Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-1

CHAPTER 12

REPORTING AND ANALYZING PARTNERSHIPS

Related Assignment Materials

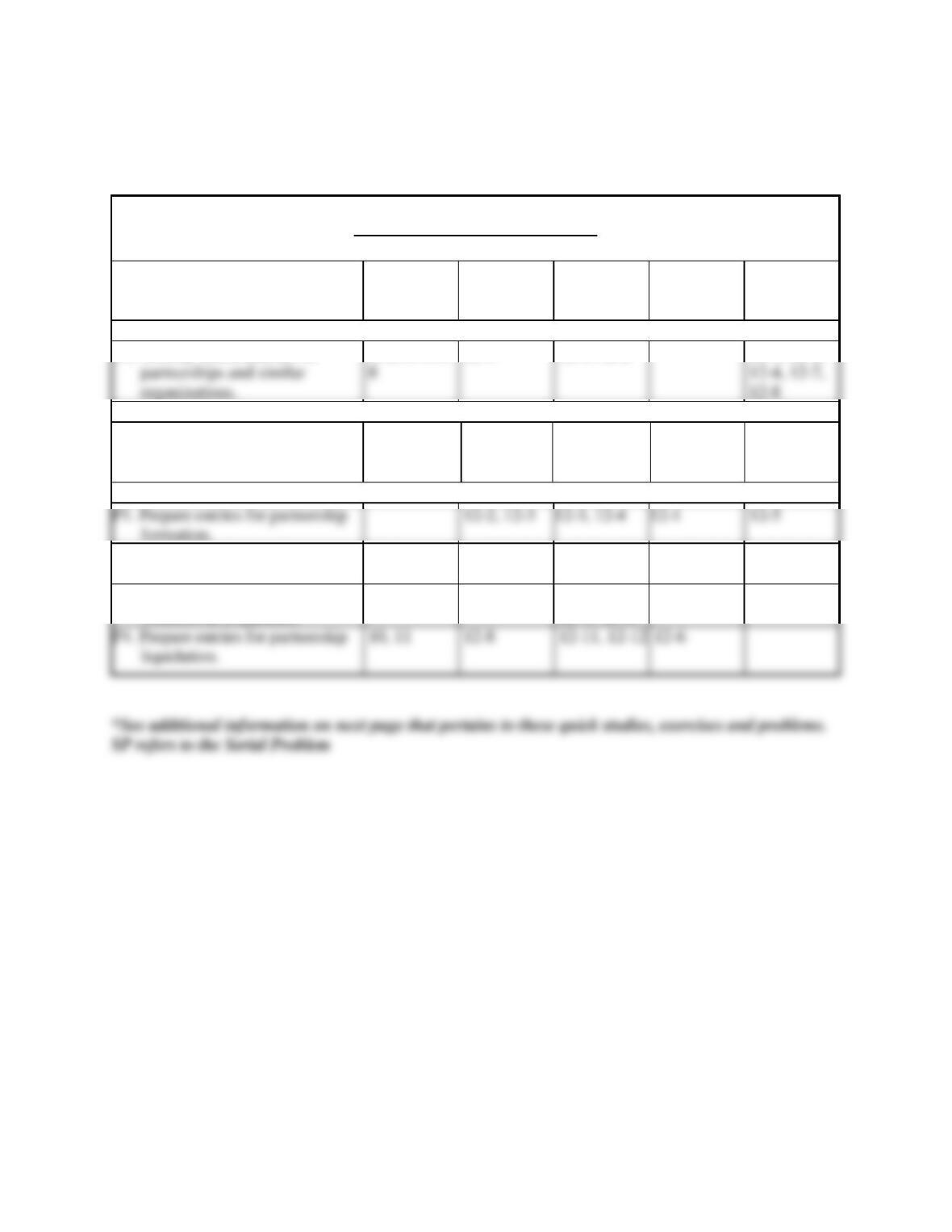

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Identify characteristics of

1, 2, 3, 4, 5,

12-1

12-1, 12-2

12-1, 12-2,

Analytical objectives:

Al. Compute partner return on

equity and use it to evaluate

partnership performance.

12-9

12-13

Procedural objectives:

P2. Allocate and record income and

loss among partners.

6, 7

12-4, 12-5

12-5, 12-6,

12-7

12-2, 12-3,

12-4

12-3, 12-5,

12-6

P3. Account for the admission and

withdrawal of partners.

9, 12

12-6, 12-7

12-7, 12-8,

12-9, 12-10

12-5, SP

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and

Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows

instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

The Serial Problem for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revision

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-3

Chapter Outline

Notes

I. Partnership Formation—An unincorporated association of two or

more people to pursue a business for profit as co-owners.

A. Characteristics of Partnerships

1. Voluntary association.

3. Limited life—death, bankruptcy, or expiration of the contract

period automatically ends a partnership.

5. Mutual agency—each partner is an agent of the partnership

6. Unlimited liability—each general partner is responsible for

7. General partnership—all partners have mutual agency and

unlimited liability

8. Co-ownership of property—assets are owned jointly by all

partners but claims on partnership assets are based on their

capital account and the partnership contract.

B. Organizations with Partnership Characteristics

1. Limited Partnership (LP or Ltd.) has two classes of partners,

general (at least one) and limited. The general partners assume

2. Limited Liability Partnership (LLP) is designed to protect

3. S Corporation has 100 or fewer stockholders, is treated as a

4. Limited Liability Company (LLC or LC) owners are called

members, are protected with the limited liability feature of

corporations and can assume an active management role. The

LLC typically is classified as a partnership for tax purposes.

B. Choosing a Business Form

Factors to be considered include: taxes, liability risk, tax and fiscal

year-end, ownership structure, estate planning, business risks, and

earnings and property distributions.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-4

Chapter Outline

Notes

II. Accounting for Partnership Formation—Same as accounting for a

proprietorship except for transactions directly affecting partners’

equity. Use separate capital and withdrawal accounts for each partner.

Allocates net income or loss to partners according to the partnership

agreement.

A. Organizing a Partnership

B. Dividing Partnership Income and Loss

1. Any agreed upon method of dividing income or loss is

2. Common methods of dividing partnership earnings use:

a. Stated ratio.

b. Allocation on capital balances.

c. Allocation on service, capital, and stated ratio—salary and

interest allowances, and a fixed ratio are specified—when

4. Partners may agree to salary and interest allowances to reward

unequal contributions of services or capital.

C. Partnership Financial Statements

Similar to a proprietorship except:

1. The statement of partners' equity usually shows changes for

2. The balance sheet generally lists a separate capital account for

each partner.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-5

Chapter Outline

Notes

III. Admission of a Partner

A. Admission of a Partner—two means:

1. Purchase of partnership interest.

a. The purchase is a personal transaction between one or

2. Investing assets in a partnership.

a. The transaction is between the new partner and the

partnership. Invested assets become partnership property.

income and loss sharing agreement.

B. Withdrawal of a Partner—two means:

2. Cash or other assets of the partnership can be distributed to the

withdrawing partner in settlement of his or her interest.

a. Withdrawing partner may accept assets equal to, less than,

or greater than his/her equity.

C. Death of a Partner

1. Dissolves a partnership.

2. Deceased partner's estate is entitled to receive his or her

3. Settlement of the deceased partner's equity can involve selling

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-6

Chapter Outline

Notes

IV. Liquidation of a Partnership

A. Involves four basic steps:

2. Gain or loss on liquidation is allocated to partners using their

income-and-loss ratio.

4. Distribute any remaining cash to partners according to their

capital account balances.

B. Allocating gains or losses on liquidation may result in:

1. No capital deficiencies—all partners’ have a zero or credit

2. Capital deficiencies—when at least one partner has a debit

balance in his/her capital account.

a. Partners with a capital deficiency must, if possible, cover

the deficit by paying cash into the partnership.

b. When a partner is cannot pay the deficiency, the

V. Decision Analysis—Partner Return on Equity

A. Evaluates partnership success compared with other opportunities.

B. Computed separately for each partner.

C. Computed by dividing partner’s share of net income by that

partner’s average partner equity.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-7

Chapter 12 Alternate Demonstration Problem

Sand, Mell, and Rand are partners who share incomes and losses in a 1:4:5

ratio. After lengthy disagreements among the partners and several

unprofitable periods, the partners decided to liquidate the partnership.

Before the liquidation, the partnership balance sheet showed Cash $10,000,

total “other assets”, $106,000; total liabilities, $88,000; Sand, Capital,

$1,200; Mell, Capital, $11,700; and Rand, Capital, $15,100. The “other

assets” were sold for $ 85,000.

Determine the following:

1. The gain (or loss) realized on the sale of the assets.

3. Assume that if any capital deficits exist, they are not made-up. How

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

12-8

Chapter 12 Alternate Demonstration Problem: Solution

1.

Proceeds from sale

$85,000

2.

Sands

Mell

Rand

Capital account balance prior to

distribution of loss on sale of

$1,200

$11,700

$15,100

3.

Sands

Mell

Rand

Capital account balance after

distribution of loss on sale of