12–35

PROBLEM 12-50 (45 MINUTES)

1.

a.

The semiannual installments and total bonus for the Charter Division are

calculated as follows:

COMMLINE EQUIPMENT CORPORATION: CHARTER DIVISION

GAIN-SHARING BONUS CALCULATION

FOR THE YEAR ENDED DECEMBER 31, 20X1

First installment, January–June:

$18,480

Sales returns

Semiannual installment …………………………………..

First semiannual bonus awarded …………………………

Second installment, July–December:

Sales returns

Semiannual installment …………………………………..

Second semiannual bonus awarded …………………….

Total bonus awarded for the year ………………………..

$17,600

b.

The employees of the Charter Division are likely to be frustrated by the new plan,

since the division bonus is more than $40,000 less than that of the previous

12–36

PROBLEM 12-50 (CONTINUED)

2.

a.

The semiannual installments and total bonus for the Mesa Division are

calculated as follows:

COMMLINE EQUIPMENT CORPORATION: MESA DIVISION

GAIN-SHARING BONUS CALCULATION

FOR THE YEAR ENDED DECEMBER 31, 20X1

First installment, January–June:

Profitability (.02 $684,000) …………………………...

$13,680

Rework [(.02 $684,000) – $12,000] …………………

-0-*

Sales returns

{[(.015 $5,700,000) – $89,500] 50%} ……..

Semiannual installment …………………………………..

First semiannual bonus awarded …………………………

Second installment, July-December:

Profitability (.02 $812,000) …………………………...

$16,240

Rework [(.02 $812,000) – $16,000] …………………

-0-*

Sales returns

{[(.015 $5,800,000) – $85,000] 50%} ……..

Semiannual installment …………………………………..

Second semiannual bonus awarded …………………….

Total bonus awarded for the year ………………………..

*Rework costs not in excess of 2 percent of operating income.

b.

The employees of the Mesa Division should be as satisfied with the new plan as

with the old plan, because the bonus was almost equivalent. However, there is

12–37

PROBLEM 12-50 (CONTINUED)

3.

Harrington’s revised bonus plan for the Charter Division fostered improvements

including the following:

• Increase of 1.9 percent in on-time deliveries

However, operating income as a percentage of sales has decreased from 11 to 10

percent.

The Mesa Division’s bonus has remained at the status quo. The effects of the

revised plan at CommLine Equipment Corporation have been offset by the following:

These results suggest that the gain-sharing bonus plan needs revisions.

Suggestions include the following:

12–38

PROBLEM 12-51 (60 MINUTES)

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12–39

SOLUTIONS TO CASES

CASE 12-52 (60 MINUTES)

1.

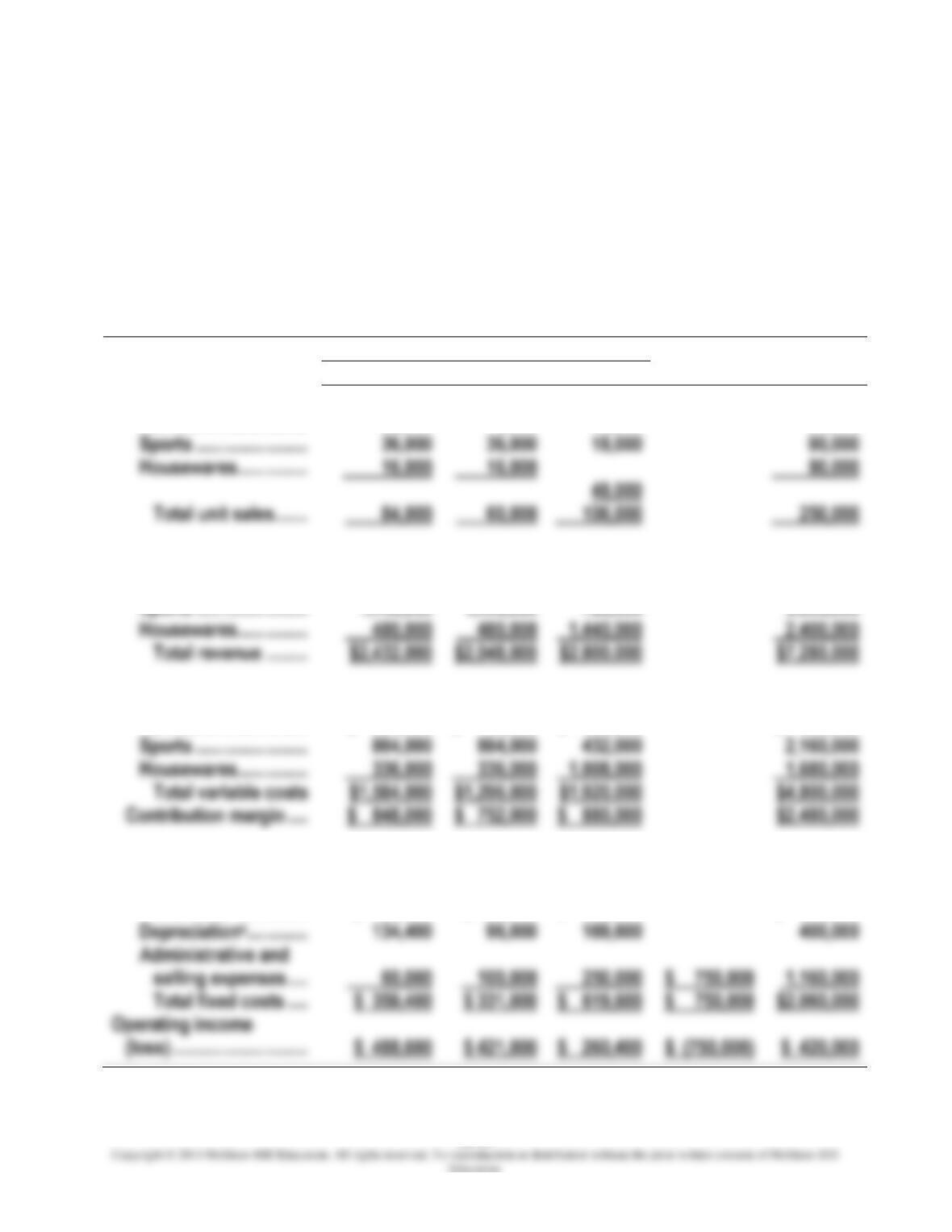

Segmented income statement by geographic areas:

NORTH AMERICAN INDUSTRIES

SEGMENTED INCOME STATEMENT BY GEOGRAPHIC AREAS

FOR THE FISCAL YEAR ENDED APRIL 30, 20×4

Geographic Areas

United States

Canada

Mexico

Unallocated

Total

Sales in unitsa

Furniture ………………..

32,000

8,000

40,000

80,000

Sports ……………………

36,000

36,000

18,000

Housewares ……………

Total unit sales …….

Revenueb

Furniture ………………..

$ 512,000

$ 128,000

$ 640,000

$1,280,000

Sports ……………………

1,440,000

1,440,000

720,000

3,600,000

Housewares ……………

Total revenue ………

$2,048,000

$2,800,000

$7,280,000

Variable costsc

Furniture ………………..

$ 384,000

$ 96,000

$ 480,000

$ 960,000

Sports ……………………

864,000

432,000

2,160,000

Housewares ……………

Total variable costs

$1,296,000

$1,920,000

$4,800,000

Contribution margin ….

$ 848,000

$ 752,000

$ 880,000

$2,480,000

Fixed costs

Production

overheadd ……………

$ 165,000

$ 135,000

$ 200,000

$ 500,000

Depreciatione ………….

96,000

169,600

400,000

Administrative and

Total fixed costs ….

$ 359,400

$ 331,000

$ 619,600

$ 750,000

$2,060,000

12–40

CASE 12-52 (CONTINUED)

SUPPORTING CALCULATIONS

aSales in units

Total Units

% of Sales

=

Units Sold

United States

Furniture ……………………………………..

80,000

.40

32,000

Sports ………………………………………….

90,000

36,000

Housewares …………………………………

80,000

16,000

Canada

Furniture ……………………………………..

80,000

Sports ………………………………………….

90,000

36,000

Housewares …………………………………

80,000

16,000

Mexico

80,000

40,000

Sports ………………………………………….

90,000

18,000

bRevenue

Units Sold

Unit Price

Revenue

United States

Furniture ………………………………………

32,000

$16.00

$ 512,000

Sports …………………………………………..

36,000

Housewares ………………………………….

16,000

Canada

Furniture ………………………………………

Sports …………………………………………..

36,000

Housewares ………………………………….

16,000

Mexico

Furniture ………………………………………

40,000

Sports …………………………………………..

18,000

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12–41

CASE 12-52 (CONTINUED)

cVariable costs

Units

Sold

(1)

Variable

Production

Cost/Unit

(2)

Variable

Selling

Cost/Unit

(3)

Total

Variable

Cost

(1) [(2) + (3)]

United States

Furniture ………………………

32,000

$8.00

$4.00

$ 384,000

Sports …………………………..

36,000

19.00

5.00

864,000

Housewares ………………….

16,000

16.50

336,000

Canada

Furniture ………………………

8,000

8.00

4.00

96,000

Sports …………………………..

36,000

19.00

5.00

864,000

Housewares ………………….

16,000

16.50

4.50

336,000

Mexico

Furniture ………………………

40,000

8.00

4.00

480,000

Sports …………………………..

18,000

19.00

5.00

432,000

dProduction overhead

Total

Production

Overhead

Area

Variable

Costs

Proportion

of

Total

Allocated

Production

Cost

Canada …………………………….

500,000

Mexico ……………………………..

500,000

12–42

CASE 12-52 (CONTINUED)

eDepreciation expense

Total

Depreciation

Area

Units

Sold

Proportion

of

Total

Allocated

Depreciation

United States ……………………

$400,000

84,000

33.6%

$134,400

Canada …………………………….

60,000

24.0%

Mexico ……………………………..

42.4%

2.

Areas where the company’s management should focus its attention in order to

improve corporate profitability include the following:

• The income statement by product line shows that the furniture product line may

not be profitable. The furniture product line does have a positive contribution.

However, the fixed costs assigned to the product line result in a loss. Management

should investigate:

—The possibility of increasing the selling price of these products.

—Cutting variable costs associated with this product line.

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12–43

CASE 12-52 (CONTINUED)

• The income statement by geographic area shows that the Mexican market is the

least profitable sales area. In order to improve the profit margin in the Mexican

market, management should:

12–44

CASE 12-53 (45 MINUTES)

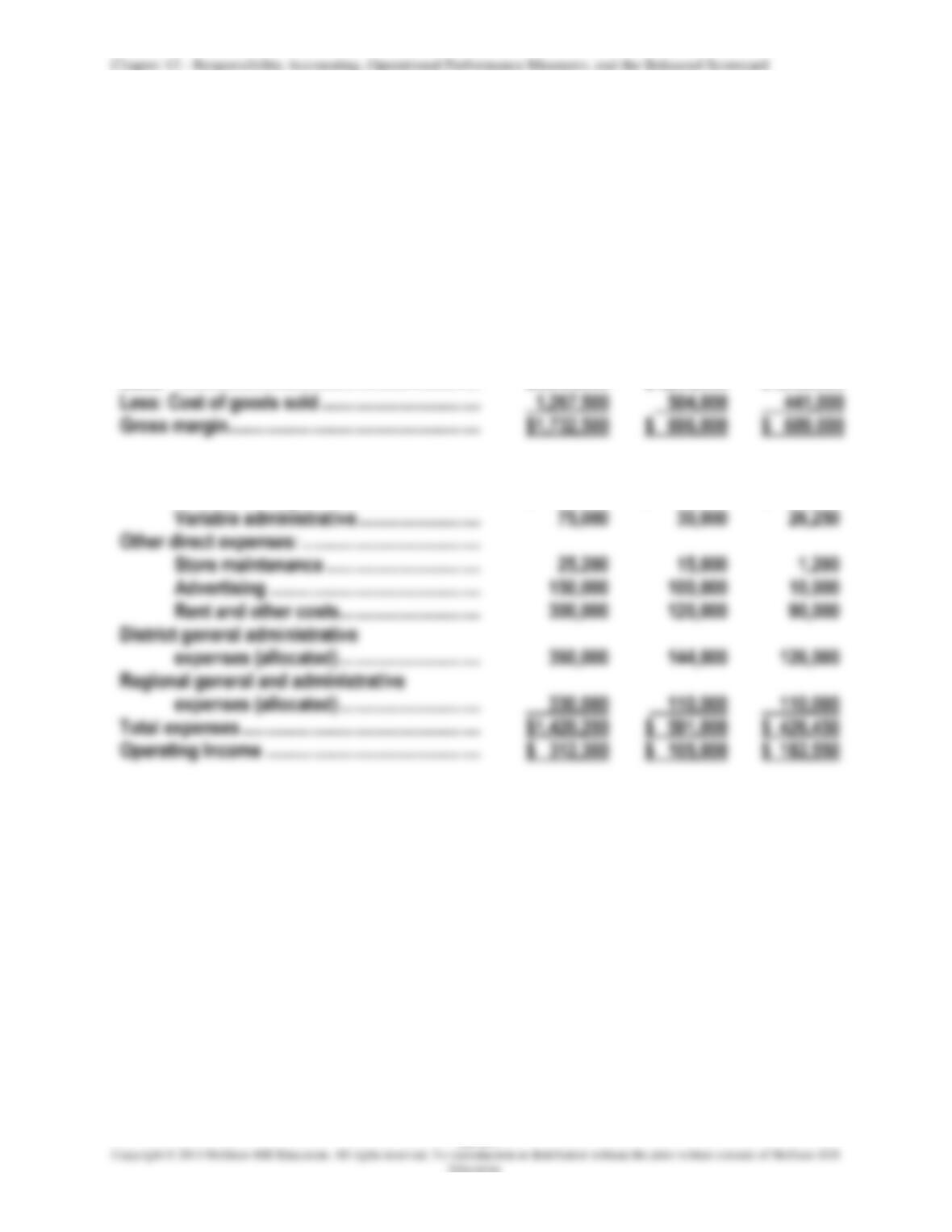

1. Segmented income statement:

ELITE CLASSIC CLOTHES: NEW ENGLAND REGION

SEGMENTED INCOME STATEMENT

FOR MAY

Coastal

District

New Haven

Store

Boston

Store

Sales ………………………………………………………..

Operating expenses:

Variable selling …………………………………

$3,000,000

$ 180,000

$1,200,000

$ 72,000

$1,050,000

$ 63,000

12–45

CASE 12-53 (CONTINUED)

Supporting calculations:

Coastal District

New Haven Store

Boston Store

Sales …………………………………..

Given

$3,000,000 x .40

$3,000,000 x .35

3. The impact of the responsibility-accounting system and bonus structure on the

managers’ behavior and the effect of this behavior on the financial results for the two

stores include the following:

12–46

CASE 12-53 (CONTINUED)

(b) Boston Store:

• Because the manager of the Boston store is motivated to maximize operating income,

4. The assistant controller’s actions violate several standards of ethical conduct for

management accountants, including the following:

Competence:

Integrity:

Credibility:

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12–47

FOCUS ON ETHICS (See page 522 in the text.)

There is plenty of anecdotal evidence that managers may engage in a short-sighted view

of cost cutting, as depicted in this scenario.

If truly motivated by the chance of promotion, rather than by the need for a “lean

company,” then Winters is not acting ethically in making these cost cuts. He is ranking

potential short-term personal gain as more important than the long-term value of the