BYP 12-3 RESEARCH CASE

(a) At the end of 2009 the nonfinancial companies in the Standard and

(b) First, cash (and short term investments) do not generate a very good

return. Thus, having too much cash on your balance sheet can drag down

the return on assets. Second, managers worry that if they accumulate too

(c) In order to motivate its managers to accumulate cash, Alcoa pegged

the compensation of its top executives to cash goals. In response, top

(d) At the time the article was written the stock prices of the Standard and

Poor’s 500 was 29% below its October 2007 peak. As a consequence,

(e) In addition to acquisitions, companies can increase their dividends or

do stock buybacks (buy treasury shares).

BYP 12-4 RESEARCH CASE

(a) The stock was issued at a price of $70 per share. A few months

previously it sold for more than $300 per share.

(b) The company issued shares of stock, even though its stock price was

BYP 12-5 INTERPRETING FINANCIAL STATEMENTS

(a) Current ratio —2001: $1,207.9 ÷ $ 921.4 = 1.31

—2004: $2,539.4 ÷ $1,620.4 = 1.57

Current cash debt

(b) Cash debt

coverage—2001: ($119.8) ÷ $3,090.0 = (.04) times

(c) Free cash flow —2001: ($119.8) – $50.3 – $0 = ($170.1)

BYP 12-5 (Continued)

(d) While these measures tell us a lot about Amazon.com, they don’t tell us

whether the stock price is reasonable. Amazon.com’s high stock price

BYP 12-6 REAL-WORLD FOCUS

Answers will vary depending on the company chosen by the student.

BYP 12-7 DECISION MAKING ACROSS THE ORGANIZATION

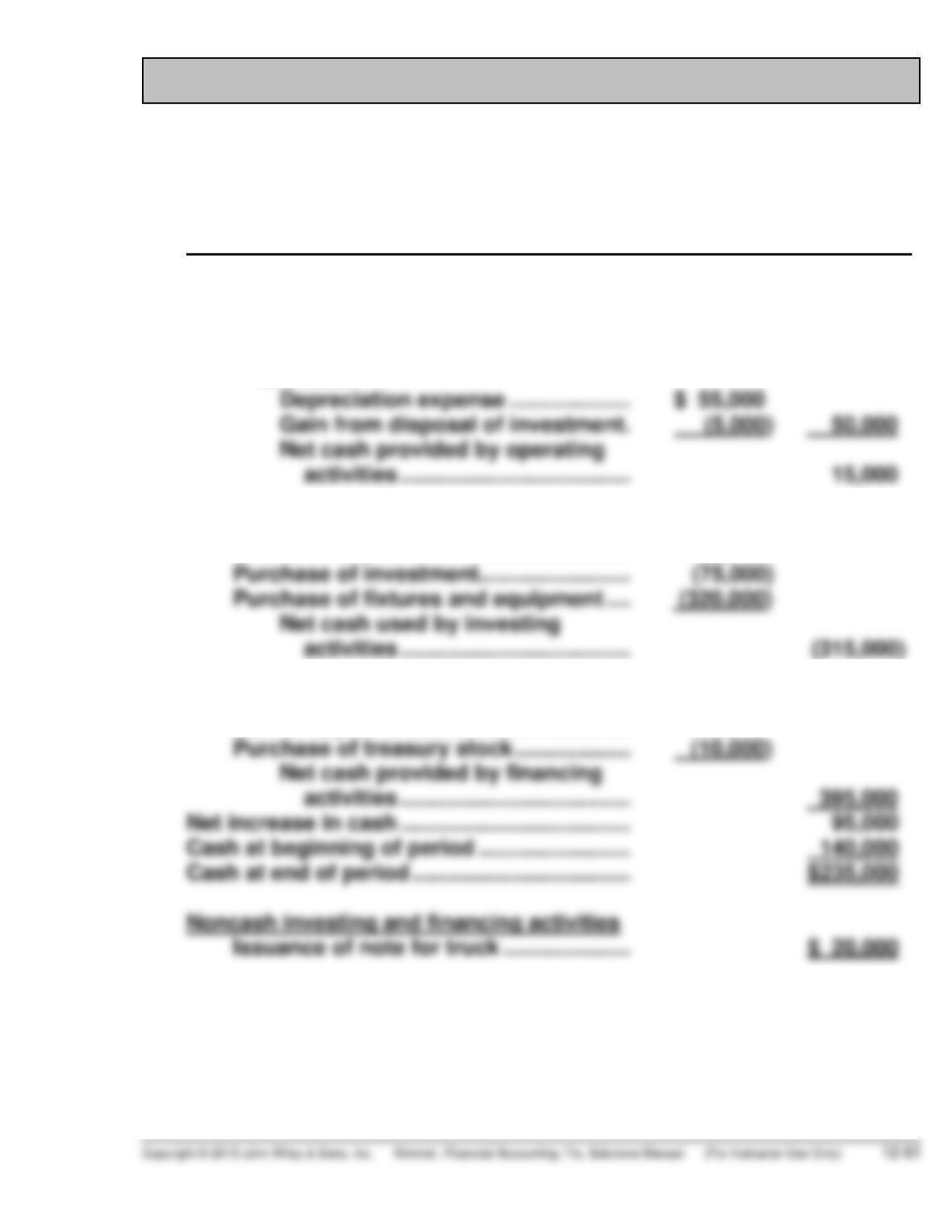

(a) GILBERT COMPANY

Statement of Cash Flows

For the Year Ended January 31, 2014

Cash flows from operating activities

Net loss …………………………………………… $ (35,000)*

Adjustments to reconcile net income

to net cash provided by operating

activities:

Cash flows from investing activities

Sale of investment …………………………… 80,000

Cash flows from financing activities

Sale of capital stock …………………………. 405,000

BYP 12-7 (Continued)

*Computation of net income (loss)

Sales of merchandise ………………………….. $385,000

(b) From the information given, it appears that from an operating stand-

point, Gilbert Company did not have a superb first year, having suf-

fered a $35,000 net loss. Robyn is correct; the statement of cash flows

BYP 12-8 COMMUNICATION ACTIVITY

MEMO

To: Jack Werth

From: Student

Re: Statement of cash flows

The statement of cash flows provides information about the cash receipts

and cash payments of a firm, classified as operating, investing, and financing

activities. The operating activities section of the company’s statement of

The financing activities section of the statement reports cash flows resulting

from changes in long-term liabilities and stockholders’ equity. The company

BYP 12-9 ETHICS CASE

(a) The stakeholders in this situation are:

Rick Hanigan, president of Templeton Automotive Corporation.

(b) The president’s statement, “We must get that amount above $1 million,”

puts undue pressure on the controller. This statement along with his

(c) It is unlikely that any board members (other than board members who

are also officers of the company) would discover the misclassification.

Board members generally do not have detailed enough knowledge of

their company’s transactions to detect this misstatement. It is possible

BYP 12-10 ALL ABOUT YOU

(a) The article describes three factors that determine how much money

you should set aside. (1) Your willingness to take risk. You need to evaluate

how willing you are to experience wide swings in your financial position.

(2) Your needs. You need to carefully evaluate your situation and evaluate

(b) They recommend having at least three months of living expenses set

aside, and up to six months.

(c) Responses to this question will vary. What is most important is that

BYP 12-11 FASB CODIFICATION ACTIVITY

(a) Cash equivalents are short-term, highly liquid investments that have

both of the following characteristics:

a. Readily convertible to known amounts of cash

b. So near their maturity that they present insignificant risk of changes

in value because of changes in interest rates.

Generally, only investments with original maturities of three months or

less qualify under that definition. Original maturity means original

(b) Financing activities include obtaining resources from owners and

providing them with a return on, and a return of, their investment;

(c) Investing activities include making and collecting loans and acquiring

and disposing of debt or equity instruments and property, plant, and

BYP 12-11 (Continued)

(d) Operating activities include all transactions and other events that are

not defined as investing or financing activities (see paragraph 230-10-

(e) The primary objective of a statement of cash flows is to provide

relevant information about the cash receipts and cash payments of an

entity during a period.

As indicated in the glossary at this same section, cash includes not

only currency on hand but demand deposits with banks or other

(f) Information about all investing and financing activities of an entity

during a period that affect recognized assets or liabilities but that do

IFRS CONCEPTS AND APPLICATION

IFRS 12-1

Under IFRS bank overdrafts are treated as part of cash and cash

equivalents on the balance sheet. As a result, on the statement of cash

IFRS 12-2

The treatment of these items under IFRS and GAAP is as follows:

IFRS GAAP

(a) Interest paid Operating or financing Operating

IFRS 12-3

IFRS 12-4 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) The company reports interest paid as an operating activity.

(b) Zetar’s balance in cash and cash equivalents is negative because the

(c) Under GAAP bank overdrafts are not reported in cash and cash

equivalents. Instead they are treated as a financing activity, and would

be reported on the balance sheet as a liability.