365

CHAPTER 12

DIFFERENTIAL ANALYSIS AND

PRODUCT PRICING

CLASS DISCUSSION QUESTIONS

1. a. Differential revenue is the amount of

increase or decrease in revenue ex-

pected from a particular course of action

compared with an alternative.

2. This decision is an example of a make-or-buy

decision. The company is focusing on its

comparative advantages, which include

marketing and distribution, while building

partnerships with other suppliers to actually

manufacture key elements of the product.

4. Assuming there is demand for the premium-

grade product, this would assume the differ-

ential price (premium less commodity)

exceeded the differential cost to process the

product to premium grade.

5. A business should only accept business at a

special price if the lower price will not con-

offering discount business to a customer

that may wish to order in the future.

6. Other issues to consider would be if the

$1.60 ($7.75 – $6.15). That is, if the elimi-

nated fixed cost were less than $1.60 per

unit, then the variable cost per unit would

exceed the supplier’s price, making the sup-

plier price more attractive. The company

must also consider the reliability of the sup-

value of the equipment and land (either in

cash or rental income) should be consid-

ered. For example, if the opportunity value

of the assets were $10,000 per month, then

the store would need to have a profitability

exceeding this amount to remain an attrac-

tive alternative.

8. In the long run, the normal selling price must

366

10. In setting prices, managers should also

11. The target cost concept begins with a price

that can be sustained in the marketplace,

then subtracts a target profit, thus determin-

ing the target cost. The cost is made to

conform to the price required in the market. In

12. The target cost concept is most appropriate

in highly competitive product markets, where

margins are under pressure and prices are

falling.

367

EXERCISES

E12–1

a. PIKE INDUSTRIES

Proposal to Lease or Sell Machinery

Differential Analysis Report

Differential revenue from alternatives:

Revenue from lease …………………………………………… $107,500

Proceeds from sale ……………………………………………. (72,500)

Differential revenue from lease ……………………… $ 35,000

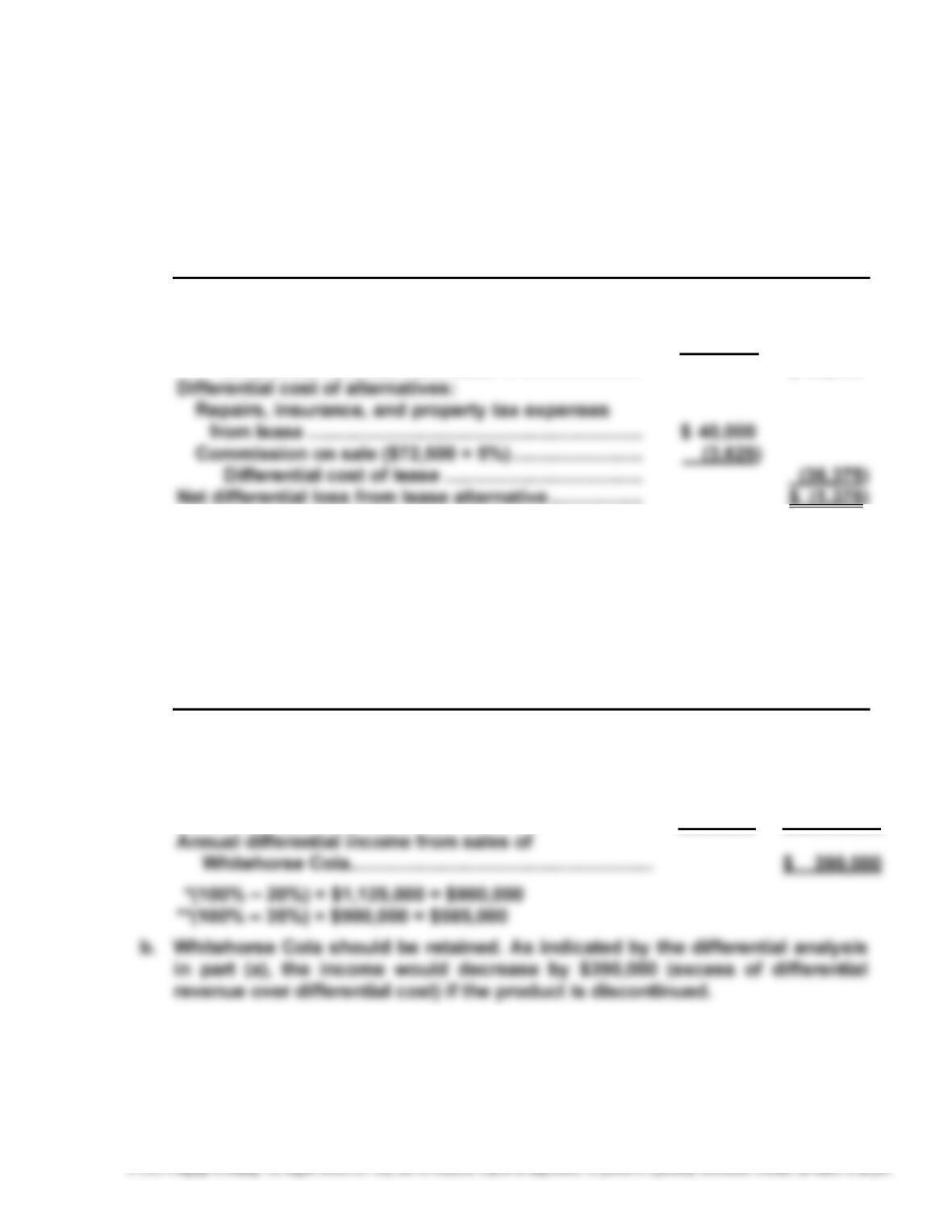

b. Sell the machinery. The net loss from leasing is $1,375.

E12–2

a. YUKON BEVERAGES INC.

Proposal to Discontinue Whitehorse Cola

Differential Analysis Report

Differential revenue from annual sales of Whitehorse Cola:

Revenue from sales …………………………………………….. $ 1,875,000

Differential cost of annual sales of Whitehorse Cola:

Variable cost of goods sold …………………………………. $900,000*

Variable operating expenses ………………………………… 585,000** (1,485,000)

368

E12–3

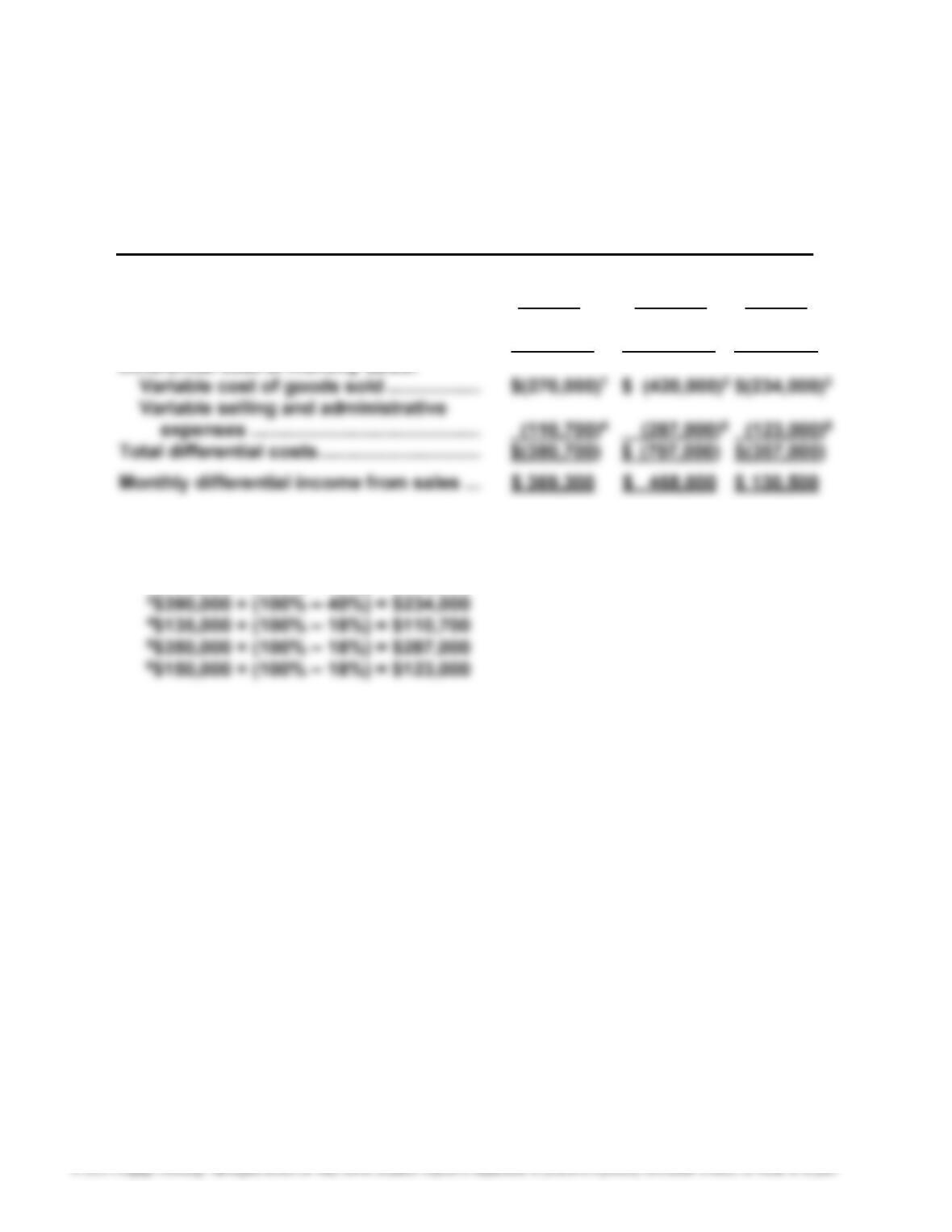

a.

BLONDE ESPRESSO COMPANY

Product-Line Income Statement

Differential Analysis Report

Light Medium Dark

Roast Roast Roast

Differential revenue from monthly sales:

Revenue from sales …………………………. $ 750,000 $1,175,000 $ 487,500

Computations:

1$450,000 × (100% – 40%) = $270,000

2$700,000 × (100% – 40%) = $420,000

b. The Dark Roast line should be retained. As indicated by the differential analy-

sis in part (a), the income would decrease by $130,500 (excess of differential

revenue over differential cost) if the Dark Roast line is discontinued.

369

E12–4

Note to Instructors: Many students may be unfamiliar with the financial services

industry. This exercise provides an opportunity to introduce students to some

basic terms and concepts used within the industry.

a. The “Investor (Retail) Services” segment serves the retail customer, meaning

b. Variable costs in the “Investor (Retail) Services” segment include:

1. Commissions to brokers

Fixed costs in the “Investor (Retail) Services” segment include:

1. Depreciation on brokerage offices

c.

Investor

(Retail) Advisor

Services Services

Operating income before taxes ……………… $2,475 $1,175

Plus depreciation and amortization ……….. 203 66

Estimated contribution margin ……………… $2,678 $1,241

d. If one assumes that the fixed assets that serve advisory services (computers,

370

E12–5

The flaw in the decision was the failure to focus on the differential revenues and

costs, which indicate that operating income would be reduced by $42,500 if Half

Moon is discontinued. This differential income from sales of Half Moon can be de-

termined as follows:

E12–6

a. POST TECHNOLOGIES COMPANY

Manufacture Carrying Case

Differential Analysis Report

Purchase price of carrying case ……………………………. $ 13.00

Differential cost to manufacture carrying case:

Direct materials …………………………………………………. $4.00

371

E12–7

a. WISCONSIN ARTS OF MILWAUKEE

Purchase Outside Page Layout Services

Differential Analysis Report

Differential revenue:

Residual value of computer equipment ……………………. $ 6,500

Differential cost of alternatives:

Cost to perform internally:

Salaries ………………………………………………………………. $ 185,000

b. The benefit from using an outside service is shown to be $11,500 greater than

performing the layout work internally. The fixed costs (depreciation expens-

es) in the budget are irrelevant to the decision. Thus, based strictly on a fi-

nancial basis, the work should be purchased from the outside. In addition, the

c. Before electing to terminate the five employees, Wisconsin Arts should con-

sider the long-run impact of the decision. Specifically, future page layout

372

E12–8

a. Annual variable costs—old equipment ………………….. $ 30,000

Annual variable costs—new equipment …………………. (9,000)

Annual differential decrease in cost ………………………. $ 21,000

Number of years applicable …………………………………… × 8

b. The sunk cost is the $185,000 book value ($315,000 cost less $130,000

accumulated depreciation) of the old equipment. The original cost and accumu-

lated depreciation were incurred in the past and are irrelevant to the decision

to replace the machine.

373

E12–9

a. WHITE NOISE TECHNOLOGIES INC.

Replace Machine

Differential Analysis Report

Annual costs and expenses—present machine ………………………….. $ 432,500

Annual costs and expenses—new machine ……………………………….. (411,000)

Annual differential decrease in costs and expenses …………………… $ 21,500*

Decrease in direct labor costs ………………………………….. $ 50,000

Less: Increase in power and maintenance ……………….. $25,000

Increase in taxes, insurance, etc. ………………….. 3,500 (28,500)

Annual differential decrease in costs and expenses ….. $ 21,500

b. The proposal should be accepted.

c. In addition to the factors given, consideration should be given to such factors

E12–10

a. Differential revenue: $415 – $320 = $95 per hundred board feet

374

E12–11

a. HAPPY HOUR COFFEE COMPANY

Process Columbian Coffee Further

Differential Analysis Report

Differential revenue from further processing per batch:

Revenue from sale of Decaf Columbian [(5,000

pounds – 150* pounds loss) × $9.50] ………………………… $ 46,075

b. The differential revenue from processing further to Decaf Columbian is more

than the differential cost of processing further. Thus, Happy Hour Coffee Com-

pany should process further to Decaf Columbian.

c. The price of Decaf Columbian would need to decrease to $9.02 per pound in

order for the differential analysis to yield neither an advantage nor a disad-

vantage (indifference). This is determined as follows:

Revenue from sale of Columbian coffee

(5,000 pounds × $8.00) …………………………………………….. 40,000

Differential revenue ………………………………………………………… $ 3,747

Differential cost per batch:

Additional cost of producing Decaf Columbian …………….. (3,750)

Differential income from further processing:

375

E12–12

a. MADISON INDUSTRIES INC.

Sell to Story Mills Company

Differential Analysis Report

Differential revenue from accepting the offer:

Revenue from sale of 125,000 additional units at $41 ……………. $5,125,000

Differential cost of accepting the offer:

Variable costs from sale of 125,000 additional units at $36 ……. (4,500,000)

Differential income from accepting the offer ……………………………… $ 625,000

E12–13

a. Budgeted cost per battery for June = Total manufacturing costs ÷ Budgeted

production

Budgeted cost per battery for June = $1,434,000 ÷ 60,000 batteries = $23.90

per battery

376

E12–14

a. RUBBER MEETS THE ROAD COMPANY

Sell to Cruising Motors

Differential Analysis Report

Per Unit Total

Differential revenue from accepting special offer … $10.00 $ 200,000*

Differential costs from accepting special offer:

Direct materials ………………………………………………. $ 5.00

*$10 × 20,000 tires = $200,000

**2% × $20. The avoided sales commission should not be computed on the

basis of the $10 price to Cruising Motors, but on the existing domestic sales

price of $20.

***$9.20 × 20,000 tires = $184,000

b. Differential cost per tire for special order:

377

E12–15

a. $2,400,000 ($12,000,000 × 20%)

b. Total costs:

Variable ($240 × 200,000 units) …………………………………………….. $48,000,000

Fixed ($800,000 + $1,200,000) ………………………………………………. 2,000,000

d. Cost amount per unit ……………………………………………………………….. $250

Markup ($250 × 4.8%) ………………………………………………………………. 12

Selling price …………………………………………………………………………….. $262

E12–16

a. The price will be set at the estimated average market price required to remain

competitive, or $26,000. Under the target cost concept, the market dictates

the price, not the markup on cost.

Since the estimated manufacturing cost of $22,000 exceeds the target cost of

$20,800, Toyota will try to remove $1,200 from its total costs in order to main-

tain competitive pricing within its profit objectives.

378

E12–17

a. Historical markup percentage on product cost: $200 –– $160

$160 = 25% or

b. Required cost reduction: $160.00 – $145.60 = $14.40

c.

1. Direct labor reduction: min. 60

min. 6 × $20 = $ 2.00

2. Additional inspection: min. 60

min. 9 × $20 = $(3.00)

Direct materials reduction: 7.25 4.25

The total savings exceeds the required target cost reduction by $0.65 ($15.05 –

$14.40). Thus, these improvements are sufficient to meet the target cost.

E12–18 Appendix

a. Total manufacturing costs:

Variable ($220 × 200,000 units) …………………………………………….. $44,000,000

Fixed factory overhead ……………………………………………………….. 800,000

Total ……………………………………………………………………………………….. $44,800,000

Cost amount per unit: $44,800,000 ÷ 200,000 units = $224

379

c. Cost amount per unit ……………………………………………………………….. $224

Markup ($224 × 16.96%) ……………………………………………………………. 38

Selling price …………………………………………………………………………….. $262

E12–19 Appendix

a. Total variable costs: $240 × 200,000 units …………………………………. $48,000,000

c. Cost amount per unit ……………………………………………………………….. $240

Markup ($240 × 9.17%) ……………………………………………………………… 22

Selling price …………………………………………………………………………….. $262