20 Minutes, Medium

a. Capital Stock Additional Total

($1 par Paid-in Retained Treasury Stockholders’

value) Capital Earnings Stock Equity

Balances, January 1, 20xx 130,000$ 1,170,000$ 1,400,000$ –$ 2,700,000$

Prior period adjustment (net of income tax benefit)

(47,000) (47,000)

Issuance of common stock; 20,000 shares @ $15 20,000 280,000 300,000

(part b is on following page)

PROBLEM 12.5B

DRY WALL, INC.

DRY WALL, INC.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20xx

Declaration and distribution of 10% stock dividend

b.

Declaration/distribution of a 10% stock dividend has no effect on total stockholders’

equity. Declaration of a cash dividend reduces total stockholders’ equity by the amount of

the dividend.

PROBLEM 12.5B

DRY WALL, INC. (concluded)

The two types of dividends do not have the same impact upon stockholders’ equity. A cash

40 Minutes, Strong

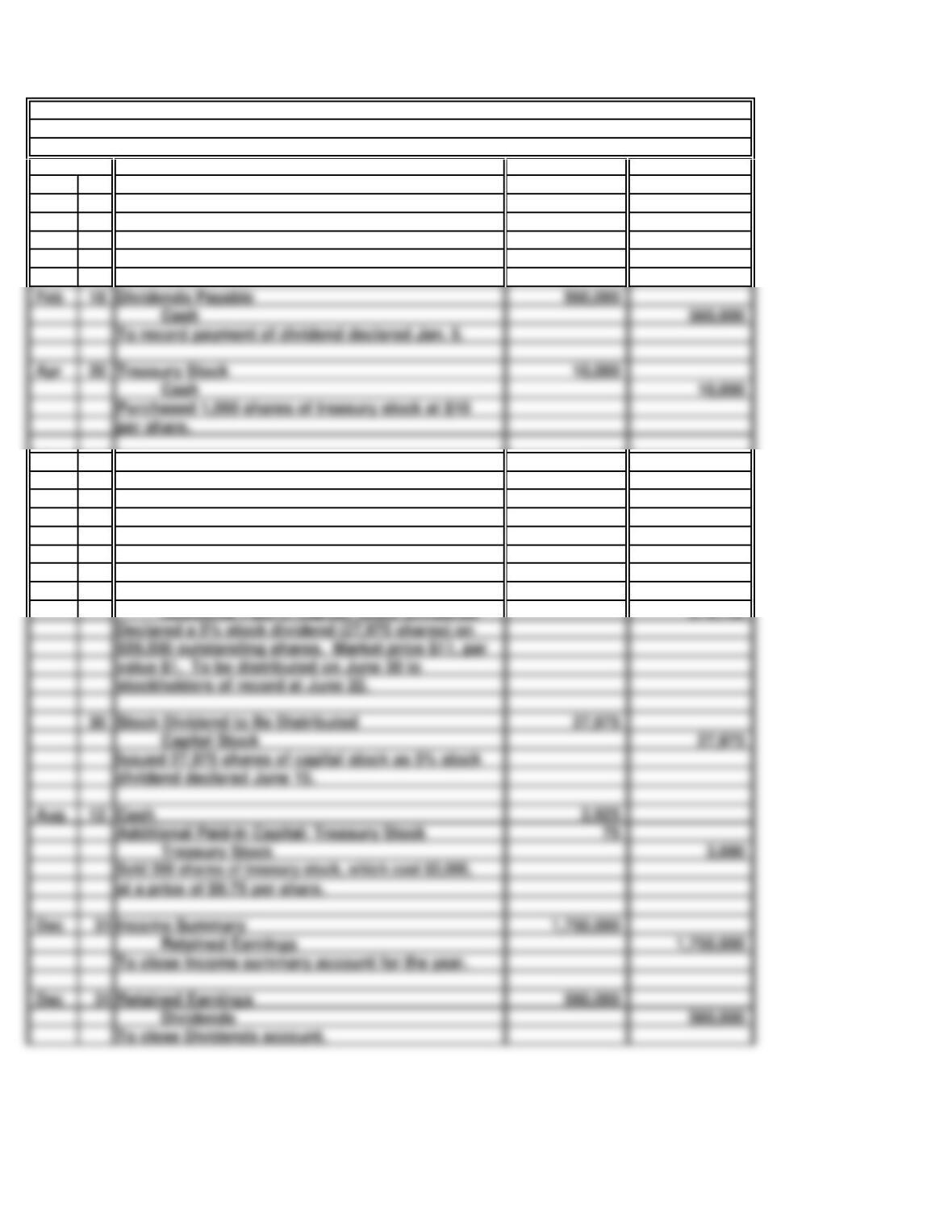

Jan 5 Dividends 560,000

Dividends Payable 560,000

May 25 Cash 6,000

Treasury Stock 5,000

1,000

June 15 307,725

27,975

279,750

Aug 12 2,925

Treasury Stock 3,000

Dec 31 1,750,000

1,750,000

Dec 31 560,000

at a price of $9.75 per share.

Income Summary

Retained Earnings

To close Dividends account.

Retained Earnings

To close Income summary account for the year.

Declared a 5% stock dividend (27,975 shares) on

Issued 27,975 shares of capital stock as 5% stock

Additional Paid-in Capital: Treasury Stock

value $1. To be distributed on June 30 to

stockholders of record at June 22.

Stock Dividend to Be Distributed

dividend declared June 15.

Cash

559,500 outstanding shares. Market price $11, par

dividend payable on Feb. 18 to stockholders of

PROBLEM 12.6B

a.

General Journal

GREENE, INC.

record on Jan. 31.

2018

To record declaration of $1 per share cash

Additional Paid-in Capital: Stock Dividends

Sold 500 shares of treasury stock, which cost

$5,000, at a price of $12 per share.

Additional Paid-in Capital: Treasury Stock

Retained Earnings

Stock Dividend to Be Distributed

Feb 18 560,000

Apr 20 10,000

Dividends Payable

To record payment of dividend declared Jan. 5.

Cash

per share.

Purchased 1,000 shares of treasury stock at $10

Treasury Stock

b.

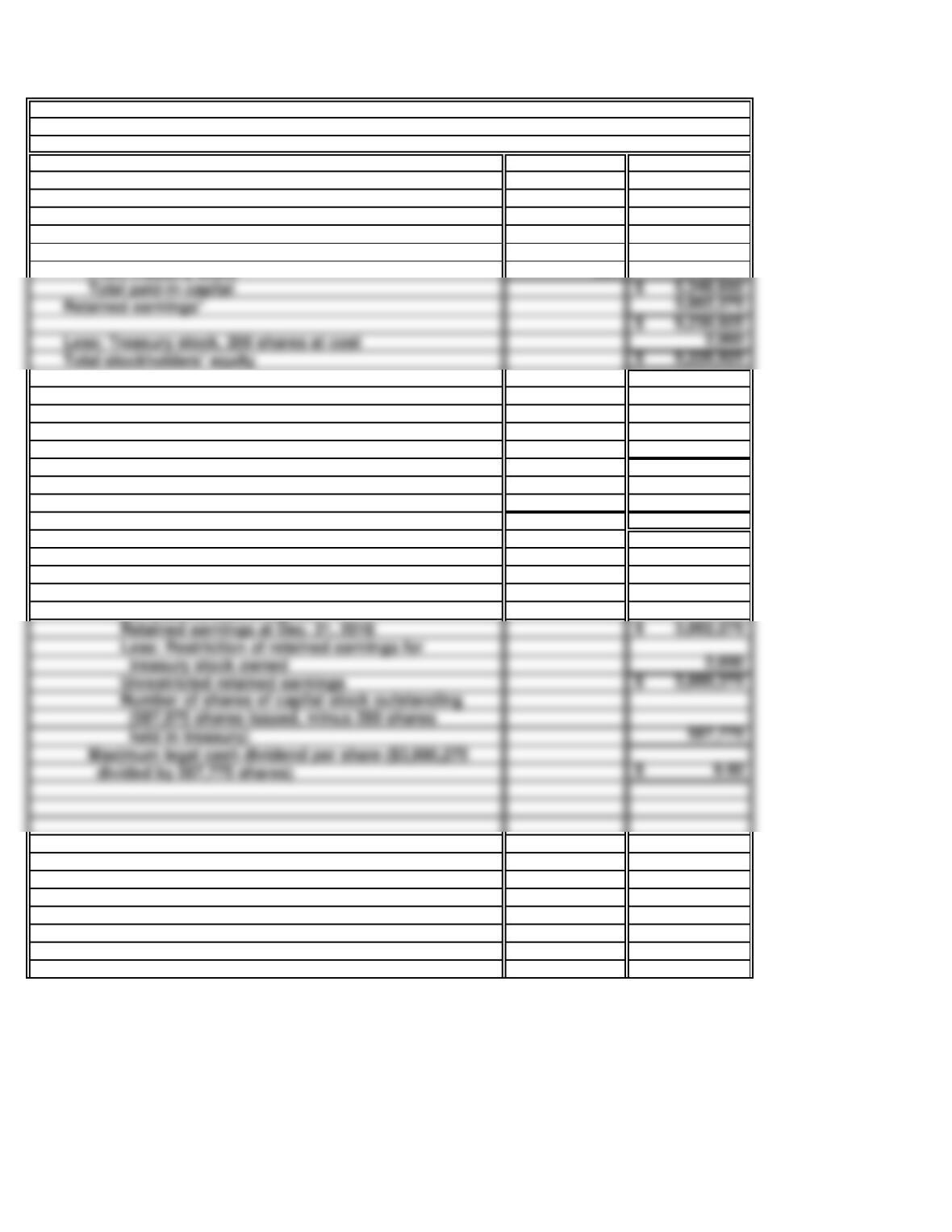

Stockholders’ equity:

Capital stock, $1 par value, 1,000,000 shares authorized,

587,975 shares issued, of which 200 are held in the treasury 587,975$

Additional paid-in capital:

From issuance of capital stock 4,480,000$

From stock dividend 279,750

From treasury stock 925 4,760,675

*Computation of retained earnings at Dec. 31, 2018:

Retained earnings at beginning of year 3,000,000$

Add: Net income for year 1,750,000

Subtotal 4,750,000$

Less: Cash dividend declared Jan. 5 560,000$

Stock dividend declared June 15 307,725 867,725

Retained earnings, Dec. 31, 2018 3,882,275$

c. Computation of maximum legal cash dividend

per share at Dec. 31, 2018:

Unrestricted retained earnings 3,880,275$

Maximum legal cash dividend per share ($3,880,275

divided by 587,775 shares) 6.60$

PROBLEM 12.6B

GREENE, INC.

December 31, 2018

Partial Balance Sheet

GREENE, INC. (concluded)

Total paid-in capital 5,348,650$

Retained earnings* 3,882,275

Less: Treasury stock, 200 shares at cost 2,000

30 Minutes, Strong

Net

(from

Income Source)

NE DNE NE

b. 1.

2.

3.

4.

5.

The purchase of treasury stock has no effect on either revenue or expenses and,

Reissuance of treasury stock at a price less than its original cost results in a loss, but

HOT WATER, INC.

Payment of a cash dividend has no effect on revenue or expenses, but it reduces cash.

1

PROBLEM 12.7B

Stockholders’

Equity

Current

Assets

Net Cash Flow

Declaration of a cash dividend has no immediate effect upon net income or cash flows.

a.

Event

2

3

4

5

50 Minutes, Strong

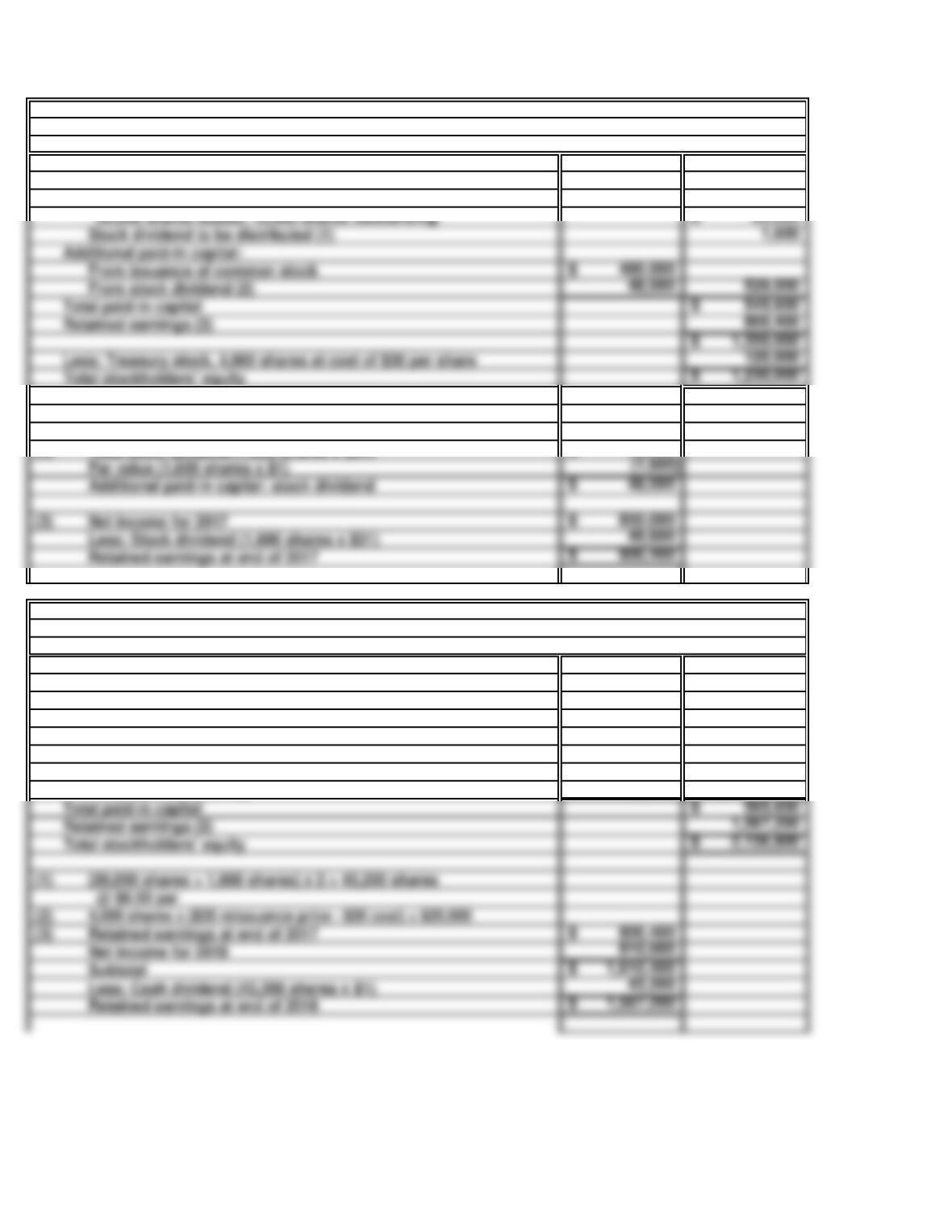

a.

Stockholders’ equity:

Capital stock:

Common stock, $1 par, 100,000 shares authorized,

(1) (20,000 shares – 4,000 shares) x 10% = 1,600 shares

@$1 par

(2) Total stock dividend (1,600 shares x $31) 49,600$

Par value (1,600 shares x $1) (1,600)

Additional paid-in capital: stock dividend 48,000$

Less: Stock dividend (1,600 shares x $31) 49,600

Retained earnings at end of 2017 800,400$

b.

Stockholders’ equity:

Capital stock:

Common stock, $0.50 par, 200,000 shares authorized,

43,200 shares issued and outstanding (1) 21,600$

Additional paid-in capital:

From issuance of common stock 480,000$

From stock dividend 48,000

From treasury stock (2) 20,000 548,000

Total paid-in capital 569,600$

(1) (20,000 shares + 1,600 shares) x 2 = 43,200 shares

@ $0.50 par

(2) 4,000 shares x ($35 reissuance price – $30 cost) = $20,000

(3) Retained earnings at end of 2017 800,400$

Retained earnings at end of 2018 1,567,200$

December 31, 2018

PROBLEM 12.8B

ADAMS CORPORATION

December 31, 2017

Partial Balance Sheet

ADAMS CORPORATION

ADAMS CORPORATION

Partial Balance Sheet

20,000 shares issued, 16,000 shares outstanding 20,000$

Stock dividend to be distributed (1) 1,600

Additional paid-in capital:

From issuance of common stock 480,000$

From stock dividend (2) 48,000 528,000

Total paid-in capital 549,600$

25 Minutes, Strong

CORP.

a.

(Dollars in

Thousands)

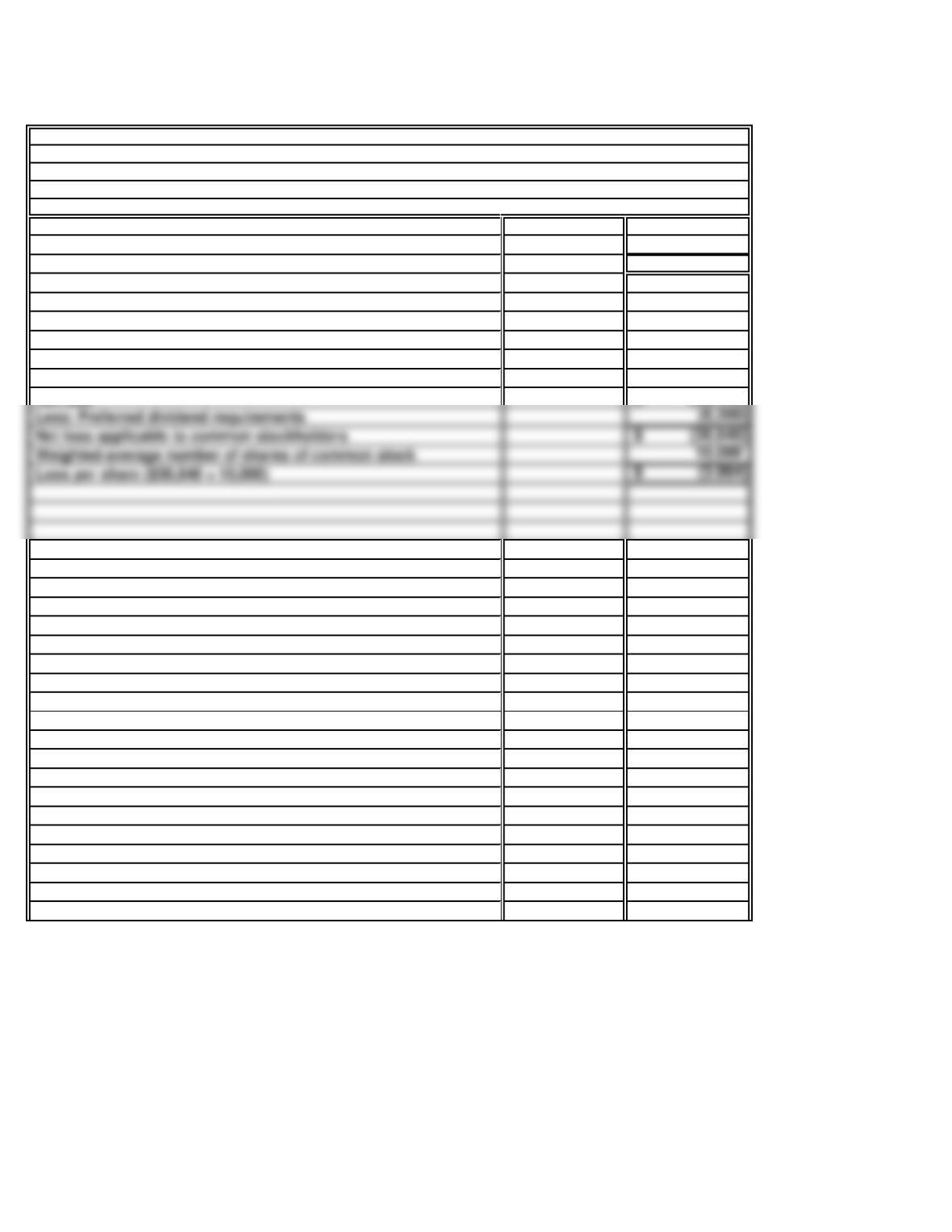

Loss from continuing operations [($(38,940) – $(17,500)] (56,440)$

Income from discontinued operations 24,000

Net loss (32,440)$

b.

Net loss (32,440)$

PROBLEM 12.9B

CARDINAL MANUFACTURING CORPORATION

For the Year Ended December 31, Current Year

Partial Income Statement

CARDINAL MANUFACTURING

Less: Preferred dividend requirements (6,200)

Net loss applicable to common stockholders (38,640)$

Weighted-average number of shares of common stock 10,000

20 Minutes, Easy

a.

b.

c.

SOLUTIONS TO CRITICAL THINKING CASES

WHAT’S THIS?

CASE 12.1

ATLANTIC RICHFIELD: Both the operating loss from the noncoal minerals activities and the

GEORGIA PACIFIC: This item appears to meet the criteria for being presented as an

UNION CARBIDE: The explosion of a chemical plant for a company like Union Carbide

20 Minutes, Medium

b.

d.

CASE 12.2

The operating loss incurred by the baseball team in 2018 indicates that the team’s expenses (net of tax

In 2018, JPI’s newspaper business earned $4,500,000, as shown by the subtotal, Income from

IS THERE LIFE WITHOUT BASEBALL?

30 Minutes, Strong

a.

The diluted earnings per share figures show the effect that conversion of all of the

convertible preferred stock into common shares would have had upon this year’s

CASE 12.3

USING EARNINGS PER SHARE FIGURE

The company reports earnings per share computed on both a basic and a diluted basis

because it has outstanding convertible preferred stock. The conversion of these securities

35 Minutes, Strong

a.

c.

e.

g.

CASE 12.4

INTERPRETING A STATEMENT OF

STOCKHOLDERS’ EQUITY

Beginning of year: 77,987,500 shares outstanding (82,550,000 issued – 4,562,500 held in

treasury)

This answer appears reasonable, since the number of common shares outstanding ranged

The stock issued during the year for the stock option plans consisted of treasury shares, not

newly issued shares. The Treasury Stock account is used to account for repurchases of a

The aggregate reissue price for the treasury shares must have been lower than the cost to

acquire those treasury shares, because the Additional Paid-in Capital account was reduced

60 Minutes, Strong

a.

b.

c

d.

Writing assets down, or writing them entirely off, now should have a positive effect on

One would expect the earnings per share to be less as the losses flow through the income

CASE 12.5

An asset represents something with future economic benefit. But if the amount at which the

These losses appear to be unusual and/or infrequent. At least, management would hope

CLASSIFICATION OF UNUSUAL ITEMS—

AND THE POTENTIAL FINANCIAL IMPACT

e.

Note to instructor: This case is adapted from an incident involving an international

pharmaceutical company. The details of the situation have been altered for the purpose of

creating an introductory level textbook assignment, and the so-called quotations from corporate

Who were the losers? Anyone who bought the stock between the release of the original earnings

figures and the announcement that substantial losses would be reclassified.

Writing off losses currently would be expected to positively effect earnings in future periods.

The assets that are being written down or written completely off will no longer be

CASE 12.5

CLASSIFICATION (continued)

30 Minutes, Medium

The fact that sales are sluggish but net income is steadily increasing at least raises an issue that

should be explored. All other things being equal, which they rarely are, one would not expect this

A possible explanation that is at least worth exploring is whether management has taken

conscious steps to overstate inventory. The motivation would be to increase reported net income

to enhance the position of management. The relationship of inventory to net income is as follows:

an overstatement of inventory is offset by an understatement of cost of goods sold which, in turn,

overstates net income. By overstating inventory, either intentionally or in error, net income is

improved and the company appears to be more profitable that it actually is.

CASE 12.6

MANAGING PROFITABILITY

This case is tended to encourage students to think about how certain financial statement numbers

should ordinarily be expected to move in relation to other numbers (e.g., net income in

comparison with sales) and steps that might be taken by management to manage, or manipulate

Relationship of sales revenue and net income

ETHICS, FRAUD & CORPORATE GOVERNANCE

CASE 12.6

MANAGING PROFITABILITY (concluded)

Reduction in allowance for inventory obsolescence

The allowance to reduce inventory for obsolescence functions much as an allowance for

uncollectible accounts does to reduce accounts receivable to their net realizable value. If

inventory includes some obsolescence, but the specific obsolete items are not known in advance,

an allowance is established to reduce the total inventory to a lower recoverable amount with the

specific items that include the obsolescence to be determined at some later time. From the

30 Minutes, Medium

c. There is no direct relationship between the amount the stock originally sold for and

d. The three-year trend in basic earnings per share (EPS), including discontinued

CASE 12.7

INTERNET

a. Martin Marietta Materials, Inc. is a leading supplier of aggregate and heavy building

b. The number of shares of common stock outstanding on Dec. 31, 2015 was

STOCKHOLDERS’ EQUITY AND EPS