205

chapter

11

Corporations: Organization,

Stock Transactions, and

Dividends

______________________________________________

OPENING COMMENTS

This chapter explains the characteristics of a corporation. It also introduces many of the terms related to

stock: common, preferred, par value, stated value, no-par, cumulative, and noncumulative. Additional

topics covered in Chapter 11 are treasury stock (cost method), stock splits, dividends, and computation

and significance of earnings per share.

After studying the chapter, your students should be able to:

2. Describe and illustrate the characteristics of stock, classes of stock, and entries for issuing stock.

4. Describe and illustrate the accounting for treasury stock transactions.

6. Describe the effect of stock splits on corporate financial statements.

7. Describe and illustrate the use of earnings per share in evaluating a company’s profitability.

KEY TERMS

cash dividend

common stock

206 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

cumulative preferred stock

discount

earnings per common share (EPS)

in arrears

outstanding stock

par value

preferred stock

premium

prior period adjustment

restrictions

STUDENT FAQS

• Why is there a difference between issued and outstanding stock?

• When you sell stock above par value, why can you not have a gain instead of having to put it in paid-

in capital in excess of par value?

• Treasury stock cannot be a good name for ownership of stock in our own company. Can we call it by

some other name, and why can we not record a gain/loss on the sale of treasury stock?

• Treasury stock is not an asset, but I do not understand why. Can you explain?

• Does common stock always have to be sold before preferred stock?

• Why would a company consider issuing preferred stock? If it needs to raise capital, wouldn’t it be

better just to borrow the money from a bank?

• If “dividends in arrears” means we still owe the preferred shareholders a dividend, why are we not

required to book it as a liability? After all, isn’t it a debt or obligation of the company?

• What is the most number of shares a company can issue? Is there a limit on the number besides what

is listed as authorized stock?

• How is it that common stock investors have a greater potential for earning more dividends than do

investors in preferred stock?

Chapter 11 Corporations: Organization, Stock Transactions, and Dividends 207

• When a corporation buys back its own stock, the cash account is credited – where does the cash

physically “go”?

OBJECTIVE 1

Describe the nature of the corporate form of organization.

SYNOPSIS

A corporation is a distinct, separate legal entity. Many large businesses are corporations; as a result, they

generate 90% of the total business dollars in the United States. Corporations have the ability to generate

large amounts of capital. A corporation can also sell shares of ownership called stock. Stock can be

bought and sold without affecting the operation or continued existence of the corporation. Stockholders

have limited liability; they can only lose the amount they have invested in the stock. Stockholders control

a corporation by electing a board of directors. Exhibit 1presents an organization chart for a corporation.

Key Terms and Definitions

• Stock – Shares of ownership of a corporation.

• Stockholders – The owners of a corporation.

Relevant Example Exercises and Exhibits

• Exhibit 1 – Organizational Structure of a Corporation

• Exhibit 2 – Advantages and Disadvantages of the Corporate Form

• Exhibit 3 – Example of Corporations and Their States of Incorporation

SUGGESTED APPROACH

Objective 1 opens with the characteristics of a corporation. Use Transparency Master (TM) 11-1 to

review these characteristics. When covering the concept of limited liability, point out that it is common

208 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

The following is an interesting real-world note you can share with your students: Nonprofit entities often

organize as corporations to limit their legal liability and to obtain favorable tax treatment under federal

tax laws. Examples of nonprofit corporations include the United Way and the Salvation Army.

LECTURE AID—Organization Costs

To begin the process of forming a corporation, a business must file an application of incorporation with

the state in which the company will incorporate. After approving this application, the state grants a charter

(or articles of incorporation) that formally creates the corporation. You may wish to point out that state

incorporation laws differ. Since Delaware has more favorable incorporation laws than other states, more

than half of the largest companies are incorporated in Delaware. Exhibit 3 in the text lists some of them.

Organization costs are the costs incurred during the process of incorporating a business. These costs can

be significant. They include the following:

2. Taxes

4. License fees

5. Promotional costs

Organization costs are recorded as an expense as they are incurred.

GROUP LEARNING ACTIVITY—Organization Costs

Ask your students to record the following entry for Hoover Corporation (see TM 11-2). The correct

journal entry is listed on TM 11-3.

Hoover Corporation was organized early this year. Legal costs and other fees associated with

incorporation totaled $3,500.

OBJECTIVE 2

Describe and illustrate the characteristics of stock, classes of stock, and entries for issuing

stock.

SYNOPSIS

The two main sources of stockholders’ equity are paid-in capital (or contributed capital) and retained

earnings. The main source of paid-in capital is from issuing stock. Authorized stock is the number of

Chapter 11 Corporations: Organization, Stock Transactions, and Dividends 209

shares of stock that a corporation is authorized to issue in its charter. Issued stock refers to the number of

shares sold to stockholders. Sometimes a corporation may reacquire its own stock; reacquired stock is

referred to as Treasury Stock, while stock still in the hands of stockholders is referred to as outstanding

stock. Exhibit 4 depicts the relationship between authorized, issued, and outstanding shares in an easy–to–

remember bull’s eye graphic. Some states that incorporate businesses require the stock to have a par

value or stated value per share. Some states also have a minimum requirement for capital, called the legal

capital; this usually includes the par value of the stock. A corporation may have different classes of stock:

common stock, preferred stock, and cumulative preferred stock. Stock rights include the right to vote on

Key Terms and Definitions

• Common Stock – The stock outstanding when a corporation has issued only one class of stock.

• Cumulative Preferred Stock – Stock that has a right to receive regular dividends that were not

declared (paid) in prior years.

• Discount – The interest deducted from the maturity value of a note or the excess of the face

amount of bonds over their issue price.

• In Arrears – Cumulative preferred stock dividends that have not been paid in prior years are said

to be in arrears.

Relevant Example Exercises and Exhibits

• Example Exercise 11-1 Dividends per Share

• Example Exercise 11-2 Entries for Issuing Stock

• Exhibit 4 – Authorized, Issued, and Outstanding Stock

• Exhibit 5 – Dividend Preferences

SUGGESTED APPROACH

As you can see from the list of key terms above, this objective presents a number of definitions. Use the

following Lecture Aid to explain the difference between common and preferred stock. You will also need

210 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

to reinforce the difference between cumulative and noncumulative preferred stock, using a Demonstration

Problem.

Other terms that merit special emphasis are “legal capital” and “outstanding shares.” Legal capital is the

amount invested by shareholders that cannot be returned in the form of dividends. In most states, the par

or stated value of the stock establishes legal capital. Legal capital provides protection to creditors

because, even in liquidation, it cannot be returned to stockholders until all debts are paid.

LECTURE AID—Classes of Capital Stock

A corporation may have different classes of stockholders. The most common class of stock is called

common stock. The major rights usually granted to a common shareholder are:

2. The right to share in distributions of earnings

3. The right to share in assets upon liquidation

A corporation may establish additional classes of stock by granting certain shareholders preferential

treatment in one or more of these rights. In many cases, the corporation will issue stock that is given

preferential treatment in the area of dividends, called preferred stock. A corporation can even establish

more than one class of preferred stock. Ask your students to check The Wall Street Journal and identify

corporations that have multiple classes of preferred stock.

LECTURE AID—Preferred Stock

Before discussing the dividend characteristics of preferred stock, stress that dividends are not a liability of

a corporation until declared by the board of directors. Corporations are not required to pay dividends.

Chapter 11 Corporations: Organization, Stock Transactions, and Dividends 211

If the preferred stock is cumulative, all dividends in arrears must be paid before any current year preferred

dividends or any common dividends can be paid. If the preferred stock is noncumulative, the preferred

stockholder forfeits any passed dividends.

DEMONSTRATION PROBLEM—Distributing Dividends

Belson Corporation has 10,000 common shareholders and 5,000 preferred shareholders. The preferred

stock has a $5 dividend rate. Two years of dividends are currently in arrears. Assume that the preferred

stock is cumulative. Belson has $155,000 to distribute in the form of dividends. Use this information to

calculate the dividends distributed to the preferred and common shareholders.

Preferred Common Total

Shareholders Shareholders Distributed

Dividends in arrears (5,000 $5 2) $50,000 $ 50,000

Regular dividend 25,000 75,000

Remainder $80,000

Total dividends paid $75,000 $80,000 $155,000

Per share dividends $15 $8

GROUP LEARNING ACTIVITY—Distributing Dividends

Ask your students to work in groups to distribute $65,000 of dividends to be paid by Belson Corporation

under each of the following assumptions:

2. There are three years of preferred dividends in arrears. The preferred stock is noncumulative.

The solutions are shown on TMs 11-4 and 11-5.

212 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

WRITING EXERCISE—Characteristics of Preferred Stock

Ask your students to respond to the following question (TM 11-6):

Possible response: Both Company A and Company B stocks will provide the same dividend per share,

assuming dividends are paid. However, since Company A stock is less expensive, the investor can obtain

more of Company A stock. Company B provides the additional guarantee that if dividends are not

declared in a given year, they will be paid in future years. In order to receive this additional “piece of

mind,” the investor must pay $5 more per share to invest in Company B. The answer will depend on the

SUGGESTED APPROACH—Journalizing the Entries for Issuing Stock

Explain the terms “par value” and “stated value.” Illustrate how these stock characteristics affect the

journal entries for issuing stock, using the Demonstration Problem below.

DEMONSTRATION PROBLEM—Entries for Issuance of Capital Stock

Par value is an arbitrary amount assigned to shares of stock. When preferred or common stock is issued,

the par value of the stock is credited to the stock account. Any amount received above par (called a

Chapter 11 Corporations: Organization, Stock Transactions, and Dividends 213

Example: Belson Corporation sold 1,000 shares of $10 par value common stock for $17 per share.

Cash………………………………………………………….…… 17,000

Common Stock…………………………………………… 10,000

Paid-In Capital in Excess of Par—Common Stock………. 7,000

To emphasize that par value is not related to market value, compare the par value of the sample annual

report for common stock found in Appendix C to the current selling price from The Wall Street Journal.

No-par stock does not have an assigned par value. Some states require that a stated value be assigned to

any no-par stock. If a stock has a stated value, it is treated the same as a par value in recording the stock.

1. Camden Corporation issued 100 shares of no-par preferred stock for $50 per share.

2. Camden Corporation also issued 500 shares of common stock with a stated value of $5 per share for $7

per share.

3. Camden Corporation also issued 1,000 shares of $5 stated value common stock in exchange for

equipment with a fair market value of $8,500.

Equipment………………………………………………………… 8,500

Common Stock……………………………………………. 5,000

Paid-In Capital in Excess of Stated Value—Common Stock 3,500

214 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

OBJECTIVE 3

Describe and illustrate the accounting for cash dividends and stock dividends.

SYNOPSIS

The board of directors of a corporation declares dividends. A cash dividend requires the authorization of

A stock dividend is normally only declared on common stock. Additional shares of common stock are

distributed to common stockholders. A stock dividend affects only stockholders’ equity. The amount of

the stock dividend is transferred from Retained Earnings to Paid-In Capital; the amount transferred is

normally the fair value of the shares issued in the stock dividend. The transaction is recorded as a debit to

Key Terms and Definitions

• Cash Dividend – A cash distribution of earnings by a corporation to its shareholders.

• Stock Dividend – A distribution of shares of stock by a corporation to its stockholders.

Relevant Example Exercises and Exhibits

• Example Exercise 11-3 Entries for Cash Dividends

• Example Exercise 11-4 Entries for Stock Dividends

Chapter 11 Corporations: Organization, Stock Transactions, and Dividends 215

SUGGESTED APPROACH

Begin this topic by commenting on dividend policies. Point out that some companies make it a policy not

to pay dividends at all, plowing all profits back into the company. Stockholders in these corporations

count on share appreciation in order to receive a return on their investment. Companies that do pay

dividends usually try to maintain a stable regular dividend, generally paid quarterly.

Next, review the entries for cash dividends, stressing the importance of the three dividend dates

DEMONSTRATION PROBLEM—Cash Dividends

On January 15, the board of directors of Barns Incorporated declared a $0.25 per-share dividend on its

common stock to shareholders of record on January 31, payable on February 15. Barns has 25,000 shares

of stock authorized, 10,000 shares issued, and 8,000 shares outstanding.

1. Date of Declaration: Once declared, the dividend becomes a liability of the corporation.

Therefore, it is credited to a liability account.

2. Date of Record: No journal entry is required. This date determines who will receive the

dividend. Anyone owning stock in Barns at the close of business that day will receive the dividend.

3. Date of Payment: The liability is paid by mailing the dividend checks.

216 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

LECTURE AID—Stock Dividends

When stock dividends are “paid,” additional shares of stock are mailed to the shareholders (or credited to

their account, actual paper shares of stock being rare these days). This allows the corporation to give a

return to its shareholders without using any of its cash.

A corporation issuing a stock dividend doesn’t get any bigger because the dividend doesn’t bring in any

new assets. The corporation also doesn’t get any smaller because a stock dividend doesn’t use up any

assets. The corporation is just divided into smaller pieces. All shareholders have more pieces, but they’re

still getting the same share of the pie.

How do shareholders profit from stock dividends? In theory, a 10 percent stock dividend should reduce

DEMONSTRATION PROBLEM—Stock Dividends

On June 20, the board of directors of Carlisle Corporation declares a 4 percent stock dividend on its

50,000 shares of common stock. The shares will be issued on July 14. The par value of the stock is $10

per share; the market value on June 20 is $16 per share.

1. Declaration Date: A liability to distribute the dividends is established with a credit to the Stock

Dividends Distributable account.

June 20 Stock Dividends………………………………… 32,000

Stock Dividends Distributable………………….. 20,000

2. Distribution Date: The additional shares are mailed to the shareholders, relieving the corporation’s

liability. The shares are recorded as outstanding by crediting the common stock account.

July 14 Stock Dividends Distributable…………… 20,000

Common Stock…………………… 20,000

WRITING EXERCISE—Stock Dividends

Ask your students to explain the following (TM 11-10):

Explain the benefits of a stock dividend, both to the corporation issuing the dividend and

to the shareholder receiving the dividend.

Answer from Lecture Aid above: A corporation issuing a stock dividend does not get any bigger

because the dividend does not bring in any new assets. The corporation also does not get any smaller

because a stock dividend does not use up any assets. The corporation is just divided into smaller pieces.

All shareholders have more pieces, but they are still getting the same share of the pie.

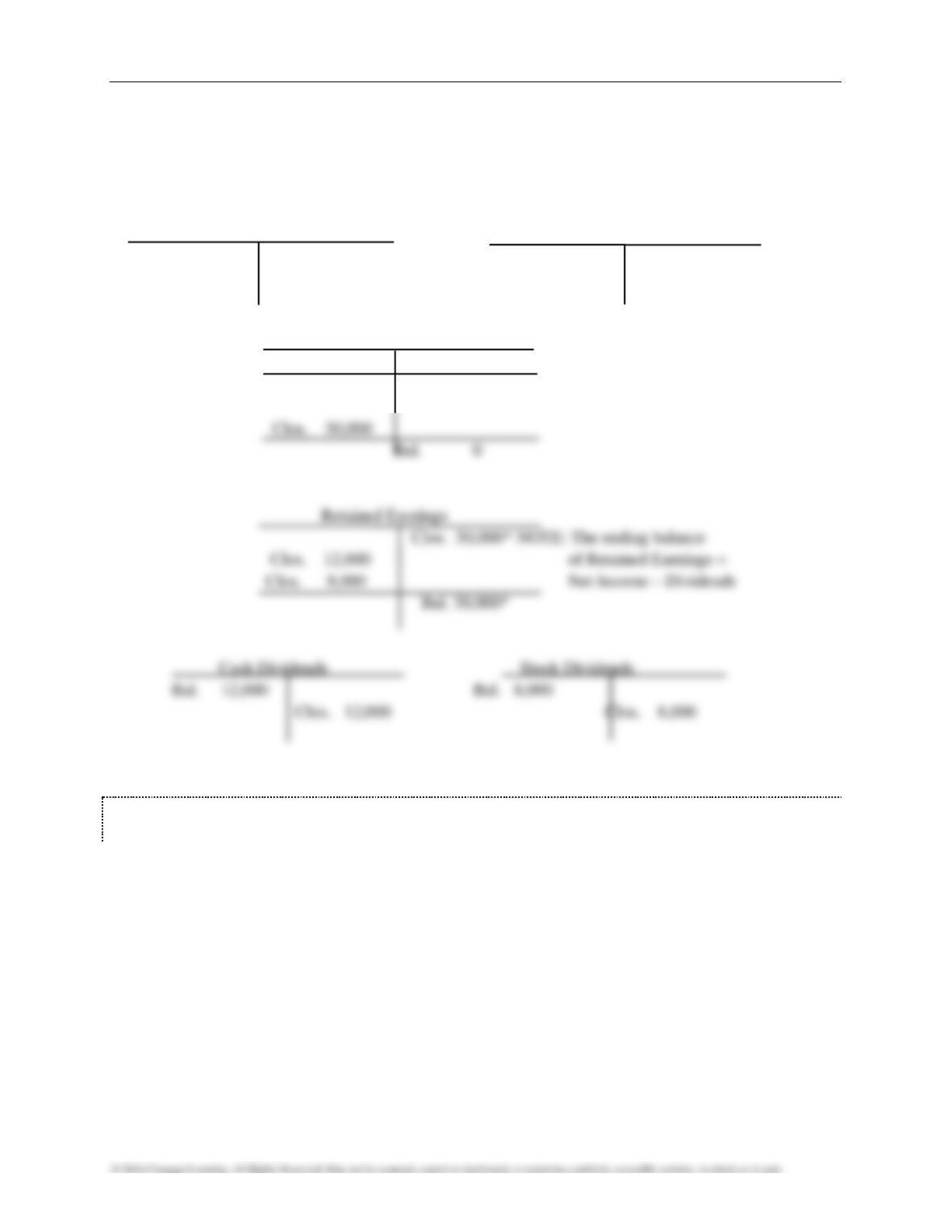

DEMONSTRATION PROBLEM—Closing Entries for a Corporation

Assume a corporation had the following account balances at the end of a fiscal year. (For simplicity, this

is its first year of operations and all expenses are assumed to be recorded in one expense account.)

Revenues $200,000

Expenses 150,000

Cash Dividends 12,000

Stock Dividends 8,000

218 Chapter 11 Corporations: Organization, Stock Transactions, and Dividends

Use these accounts to demonstrate closing entries for a corporation. Remind students that (1) revenues

and expenses are closed to Income Summary, (2) Income Summary is closed to Retained Earnings, and

(3) dividend accounts are closed to Retained Earnings.

Revenues Expenses

Bal. 200,000 Bal. 150,000

Clos. 200,000 Clos. 150,000

Income Summary

Clos. 150,000 Clos. 200,000

Bal. 50,000

OBJECTIVE 4

Describe and illustrate the accounting for treasury stock transactions.

SYNOPSIS

Treasury stock is stock the corporation has issued or sold and then repurchased. A business may do this

for a variety of reasons: to provide shares for resale to employees, to reissue as bonuses, or to support the

market price of the stock. The method for recording this purchase is known as the cost method. When

purchased, the stock is debited at cost to Treasury Stock. When the stock is resold, this account is credited

for its cost; any difference between the cost and the selling price is debited or credited to Paid-In Capital

from Sale of Treasury Stock.