CHAPTER 12

Accounting for Partnerships

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Discuss and account

for the formation of a

partnership.

1, 2, 3, 4, 5,

17

1, 2

1

1, 2, 3

1A

2. Explain how to account for

net income or net loss of a

partnership.

6, 7, 8, 9, 10,

11

3, 4, 5

2

4, 5, 6, 7

1A, 2A

3. Explain how to account for

12, 13, 14, 15,

6

8, 9, 10

3A

*4. Prepare journal entries when

a new partner is either

admitted or withdraws.

18, 19, 20, 21,

7, 8, 9, 10

11, 12, 13, 14,

15

4A, 5A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare entries for formation of a partnership

and a balance sheet.

Simple

20–30

2A

Journalize divisions of net income and prepare

a partners’ capital statement.

Moderate

30–40

3A

Prepare entries with a capital deficiency in liquidation

of a partnership

Moderate

30–40

Journalize withdrawal of a partner under different

Moderate

30–40

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 12

ACCOUNTING FOR PARTNERSHIPS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

AP

Simple

2–4

BE2

1

AP

Simple

3–5

BE3

2

AP

Simple

4–6

BE4

2

AP

Simple

4–6

BE5

2

AP

Simple

6–8

BE6

3

AP

Simple

2–4

4

AP

Simple

2–4

4

AP

Simple

3–5

4

AP

Simple

2–4

*BE10

4

AP

Simple

3–5

DI1

1

C

Simple

2–4

DI2

2

AP

Simple

4–6

DI3a

3

AP

Simple

8–10

DI3b

3

AP

Moderate

6–8

EX1

1

C

Simple

6–8

EX2

1

AP

Simple

6–8

EX3

1

AP

Simple

4–6

EX4

2

AP

Simple

10–12

EX5

2

AP

Simple

8–10

EX6

2

AP

Simple

6–8

EX7

2

AP

Simple

8–10

EX8

3

AP

Simple

6–8

EX9

3

AP

Simple

6–8

EX10

3

AP

Simple

6–8

*EX11

4

AP

Simple

4–6

*EX12

4

AP

Simple

6–8

*EX13

4

AP

Simple

4–6

*EX14

4

AP

Moderate

8–10

*EX15

4

AP

Moderate

6–8

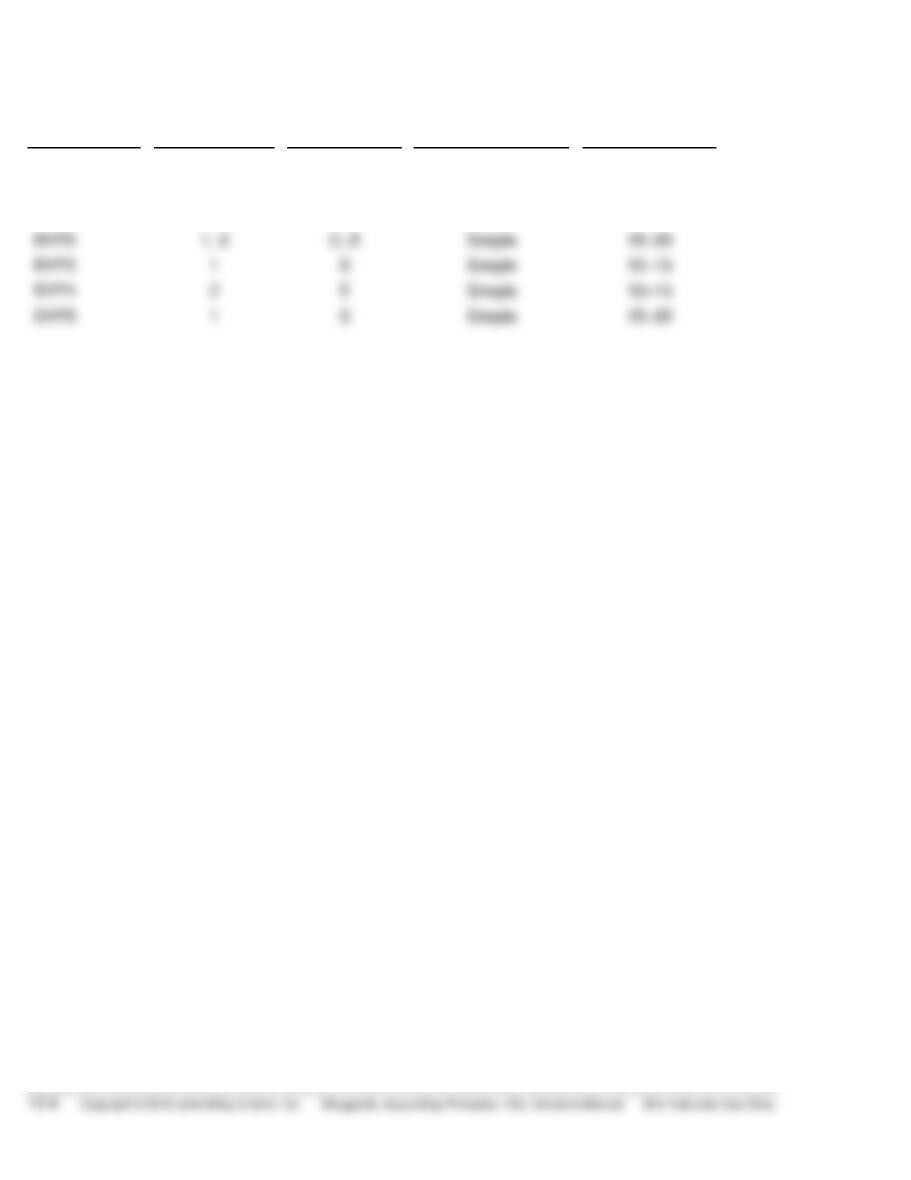

P1A

1, 2

AP

Simple

20–30

P2A

2

AP

Moderate

30–40

P3A

3

AP

Moderate

30–40

ACCOUNTING FOR PARTNERSHIPS (Continued)

Number

LO

BT

Difficulty

Time (min.)

*P4A

4

AP

Moderate

30–40

*P5A

4

AP

Moderate

30–40

BYP1

—

C

Simple

8–10

BYP2

Simple

15–20

BYP3

1

S

Simple

10–15

BYP4

2

E

Simple

10–15

BYP5

1

S

Simple

15–20

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Discuss and account for

the formation of a

partnership.

Q12-1 Q12-17

Q12-2 DI12-1

Q12-3 E12-1

Q12-4

Q12-5

BE12-1

BE12-2

E12-2

E12-3

P12-1A

2. Explain how to account for

net income or net loss of a

Q12-6

Q12-7

Q12-8

Q12-10

E12-5

EI12-6

3. Explain how to account for

the liquidation of a

partnership.

Q12-12

Q12-13

Q12-14

Q12-15

Q12-16

BE12-6

DI12-3a

DI12-3b

E12-8

E12-9

E12-10

P12-3A

*4. Prepare journal entries

when a new partner is

either admitted or

withdraws.

Q12-18

Q12-19

Q12-23

Q12-24

Q12-20

Q12-21

Q12-22

BE12-7

E12-12

E12-13

E12-14

E12-15

partnership.

Q12-9

BE12-3

EI12-7

ANSWERS TO QUESTIONS

1. (a) Association of individuals. A partnership is a voluntary association of two or more individuals

based on as simple an act as a handshake. Preferably, however, the agreement should be in

writing. A partnership is both a legal entity and an accounting entity, but it is not a taxable entity.

(b) Limited life. A partnership does not have unlimited life. A partnership may be ended voluntarily

or involuntarily. Thus, the life of a partnership is indefinite. Any change in the members of a

2. (a) Mutual agency. This characteristic means that the act of any partner is binding on all other

partners when engaging in partnership business. This is true even when the partners act

beyond the scope of their authority, so long as the act appears to be appropriate for the

partnership.

(b) Unlimited liability. Each partner is personally and individually liable for all partnership liabilities.

Creditors’ claims attach first to partnership assets and then to personal resources of any

partner, irrespective of that partner’s equity in the partnership.

3. The advantages of a partnership are: (1) combining skills and resources of two or more individuals,

(2) ease of formation, (3) freedom from governmental regulations and restrictions, and (4) ease

of decision making. Disadvantages are: (1) mutual agency, (2) limited life, and (3) unlimited liability.

7. Factors to be considered in determining how income and loss should be divided are: (1) a fixed

ratio is easy to apply and it may be an equitable basis in some circumstances; (2) capital balance ratios,

when the funds invested in the partnership are considered the most critical factor; and (3) salary

allowance and/or interest allowance coupled with a fixed ratio. This last approach gives specific

recognition to differences that may exist among partners by providing salary allowances for time

worked and interest allowances for capital invested.

8. The net income of $42,000 should be divided equally—$21,000 to M. Elston and $21,000 to R. Ogle

Questions Chapter 12 (Continued)

10.

Division of Net Income

T. Greer

R. Parks

Total

Salary Allowance ………………………………………

Deficiency: ($15,000)

($40,000 – $55,000)

($30,000)

($25,000)

($55,000)

11. The financial statements of a partnership are similar to those of a proprietorship. The differences

are due to the number of partners involved. The income statement for a partnership is identical to

the income statement for a proprietorship except for the detailed information concerning the division

12. Liquidation of a partnership ends both the legal and economic life of the entity. Partnership

dissolution occurs whenever a partner withdraws or a new partner is admitted. Dissolution does not

necessarily mean that the business ends. If the continuing partners agree, operations can continue

without interruption by forming a new partnership.

13. No, Roger is not correct. All gains and losses on liquidation should be allocated to the partners

on the basis of their income ratio. However, final cash distributions should be based on their

capital balances.

15. Total cash after paying liabilities …………………………………………………………………… $103,000

Total capital balances ($34,000 + $31,000 + $28,000) …………………………………….. 93,000

Excess (gain on sale of noncash assets) ……………………………………………………….. $ 10,000

16. Capital deficiency, M. Luthi ………………………………………………………………………….. $ 4,000

Loss allocated to: L. Seastrom, capital ($4,000 X 3/8) …………………………………….. $ 1,500

17. A partnership is an association of two or more persons to carry on as co-owners of a business for

profit. Apple is a corporation since its has thousands of owners (called stockholders).

Questions Chapter 12 (Continued)

*18. This transaction represents the purchase of an existing partner’s interest. It is a personal trans–

action that has no effect on partnership net assets.

*20. Jamar, Capital …………………………..………………………………………………… 68,000

Parsons, Capital ……………………………………………………………………. 68,000

*22. Pester’s share of the $4,000 bonus is computed as follows:

Partnership assets ………………………………………………………………… $85,000

Capital credit, Riley ……………………………………………………………….. 81,000

Bonus to retiring partner …………………………………………………………. 4,000

*23. Recording the revaluations violates the cost principle, which requires that assets be stated at

original cost. It is also a departure from the going-concern assumption, which assumes the entity

will continue indefinitely.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 12-1

Cash …………………………………………………………………….. 10,000

Equipment…………………………………………………………….. 4,000

Fred Nichols, Capital ………………………………………. 14,000

BRIEF EXERCISE 12-2

BRIEF EXERCISE 12-3

The division is: Rod $45,000 ($75,000 X 60%) and Dall $30,000 ($75,000 X 40%).

The entry is:

BRIEF EXERCISE 12-4

Division of Net Income

Pitts

Filbert

Witten

Total

Salary allowance …………………..

Remaining income, $20,000:

($45,000 – $25,000)

$15,000

$ 5,000

$ 5,000

$25,000

BRIEF EXERCISE 12-5

Division of Net Income

Nabb

Fry

Total

Salary allowance …………………………………..

Interest allowance …………………………………

Remaining deficiency, ($6,000):

$15,000

7,000

$10,000

5,000

$25,000

12,000

BRIEF EXERCISE 12-6

A, Capital ………………………………………………………………… 8,000

*BRIEF EXERCISE 12-7

*BRIEF EXERCISE 12-8

Cash ………………………………………………………………………. 58,000

Irey, Capital (50% X $8,600*) …………………………………….. 4,300

*BRIEF EXERCISE 12-9

Fernetti, Capital ……………………………………………………….. 20,000

*BRIEF EXERCISE 12-10

Fernetti, Capital ……………………………………………………….. 20,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 12-1

1. True.

2. False. If a partnership is dissolved, each partner has a claim on total

assets equal to the balance in his or her capital account. The claim

DO IT! 12-2

The division of net income is as follows:

Miley

Guthrie

Total

Salary allowance …………………………………..

Remaining income ($75,000 – $43,000)

$25,000

$18,000

$43,000

DO IT! 12-2 (Continued)

DO IT! 12-3a

Item

Cash

+

Noncash

Assets

=

Liabilities

+

Cisneros

, Capital

+

Gunselman,

Capital

+

Forren,

Capital

Balance before

liquidation

15,000

90,000

40,000

20,000

32,000

13,000

(40,750)

Sale of noncash assets

DO IT! 12-3b

Oakley, Capital ($14,000 X 3/7) ………………………………….. 6,000

Ellis, Capital ($14,000 X 4/7) ………………………………………. 8,000

SOLUTIONS TO EXERCISES

EXERCISE 12-1

1. False. A partnership is an association of two or more persons to carry

on as co-owners of a business for profit.

2. False. Partnerships are fairly easy to form; they can be formed simply

EXERCISE 12-2

(a) Cash …………………………………………………………………. 50,000

Decker, Capital …………………………………………… 50,000

Land …………………………………………………………………. 15,000

Buildings ………………………………………………………….. 80,000

Rosen, Capital …………………………………………… 95,000

EXERCISE 12-3

Jan. 1 Cash …………………………………………………………. 12,000

Accounts Receivable …………………………………. 14,000

Equipment ………………………………………………….. 23,500

EXERCISE 12-4

(a)

(1)

DIVISION OF NET INCOME

McGill

Smyth

Total

Salary allowance ………………………….

Interest allowance

McGill ($50,000 X 10%) …………..

Smyth ($40,000 X 10%) …………..

$22,000

5,000

$13,000

4,000

$35,000

(2)

DIVISION OF NET INCOME

McGill

Smyth

Total

Salary allowance ………………………….

Interest allowance ………………………..

($22,000)

( 5,000)

($13,000

( 4,000

$35,000

9,000

(b) (1) Income Summary ………………………………………. 50,000

McGill, Capital ……………………………………… 30,600

EXERCISE 12-5

(a) Income Summary ……………………………………………… 80,000

Coburn, Capital ($80,000 X 45%) …………………. 36,000

Webb, Capital ($80,000 X 55%) ……………………. 44,000

(b) Income Summary ……………………………………………… 80,000

(c) Income Summary ………………………………………………. 80,000

Coburn, Capital ………………………………………….. 41,000

Webb, Capital …………………………..………………… 39,000

EXERCISE 12-6

(a) NATIONAL CO.

Partners’ Capital Statement

For the Year Ended December 31, 2017

N. Payne

A. Dody

Total

Capital, January 1 ………………..

Add: Net income …………………

$20,000

20,000

$18,000

20,000

$38,000

40,000

EXERCISE 12-6 (Continued)

(b) NATIONAL CO.

Partial Balance Sheet

December 31, 2017

Owners’ equity

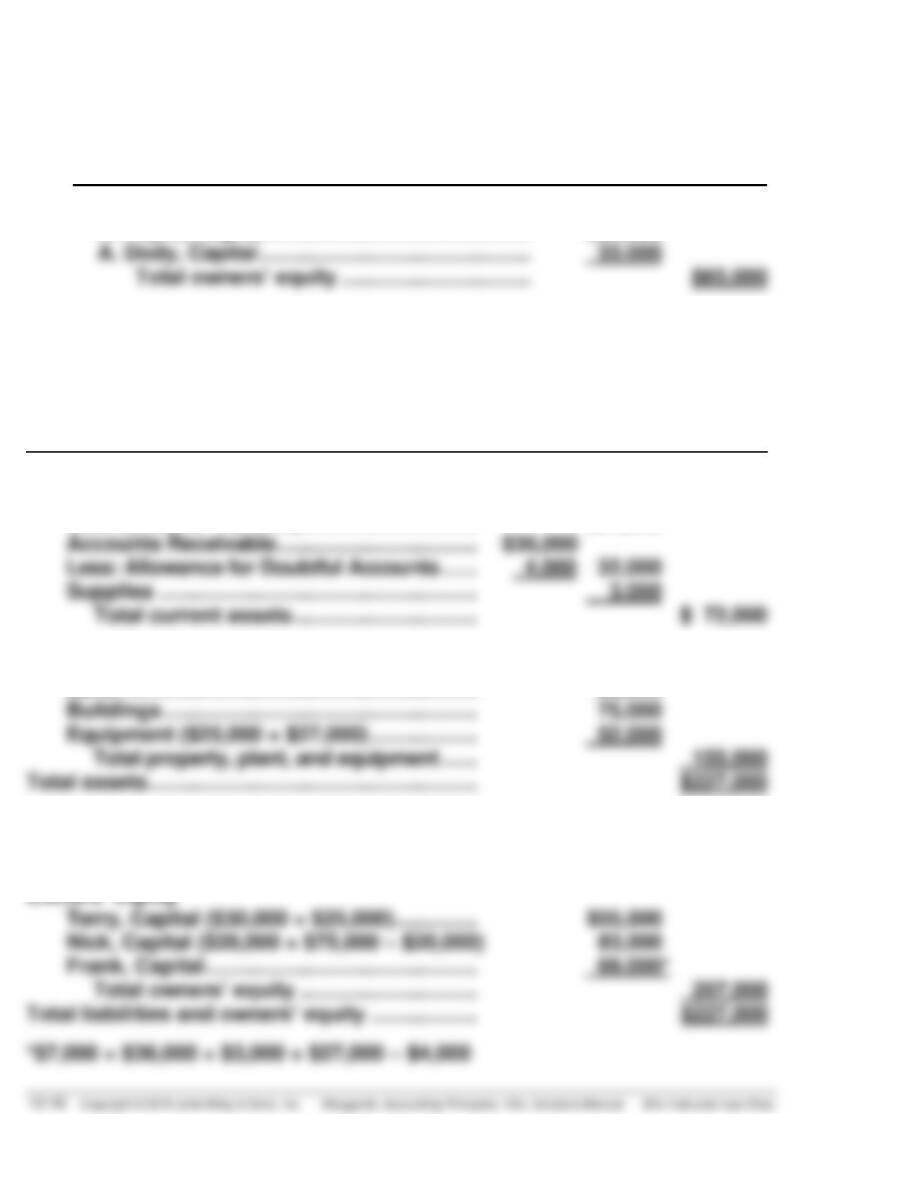

EXERCISE 12-7

THE DOCTOR PARTNERSHIP

Balance Sheet

December 31, 2017

Assets

Current Assets

Cash ($30,000 + $7,000) ………………………… $37,000

Accounts Receivable ……………………………. $36,000

Total current assets …………………………. $ 72,000

Property, Plant and Equipment

Land ……………………………………………………. 28,000

Buildings …………………………………………….. 75,000

Liabilities and Owners’ Equity

Long-term Liabilities

Mortgage Payable ………………………………… $ 20,000

Owners’ Equity

Terry, Capital ($30,000 + $25,000) ………….. $55,000

EXERCISE 12-8

SEDGWICK COMPANY

Schedule of Cash Payments

Item

Cash

+

Noncash

Assets

=

Liabilities

+

Floyd,

Capital

+

DeWitt,

Capital

Balances before

liquidation

Sale of noncash

assets and allo-

$ 20,000

($100,000)

($55,000)

$45,000

$20,000

EXERCISE 12-9

(a) Cash ………………………………………………………………. 105,000

Noncash Assets ………………………………………. 100,000

Gain on Realization ………………………………….. 5,000

(d) Floyd, Capital …………………………..…………………….. 48,000

DeWitt, Capital …………………………..…………………… 22,000

Cash ……………………………………………………….. 70,000

EXERCISE 12-10

(a) (1) Cash …………………………………………………………. 8,000

Pena, Capital ………………………………………. 8,000

(b) (1) Vogel, Capital ($8,000 X 5/8) ……………………….. 5,000

Utech, Capital ($8,000 X 3/8) ……………………….. 3,000

Pena, Capital ………………………………………. 8,000

*EXERCISE 12-11

(a) K. Kolmer, Capital ($34,000 X 50%) ……………………. 17,000

D. Jernigan, Capital ……………………………………. 17,000

*EXERCISE 12-12

(a) Cash ………………………………………………………………… 90,000

S. Pagon, Capital (6/10 X $15,000) ……………….. 9,000

T. Tabor, Capital (4/10 X $15,000) ………………… 6,000

W. Wolford, Capital ……………………………………. 75,000

*EXERCISE 12-12 (Continued)

Investment by new partner, Wolford …. $ 90,000

Wolford’s capital credit ……………………. 75,000

Bonus to old partners ……………………… $ 15,000

(b) Cash …………………………………………………………………. 50,000

S. Pagan, Capital (6/10 X $13,000) ………………………. 7,800

T. Tabor, Capital (4/10 X $13,000) ……………………….. 5,200

W. Wolford, Capital …………………………………….. 63,000

Investment by new partner, Wolford …. $ 50,000

Wolford’s capital credit ……………………. 63,000

Bonus to new partner ………………………. $ 13,000

*EXERCISE 12–13

1. C. Heganbart, Capital ………………………………………… 30,000

N. Essex, Capital ………………………………………… 15,000

C. Gilmore, Capital ……………………………………… 15,000