735

Problem 12-5A (50 minutes)

Part 1

a)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Feb. 1

Benson, Capital ………………………………………………..

138,000

Feb. 1

Benson, Capital ………………………………………………..

138,000

Feb. 1

Benson, Capital ………………………………………………..

138,000

Meir, Capital* ……………………………………………………

e)

Feb. 1

Benson, Capital ………………………………………………..

138,000

Accumulated Depreciation—Equipment ……………

736

Problem 12-5A (Concluded)

Part 2

a)

Feb. 1

Cash ………………………………………………………………..

200,000

b)

Feb. 1

Cash ………………………………………………………………..

145,000

c)

Feb. 1

Cash ………………………………………………………………..

262,000

737

Problem 12-6A (75 minutes)

Note: All entries in this problem are dated May 31.

1.

2.

738

Problem 12-6A (Concluded)

3.

(a)

Cash ………………………………………………………………..

320,000

217,200

108,600

Cash ………………………………………………………………..

(c)

245,500

140,100

130,800

4.

(a)

Cash ………………………………………………………………..

250,000

287,200

143,600

(c)

245,500

102,266

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 12

PROBLEM SET B

Problem 12-1B (30 minutes)

Cash ………………………………………………………………………………

200

Supplies …………………………………………………………………………

600

Equipment ……………………………………………………………………..

740

Problem 12-2B (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Bell = $104,000/$260,000 = 40%

Green = $156,000/$260,000 = 60%

Plan (b)

Percentages based on time

Bell = 0.333/1.333 = 25%

Green = 1.000/1.333 = 75%

Plan (c) & Plan (d)

Salary allowance

Green = 12 x $4,000 = $48,000

Plan (d)

Interest allowances

Bell = 10% x $104,000 = $10,400

Green = 10% x $156,000 = $15,600

Income (Loss)

Year 1

Sharing Plan

Calculations

Bell

Green

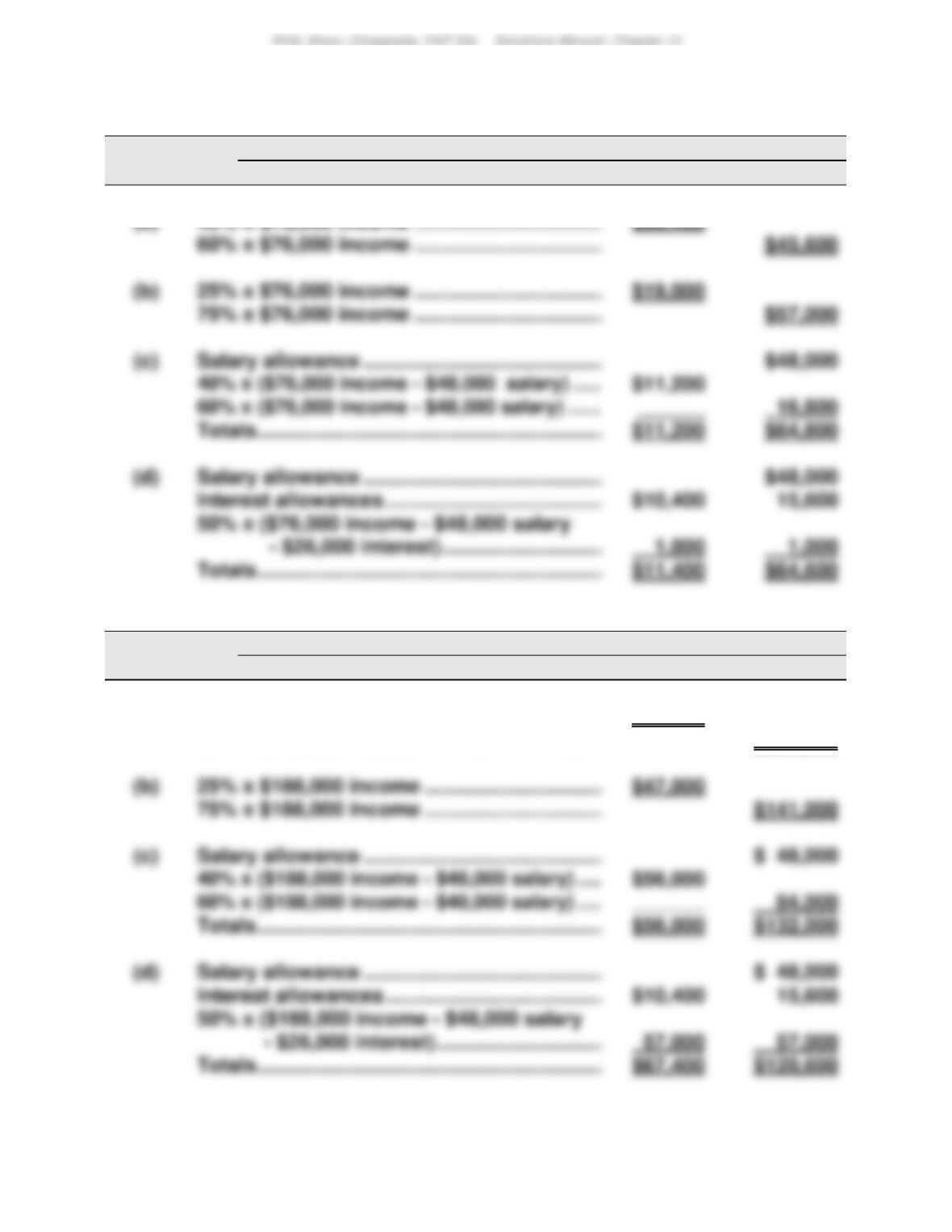

(a)

40% x $36,000 loss ……………………………………………

$(14,400)

60% x $36,000 loss ……………………………………………

25% x $36,000 loss ……………………………………………

75% x $36,000 loss ……………………………………………

(c)

Salary allowance ………………………………………………

40% x ($36,000 loss + $48,000 salary) ………………..

60% x ($36,000 loss + $48,000 salary) ………………..

Totals ……………………………………………………….

Salary allowance ………………………………………………

Totals ……………………………………………………….

741

Problem 12-2B (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Bell

Green

(a)

40% x $76,000 income ………………………………………

$30,400

60% x $76,000 income ………………………………………

25% x $76,000 income ………………………………………

$19,000

75% x $76,000 income ………………………………………

(c)

Salary allowance ………………………………………………

$11,200

Totals ……………………………………………………….

$11,200

Salary allowance ………………………………………………

$10,400

Income (Loss)

Year 3

Sharing Plan

Calculations

Bell

Green

(a)

40% x $188,000 income …………………………..

$75,200

60% x $188,000 income …………………………..

$112,800

25% x $188,000 income …………………………..

$47,000

75% x $188,000 income …………………………..

$141,000

(c)

Salary allowance ………………………………………………

$ 48,000

$56,000

Totals ……………………………………………………….

$56,000

$132,000

Salary allowance ………………………………………………

$10,400

742

Problem 12-3B (50 minutes)

1.

Dec. 31

Income Summary ……………………………………………..

270,000

Andy Albin, Capital ……………………………………..

Paris Peters, Capital ……………………………………

Ram Ramsey, Capital ………………………………….

2.

Dec. 31

Income Summary ……………………………………………..

270,000

Andy Albin, Capital ……………………………………..

135,000

Paris Peters, Capital ……………………………………

Ram Ramsey, Capital ………………………………….

($164,000/$328,000) x $270,000 = $135,000

($98,400/$328,000) x $270,000 = $81,000

3.

Dec. 31

Income Summary ……………………………………………..

270,000

Andy Albin, Capital ……………………………………..

118,800

Paris Peters, Capital ……………………………………

Ram Ramsey, Capital ………………………………….

62,960

*Supporting calculations

Albin

Peters

Ramsey

Total

Net income …………………………………………

$270,000

Salary allowances

Peters ……………………………………………..

$72,000

Total salaries ……………………………………..

Interest allowances

Albin (10% on $164,000) ……………………

Ramsey (10% on $65,600) …………………

6,560

Bal. after interest and salaries ……………..

Balance allocated equally ……………………

6,400

Balance of income …………………………..

$ 0

743

Problem 12-4B (30 minutes)

Part 1

Income (Loss)

Sharing Plan

Calculations

Cook

Jing

Schwartz

Total

$240,000/3 ……………………………………………

$ 80,000

Total allocated …………………………..

(c)

Net income …………………………………………..

$240,000

Salary allowances …………………………..

$ 30,000

(150,000)

Balance of income…………………………..

Interest allowances

Total interest …………………………..

Balance of income…………………………..

Balance allocated equally……………………..

Balance of income…………………………..

$ 0

744

Problem 12-4B (Concluded)

Part 2

CJS PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Cook

Jing

Schwartz

Total

Beginning capital balances ……………..

$ 0

$ 0

$ 0

$ 0

Plus

Investments by owners …………………..

Net income

Part 3

Dec. 31

Income Summary ……………………………………………..

87,600

Cook, Capital ……………………………………………………

18,000

38,000

Schwartz, Capital ……………………………………………..

24,000

745

Problem 12-5B (50 minutes)

Part 1

a)

Apr. 30

Gibbs, Capital …………………………………………………..

606,000

Brady, Capital ……………………………………………..

b)

Apr. 30

Gibbs, Capital …………………………………………………..

606,000

Kannon, Capital……………………………………………

c)

Apr. 30

Gibbs, Capital …………………………………………………..

606,000

Cash …………………………………………………………..

d)

Apr. 30

Gibbs, Capital …………………………………………………..

606,000

Hook, Capital* …………………………..…………………….

Chan, Capital** ……………………………………………

Cash …………………………………………………………..

e)

Apr. 30

Gibbs, Capital …………………………………………………..

606,000

Accum. Deprec.—Manufacturing Equipment ……..

336,000

Hook, Capital*……………………………………………..

Chan, Capital** ……………………………………………

Manufacturing Equipment …………………………..

Cash …………………………………………………………..

746

Problem 12-5B (Concluded)

Part 2

a)

Apr. 30

Cash ………………………………………………………………..

300,000

b)

Apr. 30

Cash ………………………………………………………………..

196,000

Hook, Capital ($83,200* x 1/10) …………………………..

Chan, Capital ($83,200* x 4/10) …………………………..

c)

Apr. 30

Cash ………………………………………………………………..

426,000