Chapter 11

Current Liabilities and Payroll

Review Questions

1. What are the three main characteristics of liabilities?

The three main characteristics of liabilities are:

2. What is a current liability? Provide some examples of current liabilities.

Current liabilities must be paid with cash or with goods and services within one year or within

3. How is sales tax recorded? Is it considered an expense of a business? Why or why not?

4. How do unearned revenues arise?

5. What do short-term notes payable represent?

6. Coltrane Company has a $5,000 note payable that is paid in $1,000 installments over five years.

How would the portion that must be paid within the next year be reported on the balance sheet?

7. What is the difference between gross pay and net pay?

Gross pay is the total amount of salary, wages, commissions, and bonuses earned by the employee

11-2

8. List the required employee payroll withholding deductions, and provide the tax rate for each.

Required payroll withholding deductions are:

Withholding Deductions

Tax Rate

Federal, State and Local Income Tax

The amount withheld depends on the

employee’s gross pay, filing status,

and the number of withholding

allowances he or she claims.

$200,000.

9. How might a business use a payroll register?

Many companies use a payroll register to help summarize the earnings, withholdings, and net pay for

each employee.

10. What payroll taxes is the employer responsible for paying?

The payroll taxes an employer is responsible for paying are:

11. What are the two main controls for payroll? Provide an example of each.

There are two main controls for payroll: controls for efficiency and controls to safeguard payroll

disbursements.

OASDI tax rate at the time of this

writing is 6.2%.

then 2.35% on any earnings above

11-3

When do businesses record warranty expense, and why?

The matching principle requires businesses to record Warranty Expense in the same period that the

12. What is a contingent liability? Provide some examples of contingencies.

13. Curtis Company is facing a potential lawsuit. Curtis’s lawyers think that it is reasonably possible

that it will lose the lawsuit. How should Curtis report this lawsuit?

14. How is the times-interest-earned ratio calculated, and what does it evaluate?

The times-interest-earned ratio is calculated as earnings before interest and taxes or EBIT (Net

Short Exercises

For all payroll calculations, use the following tax rates and round amounts to the nearest cent.

Employee: OASDI: 6.2% on first $118,500 earned; Medicare: 1.45% up to $200,000, 2.35% on

earnings above $200,000.

Employer: OASDI: 6.2% on first $118,500 earned; Medicare: 1.45%; FUTA: 0.6% on first $7,000

earned; SUTA: 5.4% on first $7,000 earned.

S11-1 Determining current versus long-term liabilities

Learning Objective 1

Rios Raft Company had the following liabilities.

a. Accounts Payable

b. Note Payable due in 3 years

c. Salaries Payable

d. Note Payable due in 6 months

e. Sales Tax Payable

f. Unearned Revenue due in 8 months

g. Income Tax Payable

Determine whether each liability would be considered a current liability (CL) or a long-term liability

(LTL).

SOLUTION

a.

current liability (CL)

long-term liability (LTL)

c.

current liability (CL)

current liability (CL)

e.

current liability (CL)

current liability (CL)

current liability (CL)

S11-2 Recording sales tax

Learning Objective 1

On July 5, Williams Company recorded sales of merchandise inventory on account, $55,000. The sales

were subject to sales tax of 4%. On August 15, Williams Company paid the sales tax owed to the state

from the July 5 transaction.

Requirements

1. Journalize the transaction to record the sale on July 5. Ignore cost of goods sold.

2. Journalize the transaction to record the payment of sales tax to the state on August 15.

S11-2, cont.

SOLUTION

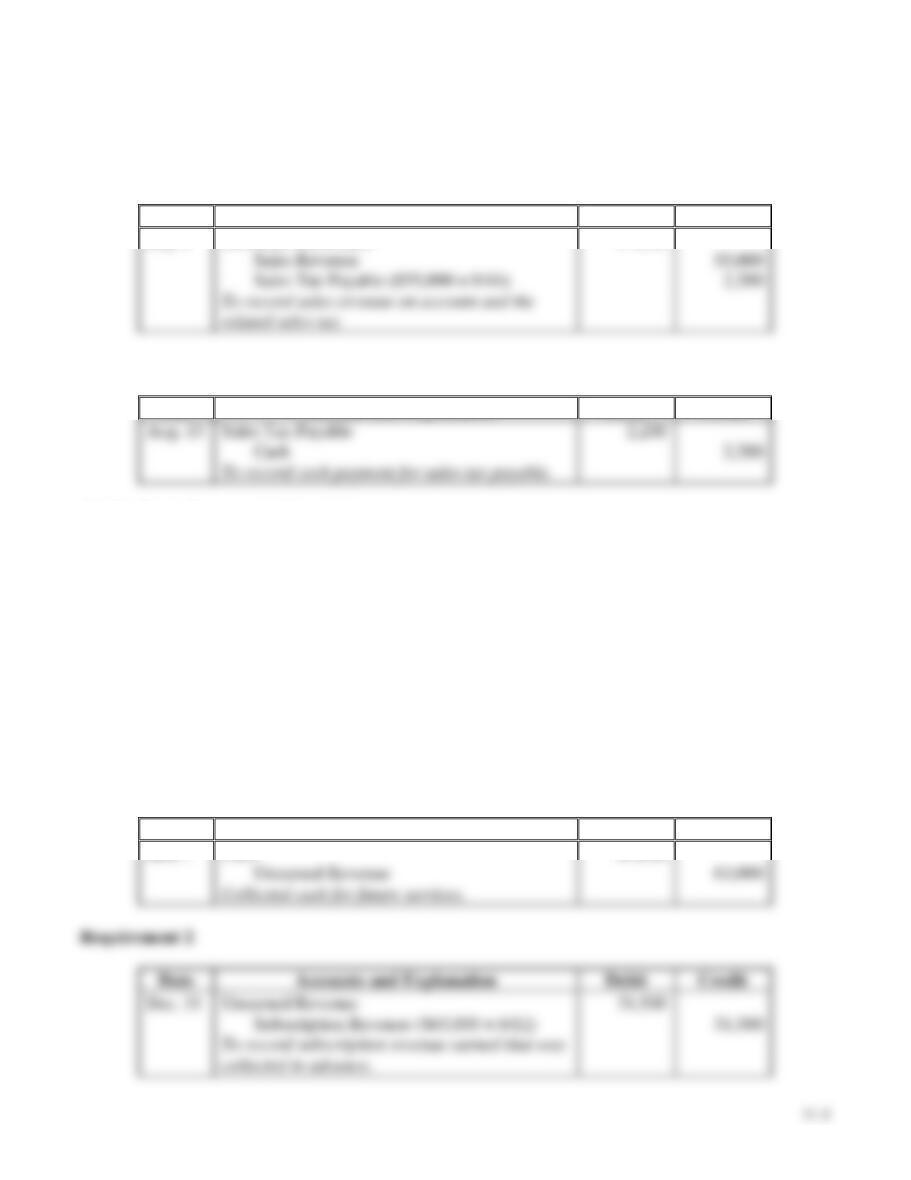

Requirement 1

Date

Accounts and Explanation

Debit

Credit

July 5

Accounts Receivable

57,200

Sales Revenue

55,000

Sales Tax Payable ($55,000 × 0.04)

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Aug. 15

Sales Tax Payable

Cash

S11-3 Recording unearned revenue

Learning Objective 1

On June 1, Hunting Man Magazine collected cash of $63,000 on future annual subscriptions starting on

July 1.

Requirements

1. Journalize the transaction to record the collection of cash on June 1.

2. Journalize the transaction required at December 31, the magazine’s year-end, assuming no revenue

earned has been recorded. (Round adjustment to the nearest whole dollar.)

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 1

Cash

63,000

Unearned Revenue

63,000

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Unearned Revenue

31,500

S11-4 Accounting for a note payable

Learning Objective 1

On December 31, 2017, Franklin purchased $13,000 of merchandise inventory on a one-year, 9% note

payable. Franklin uses a perpetual inventory system.

Requirements

1. Journalize the company’s purchase of merchandise inventory on December 31, 2017.

2. Journalize the company’s accrual of interest expense on June 30, 2018, its fiscal year-end.

3. Journalize the company’s payment of the note plus interest on December 31, 2018.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2017

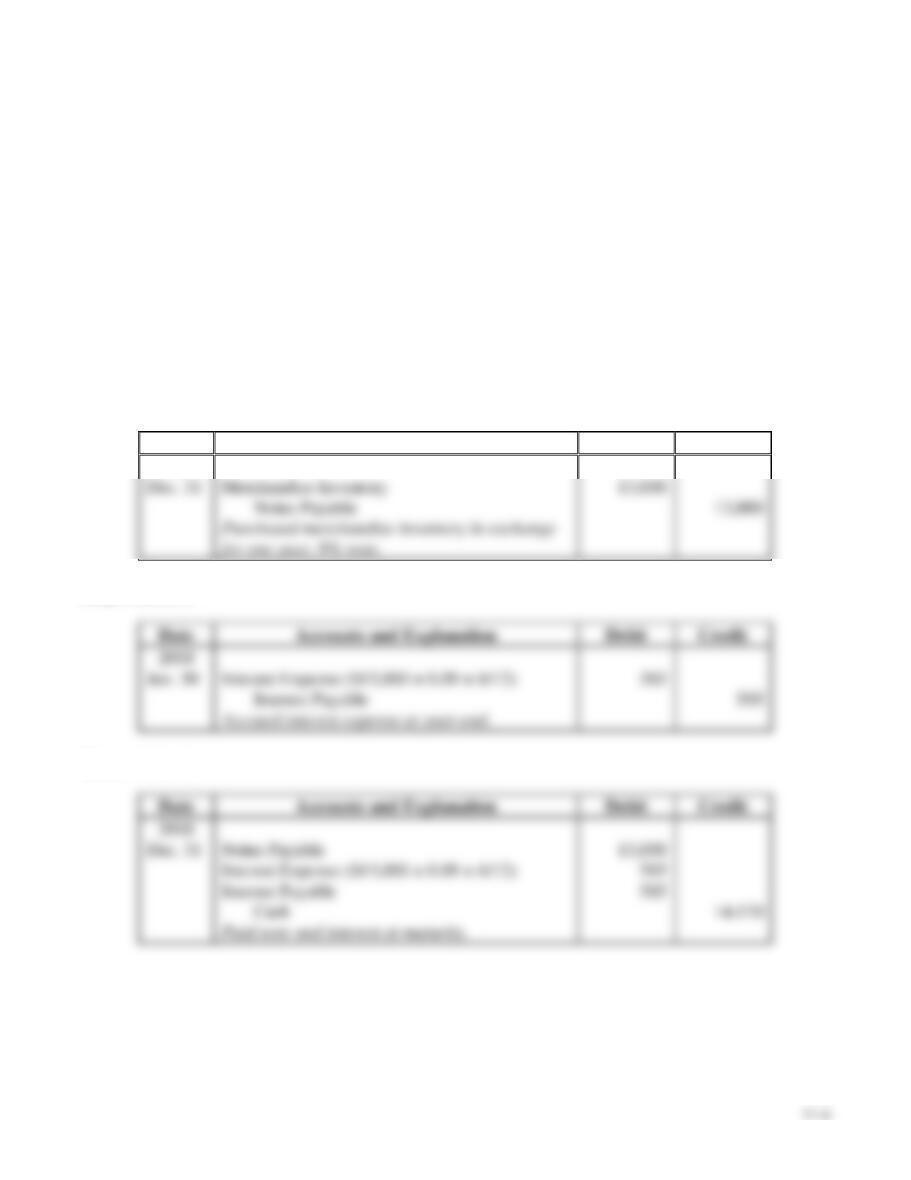

Dec. 31

Merchandise Inventory

Date

Accounts and Explanation

Debit

Credit

2018

Jun. 30

Interest Expense ($13,000 × 0.09 × 6/12)

Requirement 2

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Notes Payable

Interest Expense ($13,000 × 0.09 × 6/12)

Interest Payable

Requirement 3

S11-5 Determining current portion of long-term note payable

Learning Objective 1

On January 1, Irving Company purchased equipment of $280,000 with a long-term note payable. The

debt is payable in annual installments of $56,000 due on December 31 of each year. At the date of

purchase, how will Irving Company report the note payable?

SOLUTION

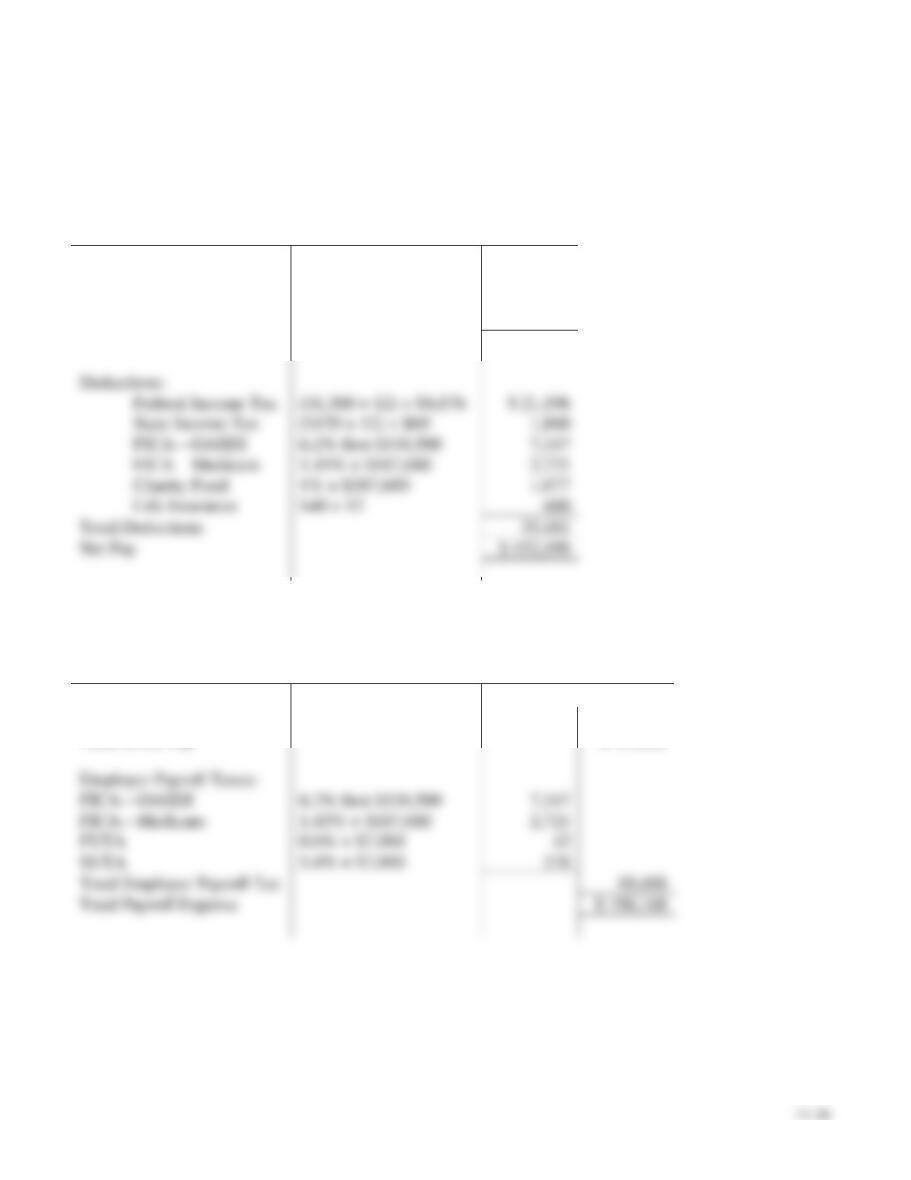

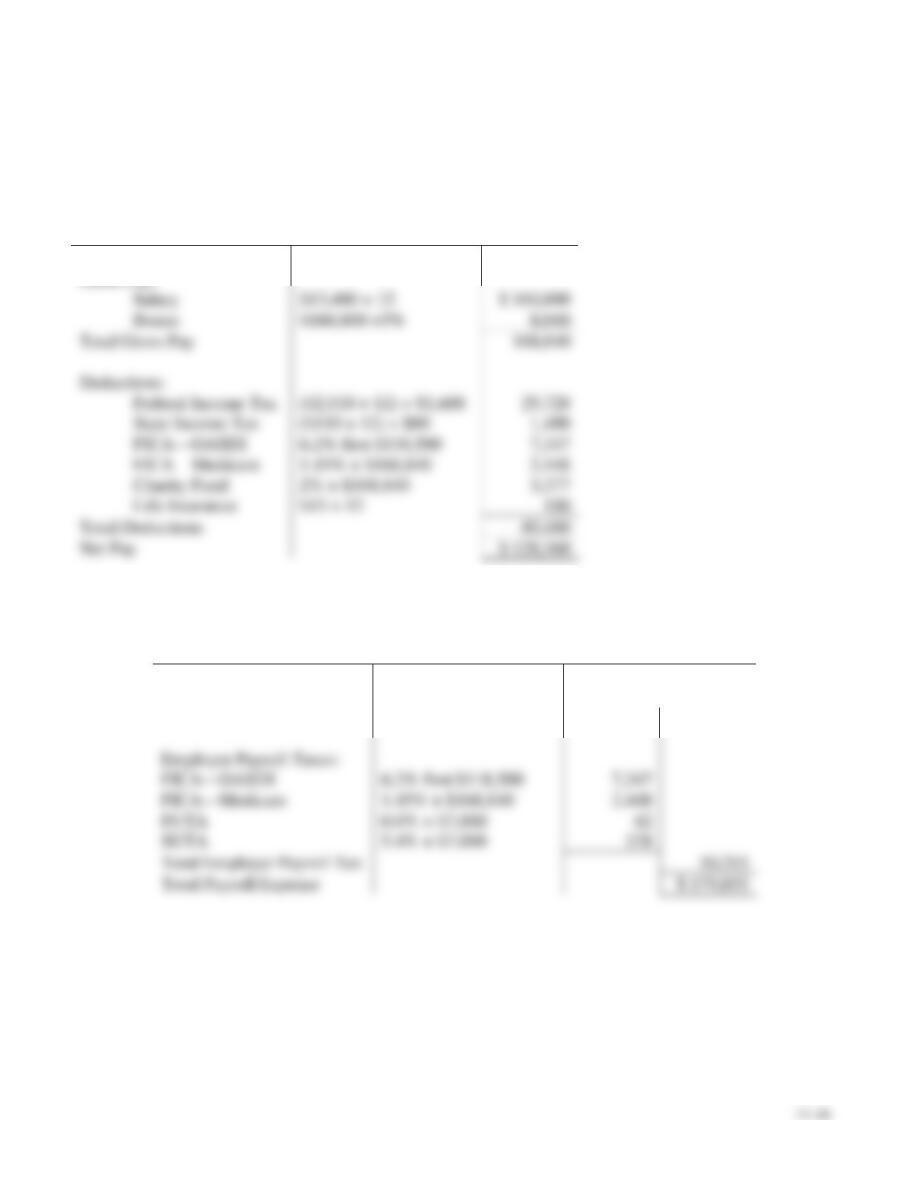

S11-6 Computing and journalizing an employee’s total pay

Learning Objective 2

Lucy Rose works at College of Fort Worth and is paid $12 per hour for a 40-hour workweek and time-

and-a-half for hours above 40.

Requirements

1. Compute Rose’s gross pay for working 60 hours during the first week of February.

2. Rose is single, and her income tax withholding is 15% of total pay. Rose’s only payroll deductions

are payroll taxes. Compute Rose’s net (take–home) pay for the week. Assume Rose’s earnings to date

are less than the OASDI limit.

3. Journalize the accrual of wages expense and the payment related to the employment of Lucy Rose.

SOLUTION

Requirement 1

Straight-time pay for 40 hours ($12 × 40 hours)

$ 480

Overtime pay for 20 hours (20 hours × $12 × 1.5)

Gross Pay

$ 840

Withholding deductions:

Employee income tax (15%)

Employee OASDI tax (6.2%)

Employee Medicare tax (1.45%)

Total withholdings

Net (take-home) pay

S11-6, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Wages Expense

840.00

126.00

Wages Payable

649.74

Wages Payable

649.74

Cash

649.74

S11-7 Computing payroll amounts considering FICA tax limits

Learning Objective 2

Lily Carter works for JDK all year and earns a monthly salary of $12,100. There is no overtime pay.

Lily’s income tax withholding rate is 10% of gross pay. In addition to payroll taxes, Lily elects to

contribute 5% monthly to United Way. JDK also deducts $250 monthly for co-payment of the health

insurance premium. As of September 30, Lily had $108,900 of cumulative earnings.

Requirements

1. Compute Lily’s net pay for October.

2. Journalize the accrual of salaries expense and the payment related to the employment of Lily Carter.

11-9

S11-7, cont.

SOLUTION

Requirement 1

Gross pay

$ 12,100.00

Withholding deductions:

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Salaries Expense

12,100.00

Employee Income Taxes Payable

1,210.00

9,264.35

Salaries Payable

9,264.35

9,264.35

Employee income tax (10%)

$ 1,210.00

Employee OASDI tax (6.2%)*

Employee Medicare tax (1.45%)

Employee health insurance

Employee contribution to United Way (5%)

Total withholdings

Net (take-home) pay

*Calculation of tax for OASDI

Employee earnings subject to tax

$ 118,500

Employee earnings prior to the current month

Current pay subject to tax

Tax rate

Tax to be withheld from paycheck

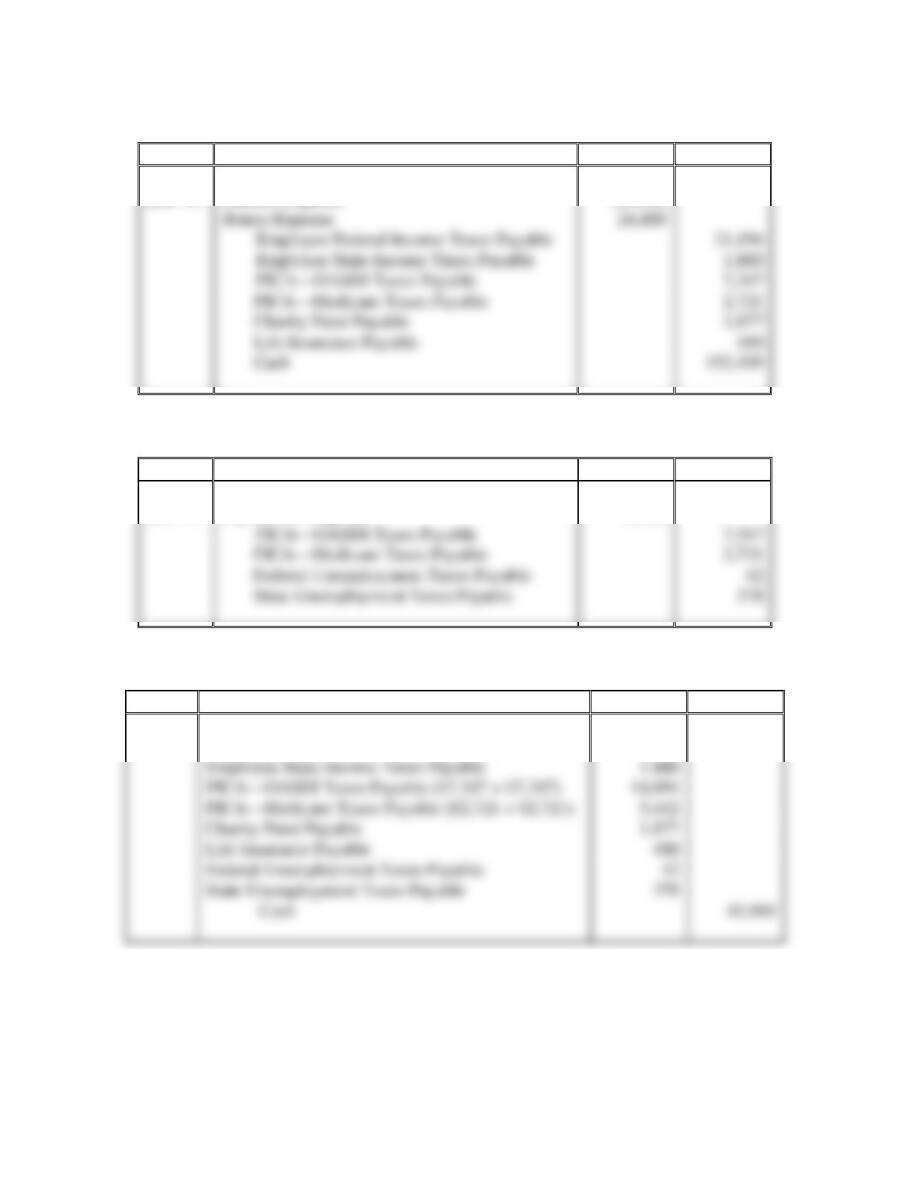

S11-8 Computing and journalizing the payroll expense and payments

Learning Objective 2

Macintosh Company has monthly salaries of $26,000. Assume Macintosh pays all the standard payroll

taxes, no employees have reached the payroll tax limits, total income tax withheld is $2,000, and the

only payroll deductions are payroll taxes. Journalize the accrual of salaries expense, accrual of employer

payroll taxes, and payment of employee and employer payroll taxes for Macintosh Company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Salaries Expense

26,000

FICA—OASDI Taxes Payable (6.2% × $26,000)

1,612

FICA—Medicare Taxes Payable (1.45% × $26,000)

377

2,000

22,011

Payroll Tax Expense

3,549

FICA—OASDI Taxes Payable (6.2% × $26,000)

1,612

FICA—Medicare Taxes Payable (1.45% × $26,000)

377

156

State Unemployment Taxes Payable (5.4% × $26,000)

1,404

3,224

754

Employee Income Taxes Payable

2,000

Federal Unemployment Taxes Payable

156

State Unemployment Taxes Payable

1,404

Cash

7,538

S11-9 Computing bonus payable

Learning Objective 3

On December 31, Weston Company estimates that it will pay its employees a 5% bonus on net income

after deducting the bonus. The company reports net income of $64,000 before the calculation of the

bonus. The bonus will be paid on January 15 of the next year.

Requirements

1. Journalize the December 31 transaction for Weston.

2. Journalize the payment of the bonus on January 15.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Employee Bonus Expense

3,047.62

3,047.62

Date

Accounts and Explanation

Debit

Credit

Employee Bonus Payable

3,047.62

3,047.62

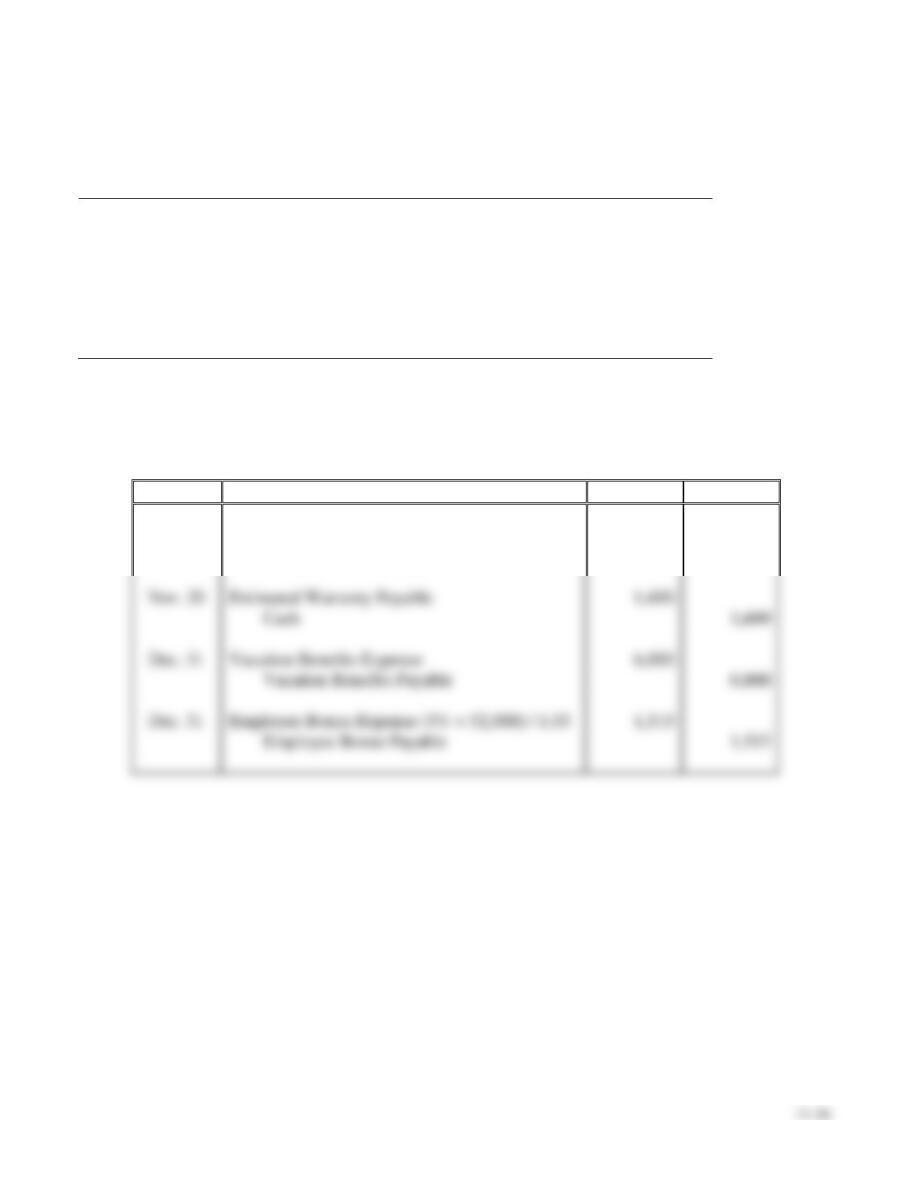

S11-10 Journalizing vacation benefits

Learning Objective 3

Samuel Industries has three employees. Each employee earns two vacation days a month. Samuel pays

each employee a weekly salary of $1,250 for a five-day workweek.

Requirements

1. Determine the amount of vacation expense for one month.

2. Journalize the entry to accrue the vacation expense for the month.

SOLUTION

Requirement 1

Employees

3

Weekly salary

$1,250

× Vacation Days per month

× 2

÷ Days in the week

5

= Total days to accrue

6

= Pay per day

= $250

Total amount to accrue 6 days times $250 per day = $1,500 for one month

Vacation Benefits Expense

1,500

1,500

S11-11 Accounting for warranty expense and warranty payable

Learning Objective 3

Trail Runner guarantees its snowmobiles for three years. Company experience indicates that warranty

costs will be approximately 5% of sales.

Assume that the Trail Runner dealer in Colorado Springs made sales totaling $600,000 during 2018. The

company received cash for 20% of the sales and notes receivable for the remainder. Warranty payments

totaled $10,000 during 2018.

Requirements

1. Record the sales, warranty expense, and warranty payments for the company. Ignore cost of goods

sold.

2. Assume the Estimated Warranty Payable is $0 on January 1, 2018. Post the 2018 transactions to the

Estimated Warranty Payable T-account. At the end of 2018, how much in Estimated Warranty

Payable does the company owe?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Cash (20% × $600,000)

120,000

Notes Receivable (80% × $600,000)

480,000

600,000

Warranty Expense (5% × $600,000)

Estimated Warranty Payable

Payments 10,000

30,000 Accrual

20,000 Bal.

11–14

S11-12 Accounting treatment for contingencies

Learning Objective 4

Freeman Motors, a motorcycle manufacturer, had the following contingencies.

a. Freeman estimates that it is reasonably possible but not likely that it will lose a current lawsuit.

Freeman’s attorneys estimate the potential loss will be $4,500,000.

b. Freeman received notice that it was being sued. Freeman considers this lawsuit to be frivolous.

c. Freeman is currently the defendant in a lawsuit. Freeman believes it is likely that it will lose the

lawsuit and estimates the damages to be paid will be $75,000.

Determine the appropriate accounting treatment for each of the situations Freeman is facing.

SOLUTION

Situation

Appropriate accounting treatment

S11-13 Computing times-interest-earned ratio

Learning Objective 5

Abernathy Electronics reported the following amounts on its 2018 income statement:

Year Ended December 31, 2018

Net income

$ 45,000

Income tax expense

6,750

Interest expense

3,750

What is Abernathy’s times-interest-earned ratio for 2018? (Round to two decimals.)

SOLUTION

Times-interest-earned ratio

Exercises

E11-14 Recording sales tax

Learning Objective 1

Sales Tax Payable $16,100

Consider the following transactions of Sapphire Software:

Mar. 31

Recorded cash sales of $230,000, plus sales tax of 7% collected for the

state of New Jersey.

Apr. 6

Sent March sales tax to the state.

Journalize the transactions for the company. Ignore cost of goods sold.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Mar. 31

Cash

246,100

Sales Revenue

230,000

Sales Tax Payable ($230,000 × 0.07)

16,100

Sales Tax Payable

16,100

Cash

16,100

11–16

E11-15 Recording note payable transactions

Learning Objective 1

Aug. 1, 2018 Interest Expense $840

Consider the following note payable transactions of Creative Video Productions.

2017

Aug. 1

Purchased equipment costing $16,000 by issuing a one-year, 9% note

payable.

Dec. 31

Accrued interest on the note payable.

2018

Aug. 1

Paid the note payable plus interest at maturity.

Journalize the transactions for the company.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2017

Aug. 1

Equipment

16,000

Notes Payable

16,000

Dec. 31

Interest Expense ($16,000 × 0.09 × 5/12)

Interest Payable

2018

Aug. 1

Notes Payable

16,000

Interest Payable

Cash

17,440

E11-16 Recording and reporting current liabilities

Learning Objective 1

Dec. 31 Subscription Revenue $80

Watson Publishing completed the following transactions during 2018:

Oct. 1

Sold a six-month subscription (starting on November 1), collecting cash of

$240, plus sales tax of 8%.

Nov.

15

Remitted (paid) the sales tax to the state of Tennessee.

Dec.

31

Made the necessary adjustment at year-end to record the amount of

subscription revenue earned during the year.

Journalize the transactions (explanations are not required). Round to the nearest dollar.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Oct. 1

Cash

259

Unearned Revenue

240

Sales Tax Payable ($240 × 8%)

Nov. 15

Sales Tax Payable

Cash

Dec. 31

Unearned Revenue

Subscription Revenue

11–18

E11-17 Journalizing current liabilities

Learning Objectives 1, 2

Salaries Expense $3,400

Erin O’Neil Associates reported short-term notes payable and salaries payable as follows:

2018

2017

Current Liabilities—partial:

Short-term Notes Payable

$ 16,900

$ 16,000

Salaries Payable

3,400

4,000

During 2018, O’Neil paid off both current liabilities that were left over from 2017, borrowed cash on

short-term notes payable, and accrued salaries expense. Journalize all four of these transactions for

O’Neil during 2018. Assume no interest on short-term notes payable of $16,000.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Notes Payable

16,000

Cash

16,000

Salaries Payable

Cash

Cash

16,900

Notes Payable

16,900

Salaries Expense

Salaries Payable

11–19

E11-18 Computing and recording gross and net pay

Learning Objective 2

1. Net Pay $576.69

Hugh Stanley manages a Dairy House drive-in. His straight-time pay is $12 per hour, with time-and-a-

half for hours in excess of 40 per week. Stanley’s payroll deductions include withheld income tax of

20%, FICA tax, and a weekly deduction of $5 for a charitable contribution to United Way. Stanley

worked 58 hours during the week.

Requirements

1. Compute Stanley’s gross pay and net pay for the week. Assume earnings to date are $18,000.

2. Journalize Dairy Houses wages expense accrual for Stanley’s work. An explanation is not required.

3. Journalize the subsequent payment of wages to Stanley.

SOLUTION

Requirement 1

Straight-time pay for 40 hours ($12 × 40 hours)

$ 480.00

Overtime pay for 18 hours: (18 × $12 × 1.5)

Gross Pay

$ 804.00

Gross pay

$ 804.00

Withholding deductions:

Employee income tax (20%)

$ 160.80

Employee OASDI tax (6.2%)

Employee Medicare tax (1.45%)

Employee contribution to United Way

Total withholdings

Net (take-home) pay

$ 576.69

11–20

E11-18, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Wages Expense

804.00

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Wages Payable

576.69

Cash

576.69

160.80

United Way Payable

Wages Payable

576.69

E11-19 Recording employer payroll taxes and employee benefits

Learning Objective 2

1. Payroll Tax Expense $6,063.00

Ricardo’s Mexican Restaurant incurred salaries expense of $62,000 for 2018. The payroll expense

includes employer FICA tax, in addition to state unemployment tax and federal unemployment tax. Of

the total salaries, $22,000 is subject to unemployment tax. Also, the company provides the following

benefits for employees: health insurance (cost to the company, $3,000), life insurance (cost to the

company, $330), and retirement benefits (cost to the company, 10% of salaries expense).

Requirements

1. Journalize Ricardo’s expenses for employee benefits and for payroll taxes. Explanations are not

required.

2. What was Ricardo’s total expense for 2018 related to payroll?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Payroll Tax Expense

6,063.00

FICA—OASDI Taxes Payable (6.2% × $62,000)

3,844.00

FICA—Medicare Taxes Payable (1.45% × $62,000)

1,188.00

Employee Benefits Expense

9,530.00

6,200.00

Salaries Expense

Payroll Tax Expense

Employee Benefits Expense

Total

Requirement 2

11–22

E11-20 Recording employee and employer payroll taxes

Learning Objective 2

2. Salaries & Wages Payable $15,923.20

County Company had the following partially completed payroll register:

11–23

Earnings

Withholdings

Net

Pay

Check

No.

Salaries

and Wages

Expense

Beginning

Cumulative

Earnings

Current

Period

Earnings

Ending

Cumulative

Earnings

OASDI

Medicare

Income

Tax

Health

Insurance

United

Way

Total

Withholdings

$ 77,000

$ 4,500

$ 900

$ 90

$ 15

801

112,000

7,200

1,200

144

35

802

48,000

3,300

600

66

0

803

61,000

3,300

850

66

20

804

0

4,500

1,100

90

0

805

$ 298,000

$ 22,800

$ 4,650

$ 456

$ 70

5. Journalize the payment for withholdings and employer payroll taxes.

Requirements

1. Complete the payroll register. Round to two decimals.

2. Journalize County Company’s salaries and wages expense accrual for the current pay period.

3. Journalize County Company’s expenses for employer payroll taxes for the current pay period.

4. Journalize the payment to employees.

SOLUTION

Requirement 1

Earnings

Withholdings

Beginning

Cumulative

Earnings

Current

Period

Earnings

Ending

Cumulative

Earnings

OASDI

Medicare

Income

Tax

Health

Insurance

United

Way

Total

Withholdings

Net Pay

Check

No.

Salaries and

Wages

Expense

$ 77,000.00

$ 4,500.00

$ 81,500.00

$ 279.00

$ 65.25

$ 900.00

$ 90.00

$ 15.00

$ 1,349.25

$ 3,150.75

801

$ 4,500.00

802

803

804

805

$ 320,800.00

11–25

E11-20, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Salaries and Wages Expense

22,800.00

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Payroll Tax Expense

1,970.80

FICA—OASDI Taxes Payable *

1,370.20

*Calculation of tax for OASDI

Employee earnings subject to tax

$ 118,500.00

Employee earnings prior to the current month

Current pay subject to tax

$ 6,500.00

Tax rate

Employer tax

$ 403.00

4,650.00

FICA—OASDI Taxes Payable

1,370.20

FICA—Medicare Taxes Payable

15,923.20

E11-20, cont.

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Salaries and Wages Payable

15,923.20

15,923.20

Requirement 5

Date

Accounts and Explanation

Debit

Credit

Employee Income Taxes Payable

4,650.00

2,740.40

Health Insurance Payable

United Way Payable

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

8,847.60

11–27

E11-21 Accounting for warranty expense and warranty payable

Learning Objective 3

1. Warranty Expense $10,170

The accounting records of Sculpted Ceramics included the following at January 1, 2018:

In the past, Sculpted’s warranty expense has been 9% of sales. During 2018, Sculpted made sales of

$113,000 and paid $7,000 to satisfy warranty claims.

Requirements

1. Journalize Sculpted’s warranty expense and warranty payments during 2018. Explanations are

not required.

2. What balance of Estimated Warranty Payable will Sculpted report on its balance sheet at

December 31, 2018?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Warranty Expense (9% × $113,000)

10,170

10,170

Estimated Warranty Payable

5,000 Beg. Bal.

Payments 7,000

10,170 Accrual

8,170 End Bal.

E11-22 Accounting for warranties, vacation, and bonuses

Learning Objective 3

Dec. 31 Employee Bonus Expense $1,515

McNight Industries completed the following transactions during 2018:

Nov. 1

Made sales of $52,000. McNight estimates that warranty expense is 6%

of sales. (Record only the warranty expense.)

20

Paid $1,600 to satisfy warranty claims.

Dec. 31

Estimated vacation benefits expense to be $6,000.

31

McNight expected to pay its employees a 3% bonus on net income after

deducting the bonus. Net income for the year is $52,000.

Journalize the transactions. Explanations are not required. Round to the nearest dollar.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Nov. 1

Warranty Expense (6% × $52,000)

3,120

Estimated Warranty Payable

3,120

Estimated Warranty Payable

1,600

Cash

1,600

Vacation Benefits Expense

6,000

Vacation Benefits Payable

6,000

Employee Bonus Expense (3% × 52,000) / 1.03

1,515

Employee Bonus Payable

1,515

11–29

E11-23 Accounting treatment for contingencies

Learning Objective 4

Analyze the following independent situations.

a. Weaver, Inc. is being sued by a former employee. Weaver believes that there is a remote chance that

the employee will win. The employee is suing Weaver for damages of $40,000.

b. Gulf Oil Refinery had a gas explosion on one of its oil rigs. Gulf believes it is likely that it will have

to pay environmental clean-up costs and damages in the future due to the gas explosion. Gulf cannot

estimate the amount of the damages.

c. Lawson Enterprises estimates that it will have to pay $75,000 in warranty repairs next year.

Determine how each contingency should be treated.

SOLUTION

Situation

Appropriate accounting treatment

E11-24 Computing times-interest-earned ratio

Learning Objective 5

1. Cash Ratio 118.80 times

The following financial information was obtained from the year ended 2018 income statements for

Cash Automotive and Pennington Automotive:

Cash

Pennington

Net income

$

26,070

$ 74,188

Income tax expense

9,270

27,080

Interest expense

300

2,900

Requirements

1. Compute the times-interest-earned ratio for each company. Round to two decimals.

2. Which company was better able to cover its interest expense?

SOLUTION

Requirement 1

Times-interest-earned ratio

Cash

Pennington

Net Income

$ 26,070

$ 74,188

+ Income Tax Expense

+ Interest Expense

Total

$ 35,640

$ 104,168

÷ Interest Expense

Ratio for 2018

11–31

Problems (Group A)

P11-25A Journalizing and posting liabilities

Learning Objectives 1, 2

1d. Rent Revenue $3,000

The general ledger of Seal-N-Ship at June 30, 2018, the end of the company’s fiscal year, includes

the following account balances before payroll and adjusting entries.

Accounts Payable

$

114,000

Interest Payable

0

Salaries Payable

0

Employee Income Taxes Payable

0

FICA—OASDI Taxes Payable

0

FICA—Medicare Taxes Payable

0

Federal Unemployment Taxes

Payable

0

State Unemployment Taxes

Payable

0

Unearned Rent Revenue

7,200

Long-term Notes Payable

210,000

The additional data needed to develop the payroll and adjusting entries at June 30 are as follows:

a. The long-term debt is payable in annual installments of $42,000, with the next installment due on

July 31. On that date, Seal-N-Ship will also pay one year’s interest at 9%. Interest was paid on

July 31 of the preceding year. Make the adjusting entry to accrue interest expense at year-end.

b. Gross unpaid salaries for the last payroll of the fiscal year were $4,700. Assume that employee

income taxes withheld are $910 and that all earnings are subject to OASDI.

c. Record the associated employer taxes payable for the last payroll of the fiscal year, $4,700.

Assume that the earnings are not subject to unemployment compensation taxes

d. On February 1, the company collected one year’s rent of $7,200 in advance.

Requirements

1. Using T-accounts, open the listed accounts and insert the unadjusted June 30 balances.

2. Journalize and post the June 30 payroll and adjusting entries to the accounts that you opened.

Identify each adjusting entry by letter. Round to the nearest dollar.

3. Prepare the current liabilities section of the balance sheet at June 30, 2018.

SOLUTION

Requirements 1 and 2

Date

Accounts and Explanation

Debit

Credit

2018

June 30

a.

Interest Expense

17,325

Interest Payable ($210,000 × 9% × 11/12)

17,325

a.

Salaries Payable

c.

Payroll Tax Expense

Unearned Rent Revenue

P11-25A, cont.

Requirements 1 and 2, cont.

Accounts Payable

114,000 Beg. Bal.

114,000 End Bal.

Employee Income Taxes Payable

0 Beg. Bal.

910 b.

910 End Bal.

FICA—OASDI Taxes Payable

0 Beg. Bal.

291 b.

291 c.

582 End Bal.

0 Beg. Bal.

68 c.

136 End Bal.

d. 3,000

210,000 Beg. Bal.

210,000 End Bal.

P11-25A, cont.

Requirement 3

SEAL-N-SHIP

Balance Sheet (Partial)

June 30, 2018

Liabilities

Current Liabilities:

Accounts Payable

$ 114,000

Current Portion of Notes Payable

Interest Payable

Salaries Payable

Employee Income Taxes Payable

Unearned Rent Revenue

Total Current Liabilities

$ 182,584

P11-26A Computing and journalizing payroll amounts

Learning Objective 2

1. Net Pay $152,199

Logan White is general manager of Valuepoint Salons. During 2018, White worked for the company all

year at a $13,600 monthly salary. He also earned a year-end bonus equal to 15% of his annual salary.

White’s federal income tax withheld during 2018 was $1,360 per month, plus $4,876 on his bonus

check. State income tax withheld came to $150 per month, plus $60 on the bonus. FICA tax was

withheld on the annual earnings. White authorized the following payroll deductions: Charity Fund

contribution of 1% of total earnings and life insurance of $40 per month.

Valuepoint incurred payroll tax expense on White for FICA tax. The company also paid state

unemployment tax and federal unemployment tax.

Requirements

1. Compute White’s gross pay, payroll deductions, and net pay for the full year 2018. Round all

amounts to the nearest dollar.

2. Compute Valuepoint’s total 2018 payroll tax expense for White.

3. Make the journal entry to record Valuepoint’s expense for White’s total earnings for the year, his

payroll deductions, and net pay. Debit Salaries Expense and Bonus Expense as appropriate. Credit

liability accounts for the payroll deductions and Cash for net pay. An explanation is not required.

4. Make the journal entry to record the accrual of Valuepoint’s payroll tax expense for White’s total

earnings.

5. Make the journal entry for the payment of the payroll withholdings and taxes.

P11-26A, cont.

SOLUTION

Requirement 1

Logan White

Payroll for the year ended December 31, 2018

Calculation

Annual

Gross Pay:

Salary

$13,600 × 12

$ 163,200

Bonus

$163,200 × 15%

24,480

Total Gross Pay

$ 187,680

Deductions:

Federal Income Tax

State Income Tax

6.2% first $118,500

1.45% × $187,680

Charity Fund

1% × $187,680

Life Insurance

$40 × 12

Total Deductions

35,481

Net Pay

$ 152,199

Requirement 2

Logan White

Employer Payroll Expense for the year ended December 31, 2018

Calculation

Annual

Total Gross Pay

$187,680

Employer Payroll Taxes:

6.2% first $118,500

1.45% × $187,680

FUTA

0.6% × $7,000

SUTA

5.4% × $7,000

Total Employer Payroll Tax

10,488

Total Payroll Expense

$ 198,168

11–37

P11-26A, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Salaries Expense

163,200

Requirement 4

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Payroll Tax Expense

10,488

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

Requirement 5

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Employee Federal Income Taxes Payable

21,196

Employee State Income Taxes Payable

14,694

Charity Fund Payable

Life Insurance Payable

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

45,969

Bonus Expense

24,480

21,196

Charity Fund Payable

Life Insurance Payable

Cash

152,199

P11-27A Journalizing liability transactions

Learning Objectives 1, 3

Jan. 29 Cash $16,695

The following transactions of Plymouth Pharmacies occurred during 2017 and 2018:

2017

Jan. 9

Purchased computer equipment at a cost of $12,000, signing a six-month,

9% note payable for that amount.

29

Recorded the week’s sales of $63,000, three-fourths on credit and one-

fourth for cash. Sales amounts are subject to a 6% state sales tax. Ignore

cost of goods sold.

Feb. 5

Sent the last week’s sales tax to the state.

Jul. 9

Paid the six-month, 9% note, plus interest, at maturity.

Aug.

31

Purchased merchandise inventory for $9,000, signing a six-month, 10%

note payable. The company uses the perpetual inventory system.

Dec.

31

Accrued warranty expense, which is estimated at 4% of sales of $609,000.

31

Accrued interest on all outstanding notes payable.

2018

Feb. 28

Paid the six-month 10% note, plus interest, at maturity.

Journalize the transactions in Plymouth’s general journal. Explanations are not required. Round to

the nearest dollar.

11–39

P11-27A, cont.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2017

Jan. 9

Computer Equipment

12,000

Notes Payable

12,000

Cash ($63,000 × ¼) + ($15,750 × 6%)

16,695

Accounts Receivable ($63,000 × ¾) + (47,250 × 6%)

50,085

63,000

Sales Tax Payable

Notes Payable

12,000

12,540

Aug. 31

Merchandise Inventory

Warranty Expense (4% × $609,000)

24,360

24,360

Interest Expense ($9,000 × 10% × 4/12)

2018

Notes Payable

Interest Payable

Interest Expense ($9,000 × 10% × 2/12)

P11-28A Journalizing liability transactions

Learning Objectives 3, 4

1. June 30 Warranty Expense $7,000

The following transactions of Jasmine Reef occurred during 2018:

Apr. 30

Reef is party to a patent infringement lawsuit of $190,000. Reef’s attorney

is certain it is remote that Reef will lose this lawsuit.

Jun. 30

Estimated warranty expense at 2% of sales of $350,000.

Jul. 28

Warranty claims paid in the amount of $5,500.

Sep. 30

Reef is party to a lawsuit for copyright violation of $80,000. Reef’s attorney

advises that it is probable Reef will lose this lawsuit. The attorney estimates

the loss at $80,000.

Dec. 31

Reef estimated warranty expense on sales for the second half of the year of

$510,000 at 2%.

Requirements

1. Journalize required transactions, if any, in Reef’s general journal. Explanations are not required.

2. What is the balance in Estimated Warranty Payable assuming a beginning balance of $0?

11–41

P11-28A, cont.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Apr. 30

No entry required

Requirement 2

Estimated Warranty Payable

7,000 Jun. 30

Jul. 28 5,500

10,200 Dec. 31

11,700 End Bal.

Jun. 30

Warranty Expense (2% × $350,000)

Estimated Warranty Payable

Sep. 30

Estimated Loss from Lawsuit

Dec. 31

Warranty Expense (2% × $510,000)

11–42

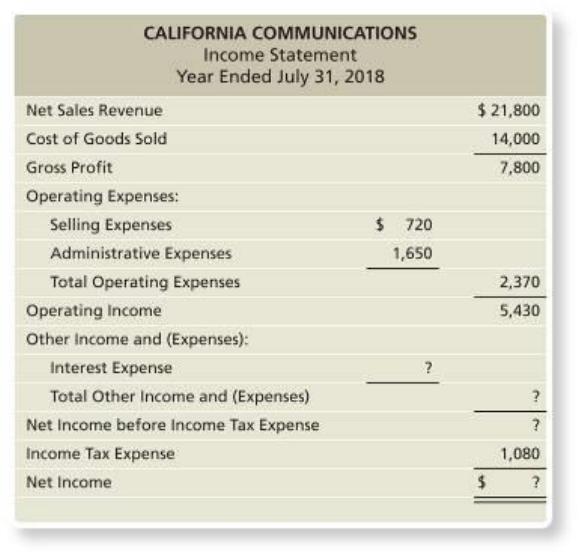

P11-29A Computing times-interest-earned ratio

Learning Objective 5

1. Net Income $4,305

The income statement for California Communications follows. Assume California Communications

signed a 3-month, 9%, $3,000 note on June 1, 2018, and that this was the only note payable for the

company.

Requirements

1. Fill in the missing information for California’s year ended July 31, 2018, income statement. Round to

the nearest dollar.

2. Compute the times-interest-earned ratio for the company. Round to two decimals.

(45)

P11-29A, cont.

SOLUTION

Requirement 1

Interest Expense = $3,000 × 9% × 2/12 = $45

Requirement 2

Times-interest-earned ratio

Net Income

$ 4,305

+ Income Tax Expense

+ Interest Expense

Total

$ 5,430

÷ Interest Expense

Ratio for 2018

Problems (Group B)

P11-30B Journalizing and posting liabilities

Learning Objectives 1, 2

1d. Rent Revenue $2,250

The general ledger of Prompt Ship at June 30, 2018, the end of the company’s fiscal year, includes the

following account balances before payroll and adjusting entries.

Accounts Payable

$ 118,000

Interest Payable

0

Salaries Payable

0

Employee Income Taxes Payable

0

FICA—OASDI Taxes Payable

0

FICA—Medicare Taxes Payable

0

Federal Unemployment Taxes Payable

0

State Unemployment Taxes Payable

0

Unearned Rent Revenue

5,400

Long-term Notes Payable

198,000

The additional data needed to develop the payroll and adjusting entries at June 30 are as follows:

a. The long-term debt is payable in annual installments of $39,600, with the next installment due on

July 31. On that date, Prompt Ship will also pay one year’s interest at 10%. Interest was paid on

July 31 of the preceding year. Make the adjusting entry to accrue interest expense at year-end.

b. Gross unpaid salaries for the last payroll of the fiscal year were $4,800. Assume that employee

income taxes withheld are $920 and that all earnings are subject to OASDI.

c. Record the associated employer taxes payable for the last payroll of the fiscal year, $4,800.

Assume that the earnings are not subject to unemployment compensation taxes.

d. On February 1, the company collected one year’s rent of $5,400 in advance.

Requirements

1. Using T-accounts, open the listed accounts and insert the unadjusted June 30 balances.

2. Journalize and post the June 30 payroll and adjusting entries to the accounts that you opened.

Identify each adjusting entry by letter. Round to the nearest dollar.

3. Prepare the current liabilities section of the balance sheet at June 30, 2018.

11–45

P11-30B, cont.

SOLUTION

Requirements 1 and 2

Date

Accounts and Explanation

Debit

Credit

2018

Jun. 30

a.

Interest Expense

18,150

Interest Payable ($198,000 × 10% × 11/12)

18,150

Accounts Payable

118,000 Beg. Bal.

118,000 End Bal.

18,150 a.

a.

Salary Expense

Salaries Payable

c.

Payroll Tax Expense

Unearned Rent Revenue

P11-30B, cont.

Requirements 1 and 2, cont.

Employee Income Taxes Payable

0 Beg. Bal.

920 b.

920 End Bal.

0 Beg. Bal.

0 Beg. Bal.

70 c.

d. 2,250

P11-30B, cont.

Requirement 3

PROMPT SHIP

Balance Sheet (Partial)

June 30, 2018

Liabilities

Current Liabilities:

Accounts Payable

$ 118,000

Current Portion of Notes Payable

Interest Payable

Salaries Payable

Employee Income Taxes Payable

Unearned Rent Revenue

Total Current Liabilities

$ 184,068

P11-31B Computing and journalizing payroll amounts

Learning Objective 2

1. Net Pay $128,360

Liam Wallace is general manager of Moonwalk Salons. During 2018, Wallace worked for the company

all year at a $13,400 monthly salary. He also earned a year-end bonus equal to 5% of his annual salary.

Wallace’s federal income tax withheld during 2018 was $2,010 per month, plus $1,608 on his bonus

check. State income tax withheld came to $110 per month, plus $80 on the bonus. FICA tax was

withheld on the annual earnings. Wallace authorized the following payroll deductions: Charity Fund

contribution of 2% of total earnings and life insurance of $15 per month.

Moonwalk incurred payroll tax expense on Wallace for FICA tax. The company also paid state

unemployment tax and federal unemployment tax.

Requirements

1. Compute Wallace’s gross pay, payroll deductions, and net pay for the full year 2018. Round all

amounts to the nearest dollar.

2. Compute Moonwalk’s total 2018 payroll tax expense for Wallace.

3. Make the journal entry to record Moonwalk’s expense for Wallace’s total earnings for the year, his

payroll deductions, and net pay. Debit Salaries Expense and Bonus Expense as appropriate. Credit

liability accounts for the payroll deductions and Cash for net pay. An explanation is not required.

4. Make the journal entry to record the accrual of Moonwalk’s payroll tax expense for Wallace’s total

earnings.

5. Make the journal entry for the payment of the payroll withholdings and taxes.

P11-31B, cont.

SOLUTION

Requirement 1

Liam Wallace

Payroll for the year ended December 31, 2018

Calculation

Annual

Gross Pay:

$13,400 × 12

$160,800 ×5%

Total Gross Pay

Deductions:

6.2% first $118,500

1.45% × $168,840

2% × $168,840

$15 × 12

Total Deductions

Net Pay

Requirement 2

Liam Wallace

Employer Payroll Expense for the year ended December 31, 2018

Calculation

Annual

Gross Pay

$168,840

Employer Payroll Taxes:

6.2% first $118,500

1.45% × $168,840

FUTA

0.6% × $7,000

SUTA

5.4% × $7,000

Total Employer Payroll Tax

Total Payroll Expense

11–49

P11-31B, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Salaries Expense

160,800

Requirement 4

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Payroll Tax Expense

10,215

7,347

2,448

Federal Unemployment Taxes Payable

Requirement 5

Date

Accounts and Explanation

Debit

Credit

2018

Dec. 31

Employee Federal Income Taxes Payable

25,728

Employee State Income Taxes Payable

1,400

14,694

4,896

Charity Fund Payable

3,377

Life Insurance Payable

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

50,695

Bonus Expense

8,040

25,728

1,400

7,347

2,448

Charity Fund Payable

3,377

Life Insurance Payable

Cash

128,360

P11-32B Journalizing liability transactions

Learning Objectives 1, 3

Jan. 29 Cash $18,020

The following transactions of Philadelphia Pharmacies occurred during 2017 and 2018:

2017

Jan. 9

Purchased computer equipment at a cost of $7,000, signing a six-month, 8%

note payable for that amount.

29

Recorded the week’s sales of $68,000, three-fourths on credit and one-

fourth for cash. Sales amounts are subject to a 6% state sales tax. Ignore

cost of goods sold.

Feb. 5

Sent the last week’s sales tax to the state.

Jul. 9

Paid the six-month, 8% note, plus interest, at maturity.

Aug.

31

Purchased merchandise inventory for $3,000, signing a six-month, 10%

note payable. The company uses a perpetual inventory system.

Dec.

31

Accrued warranty expense, which is estimated at 2% of sales of $609,000.

31

Accrued interest on all outstanding notes payable.

2018

Feb. 28

Paid the six-month 10% note, plus interest, at maturity.

Journalize the transactions in Philadelphia’s general journal. Explanations are not required.

11–51

P11-32B, cont.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2017

Jan. 9

Computer Equipment

7,000

Notes Payable

7,000

29

Cash ($68,000 × ¼) + ($17,000 × 6%)

Accounts Receivable ($68,000 × ¾) + (51,000 × 6%)

4,080

Sales Tax Payable

4,080

4,080

Notes Payable

7,000

7,280

Aug. 31

Merchandise Inventory

3,000

3,000

Warranty Expense (2% × $609,000)

31

Interest Expense ($3,000 × 10% × 4/12)

Notes Payable

3,000

Interest Payable

Interest Expense ($3,000 × 10% × 2/12)

3,150

11–52

P11-33B Journalizing liability transactions

Learning Objectives 3, 4

1. June 30 Warranty Expense $11,700

The following transactions of Belkin Howe occurred during 2018:

Apr. 30

Howe is party to a patent infringement lawsuit of $230,000. Howe’s

attorney is certain it is remote that Howe will lose this lawsuit.

Jun. 30

Estimated warranty expense at 3% of sales of $390,000.

Jul. 28

Warranty claims paid in the amount of $6,300.

Sep. 30

Howe is party to a lawsuit for copyright violation of $90,000. Howe’s

attorney advises that it is probable Howe will lose this lawsuit. The

attorney estimates the loss at $90,000.

Dec. 31

Howe estimated warranty expense on sales for the second half of the

year of $520,000 at 3%.

Requirements

1. Journalize required transactions, if any, in Howe’s general journal. Explanations are not required.

2. What is the balance in Estimated Warranty Payable assuming a beginning balance of $0?

11–53

P11-33B, cont.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2018

Apr. 30

No entry required

11,700 Jun. 30

Jul. 28 6,300

15,600 Dec. 31

21,000 End Bal.

Requirement 2

Jun. 30

Warranty Expense (3% × $390,000)

Estimated Warranty Payable

Sep. 30

Estimated Loss from Lawsuit

Dec. 31

Warranty Expense (3% × $520,000)

11–54

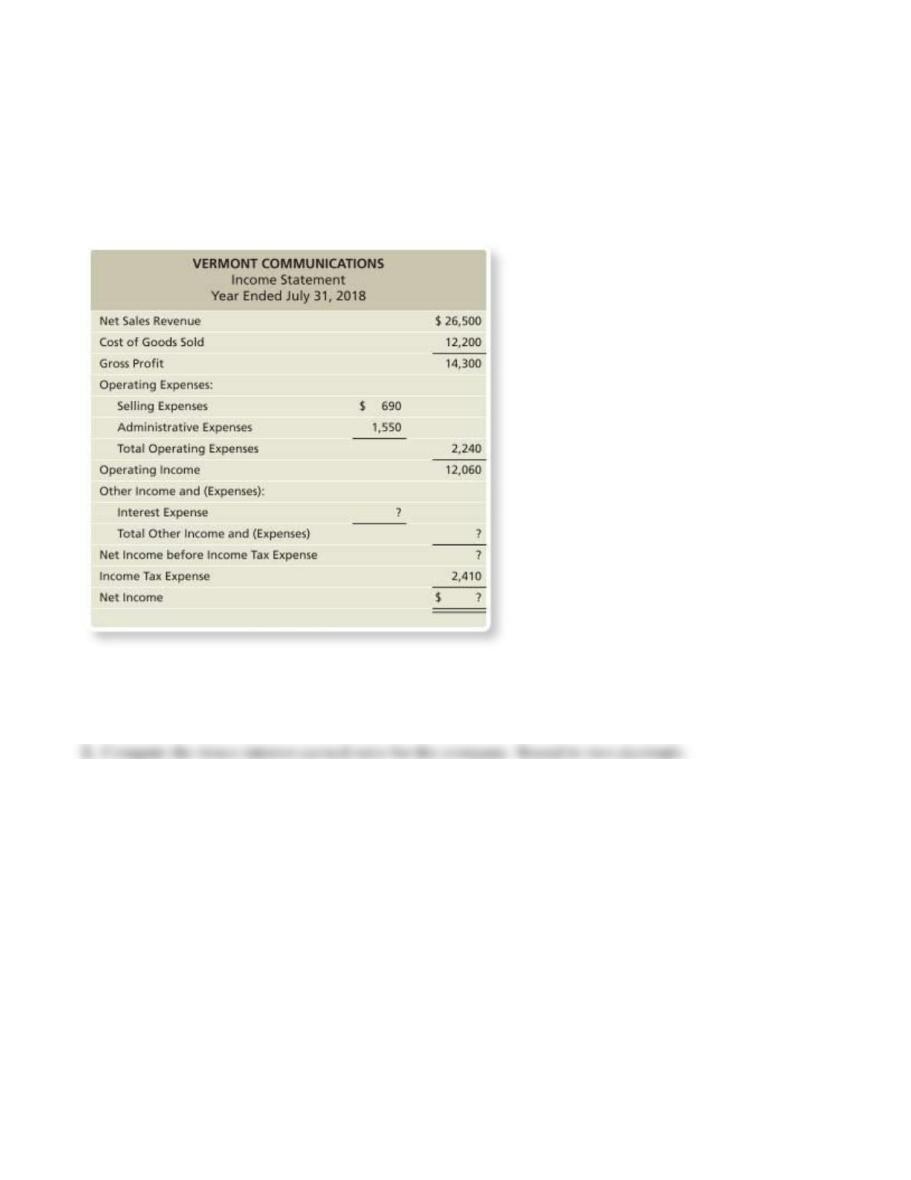

P11-34B Computing times-interest-earned ratio

Learning Objective 5

1. Net Income $9,620

The income statement for Vermont Communications follows. Assume Vermont Communications signed

a 3-month, 3%, $6,000 note on June 1, 2018, and that this was the only note payable for the company.

Requirements

1. Fill in the missing information for Vermont’s year ended July 31, 2018, income statement. Round to

the nearest dollar.

P11-34B, cont.

SOLUTION

Requirement 1

Interest Expense = $6,000 × 3% × 2/12 = $30

VERMONT COMMUNICATIONS

Income Statement

Year Ended July 31, 2018

Net Sales Revenue

$ 26,500

Cost of Goods Sold

Gross Profit

Operating Expenses:

Operating Income

12,060

Other Income and (Expenses):

(30)

Net Income before Income Tax Expense

Income Tax Expense

Net Income

$ 9,620

Requirement 2

Times-interest-earned ratio

Net Income

$ 9,620

+ Income Tax Expense

+ Interest Expense

Total

÷ Interest Expense

Ratio for 2018

11–56

Excel Skill Problem

P11-35 Using Excel for Payroll

Ankel Footwear employees three salespeople, and pays time-and-a-half for overtime. Weekly paychecks

are distributed on the Tuesday following the last day of the week (Saturday). Ankel withholds income

tax (20%), FICA—OASDI (6.2%), and FICA—Medicare (1.45%). Ankel also pays payroll taxes for

FICA—OASDI (6.2%), FICA—Medicare (1.45%), and state and federal unemployment (5.4% and

0.6% respectively). The payroll data for the three salespeople for the week ended March 31 follows:

Name

Straight

Time

Rate

Hours

Worke

d

Beginning

Cumulative

Earnings

Jimmy

Chew

$ 15

46

$ 420

Manny

Blanik

17

50

540

Alexa King

22

38

480

Requirements

1. Complete the Payroll Register for the three employees for the week ended March 31, 2018.

2. Complete the Payroll Tax Register.

3. Compute the total payroll expense for the week ended March 31.

4. Record the payroll entries Ankel makes for each of the following:

a. Wage expense related to the three employees on Saturday, March 31.

b. Employer payroll taxes related to the three employees.

c. Payment of all payroll taxes (employee and employer related) on April 3.

d. Payment of wages on Tuesday, April 3.

SOLUTION

The student templates for Using Excel are available online in MyAccountingLab in the Multimedia

11–57

Continuing Problem

P11-36 Accounting for liabilities of a known amount

This problem continues the Canyon Canoe Company situation from Chapter 10. Amber and Zack

Wilson are continuing their analysis of the company’s position and believe the company will need to

borrow $15,000 in order to expand operations. They consult Rivers Nation Bank and secure a 6%, one-

year note on September 1, 2019, with interest due at maturity. Additionally, the company hires an

employee, John Vance, on September 1. John will receive a salary of $3,000 per month. Payroll

deductions include federal income tax at 25%, OASDI at 6.2%, Medicare at 1.45%, and monthly health

insurance premium of $250. The company will incur matching FICA taxes, FUTA tax at 0.6%, and

SUTA tax at 5.4%. Round calculations to two decimals. Omit explanations on journal entries.

Requirements

1. Record the issuance of the $15,000 note payable on September 1, 2019.

2. Record the employee payroll and employer payroll tax entries on September 30, 2019.

3. Record all payments related to September’s payroll. Payments are made on October 15, 2019.

4. Record the entry to accrue interest due on the note at December 31, 2019.

5. Record the entry Canyon Canoe Company would make to record the payment to the bank on

September 1, 2020.

11–58

SOLUTION

Requirements 1-5

Date

Accounts and Explanation

Debit

Credit

2019

Sep. 1

Cash

15,000.00

Notes Payable

15,000.00

Salaries Expense

Employee Income Taxes Payable ($3,000 × 25%)

Employee Health Insurance Payable

Salaries Payable

Payroll Tax Expense

Federal Unemployment Taxes Payable ($3,000 × 0.6%)

State Unemployment Taxes Payable ($3,000 × 5.4%)

Salaries Payable

Cash

Federal Unemployment Taxes Payable

State Unemployment Taxes Payable

Employee Income Taxes Payable

Employee Health Insurance Payable

Cash

Interest Expense ($15,000 × 6% × 4/12)

Interest Payable

2020

Sep. 1

Notes Payable

15,000.00

Interest Payable

Interest Expense ($15,000 × 6% × 8/12)

15,900.00

11–59

Critical Thinking

Tying It All Together Case 11-1

UnitedHealth Group Incorporated is a diversified health and well-being company dedicated to

helping people live healthier lives. The company operates under two distinct platforms: health benefits

(UnitedHealthcare) and health services (Optum).

Requirements

1. What are contingent liabilities?

2. Review Note 13 (Commitments and Contingencies), specifically the section labeled Legal Matters.

Does UnitedHealth Group Incorporated report any contingencies? If so, provide a summary.

3. How should a company handle contingent liabilities that are reasonably possible or probable but

cannot be estimated?

4. Review Note 13 (Commitments and Contingencies), specifically the section labeled California

Claims Processing Matter. How did UnitedHealth Group Incorporated handle the recording of this

contingent liability?

SOLUTION

Requirement 1

Requirement 2

In the notes to the financial statements, UnitedHealth Group Incorporated states the company is

Requirement 3

Contingent liabilities that are either reasonably possible or probable but cannot be estimated should be

Requirement 4

UnitedHealth Group Incorporated states that the company cannot reasonably estimate the amount of loss

11–60

Decision Case 11-1

Golden Bear Construction operates throughout California. The owner, Gaylan Beavers, employs 15

work crews. Construction supervisors report directly to Beavers, and the supervisors are trusted

employees. The home office staff consists of an accountant and an office manager.

Because employee turnover is high in the construction industry, supervisors hire and fire their own

crews. Supervisors notify the office of all personnel changes. Also, supervisors forward the employee

W-4 forms to the home office. Each Thursday, the supervisors submit weekly time sheets for their

crews, and the accountant prepares the payroll. At noon on Friday, the supervisors come to the office to

get paychecks for distribution to the workers at 5 p.m.

The company accountant prepares the payroll, including the paychecks. Beavers signs all

paychecks. To verify that each construction worker is a bona fide employee, the accountant matches the

employee’s endorsement signature on the back of the canceled paycheck with the signature on that

employee’s W-4 form.

Requirements

1. Identify one way that a supervisor can defraud Golden Bear Construction under the present system.

2. Discuss a control feature that the company can use to safeguard against the fraud you identified in

Requirement 1.

SOLUTION

Requirement 1

A supervisor can enter a fictitious employee on a weekly time sheet, submit the time sheet to the

Requirement 2

To safeguard against the company fraud identified in Requirement 1, Beavers (or a home office

11–61

Decision Case 11-2

Sell-Soft is the defendant in numerous lawsuits claiming unfair trade practices. Sell-Soft has strong

incentives not to disclose these contingent liabilities. However, GAAP requires that companies report

their contingent liabilities.

Requirements

1. Why would a company prefer not to disclose its contingent liabilities?

2. Describe how a bank could be harmed if a company seeking a loan did not disclose its contingent

liabilities.

3. What ethical tightrope must companies walk when they report contingent liabilities?

SOLUTION

Requirement 1

A company would prefer not to disclose its contingent liabilities because they cast a shadow on the

Requirement 2

A contingent liability creates risk for a company. If the contingent liability is not reported, the bank may

Requirement 3

Reporting of contingent liabilities often depends on subjective judgment about whether an outcome is

11–62

Ethical Issue 11-1

Many small businesses have to squeeze down costs any way they can just to survive. One way many

businesses do this is by hiring workers as “independent contractors” rather than as regular employees.

Unlike rules for regular employees, a business does not have to pay Social Security (FICA) taxes and

unemployment insurance payments for independent contractors. Similarly, it does not have to withhold

federal, state, or local income taxes or the employee’s share of FICA taxes. The IRS has a “20 factor

test” that determines whether a worker should be considered an employee or a contractor, but many

businesses ignore those rules or interpret them loosely in their favor. When workers are treated as

independent contractors, they do not get a W-2 form at tax time (they get a 1099 instead), they do not

have any income taxes withheld, and they find themselves subject to “self–employment” taxes, by which

they bear the brunt of both the employee’s and the employer’s shares of FICA taxes.

Requirements

1. When a business abuses this issue, how is the independent contractor hurt?

2. If a business takes an aggressive position—that is, interprets the law in a very slanted way—is there

an ethical issue involved? Who is hurt?

SOLUTION

Requirement 1

The contractor must pay “self–employment tax” which represents both the employer’s and the

Requirement 2

Businesses may take aggressive positions on tax issues, and those positions may be tested in court. It is

11–63

Financial Statement Case 11-1

Details about a company’s liabilities appear in a number of places in the annual report. Visit

1. Give the breakdown of Target’s current liabilities at January 30, 2016.

2. Calculate Target’s times-interest-earned ratio for the year ending January 30, 2016. How does

Target’s ratio compare to Kohl’s Corporation’s ratio?

SOLUTION

Requirement 1

TARGET CORPORATION

Balance Sheet (partial)

January 30, 2016 (In millions)

Requirement 2

Times-Interest-Earned Ratio

(In millions)

January

30, 2016

Communication Activity 11-1

In 150 words or fewer, explain how contingent liabilities are accounted for.

SOLUTION

How businesses record or don’t record contingent liabilities is based on one of three likelihoods of the