CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Ex. 12-18

a. Cash balance………………………………………………

…

$ 35,000

Sum of capital accounts…………………………………

…

(46,000)

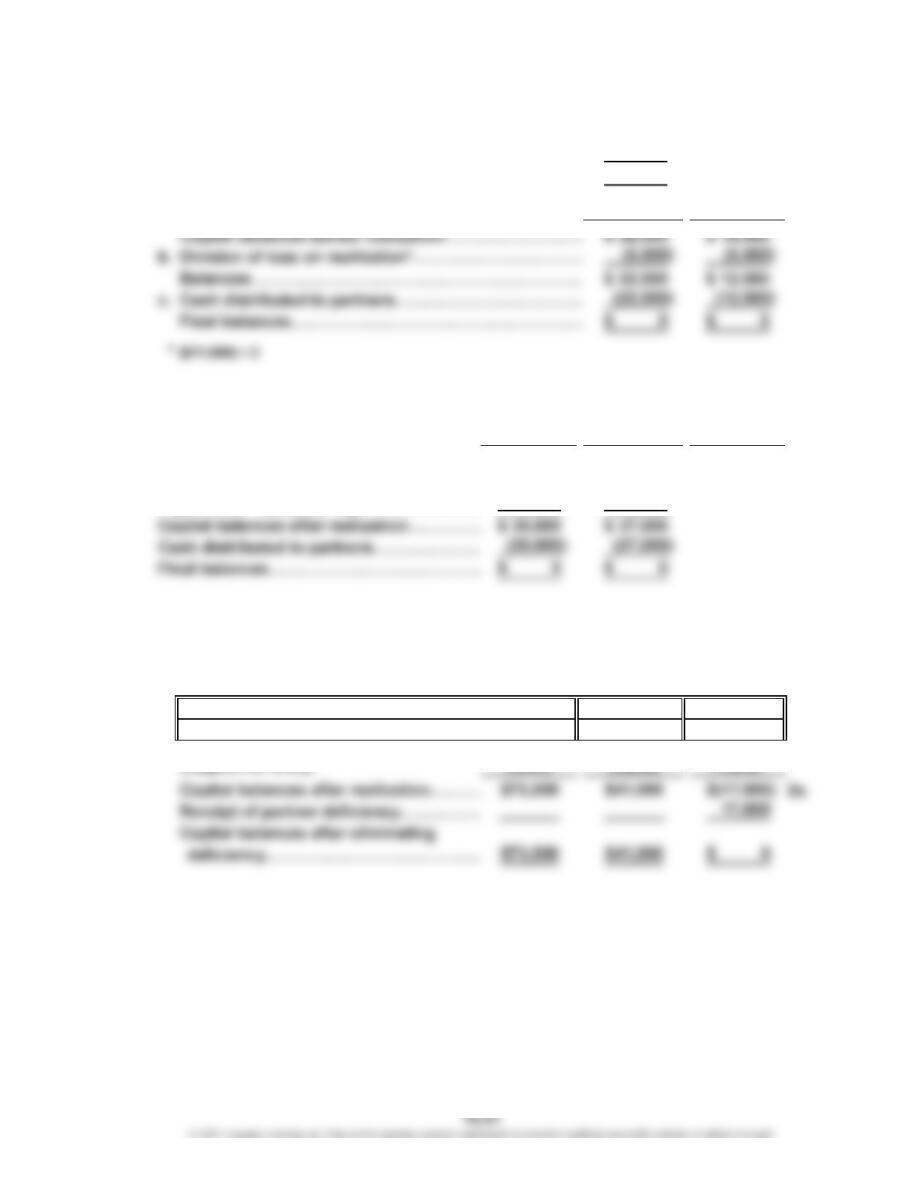

Loss on realization………………………………………… $ 11,000

Hewitt Patel

Ex. 12-19

Oliver Ansari Total

Capital balances before realization………

…

$ 28,000 $ 35,000 $63,000

Division of gain on realization

[($67,000 – $63,000) ÷ 2]…………………

…

2,000 2,000

…

Ex. 12-20

a. Deficiency

b. $97,500 ($73,500 + $41,000 – $17,000)

c. Cash

Fowler, Capital

17,000

17,000

…

…

…

…

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

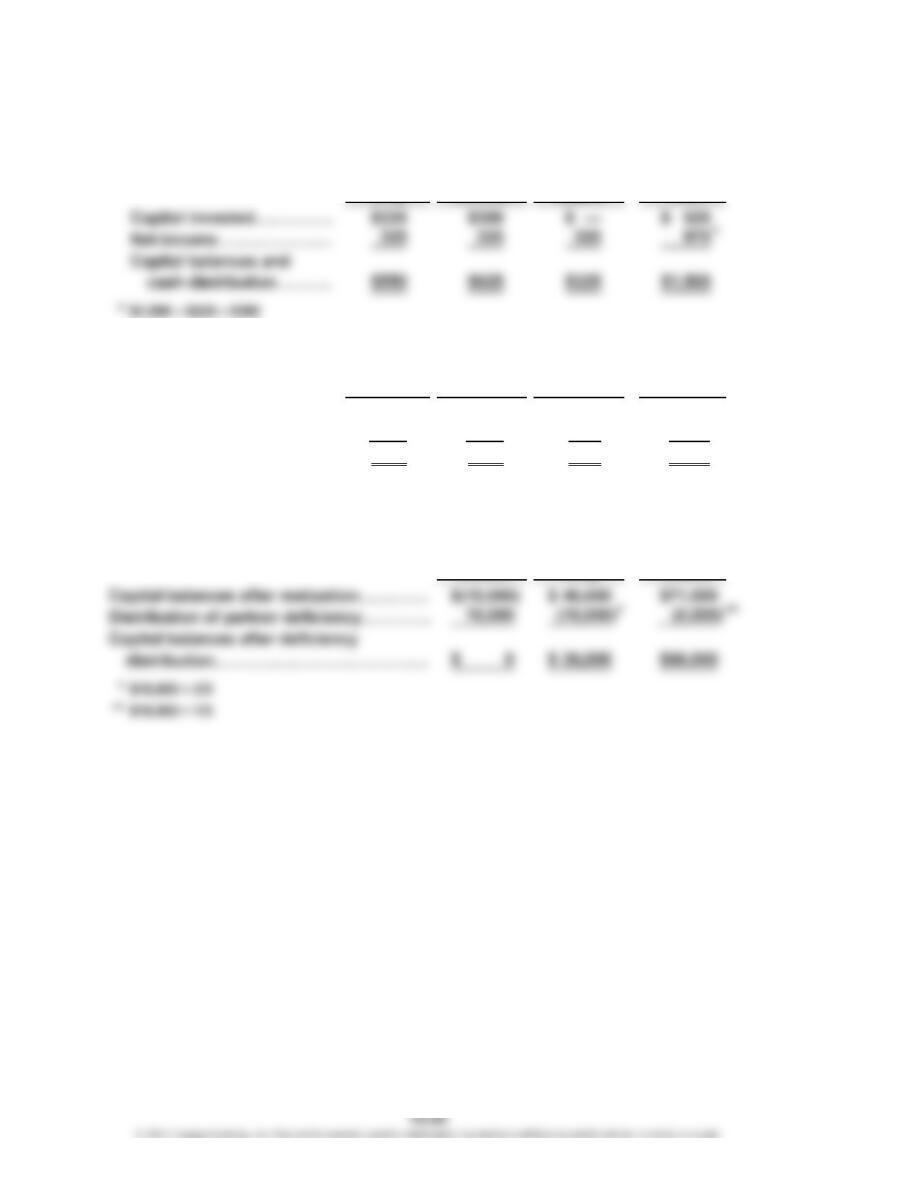

Ex. 12-21

a. $975 [$1,500 – ($225 + $300)]

b. Cash should be distributed as indicated in the following tabulation:

c. Mapes has a capital deficiency of $75, as indicated in the following

tabulation:

Bray Lincoln Mapes Total

Capital invested…………

…

$225 $300 $ — $ 525

Net loss……………………

…

(75) (75) (75) (225)

Capital balances…………

…

$150 $225 $(75) $ 300

*

$300 – $525

Ex. 12-22

Dr.

*

…

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

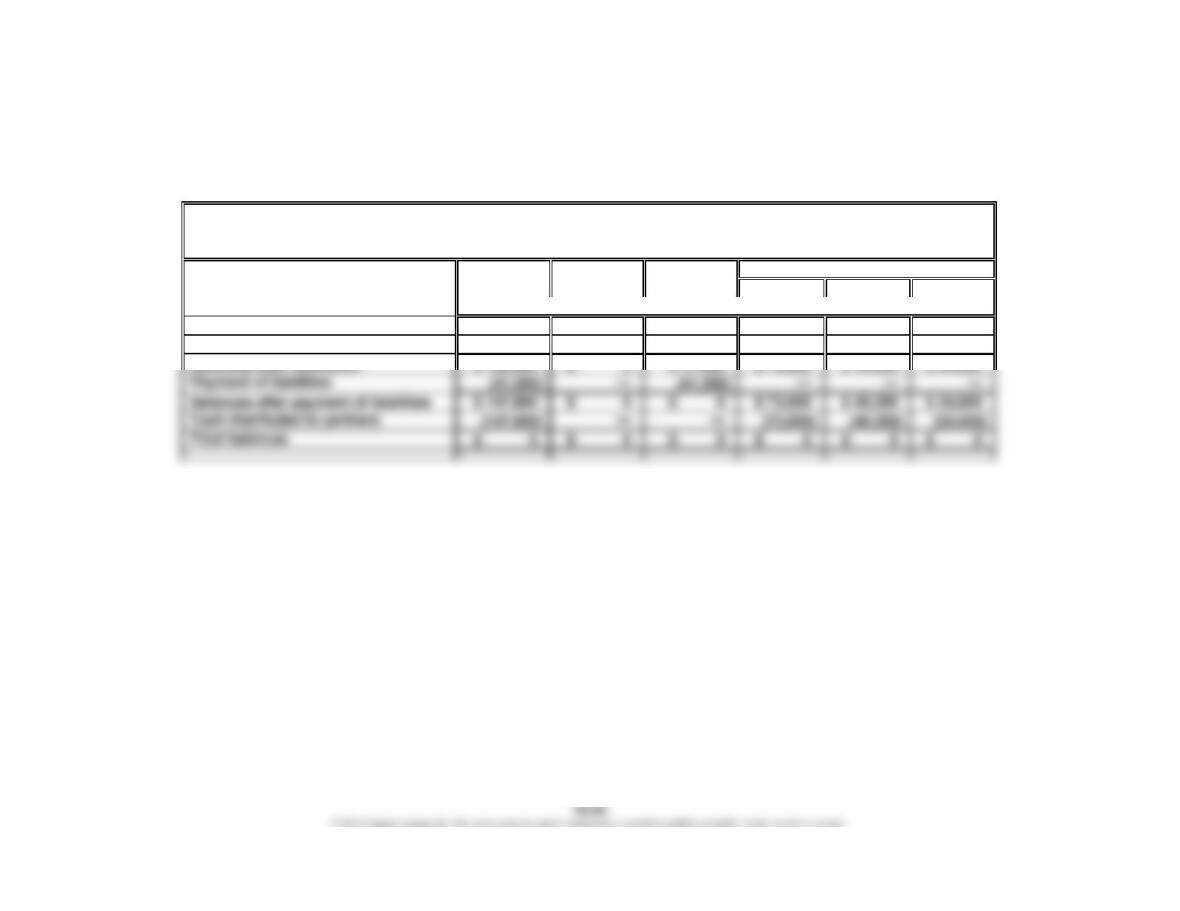

Ex. 12-23

Noncash Silver Carillo Tingley

Cash Assets Liabilities (3/6) (2/6) (1/6)

Balances before realization $ 72,500 $ 124,200 $ 41,300 $ 77,700 $ 51,800 $ 25,900

Sale of assets and division of loss 116,400 (124,200) —(3,900) (2,600) (1,300)

Silver, Carillo, and Tingley

Statement of Partnership Liquidation

For Period July 1–29

+ = +++

Capital

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Ex. 12-24

a.

Noncash Lester Torres Hearst

Cash Assets Liabilities (2/5) (2/5) (1/5)

Balances before realization $ 26,000 $ 146,000 $ 35,000 $ 49,000 $ 61,000 $ 27,000

Sale of assets and division of gain 158,000 (146,000) —4,800 4,800 2,400

b. Lester, Member Equity

Torres, Member Equity

Hearst, Member Equity

Cash

53,800

Arcadia Sales, LLC

Statement of LLC Liquidation

For Period August 1–31

+

Member Equity

=+++

65,800

29,400

149,000

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

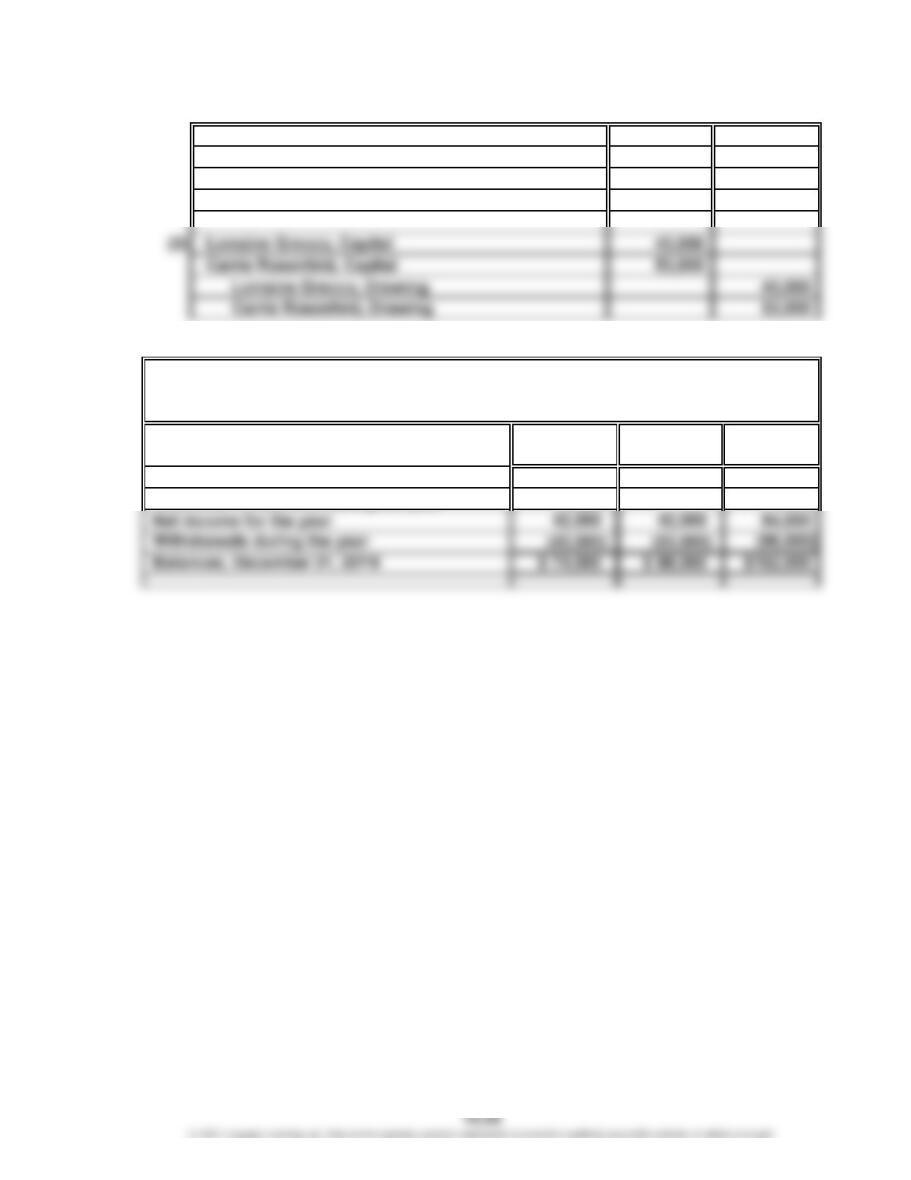

Ex. 12-25

a. (1) Revenues

Expenses 570,000

Lorraine Grecco, Capital

Carrie Rosenfeld, Capital

b.

Total

Balances, January 1, 20Y4 $163,000

Additional investment during the year 11,000

For the Year Ended December 31, 20Y4

$ 99,000

—

Rosenfeld

654,000

Lorraine

Grecco

42,000

42,000

$ 64,000

11,000

Carrie

Grecco and Rosenfeld

Statement of Partnership Equity

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Ex. 12-26

$19,900,000,000

79,347

b. The revenues increased between the two years from $18.6 billion to $19.9 billion, or

7.0% [($19.9 – $18.6) ÷ $18.6]. However, the number of employees has increased

Ex. 12-27

$27,270,000

135

$31,140,000

180

a. =

=Revenue per professional staff, current year: $250,797

a.

=

Revenue per employee, 20Y9:

Revenue per employee, 20Y8:

$202,000

$173,000

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-1A

1. Mar. 1 Cash 23,400

Merchandise Inventory 62,600

Eric Keene, Capital 86,000

1 Cash 39,000

Accounts Receivable 19,500

2.

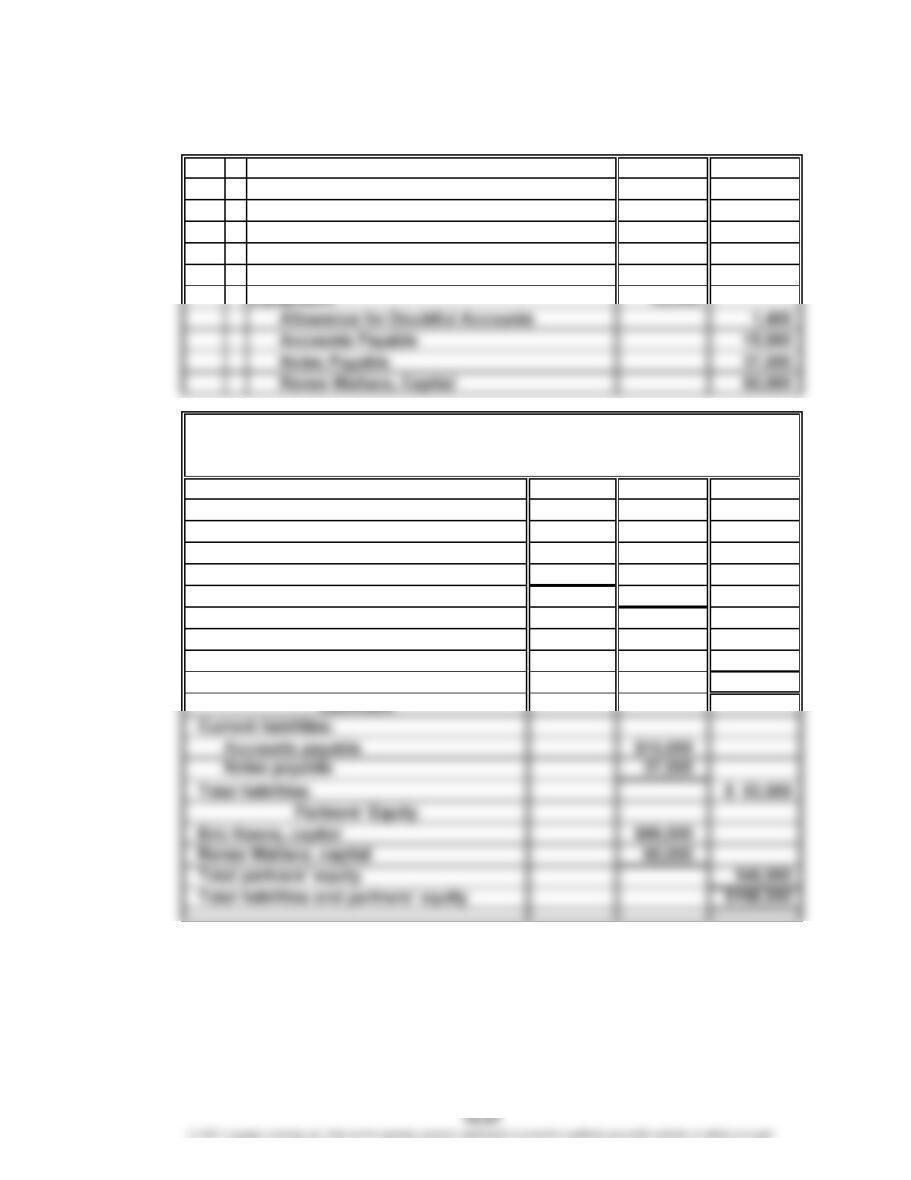

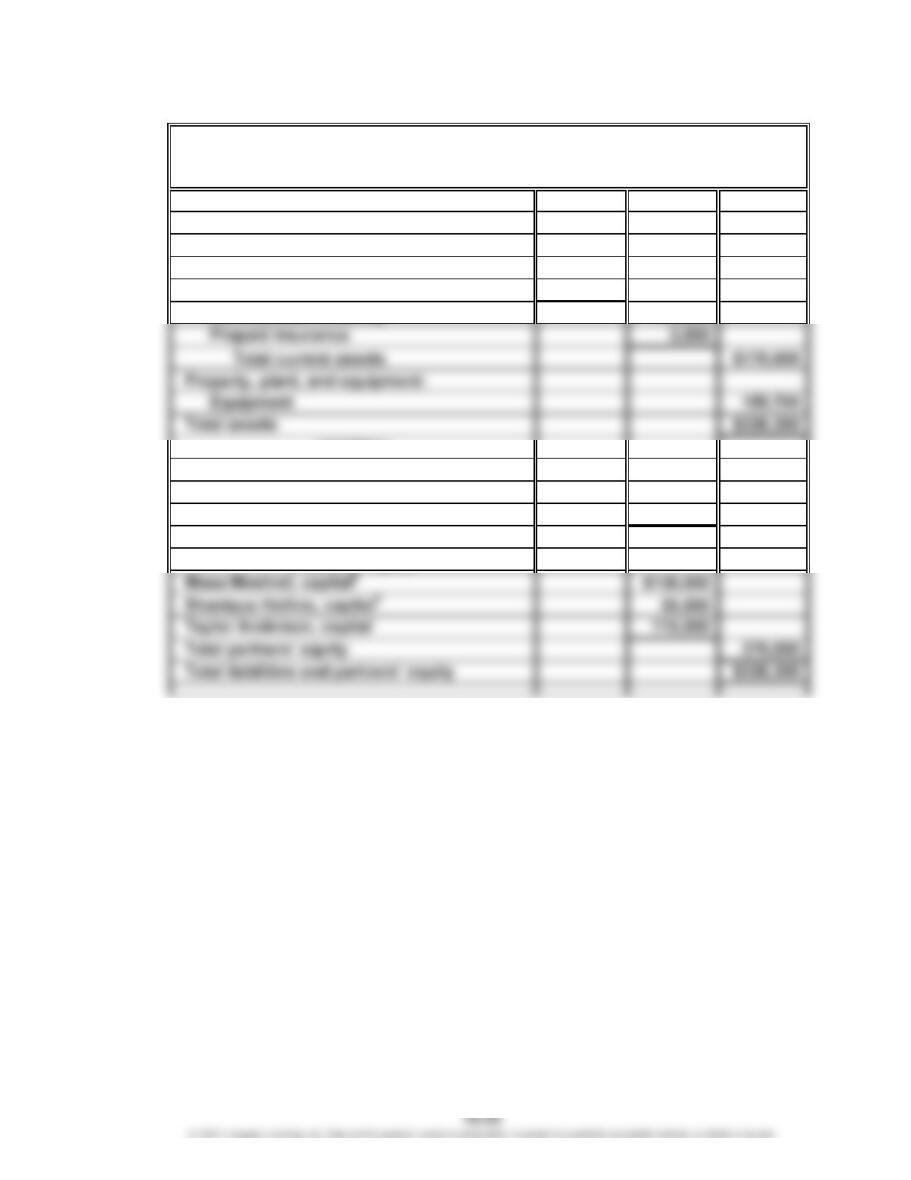

Current assets:

Cash $62,400

Accounts receivable $19,500

Less allowance for doubtful accounts 1,400 18,100

Merchandise inventory 62,600

Total current assets $143,100

Property, plant, and equipment:

Equipment 55,400

Total assets $198,500

*

$23,400 + $39,000

Assets

PROBLEMS

Keene and Wallace

Balance Sheet

March 1, 20Y8

*

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-1A (Concluded)

28 Eric Keene, Capital 19,000

Renee Wallace, Capital 24,000

Eric Keene, Drawing 19,000

Renee Wallace, Drawing 24,000

* Computations:

Total

Keene Wallace

12

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-2A

Plan Black Shannon Black Shannon

a. ……………………………………

…

$138,000 $138,000 $240,000 $240,000

b. ……………………………………

…

207,000 69,000 360,000 120,000

c. ……………………………………

…

92,000 184,000 160,000 320,000

Details:

a. Net income (1:1)………………

…

$138,000 $138,000 $240,000 $240,000

b. Net income (3:1)………………

…

$207,000 $69,000 $360,000 $120,000

c. Net income (1:2)………………

…

$92,000 $184,000 $160,000 $320,000

…

…

…

…

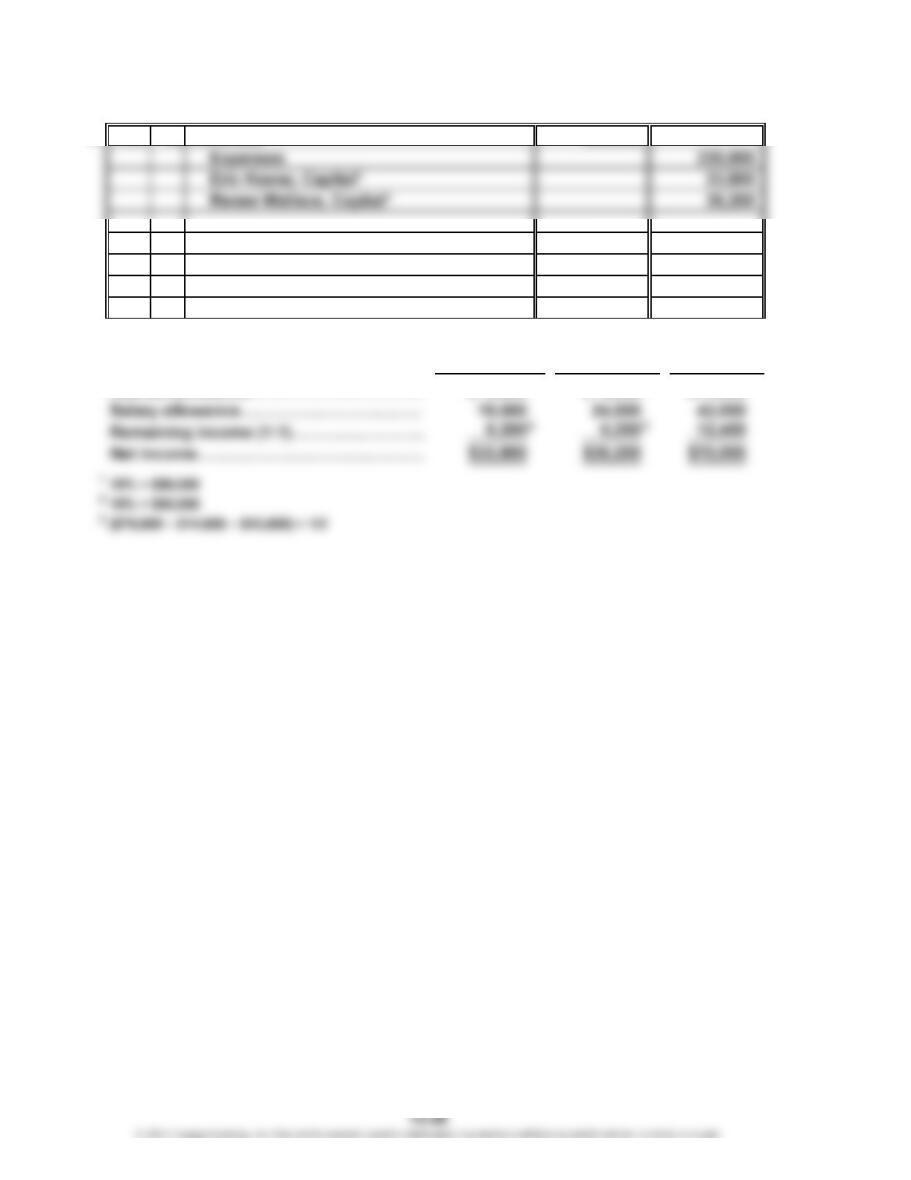

f. Interest allowance……………

…

$ 21,600 $ 7,200 $ 21,600 $ 7,200

Salary allowance………………

…

96,000 168,000 96,000 168,000

Bonus allowance………………

…

2,400 43,200

Excess of allowances over

income (1:1)…………………

…

(9,600) (9,600)

$276,000 $480,000

(1) (2)

$276,000 $480,000

Black Shannon Black Shannon

34

…

…

…

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-3A

1.

Professional fees

Operating expenses:

Salary expense

Depreciation expense—building

Division of net income:

Total

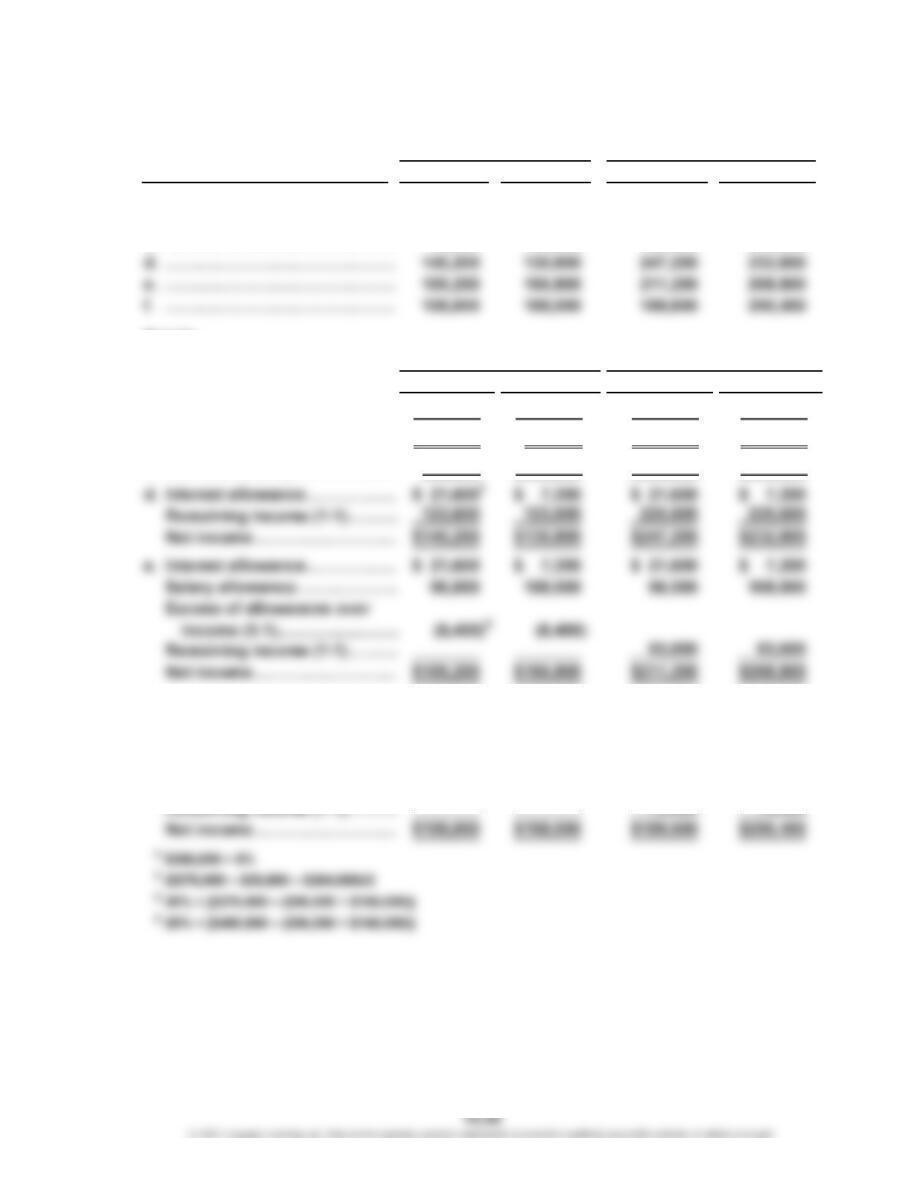

Salary allowance……………………………… $45,000 $54,700 $ 99,700

*

$135,000 × 10%

**

($88,000 – $10,000) × 10%

2.

Balances, January 1, 20Y3

Yost

Total

$ 78,000 $ 213,000

$135,000

JaylaTyler

Tyler

Lambert

Jayla

$154,500

15,700

Lambert and Yost

Income Statement

For the Year Ended December 31, 20Y3

$395,300

Lambert Yost

Lambert and Yost

Statement of Partnership Equity

For the Year Ended December 31, 20Y3

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-3A (Concluded)

3.

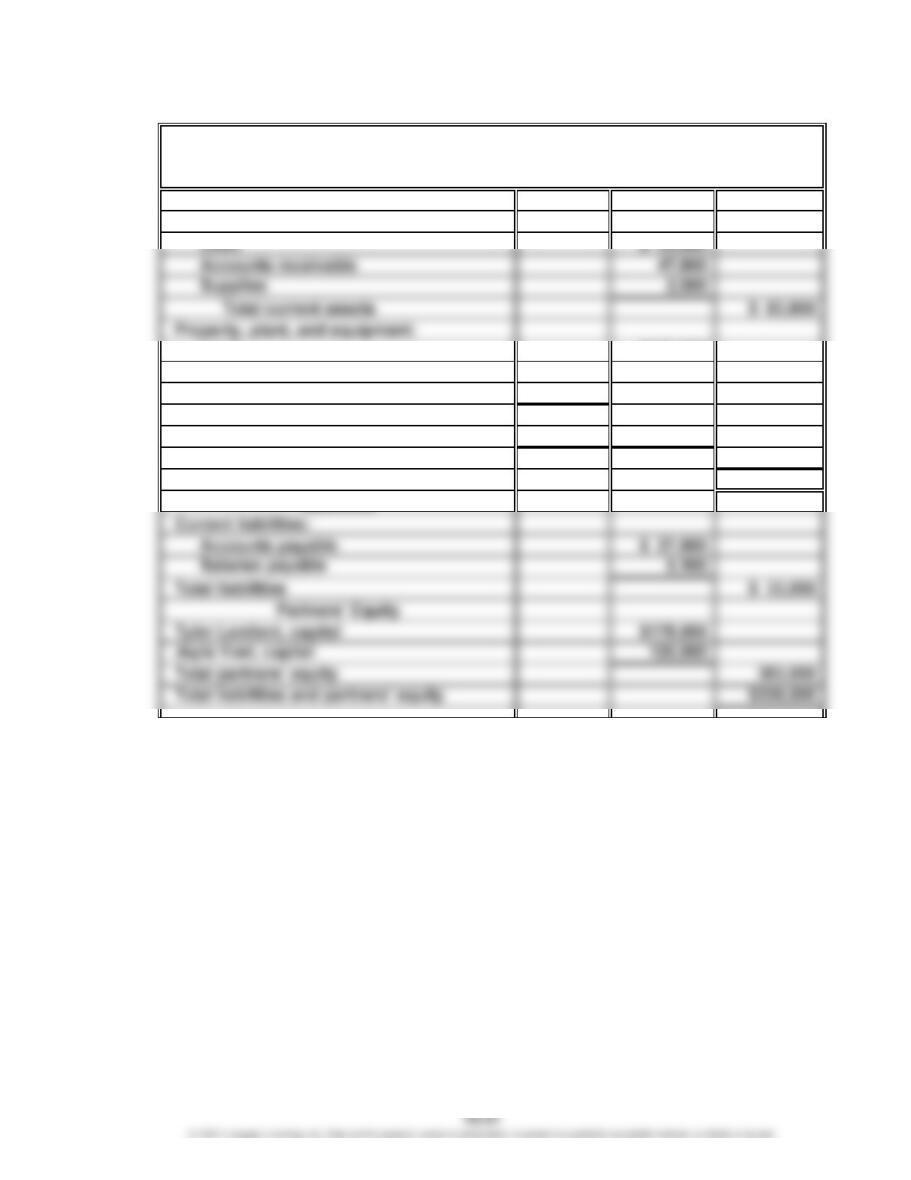

Current assets:

Land $120,000

Building $157,500

Less accumulated depreciation 67,200 90,300

Office equipment $ 63,600

Less accumulated depreciation 21,700 41,900

Total property, plant, and equip. 252,200

Total assets $336,000

Lambert and Yost

Balance Sheet

December 31, 20Y3

Assets

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-4A

1. June 30 Asset Revaluations 2,900

Accounts Receivable 2,500

Allowance for Doubtful Accounts 400

[($42,500 – $2,500) × 5%] – $1,600.

30 Accumulated Depreciation—Equipment 43,100

Equipment 24,800

Asset Revaluations 18,300

$155,700 – $180,500.

30 Asset Revaluations 20,000

Musa Moshref, Capital 10,000

Shaniqua Hollins, Capital 10,000

*

The asset revaluations account has a credit balance of ($2,900 – $4,600 – $18,300), which is

allocated to Moshref’s and Hollins’ capital accounts equally.

*

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-4A (Concluded)

3.

Current assets:

Cash1$ 53,000

Accounts receivable $40,000

Less allowance for doubtful accounts 2,000 38,000

Current liabilities:

Accounts payable $ 21,300

Notes payable 35,000

Total liabilities $ 56,300

1$8,000 + $45,000

2$120,000 + $10,000

3$85,000 + $10,000 – $70,000

Moshref, Hollins, and Anderson

Balance Sheet

July 1, 20Y7

Assets

Partners’ Equity

Liabilities

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-5A

1.

Noncash Gerloff Chu Jewett

Cash Assets Liabilities (2/4) (1/4) (1/4)

Balances before realization $ 5,200 $ 55,900 $ 15,000 $ 19,300 $ 4,500 $ 22,300

a. Sale of assets and division of loss 34,300 (55,900) —(10,800) (5,400) (5,400)

d. Cash distributed to partners (25,400) ——

(8,500) —(16,900)

Final balances $0 $0$0$0$0$0

The $900 deficiency of Chu would be divided between the other partners, Gerloff and Jewett, in their income-sharing ratio

(2:1, respectively). Therefore, Gerloff would absorb two-thirds of the $900 deficiency, or $600, and Jewett would absorb

one-third of the $900 deficiency, or $300.

b. William Gerloff, Capital*

*$8,500 – $600

** $16,900 – $300

Gerloff, Chu, and Jewett

Statement of Partnership Liquidation

For Period February 3–28

+=

Capital

+++

7,900

CHAPTER 12 Accounting for Partnerships and Limited Liability Companies

Prob. 12-6A

1. a.

Noncash Bowes Simmons Ahmed

Cash Assets Liabilities (2/5) (2/5) (1/5)

Balances before realization $ 38,000 $ 152,000 $ 24,000 $ 69,000 $ 85,000 $ 12,000

Sale of assets and division of gain 185,000 (152,000) —13,200 13,200 6,600

Bowes, Simmons, and Ahmed

Statement of Partnership Liquidation

For Period November 1–30

Capital

++=++