338 Chapter 11

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Proof:

Year

Beginning

Book Value

Rate

Depreciation

Expense

Ending Book

Value

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Patent

Amortization Expense

Other

Contributed

Retained

B. Straight-line depreciation expense (year 1)

= $26,000 [($152,000 − $22,000) ÷ 5]

Accumulated Depreciation

Depreciation Expense

Investing Activities 339

P11-17 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

B.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

C.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

D. Mechanically, goodwill is the amount paid over and above the market

obtain the extra profits.

E.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Cash

Accumulated Depreciation

Depreciation Expense

P11-18 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

July 1, 2004

Cash

–800,000

Equipment

800,000

Depreciation Expense

–75,000

–150,000

Depreciation Expense

–150,000

Depreciation Expense

Depreciation Expense

–75,000

June 30, 2007

Cash

311,000

Equipment

–800,000

Accumulated

Depreciation

450,000

Loss on Asset Sale

–39,000

C. Effect on pretax income for 2004–2007:

Total depreciation expense ($75,000 + $150,000

Investing Activities 341

Accrual and cash flow measurements usually produce the same results

when all effects of a series of related transactions are considered. The life

of a plant asset is a good example of these relationships. Cash flow and

P11-19 Asset valuation by financial institutions has been a major accounting is-

sue in recent years. Traditional accounting rules permitted banks to re-

port loans and other assets at historical cost. Nonperforming loans were

On the other hand, if the bank’s valuation of $43 million is a fair repre-

sentation of the present value of the expected cash flows the bank ex-

pects to receive from the loans, the amount may not be misleading. A rel-

evant issue is whether the loan loss reserve is sufficient to cover the

losses the bank should expect from nonperforming loans. If the bank

342 Chapter 11

P11-20 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Jan. 1

Cash

–24,000

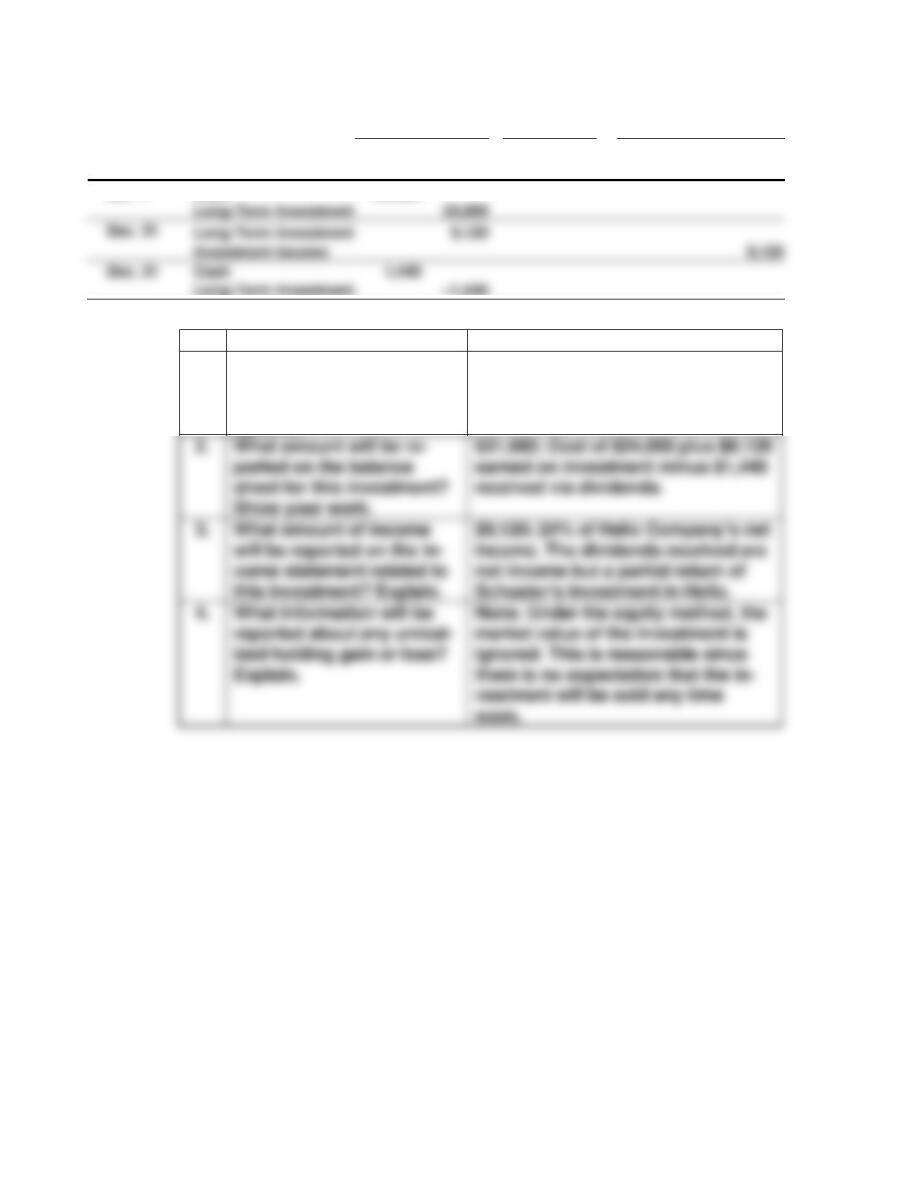

B.

Question

Solution

1.

In which section of the bal-

ance sheet will this in-

vestment be reported? Be

specific.

Long-term investment section.

2.

What amount will be re-

ported on the balance

sheet for this investment?

Show your work.

$31,680; Cost of $24,000 plus $9,120

earned on investment minus $1,440

received via dividends.

3.

What amount of income

come statement related to

not income but a partial return of

ized holding gain or loss?

Explain.

ignored. This is reasonable since

there is no expectation that the in-

vestment will be sold any time

soon.

Investment Income

Dec. 31

Cash

Investing Activities 343

P11-21

The Book Wermz

Depreciation Schedule

April–December 2008

Asset Buildings Store Equipment Transportation Equipment Total

Cost 2,200,000.00 1,000,000.00 275,000.00

Salvage 100,000.00 50,000.00 75,000.00

Life (months) 360 60 36

Method Straight-Line Declining-Balance Straight-Line Declining-Balance Straight-Line Units-of-Production Straight-Line Accelerated

Month Miles Expense

1 $ 5,833.33 $ 12,222.22 $ 15,833.33 $ 33,333.33 $ 5,555.56 1,500 $ 3,333.33 $ 27,222.22 $ 48,888.88

2 5,833.33 12,154.32 15,833.33 32,222.22 5,555.56 1,800 4,000.00 27,222.22 48,376.54

Total Accelerated $417,436.50

344 Chapter 11

If the life of the buildings was 380 months and the life of the equipment was 72 months:

Asset Buildings Store Equipment Transportation Equipment Total

Method Straight-Line Declining-Balance Straight-Line Declining-Balance Straight-Line Units-of-Production Straight-Line Accelerated

Month Miles Expense

1 $ 5,526.32 $ 11,578.95 $ 13,194.44 $ 27,777.78 $ 5,555.56 1,500 $ 3,333.33 $ 24,276.32 $ 42,690.06

Total Accelerated $372,881.91

Total Straight-line 218,486.88

Investing Activities 345

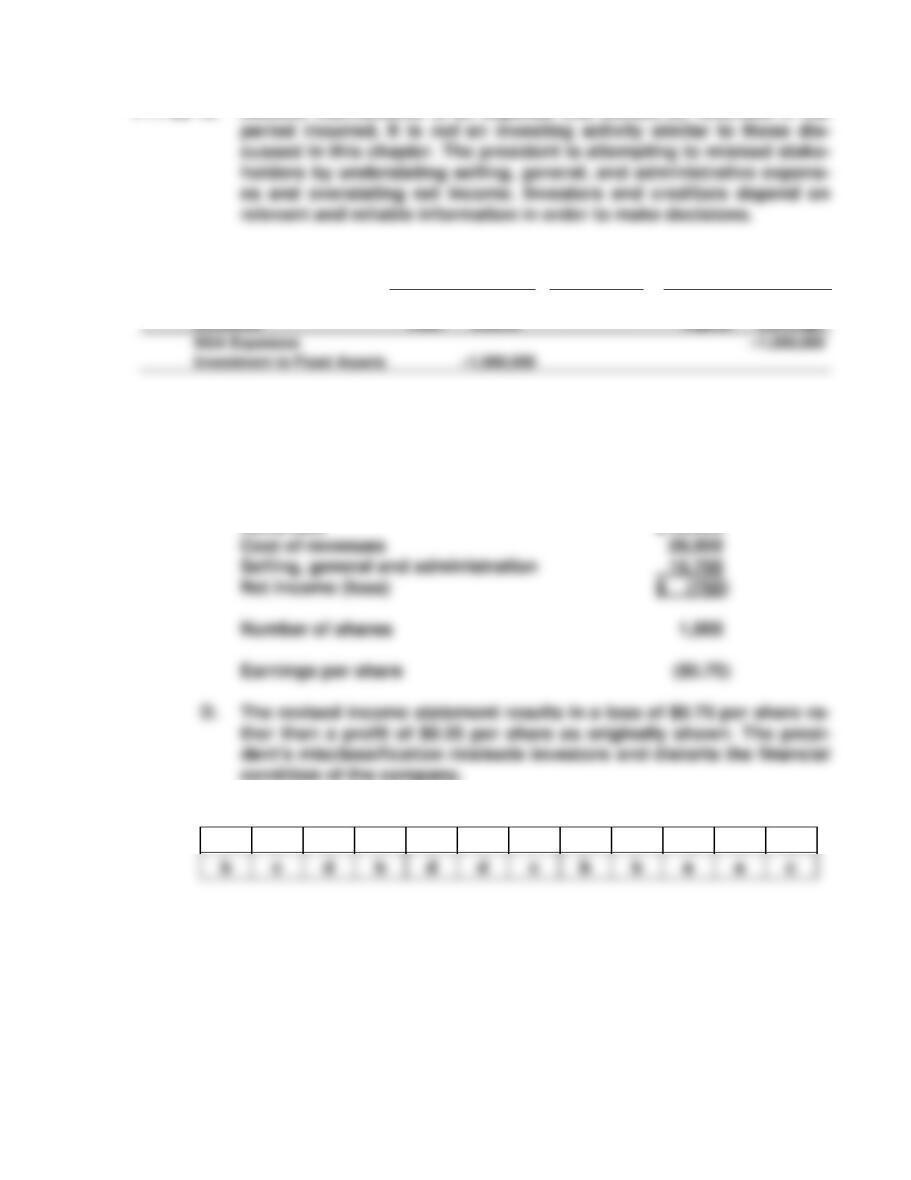

P11-22 A. Routine maintenance is an expense that should be recorded in the

B.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

SGA Expenses

Investment in Fixed Assets

C.

CMI Com World

Statement of Income

For the Year Ended 12/31/07

(In thousands)

Revenues $ 43,000

condition of the company.

P11-23

1

2

3

4

5

6

7

8

9

10

11

12

346 Chapter 11

CASES

C11-1 Financial statement effects of a purchase:

On January 1, Swenson would record an increase in plant assets and

long-term liabilities of $2 million. The assets would be depreciated as fol-

lows:

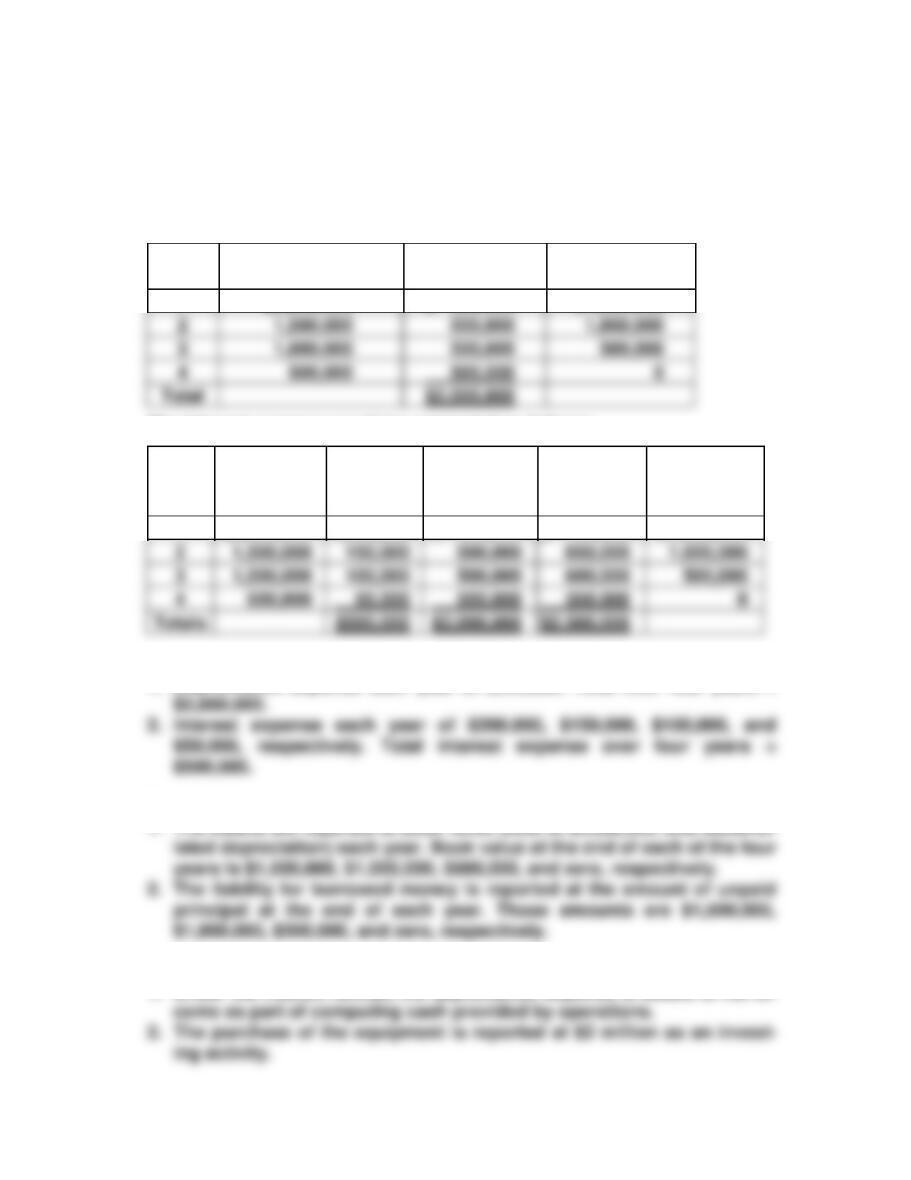

Year

Book Value at

Beginning of Year

Depreciation

Expense

Book Value at

End of Year

1

$2,000,000

$ 500,000

$1,500,000

The interest expense would be computed as follows:

(a)

Year

(b)

Beginning

Principal

(c)

Interest

at 10%

(d)

Repayment

of Principal

(c + d)

Total Cash

Payment

(b − d)

End-of-Year

Principal

1

$2,000,000

$200,000

$ 500,000

$ 700,000

$1,500,000

2

1,500,000

650,000

1,000,000

3

1,000,000

600,000

4

$500,000

$2,500,000

Summary of effects on income statement:

1. Depreciation expense each year of $500,000. Total over four years =

Summary of effects on the balance sheet:

Summary of effects on the statement of cash flows:

1. Under the indirect format, the depreciation expense is added to net in-

2

3

4

Total

Investing Activities 347

3. The borrowing of $2 million from the bank is reported in the first year

Financial statement effects of a lease:

On January 1, Swenson would capitalize the lease at the present value of

Year

Book Value at

Beginning of Year

Depreciation

Expense

Book Value at

End of Year

1

$2,012,867

$ 503,217

$1,509,650

2

3

4

The lease payment schedule would be computed as follows:

(a)

Year

(b)

Beginning

Lease

Principal

(c)

Effective

Interest

(B × 10%)

(d)

Lease

Payment

(Given)

(e)

(d − c)

Reduction

of Lease

Principal

(f)

(b − e)

End-of-Year

Lease

Principal

1

$2,012,867

$201,287

$ 635,000

$ 433,713

$1,579,154

2

1,102,069

3

4

Totals

$527,133

Summary of effects on income statement:

1. Depreciation expense each year of $503,217. Total over four years =

348 Chapter 11

Summary of effects on the balance sheet:

1. The assets are reported at book value (capitalized cost of $2,012,867

Summary of effects on the statement of cash flows:

1. Under the indirect format, the depreciation expense is added to net in-

come as part of computing cash provided by operations.

2. The portion of the lease payment that is repayment of principal is re-

Overall, the lease would result in $40,000 more in cash outflow than the

purchase over the four-year period. The present value of this difference is

C11-2 A. The primary method for depreciating buildings and equipment is the

straight-line method. Accelerated methods are generally used for in-

come tax purposes. Useful lives range from three to 50 years (Note 1–

Investing Activities 349

B. Cost of plant assets is reported in Note 5 (in millions):

Net plant assets $ 3,111

C. Marketable equitable securities are reported in the “Other Assets”

D. Plant assets at end of fiscal year 2003 reported

on the balance sheet (in millions) $2,980

Purchase of plant assets (statement of cash flows) 628