PROBLEM 12-3B

HUBBLE COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………. $1,245,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………… $105,000

Amortization expense ………………………… 15,000

Decrease in accounts receivable ………… 290,000

*PROBLEM 12-4B

HUBBLE COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ……… $5,890,000 (1)

Less cash payments:

Computations:

(1) Cash receipts from customers

Sales ………………………………………………………… $5,600,000

(2) Cash payments to suppliers

Cost of goods sold ……………………………………. $3,290,000

Add: Increase in inventories …………………….. 140,000

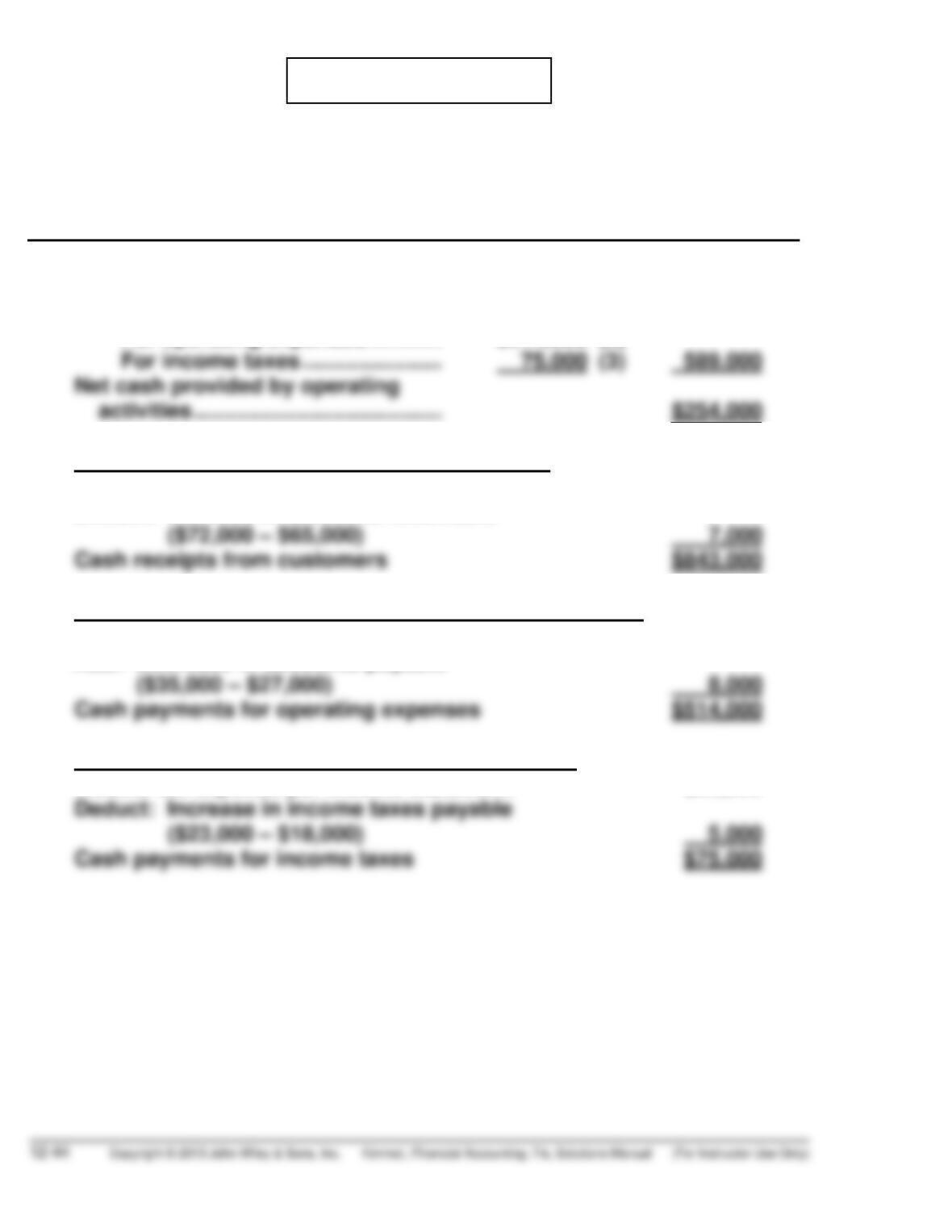

(3) Cash payments for operating expenses

Operating expenses

($420,000 + $525,000) ………………. $ 945,000

Add: Increase in prepaid

PROBLEM 12-5B

MOSLEY COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………….. $204,000

Adjustments to reconcile net income

to net cash provided by operating

activities

Depreciation expense …………………………. $56,000

Loss on disposal of equipment …………… 4,000

*PROBLEM 12-6B

MOSLEY COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ……… $843,000 (1)

Less cash payments:

For operating expenses ………… $514,000 (2)

(1) Computation of cash receipts from customers

Revenues $850,000

Deduct: Increase in accounts receivable

(2) Computation of cash payments for operating expenses

Operating expenses per income statement $506,000

Add: Decrease in accounts payable

(3) Computation of cash payments for income taxes

Income tax expense per income statement $80,000

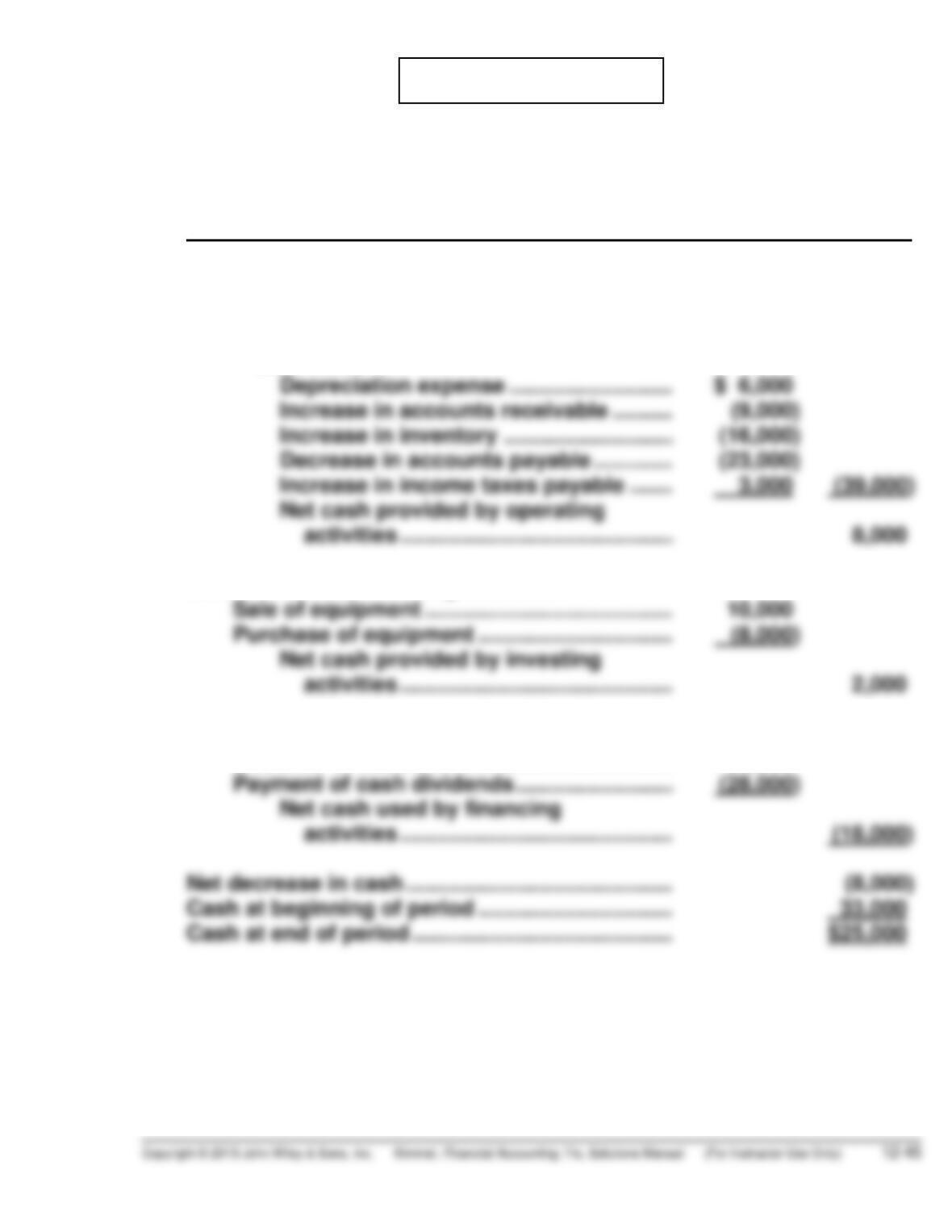

PROBLEM 12-7B

(a) FILMORE COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………….. $47,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Cash flows from investing activities

Cash flows from financing activities

Issuance of bonds ………………………………….. 10,000

PROBLEM 12-7B (Continued)

(b) 1. $8,000 ÷

$49,000* + $69,000**

2 = .136 times

*PROBLEM 12-8B

(a) FILMORE COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ….. $286,000 (1)

Less cash payments:

To suppliers ………………………. $233,000 (2)

For operating expenses

Cash flows from investing activities

Sale of equipment …………………….. 10,000

Cash flows from financing activities

Issuance of bonds …………………….. 10,000

Net decrease in cash ……………………….. (8,000)

Computations:

(1) Cash receipts from customers

Sales ………………………………………………………………. $295,000

*PROBLEM 12-8B (Continued)

(2) Cash payments to suppliers

Cost of goods sold ……………………………………………….. $194,000

(3) Cash payments for income taxes

Income tax expense ……………………………………………… $ 14,000

(b) 1. $8,000 ÷

$4 9, 0 00 * + $ 69 , 00 0 **

2 = .136 times

PROBLEM 12-9B

TURNER INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………….. $137,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………. $ 50,000

Loss on disposal of plant assets …………. 9,000

Cash flows from investing activities

Sale of plant assets …………………………………… 2,000

Cash flows from financing activities

Sale of common stock ……………………………….. 25,000

Net increase in cash …………………………………………. 4,000

*PROBLEM 12-10B

TURNER INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ………….. $594,000 (1)

Less cash payments:

To suppliers ……………………………… $294,000 (2)

Cash flows from investing activities

Sale of plant assets ………………………….. 2,000

Cash flows from financing activities

Sale of common stock ……………………… 25,000

Net increase in cash ……………………………….. 4,000

Computations:

(1) Cash receipts from customers

Sales ………………………………………… $610,000

Deduct: Increase in accounts

*PROBLEM 12-10B (Continued)

(2) Cash payments to suppliers

Cost of goods sold …………………………………………………. $290,000

(3) Cash payments for operating expenses

Operating expenses exclusive of

depreciation ……………………………………… $65,000

PROBLEM 12-11B

BERKLER COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………………. $46,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Cash flows from investing activities

Sale of land …………………………………………………… 34,000

Cash flows from financing activities

Payment of cash dividends ……………………………. (12,000)

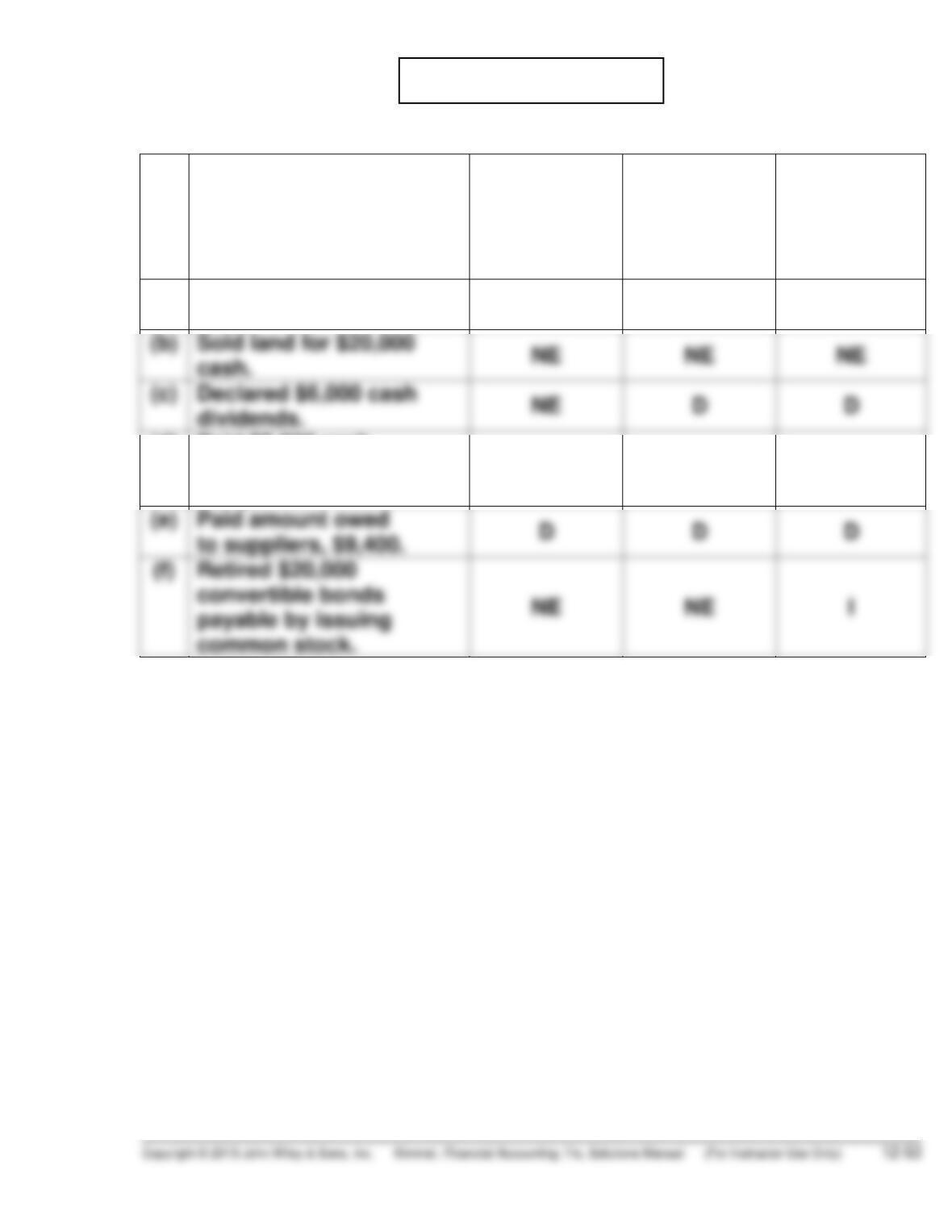

PROBLEM 12-12B

Transaction

Free Cash

Flow

($80,000)

Current

Cash Debt

Coverage

Ratio

(0.7 times)

Cash Debt

Coverage

Ratio

(0.4 times)

(a) Recorded cash sales

$4,800. I I I

(d) Paid $5,800 cash

dividends declared

last year.

D I I

BYP 12-1 FINANCIAL REPORTING PROBLEM

(a) Net cash provided by operating activities:

(c) Tootsie Roll uses the indirect method of computing and presenting the

net cash provided by operating activities.

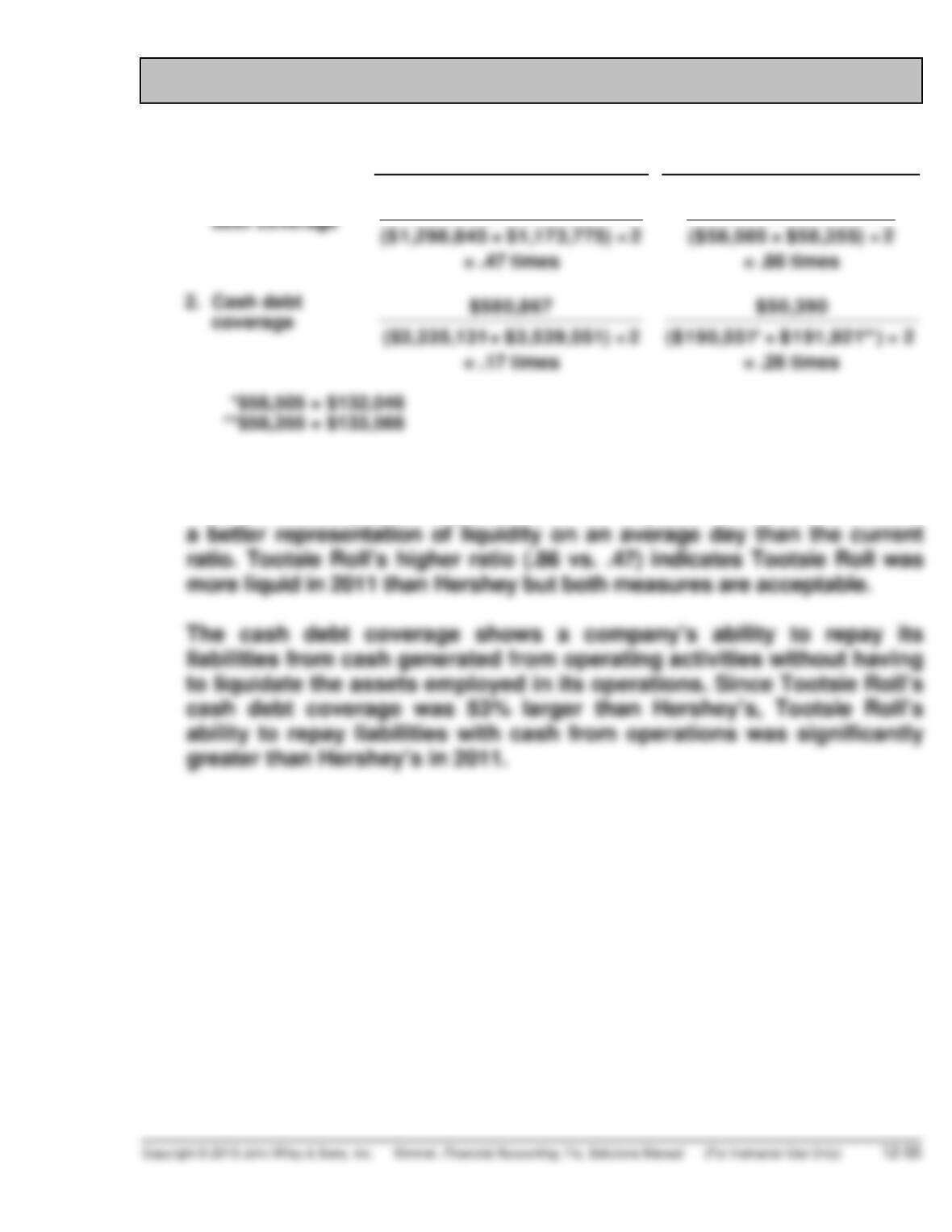

BYP 12-2 COMPARATIVE ANALYSIS PROBLEM

(

a

)

Hershe

y

Tootsie Roll

1. Current cash

$580,867

$50,390

(b) Tootsie Roll’s current cash debt coverage provides a ratio of $0.86 of net

cash provided by operating activities for every dollar of current debt. It is