratios with financial questions

5

12

LO12-4

Determine whether each of the following changes in

profitability ratios is good news or bad news about a

company

5

13

LO12-4

Explain why the return on assets and the return on

equity differ

5

14

LO12-5

Explain how earnings persistence relate to the

reporting of discontinued operations

5

15

LO12-5

Examine a trend in earnings per share before and

after discontinued operations

5

16

LO12-6

Explain the difference between conservative and

aggressive accounting practices

5

17

LO12-6

Explain why an accounting practice is conservative

5

18

LO12-6

Explain why an accounting practice is aggressive

5

19

LO12-6

Examine year-end adjustments for a common trend

5

20

LO12-6

Provide an example of a change in accounting

practice that has no effect on cash flows

5

Chapter 12 – Financial Statement Analysis

12-4

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE12-1

LO12-1

Prepare vertical analysis

15

BE12-2

LO12-2

Prepare horizontal analysis

15

BE12-3

LO12-1

Understand vertical analysis

10

BE12-4

LO12-2

Understand horizontal analysis

5

BE12-5

LO12-2

Understand percentage change

5

BE12-6

LO12-3

Calculate receivables turnover

5

BE12-7

LO12-3

Calculate inventory turnover

5

BE12-8

LO12-3

Understand inventory turnover

5

BE12-9

LO12-3

Understand the current ratio

10

BE12-10

LO12-4

Calculate profitability ratios

15

BE12-11

LO12-4

Calculate profitability ratios

10

BE12-12

LO12-5

Record discontinued operations

10

BE12-13

LO12-5

Classify income statement items

10

BE12-14

LO12-6

Distinguish between conservative and aggressive

accounting practices

10

BE12-15

LO12-6

Distinguish between conservative and aggressive

accounting practices

10

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E12-1

LO12-1, 12-2,

12-3, 12-4,

12-5, 12-6

Match terms with their definitions

20

E12-2

LO12-1

Prepare vertical analysis

15

E12-3

LO12-2

Prepare horizontal analysis

15

E12-4

LO12-1, 12-2

Prepare vertical and horizontal analyses

30

E12-5

LO12-3

Evaluate risk ratios

30

E12-6

LO12-4

Evaluate profitability ratios

30

E12-7

LO12-3

Calculate risk ratios

30

E12-8

LO12-4

Calculate profitability ratios

30

E12-9

LO12-4

Calculate profitability ratios

30

E12-10

LO12-4

Calculate profitability ratios

20

E12-11

LO12-5

Classify income statement items

15

E12-12

LO12-5

Record discontinued operations

20

E12-13

LO12-5

Record discontinued operations and other expenses

15

E12-14

LO12-6

Distinguish between conservative and aggressive

accounting practices

10

E12-15

LO12-6

Distinguish between conservative and aggressive

accounting practices

10

Chapter 12 – Financial Statement Analysis

12-5

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P12-1A

LO12-1

Perform vertical analysis

20

P12-2A

LO12-2

Perform horizontal analysis

20

P12-3A

LO12-1, 12-2

Perform vertical and horizontal analyses

30

P12-4A

LO12-3

Calculate risk ratios

30

P12-5A

LO12-4

Calculate profitability ratios

20

P12-6A

LO12-3, 12-4

Use ratios to analyze risk and profitability

45

P12-1B

LO12-1

Perform vertical analysis

20

P12-2B

LO12-2

Perform horizontal analysis

20

P12-3B

LO12-1, 12-2

Perform vertical and horizontal analyses

30

P12-4B

LO12-3

Calculate risk ratios

30

P12-5B

LO12-4

Calculate profitability ratios

20

P12-6B

LO12-3, 12-4

Use ratios to analyze risk and profitability

45

Additional

Perspectives

Topic

Time

(Min.)

AP12-1

Continuing Problem: Great Adventures

45

AP12-2

Financial Analysis: American Eagle Outfitters, Inc.

45

AP12-3

Financial Analysis: The Buckle, Inc.

45

AP12-4

Comparative Analysis: American Eagle Outfitters, Inc. vs. The

Buckle, Inc.

50

AP12-5

Ethics

20

AP12-6

Internet Research

20

AP12-7

Written Communication

20

AP12-8

Earnings Management

20

Chapter 12 – Financial Statement Analysis

12-6

Chapter Quiz Questions

The following multiple-choice questions are 10 unique quiz questions that correspond to the 10

questions at the end of each chapter. Each question covers the same learning objective but with a

little different twist. The correct answer is highlighted in bold for each item.

LO12-1

1. Common size analysis is more often referred to as:

LO12-1

2. When using vertical analysis, we express balance sheet accounts as a percentage of:

d. Sales.

LO12-2

3. Which of the following is an example of horizontal analysis?

LO12-2

4. Which of the following is an example of horizontal analysis?

LO12-3

5. Which of the following ratios is not considered to be a liquidity ratio?

Chapter 12 – Financial Statement Analysis

12-7

LO12-3

6. Which of the following is a negative indicator regarding a company’s ability to turn its

receivables into cash?

LO12-4

7. Performance, Inc., reports net income of $100,000, sales of $800,000, and average assets of

$500,000. The profit margin is:

LO12-4

8. Performance, Inc., reports net income of $100,000, sales of $800,000, and average assets of

$500,000. The asset turnover is:

a. 0.20 times.

LO12-5

9. Power Equipment incurred a material loss due to business restructuring. This loss should be

reported as:

a. Selling expenses.

LO12-6

10. Which of the following is an example of an aggressive accounting practice in relation to the

reporting of net income?

Chapter 12 – Financial Statement Analysis

12-8

Alternate Let’s Review

Problem #1

The income statements and balance sheets for Incredible Sports are as follows:

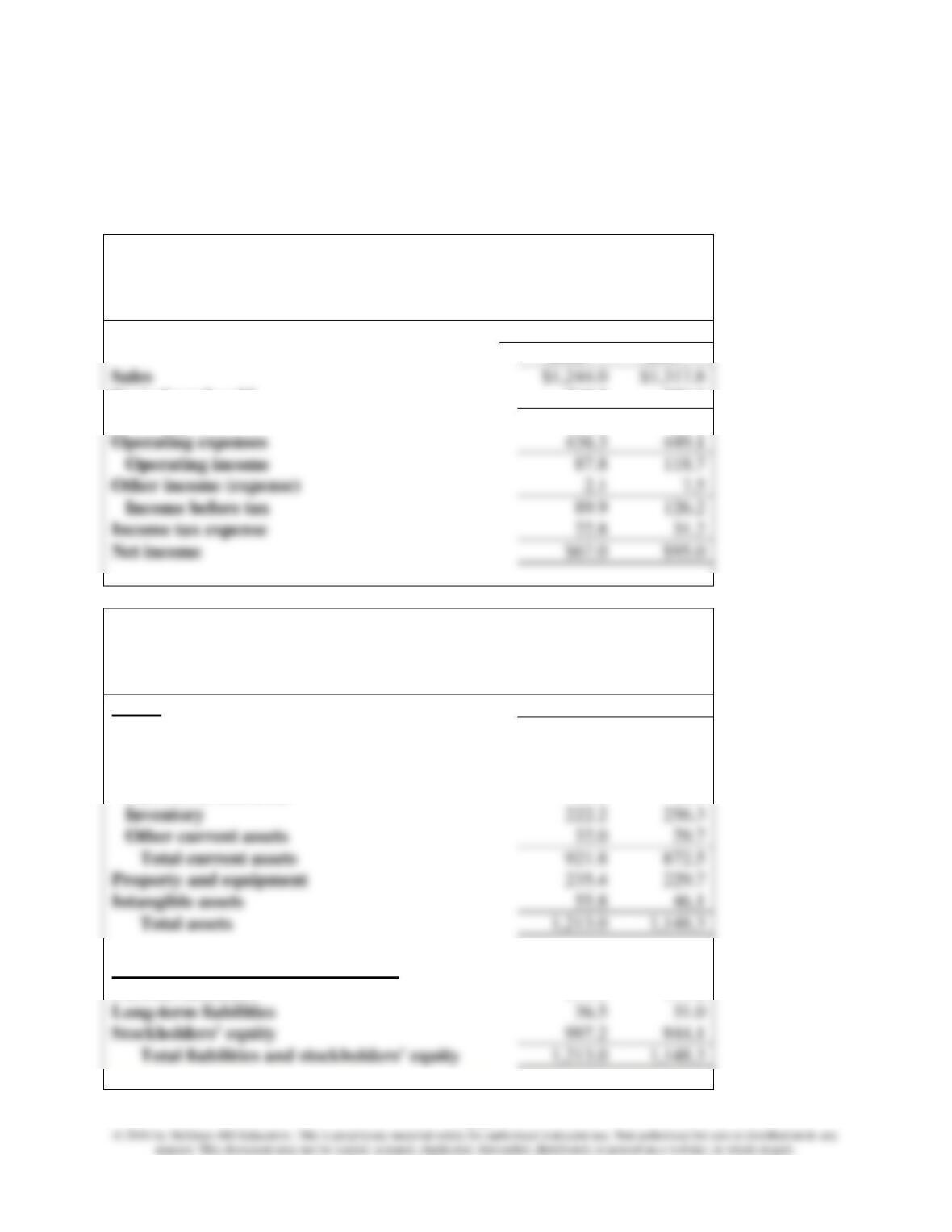

Incredible Sports

Income Statements

For the Years Ended December 31

(in millions)

2018

2017

Sales

Cost of goods sold

719.9

750.0

Gross profit

524.1

567.8

Operating expenses

436.3

449.1

Operating income

87.8

118.7

Other income (expense)

Income before tax

89.9

126.2

Income tax expense

22.8

31.2

Net income

$67.0

$95.0

Incredible Sports

Balance Sheets

December 31

(in millions)

Assets

2018

2017

Current assets:

Cash

$386.7

$230.6

Net receivables

258.1

333.5

Current investments

22.8

22.4

Inventory

222.2

256.3

Other current assets

32.0

29.7

Total current assets

921.8

872.5

Property and equipment

235.4

229.7

Total assets

Liabilities and Stockholders’ Equity

Current liabilities

179.3

173.2

Long-term liabilities

36.5

31.0

997.2

944.1

Chapter 12 – Financial Statement Analysis

12-9

Required:

Calculate the following risk ratios for the year ended December 31, 2018.

Solution:

Risk Ratios

Calculations

Liquidity

Receivables turnover ratio

$1,244.0

($258.1 + $333.5) / 2

= 4.2 times

Average collection period

= 86.9 days

Inventory turnover ratio

($222.2 + $256.3) / 2

= 3.0 times

Average days in inventory

= 121.7 days

Current ratio

= 5.1 to 1

Acid-test ratio

= 3.7 to 1

Debt to equity ratio

= 21.6%

12-10

Problem #2

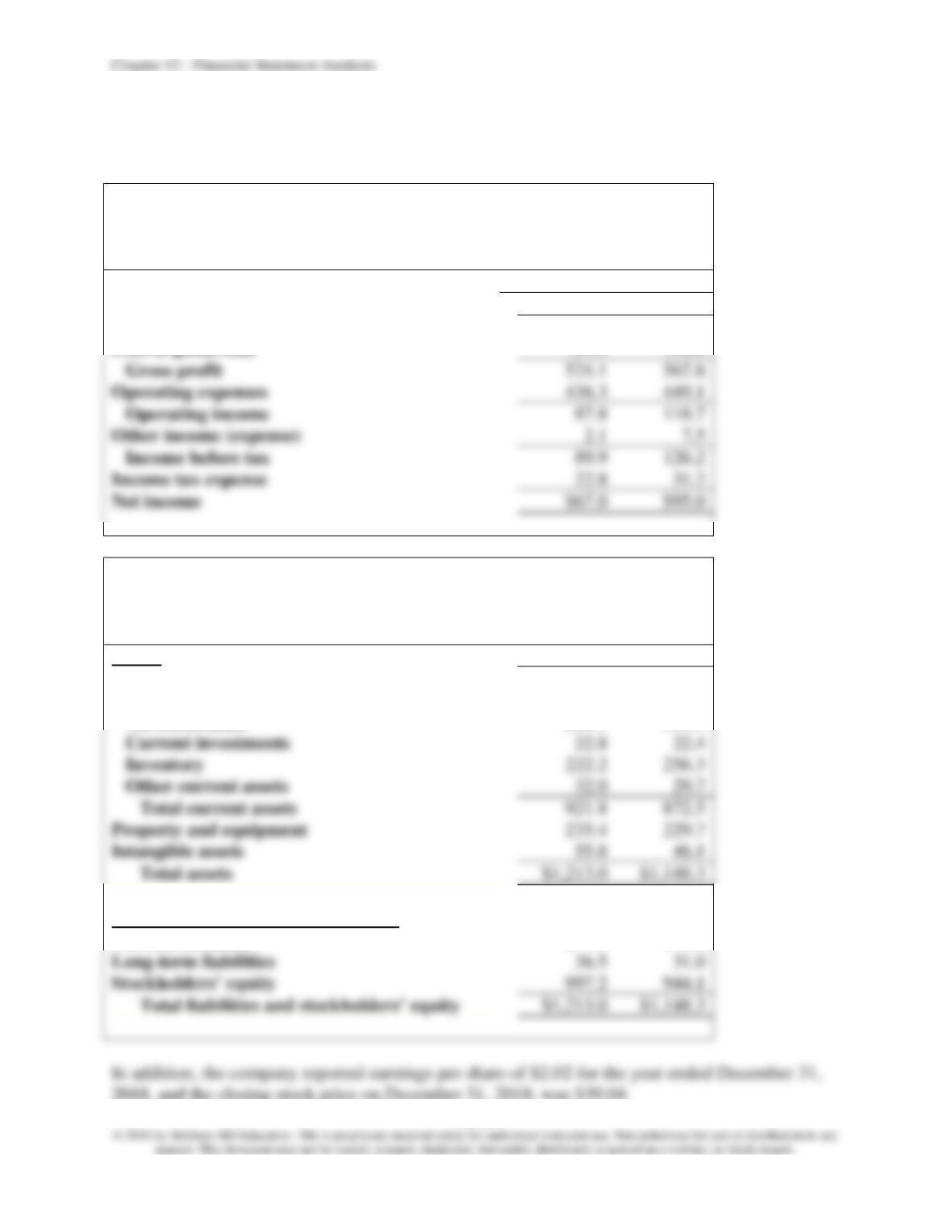

The income statements and balance sheets for Incredible Sports are as follows:

Incredible Sports

Income Statements

For the Years Ended December 31

(in millions)

2018

2017

Sales

$1,244.0

$1,317.8

Cost of goods sold

719.9

750.0

Gross profit

524.1

567.8

Operating expenses

436.3

449.1

Operating income

118.7

Other income (expense)

Income before tax

126.2

Income tax expense

Net income

$67.0

$95.0

Incredible Sports

Balance Sheets

December 31

(in millions)

Assets

2018

2017

Current assets:

Cash

$386.7

$230.6

Net receivables

258.1

333.5

Current investments

Inventory

222.2

256.3

Other current assets

Total current assets

921.8

872.5

Property and equipment

235.4

229.7

Intangible assets

Total assets

$1,213.0

$1,148.3

Liabilities and Stockholders’ Equity

Current liabilities

179.3

173.2

Long-term liabilities

Stockholders’ equity

997.2

944.1

$1,213.0

$1,148.3

2018, and the closing stock price on December 31, 2018, was $39.04.

Chapter 12 – Financial Statement Analysis

12-11

Required:

Calculate the six profitability ratios we’ve discussed for Incredible Sports for the year ended

December 31, 2018.

Solution:

Profitability Ratios

Calculations

Gross profit ratio

$524.1

$1,244.0

= 42.1%

Profit margin

$1,244.0

= 5.4%

Asset turnover

= 1.1 times

Return on equity

= 6.9%

Price-earnings ratio

$39.04

= 19.3

Chapter 12 – Financial Statement Analysis

12-12

Problem #3

Required:

Classify each of the following accounting practices as conservative or aggressive.

1. Decrease the allowance for uncollectible accounts.

2. Decrease the useful life for calculating depreciation.

3. Reduce the amount of a contingent liability reported for litigation.

4. Record a larger expense for warranties.

5. When costs are going up, change from LIFO to FIFO.

Solution:

Chapter 12 – Financial Statement Analysis

12-13

Key Points by Learning Objective

LO12-1 Perform vertical analysis.

LO12-2 Perform horizontal analysis.

LO12-3 Use ratios to analyze a company’s risk.

LO12-4 Use ratios to analyze a company’s profitability.

LO12-5 Distinguish persistent earnings from one-time items.

LO12-6 Distinguish between conservative and aggressive accounting practices.

Chapter 12 – Financial Statement Analysis

12-14

Common Mistakes

Common Mistake

In comparing an income statement account with a balance sheet account, some students

incorrectly use the balance sheet account’s ending balance, rather than the average of its

Chapter 12 – Financial Statement Analysis

12-15

Decision Points

Question

Accounting Information

Analysis

Question

Accounting Information

Analysis

How do we compare

income between companies

Common-size income

statements

A vertical analysis using common-

size income statements allows for

Chapter 12 – Financial Statement Analysis

Career Corner

Career Corner

Investors and creditors, as well as suppliers, customers, employees, and the government, among

others, rely heavily on financial accounting information. Who checks big companies like Under

Armour and Nike to make sure they are reporting accurately? Auditors. Many accounting majors

begin their careers in auditing. They then use the experience they gain in auditing to obtain

management and accounting positions in private industry, sometimes even with a company they

previously audited.

Chapter 12 – Financial Statement Analysis

Ethical Dilemma

Ethical Dilemma

Michael Hechtner was recently hired as an assistant controller for Athletic Persuasions, a

recognized leader in the promotion of athletic events. However, the past year has been a difficult

one for the company’s operations. In order to help with slowing sales, the company has extended

credit to more customers and accepted payment over longer time periods, resulting in a

significant increase in accounts receivable. Similarly, with slowing sales, its inventory of

promotional supplies has increased dramatically.

One afternoon, Michael joined the controller, J.P. Sloan, for a visit with their primary lender,

First National Bank. Athletic Persuasions had used up its line of credit and was looking to

borrow additional funds. In meeting with the loan officer at the bank, Michael was surprised at

the positive spin J.P. Sloan put on the company operations. J.P. exclaimed, “Athletic Persuasions

continues to prosper in a difficult environment. Our current assets have significantly increased in

relation to current liabilities, resulting in a much improved current ratio over the prior year. It

seems wherever I look, the company has been successful.”

Is there anything unethical in the controller’s statement to the banker? What should Michael

do in this situation? Is it acceptable for Michael just to keep quiet?

Key Issues

• When does putting a positive spin on a situation become unethical?

• What action, if any, should Michael take in this situation?