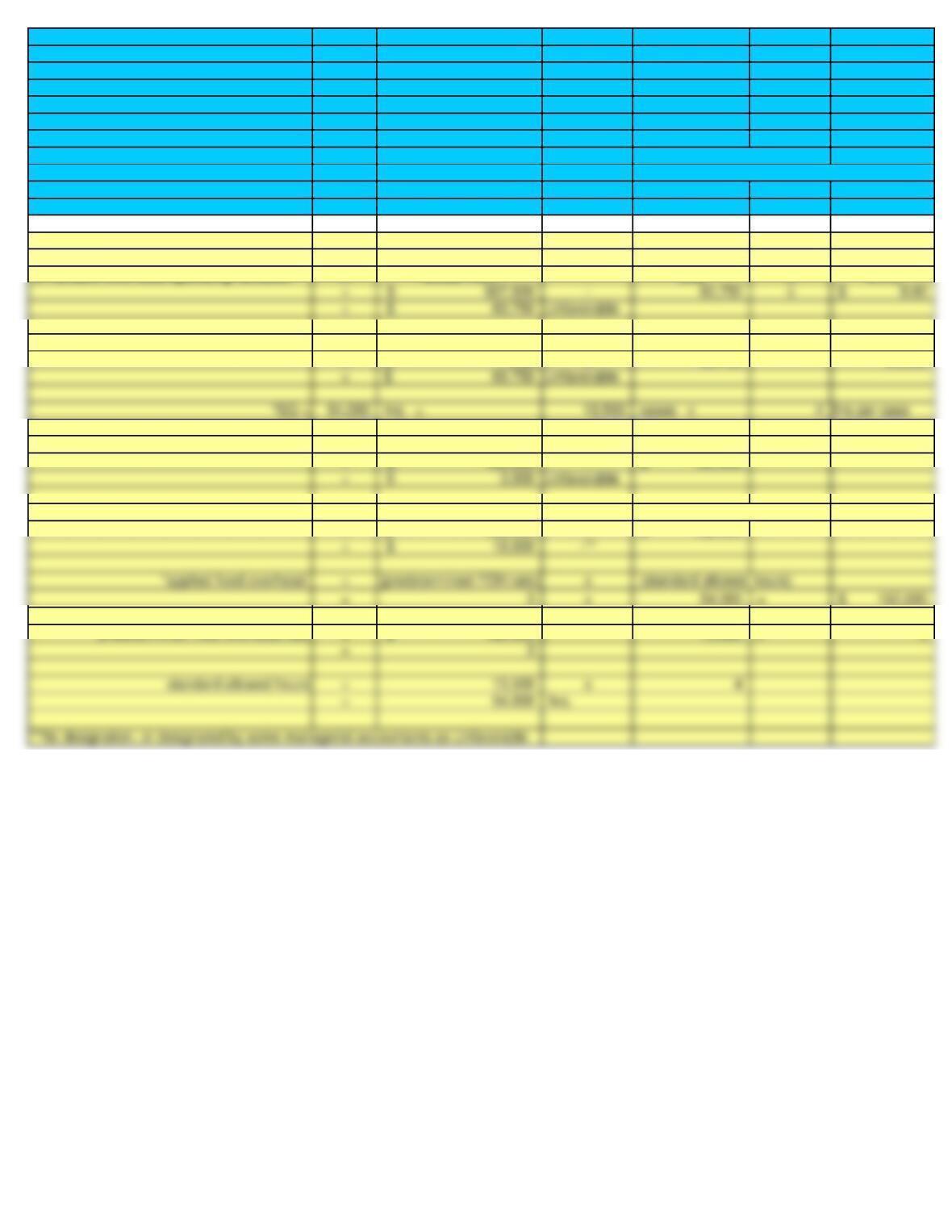

DATA INPUT

Actual output 13,500 cases

Actual variable overhead (Actual VOH) 607,500$

Actual fixed overhead (actual FOH) 183,000$

Actual machine time 60,750 machine hours

Standard variable-overhead rate 9.00$ per machine hour

Standard quantity of machine hours 4 hours per case of marshmallows

Budgeted fixed overhead (budgeted FOH) 180,000$ per month

Budgeted output 15,000 cases per month

SOLUTION

1) Variable-overhead spending variance = actual VOH – (AQ x SVR)

2) Variable-overhead efficiency variance = SVR x (AQ – SQ*)

= 9.00$ x 60,750 – 54,000

3) Fixed-overhead budget variance = actual FOH – budgeted FOH

= 183,000$ – 180,000$

4) Fixed-overhead volume variance = budgeted FOH – applied fixed overhead*

= 180,000$ – 162,000$

predetermined fixed overhead rate = 180,000$ / 15,000 x 4

= 607,500$ – 60,750 x 9.00$