Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12-1

12 INCOME AND CHANGES IN RETAINED EARNINGS

Chapter Summary

Chapter 12 continues the coverage of stockholders’ equity but shifts the focus from paid–

in capital to retained earnings. The student is already aware that net income drives the changes in

retained earnings. However, in any given period net income may reflect unusual and

nonrecurring events. We begin by explaining how to define such items and how to present them

so that the income statement may still serve as the basis for reasonable estimates of future

earnings. The two categories of events, which require special treatment, are (1) discontinued

operations, and (2) unusual and/or infrequent gains and losses.

Before turning to the impact of various dividend transactions, we briefly review basic and

diluted earnings per share. The emphasis here is on interpretation of the EPS figures, since the

detailed mechanics of calculating these measures is beyond the scope of the first course.

The second major section of the chapter explains a number of stockholder equity

transactions that affect retained earnings. The most obvious example of such transactions is the

declaration of a cash dividend. The requirements for distributing a cash dividend are outlined as

are the significant dates involved in the distribution of the dividend. Stock dividends are

discussed since they too result in a reduction in retained earnings. This portion of the chapter

closes with a brief explanation of prior period adjustments to retained earnings.

Additional topics covered in Chapter 12 include an introduction to comprehensive

income and a review of the statement of stockholders’ equity.

Learning Objectives

1. Describe how irregular income items, such as unusual and/or infrequent items and

discontinued operations, are presented in the income statement.

2. Compute earnings per share.

3. Distinguish between basic and diluted earnings per share.

4. Account for cash dividends and stock dividends, and explain the effects of these transactions

on a company’s financial statements.

5. Describe and prepare a statement of retained earnings.

6. Define prior period adjustments, and explain how they are presented in financial statements.

7. Define comprehensive income, and explain how it differs from net income.

8. Describe and prepare a statement of stockholders’ equity and the stockholders’ equity section

of the balance sheet.

9. Illustrate steps management might take to improve the appearance of the company’s net

income.

Chapter 12—Income and Changes in Retained Earnings

12-2 Instructor’s Resource Manual

Brief Topical Outline

A. Reporting the results of operations

1. Developing predictive information

2. Reporting irregular items: an illustration

3. Continuing operations

a. Income from continuing operations

4. Discontinued operations

5. Unusual and/or infrequent gains and losses—see Your Turn (page 526)

6. Earnings per share (EPS)

a. Preferred dividends and earnings per share

b. Presentation of earnings per share in the income statement

7. Basic and diluted earnings per share—see Pathways Connection, International

Case in Point, and Your Turn (page 529)

B. Other transactions affecting retained earnings

1. Cash dividends

2. Dividend dates

3. Liquidating dividends

4. Stock dividends

a. Entries to record a stock dividend

b. Reasons for stock dividends—see Case in Point (page 533)

c. Distinction between stock splits and stock dividends

5. Statement of retained earnings

6. Prior period adjustments

a. Restrictions of retained earnings

7. Comprehensive income

8. Statement of stockholders’ equity

9. Stockholders’ equity section of the balance sheet—see Ethics, Fraud, &

Corporate Governance (page 538)

C. Concluding remarks

Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12-3

Topical Coverage and Suggested Assignments

Class

Meetings

on Chapter

Topical

Outline

Coverage

Discussion

Questions*

Brief

Exercises*

Exercises*

Problems*

Critical

Thinking

Cases*

1

A

1, 2, 3, 5

1, 3, 4, 5

1, 3

3, 6

1

2

B – D

7, 8, 10, 12, 13

7, 8, 10

4, 6, 7

4

*Homework assignment (to be completed prior to class)

Comments and Observations

Teaching Objectives for Chapter 12

In this chapter, we discuss a variety of events and transactions that affect retained earnings. In

the classroom, our objectives are to:

1. Explain the purpose of reporting irregular events separately from normal and recurring

business activities.

2. Carefully define discontinued operations and unusual and/or infrequent gains and losses.

Review and discuss the financial statement presentation of each category of event.

3. Illustrate the computation of earnings per share, and briefly discuss the distinction between

basic and diluted earnings.

4. Discuss the nature and purpose of cash dividends and stock dividends, emphasizing the

effects upon total stockholders’ equity and the probable effects upon stock price. Illustrate

the journal entries for each of the events.

5. Explain the nature of prior period adjustments. Discuss probability of occurrence in

publicly owned and closely held corporations.

6. Review and discuss the statement of retained earnings.

7. Explain the nature of comprehensive income.

8. Review the statement of stockholders’ equity portrayed as an “expanded” statement of

retained earnings.

Chapter 12—Income and Changes in Retained Earnings

12-4 Instructor’s Resource Manual

General Comments

Many accounting faculty ask us why we cover discontinued operations in the

introductory course. Our answer is that in this era of “corporate restructuring,” discontinued

operations are commonplace in the financial statements of publicly owned corporations. (Prior

period adjustments, by comparison, are virtually nonexistent in the financial statements of large

corporations.)

In discussing irregular events, we focus upon the appropriate financial statement

presentation rather than upon the recording of transactions. Most of these transactions are

recorded in the same manner as ordinary transactions. Allocations of revenue, expenses, and

gains and losses to such special categories as “continuing operations,” “discontinued operations,”

and “unusual and/or infrequent gains and losses” are made on the financial statements at the end

of the period. The tax effects relating to these items also are determined and allocated as needed

for financial statement preparation rather than through journal entries.

We consider these financial statement preparation procedures beyond the scope of the

introductory course. Entries to record accounting changes and prior period adjustments also are

beyond the scope of the introductory accounting course. Anyone with responsibility for

recording such transactions needs more of an accounting background than an introductory course

can provide. Any user of financial statements, however, needs to understand the nature of these

unusual items in order to interpret properly the operating results of the current period.

Several of our problems are intended to illustrate the presentation of irregular events in

financial statements, including Problems 1, 2, and 3. These problems are successively

comprehensive and challenging. We also recommend class discussion of Case 1 involving

several well-known corporations.

In discussing earnings-per-share, we consider a conceptual understanding important, but

regard most of the mechanics of per-share computations as beyond the scope of the course. For

instance, we discuss the concept of diluted earnings-per-share, but do not get into any

computations. We do, however, review Exercise 5. This exercise helps clarify the idea that

earnings-per-share is based only upon the income applicable to common stock.

The “stockholders’ equity” portion of this chapter includes a variety of short topics. We

find an in-class review of Exercise 9 is an efficient way to cover many of these topics. As an

overview, we use Problem 5, which also acquaints students with the unofficial “statement” of

stockholders’ equity.

Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12-5

Supplemental Exercises

Group Exercise

10-K filing for the fiscal year ended June 30, 2016. Locate the consolidated income statement.

Does Microsoft report their restructuring charge as a “discontinued operation” or as an ordinary

operating expense? What might justify this reporting?

Also, read Note 14: Restructuring Charges. What else did you learn about the charges

reported on the income statement?

Internet Exercise

recent annual report filing for the following:

• Coca-Cola (ticker symbol KO)

• PepsiCo (ticker symbol PEP)

Locate the consolidated statement of stockholders’ equity. Answer the following

questions related to each company:

1. Do they report common stock, preferred stock, or both?

2. Do they report treasury stock? If so, how much?

3. Did they pay dividends during the year? If so, how much?

4. Did any items other than net income and dividends impact retained earnings? If so,

describe.

Chapter 12—Income and Changes in Retained Earnings

12-6 Instructor’s Resource Manual

CHAPTER 12 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

1. Beck Corporation declared a 2-for-1 common stock split, but this transaction was erroneously

recorded as a 100% common stock dividend. As a result:

a The common stock account is overstated.

b The total dollar amount of stockholders’ equity is overstated.

c The corporate records do not show the correct number of shares of common stock

outstanding.

d The par value per share is understated.

2. Fuller Mfg.’s financial statements for the current year include the following:

Income from continuing operations ……………………………………………………….. $663,200

Prior period adjustment (increase in prior-year net income, net of taxes) …… 180,000

Cash dividends paid to preferred stockholders ………………………………………… 196,800

Gain from discontinued operations (net of taxes) ……………………………………. 433,600

Unusual loss ………………………………………………………………………………………… 174,400

On the basis of this information, net income for the current year is:

a $488,800. b $922,400. c $725,600. d $1,102,400.

3. The following two items are disclosed in the stockholders’ equity section of Cort Corporation’s

December 31, 2018, balance sheet:

Treasury stock (500 shares, at cost) ……………………………………………………….. $50,000

Additional paid-in capital: treasury stock transactions …………………………….. 22,500

If the company had reacquired 3,000 shares of treasury stock in February of 2018 then

some of the treasury stock must have been sold during 2018 for:

a $9 per share above its par value.

b $9 per share.

c $109 per share.

d $109 per share above its cost.

4. At the beginning of the current year, Bard Corporation had 400,000 shares of $1 par common stock

outstanding and had retained earnings of $11,000,000. During the year, the company earned

$5,000,000, declared a 5% stock dividend when the price of stock was $25 per share, and paid a

year-end cash dividend of $2 per share. (The cash dividend was paid after the stock dividend had

been distributed.) Bard Corporation’s retained earnings at the end of the year amount to:

a $16,000,000. b $14,660,000. c $14,320,000. d $14,700,000

5. Donnell Corp. had 100,000 shares of 8% preferred stock, $100 par, and 500,000 shares of $1 par

common stock outstanding throughout the year. Net income for the year was $4,800,000, and

Donnell declared and distributed a cash dividend of $4 per share on its common stock. Earnings per

share amounted to:

a $8.80. b $4.00. c $8.00. d $2.00.

Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12-7

CHAPTER 12 NAME #

10-MINUTE QUIZ B SECTION

The stockholders’ equity section of the balance sheet of Global Publishing at December 31, 2017, appears

as follows:

Stockholders’ equity:

5% preferred stock, $100 par,

50,000 shares authorized, ___?__ shares issued ………………………………… $1,200,000

Common stock, $2 par, 500,000 shares authorized,

140,000 shares issued, of which ___? are held in treasury ………………. 280,000

Additional paid-in capital:

From issuance of preferred stock ………………………………………………………. 288,000

From issuance of common stock ………………………………………………………. 840,000

From treasury stock transactions ………………………………………………………. 16,000

From common stock dividends …………………………………………………………. 400,000

Total paid-in capital ……………………………………………………………………….. $3,024,000

Retained earnings ($112,000 equal to cost of treasury

stock is not available for dividends) ……………………………………………………… __880,000

$3,904,000

Less: Treasury stock (at cost: 14,000 common shares) …………………………... (112,000)

Total stockholders’ equity …………………………………………………………………… $3,792,000

Answer the following questions based on the stockholders’ equity section given above. The company had

no treasury stock purchases before 2017.

1. Refer to the above data. What was the average issue price per share of preferred stock?

a $80. b $100. c $124. d $148.

2. Refer to the above data. How many shares of common stock are outstanding?

a 140,000. b 126,000. c 500,000. d 120,000.

3. Refer to the above data. A small stock dividend of 5,000 shares was declared and distributed during

2017. What was the market price per share on the date of declaration?

a $82 per share. b $80 per share. c $2 per share. d $78 per share

4. Refer to the above data. If Global Publishing had reacquired 16,000 shares of treasury stock early in

2017, then some treasury stock must have been sold during 2017 for:

a $5 per share. b $8 per share. c $6 per share. d $16 per share.

5. Refer to the above data. Assume that all remaining treasury stock is reissued at a price of $18 per

share in January of 2018. What amount should be credited to the account Additional Paid-in Capital:

Treasury Stock Transactions in the journal entry to record this transaction?

a $96,000. b $140,000. c $112,000. d $288,000.

Chapter 12—Income and Changes in Retained Earnings

12-8 Instructor’s Resource Manual

CHAPTER 12 NAME #

10-MINUTE QUIZ C SECTION

The stockholders’ equity section of the balance sheet of Xanadu Fashions, Inc., at December 31, 2018

appears as follows:

Stockholders’ equity:

7% preferred stock, $100 par, callable at $105,

50,000 shares authorized, 40,000 shares issued ………………………………….. $4,000,000

Common stock, $2 par, 600,000 shares authorized,

450,000 shares issued, of which 30,000 are held in treasury ………………… 900,000

Additional paid-in capital:

From issuance of preferred stock ……………………………………………………….. 640,000

From issuance of common stock ………………………………………………………… 1,890,000

From treasury stock transactions ………………………………………………………… 60,000

From common stock dividends ………………………………………………………….. __450,000

Total paid-in capital ……………………………………………………………………… $7,940,000

Retained earnings ($240,000 equal to cost of treasury

stock is not available for dividends) ……………………………………………………. 3,600,000

$11,540,000

Less: Treasury stock (at cost: 30,000 common shares) ………………………….. __(240,000)

Total stockholders’ equity ………………………………………………………………….. $11,300,000

Answer the following questions based on the stockholders’ equity section given above. The company

purchased no treasury stock before 2018.

1. Refer to the above data. What was the average issue price per share of preferred stock?

2. Refer to the above data. How many shares of common stock are outstanding?

3. Refer to the above data. A small stock dividend of 20,000 shares was declared and distributed during

2018. What was the market price per share on the date of declaration?

4. Refer to the above data. If Xanadu Fashions had reacquired 35,000 shares of treasury stock early in

2018, compute the price per share for which the reissued treasury stock was sold.

5. Refer to the above data. Assume all remaining treasury stock is reissued at a price of $24 per share

in January of 2019. Prepare the journal entry to record this transaction:

Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12-9

CHAPTER 12 NAME #

10-MINUTE QUIZ D SECTION

Shown below is information relating to operations of R. Brook, Inc. for the current year:

Continuing operations:

Net sales ………………………………………………………………………………………………….. $2,750,000

Costs and expenses (including income taxes) ………………………………………………. 2,125,000

Other data:

Current-year loss generated by segment of the business

discontinued in July (net of income tax benefit) ………………………………………….. 207,500

Gain on disposal of discontinued segment (net of

income tax) ……………………………………………………………………………………………… 137,500

Prior period adjustment (decrease in prior year’s depreciation

expense, net of income taxes) ……………………………………………………………………. 45,000

Unusual loss …………………………………………………………………………………………….. 17,500

Cash dividends declared ($1.50 per share) …………………………………………………… 150,000

In the space provided, complete the income statement for R. Brook, Inc., including earnings per share

figures. R. Brook, Inc. has 100,000 shares of a single class of common stock outstanding throughout the

year.

R. BROOK, INC.

Condensed Income Statement

For the Year Ended December 31, 2017

Chapter 12—Income and Changes in Retained Earnings

12–10 Instructor’s Resource Manual

SOLUTIONS TO CHAPTER 12 10-MINUTE QUIZZES

QUIZ A

1 A

QUIZ B

QUIZ C

1

5

Cash (30,000 shares $24 per share) ……………………………………….. 720,000

Chapter 12—Income and Changes in Retained Earnings

Financial and Managerial Accounting, 18e 12–11

QUIZ D

R. BROOK, INC.

Condensed Income Statement

For the Year Ended December 31, 2017

Net sales ……………………………………………………………………………….. $2,750,000

Cost and expenses (including applicable

income taxes) ……………………………………………………………………….. (2,125,000)

Chapter 12—Income and Changes in Retained Earnings

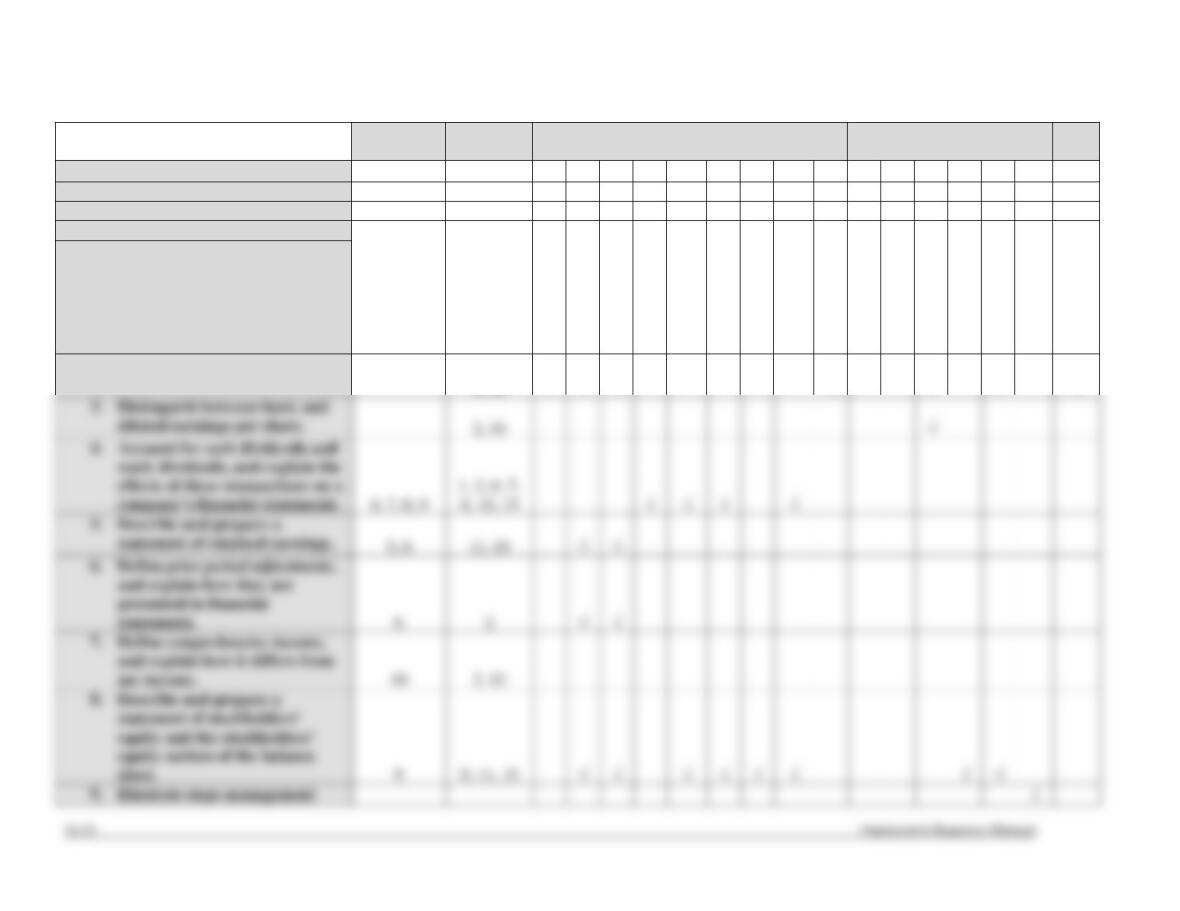

Assignment Guide to Chapter 12

Brief

Exercises

Exercises

Problems

Cases

Net

Item number

1-10

1-15

1

2

3

4

5

6

7

8

9

1

2

3

4

5

6

7

Time estimate (in minutes)

<15

<15

30

30

35

20

20

40

30

50

25

20

20

30

35

60

30

30

Difficulty rating

E

E

E

M

S

E

M

S

S

S

S

E

M

S

S

S

M

E

Learning Objectives:

1, 2, 3

2, 3, 4, 11,

15

1. Describe how irregular income

items, such as unusual and/or

infrequent items and

discontinued operations, are

presented in the income

statement.

2. Compute earnings per share.

2, 3, 4, 5,

6, 10

2, 14

4, 7, 8, 9

8, 10, 13

presented in financial

2

net income.

2, 12

sheet.

9, 11, 15

Financial and Managerial Accounting, 18e 12–13