1. (1) To pay the face (maturity) amount of the bonds at a specified date. (2) To pay periodic

interest at a specified percentage of the face amount.

2. a. Bonds that may be exchanged for other securities under specified conditions.

b. The issuing corporation reserves the right to redeem the bonds before the maturity date.

3. More than face amount. Because comparable bonds provide a market interest rate (11%) that

4. a. Greater than $26,000,000

b. 1. $26,000,000

3. 9%

5. More than the contract rate

6. a. Premiu

m

8. A mortgage note is an installment note that is secured by a pledge of the borrower’s assets.

9. A bond is an interest-bearing note that requires periodic interest payments and repayment of

the face amount of the bonds at maturity. Bonds consist of two different components:

(1) interest payments made periodically over the life of the bond and (2) the face amount that

must be repaid at maturity. The periodic payments consist entirely of interest, and the final

CHAPTER 12

LONG-TERM LIABILITIES: BONDS AND NOTES

DISCUSSION QUESTIONS

12-1

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

PE 12–1A

Earnings before bond interest and income tax………

…

$750,000 $750,000

Deduct interest on bonds…………………………………

…

350,000 238,000

Income before income tax………………………………… $400,000 $512,000

Deduct income tax…………………………………………

…

160,000 204,800

PE 12–1B

Earnings before bond interest and income tax………

…

$2,000,000 $2,000,000

Deduct interest on bonds…………………………………

…

400,000 250,000

Income before income tax………………………………… $1,600,000 $1,750,000

…

…

…

…

640,000 700,000

Plan 1 Plan 2

PRACTICE EXERCISES

Plan 1 Plan 2

1

2

3

4

1

2

3

4

12-2

…

…

…

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

PE 12–2A

a.

Cash 500,000

PE 12–2B

a.

Cash 800,000

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

PE 12–3A

PE 12–3B

Cash 2,889,599

PE 12–4A

Interest Expense 58,633

PE 12–4B

Interest Expense 176,040

PE 12–5A

Cash 2,170,604

PE 12–5B

Cash 8,308,869

12-4

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

PE 12–6A

Interest Expense 62,940

PE 12–6B

Interest Expense 409,113

*

PE 12–7A

Bonds Payable 1,500,000

PE 12–7B

Bonds Payable 500,000

PE 12–8A

a. Cash 65,000

Notes Payable 65,000

Issued installment notes for cash.

PE 12–8B

a. Cash 45,000

Notes Payable 45,000

Issued installment notes for cash.

b. Interest Expense 3,600

PE 12–9A

a. Number of times interest charges earned:

$3,200,000 + $320,000

$320,000

b. The number of times interest charges are earned has decreased from 13.0 in 2015

PE 12–9B

a. Number of times interest charges earned:

$5,544,000 + $440,000

$440,000

b. The number of times interest charges are earned has increased from 12.0 in 2015 to

2016: = 13.6

2016: = 11.0

12-6

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

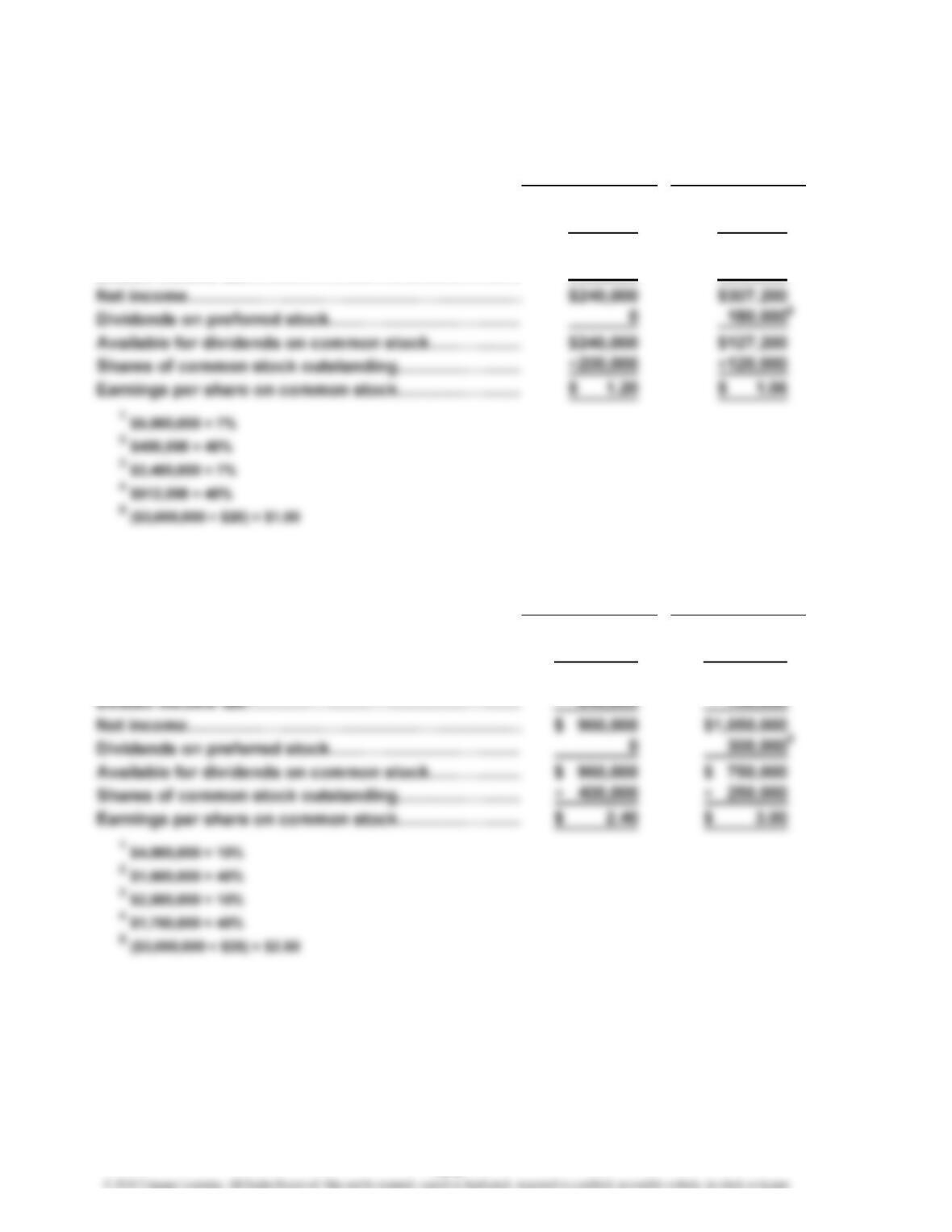

Ex. 12–1

Domanico

Co.

Shares of common stock outstanding…………………………………

…

÷ 500,000

Earnings per share on common stock…………………………………

…

$ 1.64

b. Earnings before bond interest and income tax………………………

…

$11,800,000

…

Earnings per share on common stock…………………………………

…

$ 3.20

c. Earnings before bond interest and income tax………………………

…

$13,000,000

…

Earnings per share on common stock…………………………………

…

$ 4.64

*

EXERCISES

$10,000,000 bonds payable × 8% interest

***

12-7

…

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–3

Nike’s major source of financing is common stock. It has relatively little long-term debt

compared to stockholders’ equity.

Ex. 12–4

Ex. 12–5

1 Cash 600,000

Bonds Payable 600,000

Ex. 12–6

a. 1. Cash 17,138,298

2. Interest Expense 1,061,170

3. Interest Expense 1,061,170

May

12-8

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–6 (Concluded)

b. Annual interest paid……………………………………………………………

…

$1,850,000

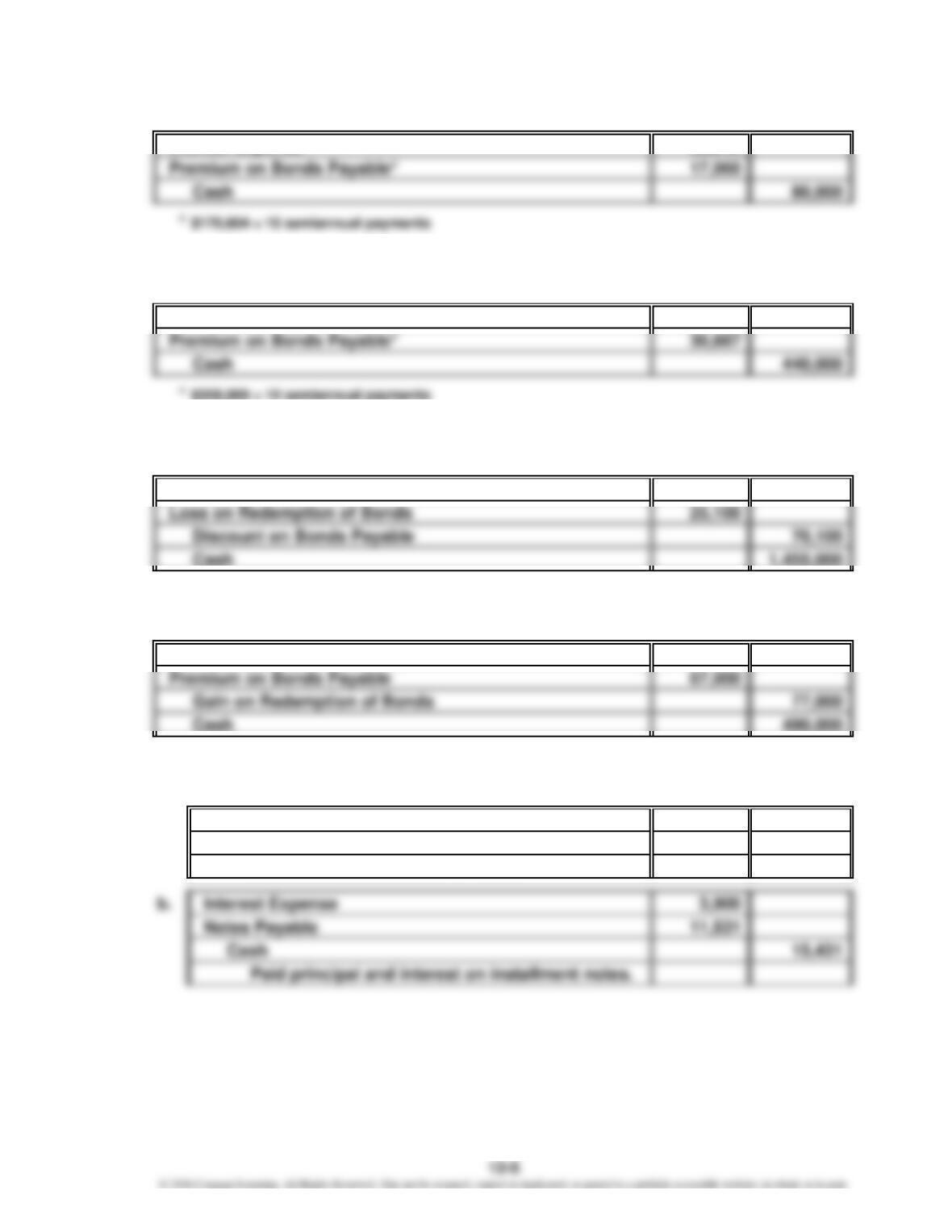

Ex. 12–7

a. Cash 13,023,576

Premium on Bonds Payable 1,023,576

Bonds Payable 12,000,000

*$1,023,576 ÷ 10 semiannual payments

Ex. 12–8

1 Cash 22,000,000

Bonds Payable 22,000,000

2016

Mar.

12-9

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–9

1 Cash 15,000,000

Bonds Payable 15,000,000

Ex. 12–10

a. 1. Cash 85,000

Notes Payable 85,000

2016

May

12-10

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–10 (Concluded)

Current liabilities:

Notes payable*………………………………………………………………………

…

$10,510

* The principal repayment portion of the next installment payment. See computation below.

Noncurrent liabilities:

Notes payable**……………………………………………………………………… $64,668

** Original note payable………………………………………………………………

…

$85,000

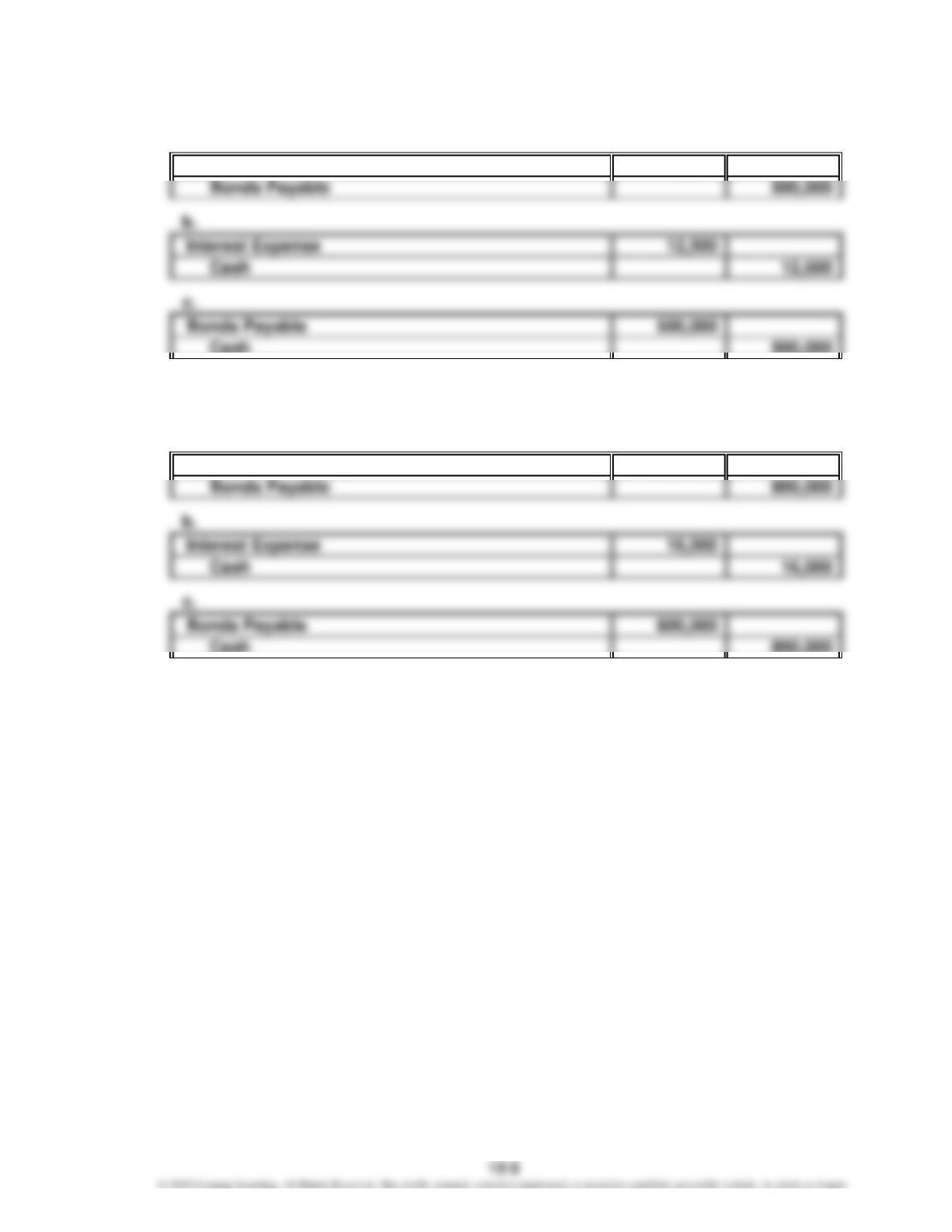

Ex. 12–11

1 Cash 175,000

Notes Payable 175,000

Jan.

2016

12-11

…

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

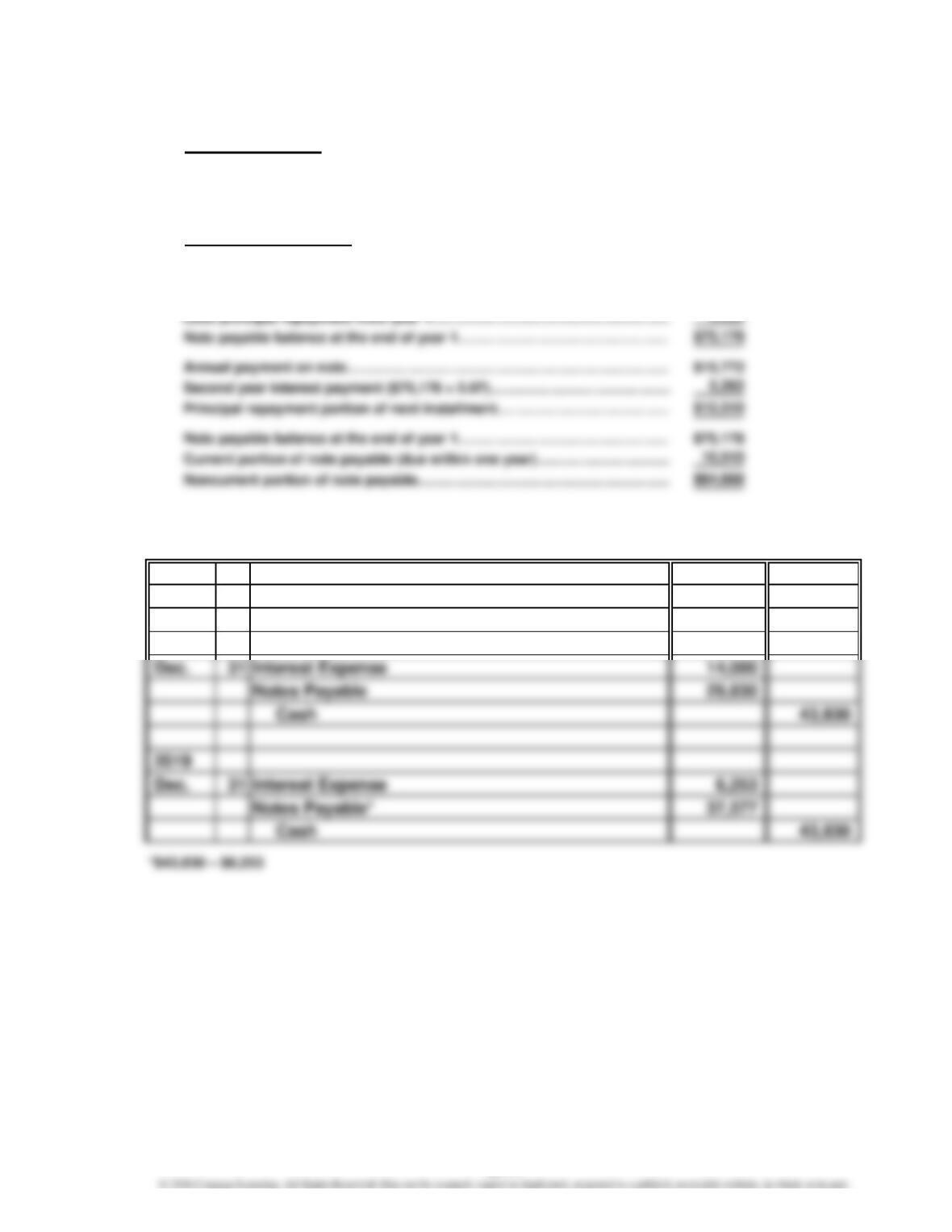

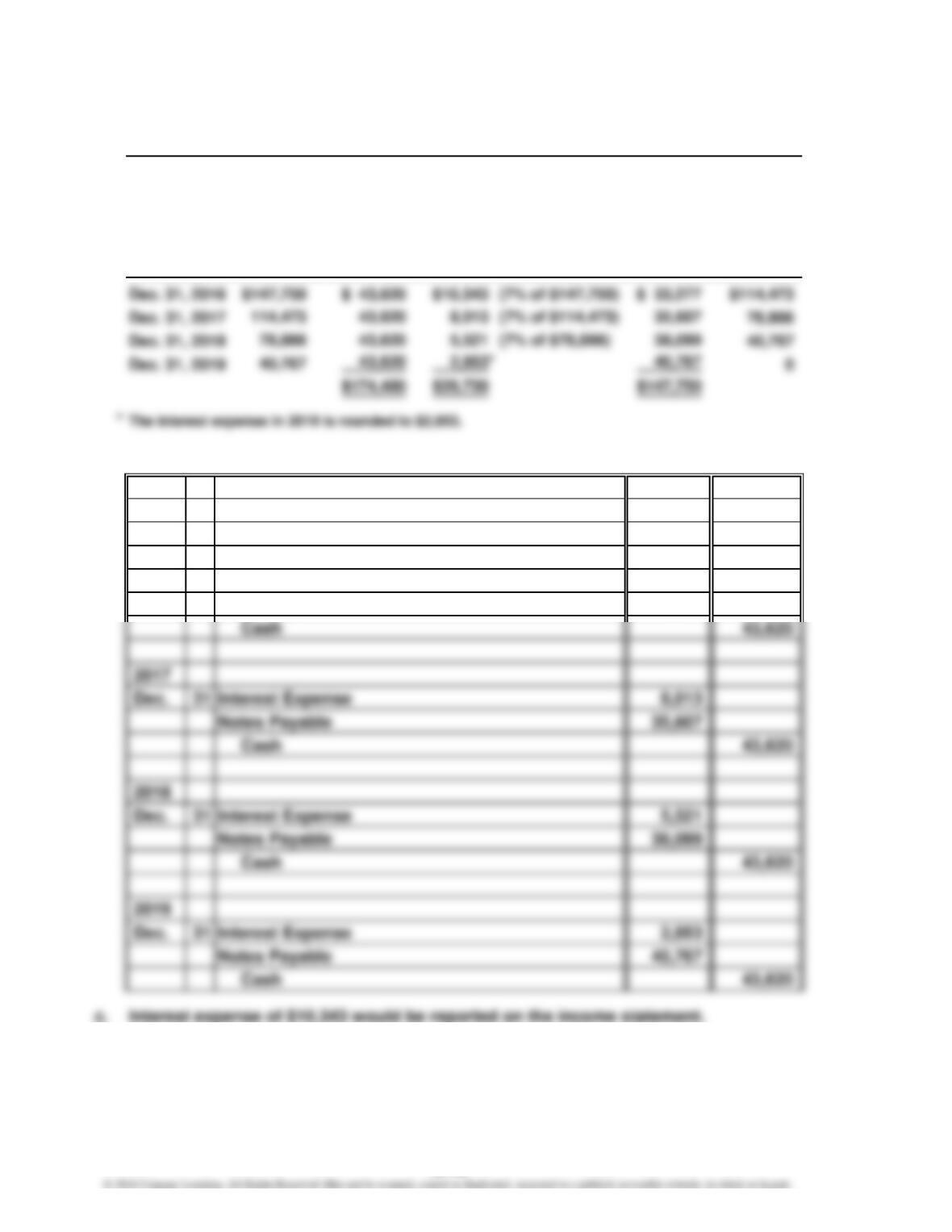

Ex. 12–12

a.

AB DE

Decrease Dec. 31

January 1 Note in Notes Carrying

Carrying Payment Payable Amount

Amount (Cash Paid) (B – C) (A – D)

b. 2016

Jan. 1 Cash 147,750

Notes Payable 147,750

Dec. 31 Interest Expense 10,343

Notes Payable 33,277

Interest Expense

Ending Note Carrying Amount)

(7% of January 1

Amortization of Installment Notes

For the

Year

C

12-12

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–13

1. The significant loss on redemption of the Simmons Industries bonds should be

2. The Hunter Corporation bonds outstanding at the end of the current year

should be reported as a current liability on the balance sheet because they

mature within one year.

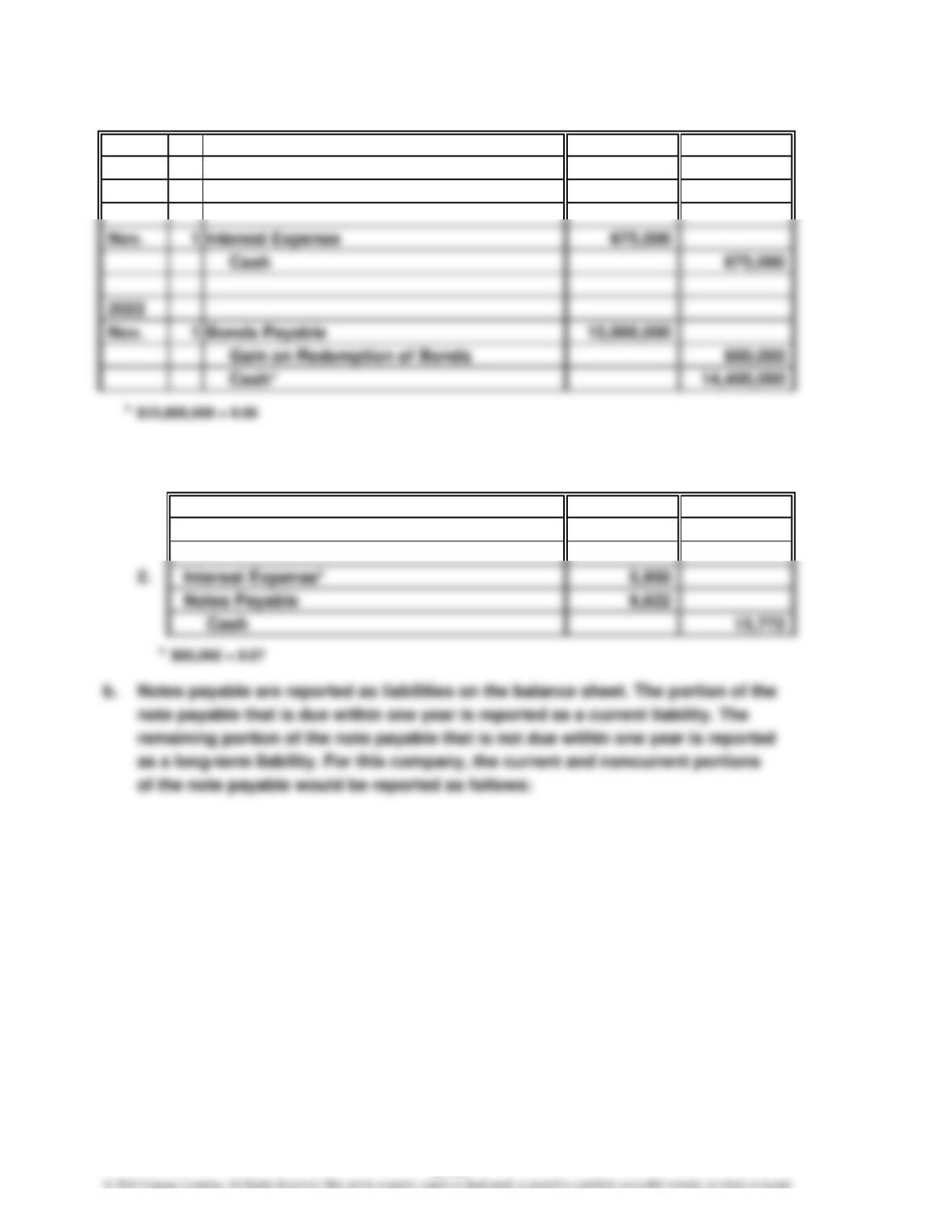

Ex. 12–14

a. Number of times interest charges earned:

$685,000,000 + $147,000,000

$147,000,000

Ex. 12–15

a. Number of times interest charges earned:

$310,500,000 + $13,500,000

$13,500,000

2016: = 24.0

Current year: = 5.7

12-13

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–16

a. Number of times interest charges earned:

b. The number of times interest charges are earned has decreased from 2.2 in 2015

Ex. 12–17

$1,000,000 × 0.75131 = $751,310

Cash on hand today can be invested to earn income. If $751,315 is invested at 10%, it wil

l

be worth $1,000,000 at the end of three years.

Ex. 12–18

a. First Year: $200,000 × 0.93458 =

Second Year: $200,000 × 0.87344 =

$186,916

174,688

2016: = 1.7

$3,500,000 + $5,000,000

$5,000,000

12-14

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–20

No. The present value of your winnings using an interest rate of 12% is $31,047,750

($6,250,000 × 4.96764), which is less than the present value of your winnings using

an interest rate of 5% ($40,395,063; see Ex. 12–19). This is because the winnings are

affected by the higher interest rate.

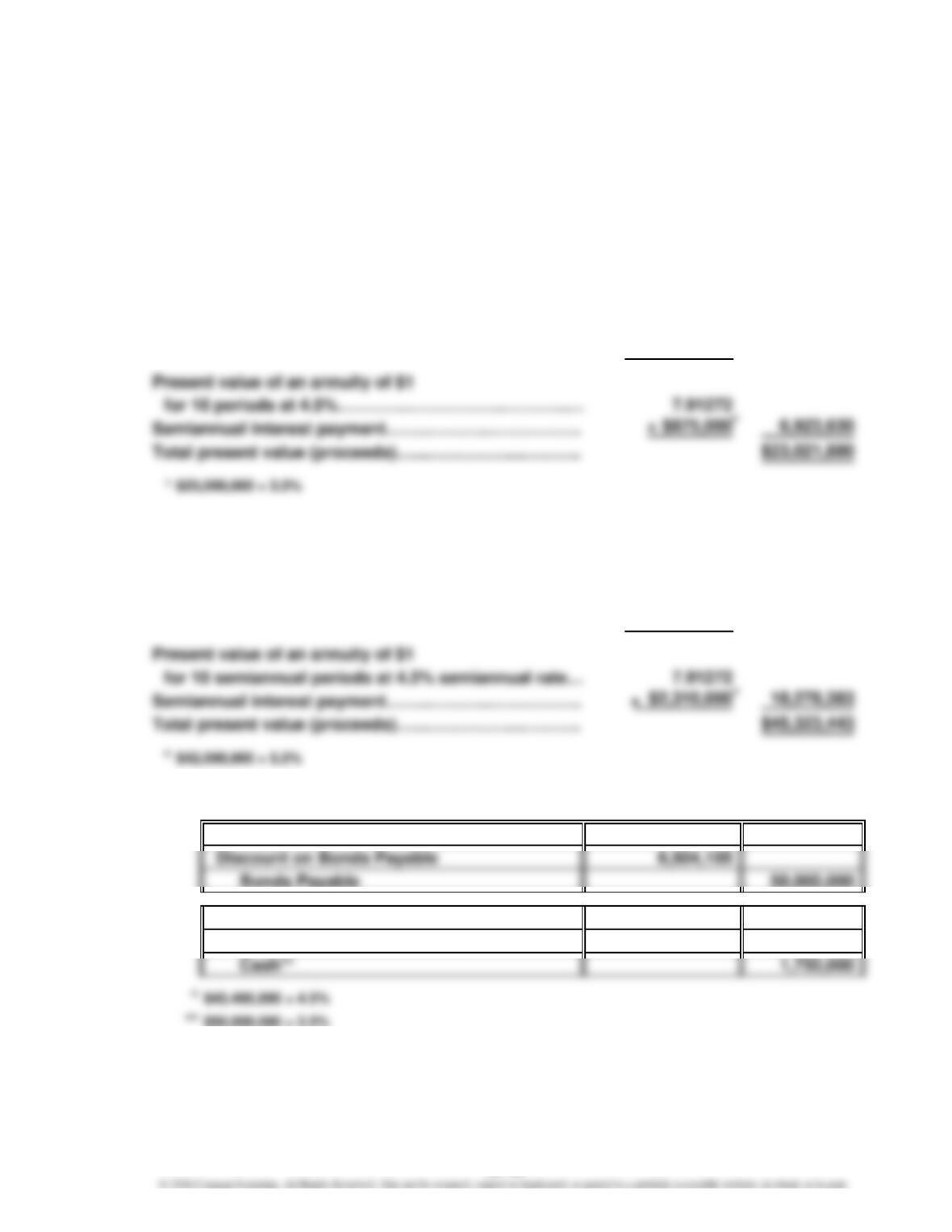

Ex. 12–21

Present value of $1 for 10 semiannual

periods at 4.5% semiannual rate………………………

…

0.64393

Face amount of bonds……………………………………… $25,000,000 $16,098,250

Ex. 12–22

Present value of $1 for 10 semiannual

periods at 4.5% semiannual rate………………………

…

0.64393

Face amount of bonds……………………………………… $42,000,000 $27,045,060

Ex. 12–23

a. 1. Cash

2. Interest Expense*

Discount on Bonds Payable

207,315

43,495,895

1,957,315

×

×

12-15

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–23 (Concluded)

3. Interest Expense* 1,966,644

Discount on Bonds Payable

Cash

*

($43,495,895 + $207,315) × 4.5%

Note: The following data in support of the proceeds of the bond issue stated in

the exercise are presented for the instructor’s information. Students are not

required to make the computations.

b. Annual interest paid…………………………………………………………

…

$ 3,500,000

Plus discount amortized*…………………………………………………… 423,959

c. The bonds sell for less than their face amount because the market rate of interest is

greater than the contract rate of interest. Investors are not willing to pay the full face

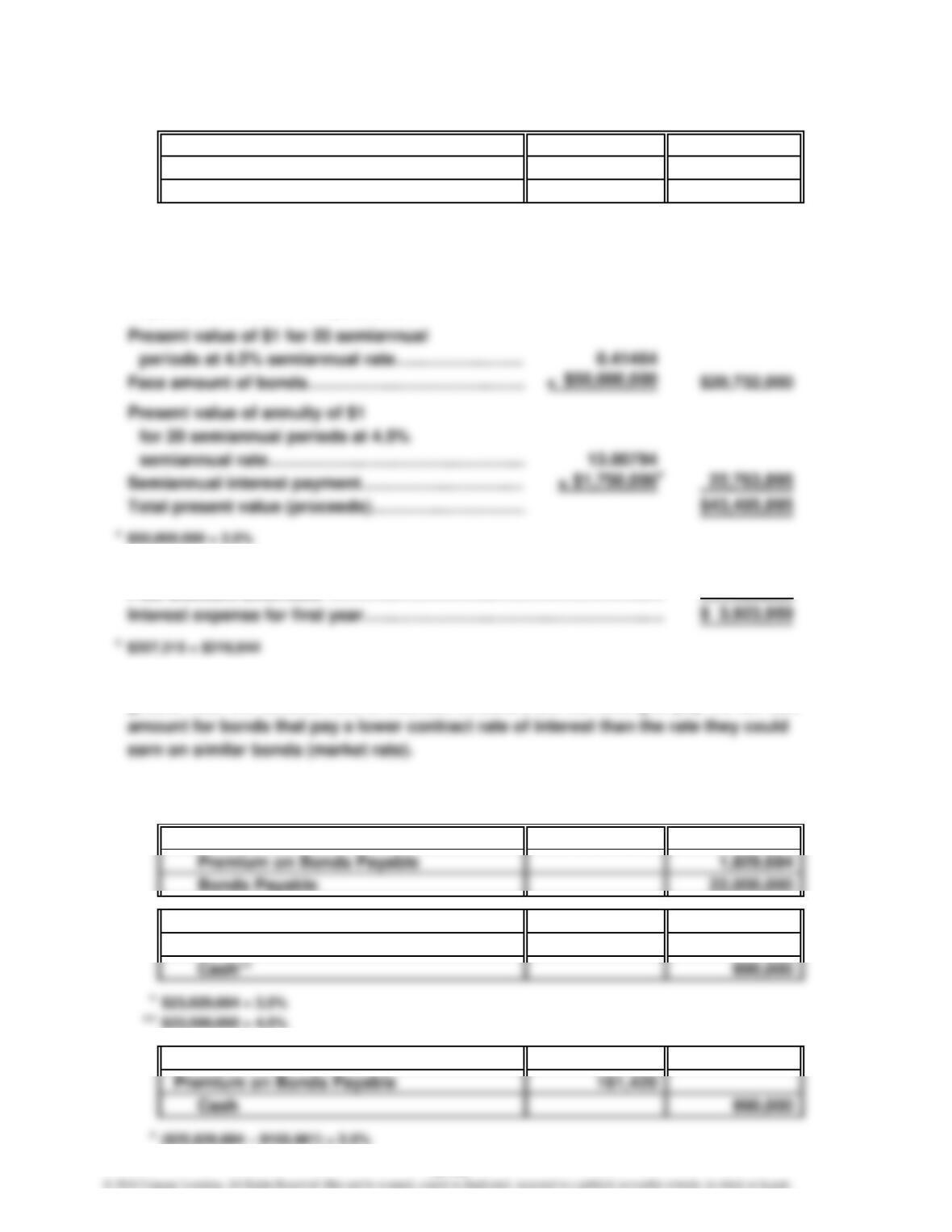

Ex. 12–24

a. 1. Cash 23,829,684

2. Interest Expense* 834,039

Premium on Bonds Payable 155,961

3. Interest Expense* 828,580

216,644

1,750,000

12-16

CHAPTER 12 Long-Term Liabilities: Bonds and Notes

Ex. 12–24 (Concluded)

b. Annual interest paid……………………………………………………………

…

$1,980,000

Less premium amortized*……………………………………………………

…

317,381

Ex. 12–25

a. Present value of $1 for 10 semiannual

periods at 5% semiannual rate……………………… 0.61391

Face amount of bonds…………………………………

…

$35,000,000 $21,486,850

Present value of an annuity of $1 for 10

semiannual periods at 5% semiannual rate………

…

7.72173

…

…

…

*

$37,702,483 – $214,876

d. Annual interest paid……………………………………………………………

…

$ 4,200,000

Less premium amortized*……………………………………………………

…

440,496

Interest expense for first year………………………………………………… $ 3,759,504

×

12-17