12–19 Ch. 12—Problems

PROBLEM 12-3

Radix, Inc.

Interim Income Statements

For the

For the Second Year-To-Date

Quarter Ended Ended

June 30, 2011 June 30, 2011

Net sales (see Schedule A) …………………………………………. $2,690,000 $4,050,000

Cost of sales (see Schedule B) …………………………………….. 2,097,200 3,209,200

Schedule A—Net Sales

First quarter of 2011 …………………………………………….. $1,360,000

Second quarter of 2011:

Schedule B—Cost of Sales

First quarter of 2011 …………………………………………….. $1,112,000

Second quarter of 2011:

Compressor business

Current-year costs ……………………………………………….. $1,564,000

2010 units:

Problem 12-3, Concluded

Schedule C—Income Taxes

YTD income:

First quarter …………………………………………………… $136,000

Second quarter ………………………………………………. 382,800

Subtotal …………………………………………………………. $518,800

Projected income …………………………………………………. 438,000

Total annual income …………………………………………….. $956,800

PROBLEM 12-4

Item A The first quarter is being restated due to a decision to discontinue an operation in the

second quarter. Therefore, the original pretax income (loss) reported for the first quar-

ter must be allocated between continuing and discontinued operations. If the original

pretax income was $70,000 and the discontinued operation accounts for a $30,000

Item B Effective tax rate for quarter 1—restated income from continuing operations:

Quarter 1

Restated

YTD income (loss)—see item A above ……………………………………………. $100,000

Projected income (loss) ($60,000 + $40,000) …………………………………… 100,000*

Total annual income (loss) …………………………………………………………….. $200,000

Carryforward of 2013 loss ……………………………………………………………… (80,000)

Estimated annual taxable income …………………………………………………… $120,000

*The original amount included a $40,000 loss that is now part of discontinued

operations.

Estimated tax:

Item C The tax expense (benefit) traceable to the continuing and discontinued components of

restated quarter 1 must total the tax expense originally reported for quarter 1 as fol-

lows:

Tax expense (benefit) traceable to restated:

Continuing operations ……………………………………………………………… $ 8,750

Problem 12-4, Continued

Item D Tax expense for quarter 2 income from continuing operations:

Quarter 2

Quarter 1—restated income (loss) ………………………………………………….. $100,000

Quarter 2 income (loss) …………………………………………………………………. 50,000

YTD income (loss) ………………………………………………………………………… $150,000

Estimated tax:

On first $50,000 @ 15% …………………………………………………………… $ 7,500

On next $50,000 @ 20% ………………………………………………………….. 10,000

On next $50,000 @ 25% ………………………………………………………….. 7,500

Remaining income @ 30% ……………………………………………………….. —

$ 25,000

Less tax credit ……………………………………………………………………………… (5,000)

Item E YTD income (loss) from discontinued operations consists of:

Quarter 1—restated………………………………………………………………………. $ (30,000)

Quarter 2:

Operating loss ………………………………………………………………………… (60,000)

12–23 Ch. 12—Problems

Problem 12-4, Concluded

Item F Total Total

Excluding Excluding

Ordinary Total Nonordinary Nonordinary

Income

Income Loss Gain

Pretax income (loss):

Continuing …………………….. $210,000 $ 210,000 $210,000 $ 210,000

Discontinued ………………….. — (145,000) — (145,000)

Extraordinary …………………. — 20,000 20,000 —

Pretax income (loss) ……….. $210,000 $ 85,000 $230,000 $ 65,000

Tax expense (benefit) ……… $ 20,000 $ — $ 25,000

Taxable income:

PROBLEM 12-5

Corrected Income Statement

For the second Quarter of 2015

Sale revenue (see Schedule A) ……………………………………. $295,000

Less: Sales returns & allowances …………………………………. (14,000)

Net sales …………………………………………………………………… $281,100

Cost of sales (see Schedule B) …………………………………….. 153,000

Schedule A

This represents the $280,000 plus the $15,000 that should have been recorded as a correction

of error in the first quarter 2015 and 2014 income.

Schedule B

Cost of sales as reported …………………………………………….. $145,000

Less: Annual inventory shrinkage …………………………………. (10,000)

Subtotal ………………………………………………………………… 135,000

Error in reporting correction of error ………………………………. 9,000

Schedule C

Selling, general & administrative as reported ………………….. $41,000

Health care insurance expense:

Number of units liquidated ……………………………………… 12,600

Correct expense included (allocate of two quarters) …… (6,300) 6,300

Contract research costs:

Incorrect expense included …………………………………….. 21,000

Correct expense included (allocate of three quarters) … (7,000) 14,000

12–25 Ch. 12—Problems

Schedule D

Quarter 1 Quarter 2

2013 2014 2015 2015

Pretax income (loss) as previously reported ………….. $(50,000) $20,000 $(48,000) $70,000

Corrections per schedule A through C ………………….. (10,000)

Correction of sales …………………………………………….. 15,000 (15,000)

Corrected tax expense (benefit):

44,000 @ 15% …………………………………………….. $(6,600)

20,000 @15% ……………………………………………… $3,000

Quarter 1 Quarter 2

2013 2014 2015 2015

YTD income (loss) ……………………………………………. $(44,000) $20,000 $(54,000) $6,000

Projected income (loss) …………………………………….. 100,000 78,000

Total annual income (loss) …………………………………. $(44,000) $ 20,000 46,000 84,000

Less net operating loss carryforward from 2013 ……..

(20,000) (24,000) (24,000)

Taxable income (Loss) ………………………………………. $(44,000) $0 $22,000 $60,000

PROBLEM 12-6

1. The identification of a segment is based on a “management approach,” which focuses on

how management organizes information about business components for purposes of mak-

2. Revenues traceable to segments generally do not agree with consolidated amounts for

several reasons. First, segmental revenues include intersegment sales or revenues that are

3. Public companies are required to disclose segmental data; therefore, such information is

publicly available to a wide variety of parties including one’s competitors. Obviously, the

more information that is publicly available allows competitors to have increased insight into

4. The determination as to whether or not a segment is considered reportable is based on

5. Interest expense on corporate bonds payable may be allocated to segments if such infor-

mation is considered by the chief operating decision maker of an entity for purposes of de-

6. Once again, it is important to remember that segmental net sales would include inter-

12–27 Ch. 12—Problems

Problem 12-6, Concluded

7. The statement of cash flows reports cash flows from operations, investing, and financing.

Certainly some, but not all, of the key information necessary to determine cash flows can

be derived from segmental reports. For example, depreciation expense for a segment could

be added back to the segment’s net profit or loss to give a rough measure of cash flows

PROBLEM 12-7

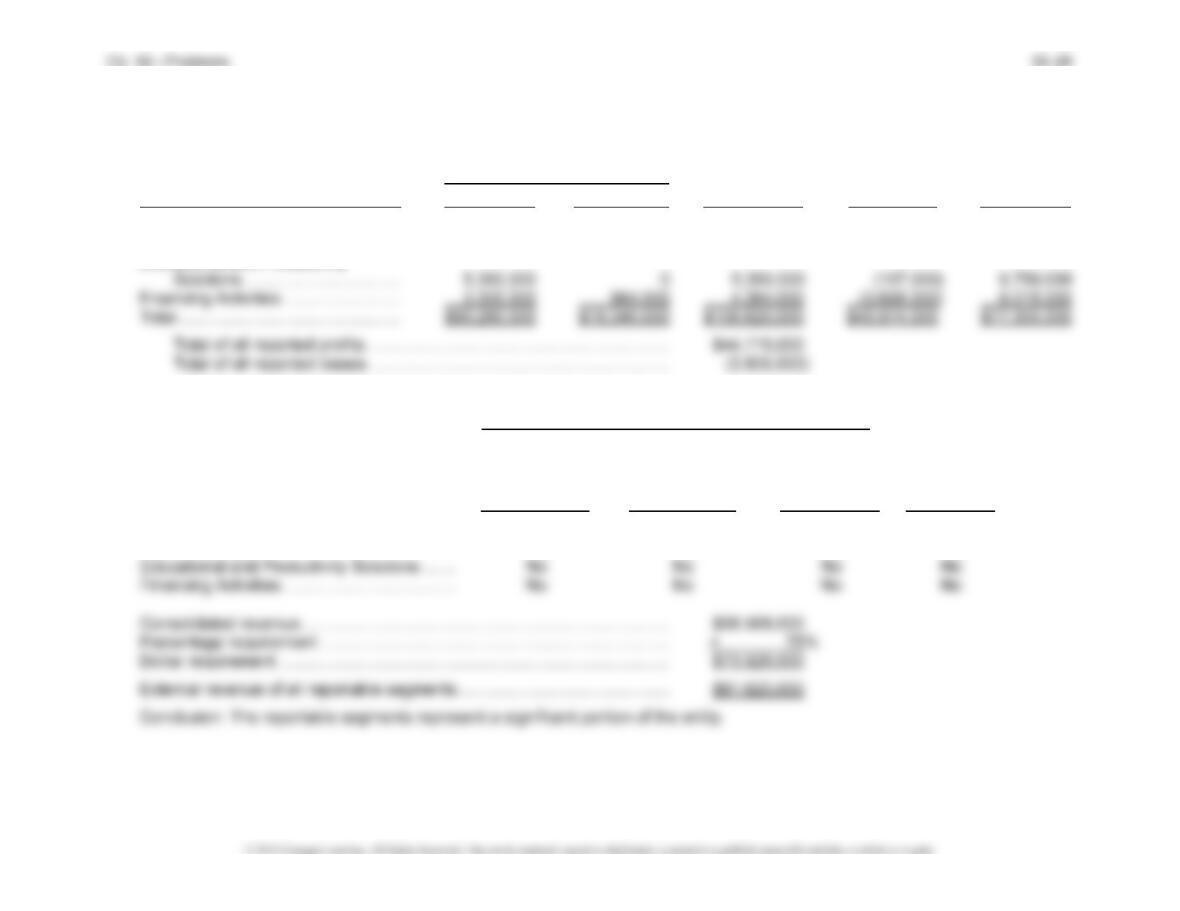

(1) Determination of whether segments are reportable:

Revenues Reported

Segment External Intersegment Total Profit (Loss) Assets

Semiconductors …………………………. $19,920,000 $ 3,970,000 $ 23,890,000 $ 90,000 $28,220,000

Control Devices …………………………. 61,700,000 11,411,000 73,111,000 44,689,000 36,320,000

Educational and Productivity

Is Segment’s

Absolute Value

Revenue 10% of Profit or Loss Assets 10%

or More of 10% or More of or More of Is Segment

$106,625,000? $44,779,000? $77,305,000? Reportable?

Semiconductors ……………………………………. Yes No Yes Yes

Control Devices ……………………………………. Yes Yes Yes Yes

Problem 12-7, Continued

(2) Presentation of segmental values:

Reportable Segments

Semiconductors Control Devices

Revenues from:

External customers ………………………………………….. $19,920,000 $61,700,000

Intersegment sales …………………………………………… 3,970,000 11,411,000

Reconciliation to Consolidated Revenue and Profit:

Revenues

Total revenues for reportable segments ………………………………….. $ 97,001,000

Revenues for nonreportable segments ……………………………………. 9,624,000

Elimination of intersegment revenue ………………………………………. (16,345,000)

Corporate-level revenues ……………………………………………………… 8,288,000

Total consolidated revenues ………………………………………………….. $ 98,568,000

Profit or loss

Total profit or loss for reportable segments ……………………………… $ 44,779,000

Profit or loss of nonreportable segments …………………………………. (3,805,000)

Assets

Total assets for reportable segments ……………………………………… $ 64,540,000

Assets of nonreportable segments …………………………………………. 12,765,000

Elimination of intersegment assets related to intersegment sales .. (700,000)*

Problem 12-7, Continued

Business Segment and Geographical Area Data

The company presented manufactures, develops, and sells a diverse range of electronic

equipment and parts. Its primary targets are consumer and industrial markets. The compa-

ny’s control device manufacturing is the company’s strongest line and together with its

Educational and Productivity Solutions produce educational and time-efficient devices. The

products are sold primarily through retailers and over the Internet.

The company’s Financing Activities segment holds a diversified portfolio of investments. It

also holds several royalty and licensing agreements with operating segments in several dif-

ferent countries.

Business Segment Revenues (Including Intersegment)**

Revenues

External

Intersegment

Semiconductors …………………………………………………… $19,920,000 $ 3,970,000

Business Segment Profit (Loss)**

Reported Profit

(Loss)

Semiconductors …………………………………………………… $ 90,000

Problem 12-7, Continued

Business Segment Assets**

Assets

Semiconductors …………………………………………………… $28,220,000

Control Devices …………………………………………………… 36,320,000

Geographic Area Revenues (Excluding Intersegment)**

Revenues

United States ………………………………………………………. $40,950,000

Japan …………………………………………………………………. 36,157,300

Geographic Area Long-Lived Assets**

Assets

United States ………………………………………………………. $33,377,000

Japan …………………………………………………………………. 20,332,900

Problem 12-7, Concluded

(3) Several ratios that may be helpful in analyzing segmental information are as follows:

Educational

and

Control Productivity Financing

Semiconductors Devices Solutions Activities Total

Return on assets* 0$28,220,00

$90,000 0$36,320,00

0$44,689,00 $6,750,000

($107,000) $6,015,000

0)($3,698,00 0$77,305,00

0$40,974,00

0.32% 123.04% –1.59% –61.48% 53.00%

0.38% 61.12% –2.00% –86.73% 38.43%

0.85 2.01 0.79 0.71 1.38

1.31 3.05 0.97 1.13 2.07

PROBLEM 12-8

(1) Presentation of segmental values:

Reportable Segments All Other

A B D Segments Total

Revenues from:

External customers …………… $ 4,023,500 $ 2,556,570 $ 5,566,725 $ 1,374,500 $13,521,295

Intersegment sales ……………. 192,430 618,525 810,955

Interest revenue ……………………. 48,000 10,000 60,000 12,000 130,000

Gain on intersegment sale of

(2) Reconciliation of Significant Items to Consolidated Amounts

Revenues

Total revenues for reportable segments …………………………………………………. $13,175,750

Problem 12-8, Concluded

Profit or Loss

Total profit or loss for reportable segments …………………………………………….. $ 6,043,745

Profit or loss on nonreportable segments

($1,386,500 – $1,220,600 – $123,395) …………………………………………….. 42,505

Elimination of intersegment profits:

Assets

Total assets for reportable segments …………………………………………………….. $17,862,000

Assets of nonreportable segments ………………………………………………………… 3,717,000

Elimination of intersegment assets related to intersegment sales ………………. (102,107)d

Corporate-level assets ($115,000 + $1,737,000) …………………………………….. 1,852,000

Total consolidated assets …………………………………………………………………….. $23,328,893

a

Segment B should depreciate the original net book value of $200,000 over 10 years rather

than the new selling price of $300,000 over 10 years. Therefore, depreciation expense

should be $20,000 per year versus $30,000. The gain on the sale of $100,000 ($300,000 –

$200,000) is included in Segment A’s total revenue.

c

Segment B recorded a cost of $144,000 on the sale to Segment C. Segment C in turn rec-

orded 75% of B’s selling price, or $144,323 (75% × $192,430), as cost of sales. The total

cost recorded was $288,323 ($144,000 + $144,323). However, the actual cost of goods

sold was 75% of B’s cost of $144,000, or $108,000. Therefore, $180,323 ($288,323 –

$108,000) of cost should be eliminated along with the $618,525 cost of the goods pur-

PROBLEM 12-9

Date

To: Bank Lending Officer

From: Student Accountant

Re: Raymack Manufacturing – Questions related to segmental reporting

In regards to the above referenced item, please accept the following responses to your ques-

tions.

1. The decision to report these areas as two segments may be due to a number of factors.

Although both segments earn revenues and generate expenses, their operating results

may be reviewed by separate chief operating decision makers for organizational

2. Often the total of segmental net sales exceed consolidated net sales because segmental

3. A likely explanation as to why consolidated pretax income is greater than segmental

pretax income is due to the fact that there are certain corporate sources of income that

are not allocated to segments. For example, corporate level gains and losses on cash

4. Tax expense or benefit is normally viewed as a consolidated component of income and

is not allocated to segments. However, the effective tax rate reported in consolidated

5. On an entity wide basis, the total of all long-lived assets must be reported by

geographical location whether or not they have been allocated to segments. The assets

6. In addition to reporting pretax operating income (loss), segments are required to report

segmental assets. This allows for a calculation of return on assets. However, segments

7. Both Germany and Spain are considered to be “European Countries”. The allocation of

sales to geographic segments is generally based on where the customer is or where the

8. Obviously a number of variables can be measured in terms of growth. It would seem that

growth in revenues, operating profit (loss), and identifiable assets would all be important

variables for purposes of measuring growth. Perhaps even as important would be to re-