331

CHAPTER 11

COST-VOLUME-PROFIT ANALYSIS

CLASS DISCUSSION QUESTIONS

1. Total variable costs vary in direct proportion

to changes in the level of activity. Unit varia-

ble costs remain the same with changes in

4. a. Fixed costs

b. Fixed costs

c. Fixed costs

5. Mixed costs are separated into their fixed

and variable cost components.

at that level to determine the total fixed cost.

10. a. No impact on the contribution margin.

b. Operating income would decrease.

11. A high contribution margin ratio, coupled

with idle capacity, indicates a potential for

increased operating income if additional sales

can be made. A large percentage of each

advantage of the low ratio of variable costs

to sales.

12. Decreases in unit variable costs, such as a

point for Gouda Company.

15. CVP analysis depends on five primary as-

sumptions. They are (1) total sales and total

costs can be represented by straight lines;

(2) within the relevant range of operating

activity, the efficiency of operations does not

sales mix percentages.

17. Operating leverage measures the relative

mix of a business’s variable costs and fixed

costs. Operating leverage measures the re-

lationship of a company’s contribution mar-

gin to operating income. It is computed as

332

EXERCISES

E11–1

1. Fixed

2. Variable

3. Variable

9. Fixed

10. Mixed

11. Variable

E11–2

a. Graph Two

d. Graph One

E11–3

1. a

2. b

333

E11–4

1. g

*(f) is better than (b) because the administrative costs would be the same

for expensive and inexpensive cars.

E11–5

a. Variable

b. Variable

c. Variable

g. Fixed

h. Fixed*

i. Fixed

334

E11–6

Components produced …… 250,000 375,000 500,000

Total costs:

Total variable costs ……. $300,000 (d) $450,000 (j) $600,000

Total fixed costs ………… 300,000 (e) 300,000 (k) 300,000

Total costs ………………… $600,000 (f) $750,000 (l) $900,000

Supporting calculations:

a. $1.20 ($300,000 ÷ 250,000 units)

b. $1.20 ($300,000 ÷ 250,000 units)

g. $1.20 ($450,000 ÷ 375,000 units; variable costs per unit do not change with

changes in volume)

h. $0.80 ($300,000 ÷ 375,000 units)

i. $2.00 ($1.20 + $0.80)

j. $600,000 ($1.20 × 500,000 units)

k. $300,000 (fixed costs do not change with volume)

335

E11–7

a. Variable Cost per Unit = Difference in Total Cost

Difference in Units Produced

The fixed cost can be determined by subtracting the estimated total variable

cost from the total cost at either the highest or lowest level of production, as

follows:

Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Cost

Highest level:

$4,300,000 = ($12.50 × 300,000 units) + Fixed Cost

b. Total Cost = (Variable Cost per Unit × Units Produced) + Fixed Cost

Total cost for 260,000 units:

Variable cost:

Units ……………………………………. 260,000

Variable cost per unit …………… × $12.50

336

E11–8

The fixed cost can be determined by subtracting the estimated total variable cost

from the total cost at either the highest or lowest level of gross-ton mile, as fol-

lows:

Total Cost = (Variable Cost per Gross-Ton Mile × Gross-Ton Miles) + Fixed Cost

Highest level:

$8,775,000 = ($1.15 × 4,500,000 gross-ton miles) + Fixed Cost

$8,775,000 = $5,175,000 + Fixed Cost

$3,600,000 = Fixed Cost

337

E11–9

b.

Sales ………………………………. $3,100,000

Contribution margin ratio … × 35%

Contribution margin ………… $1,085,000

Less fixed costs ……………… (675,000)

Operating income ……………. $ 410,000

E11–10

a.

Sales (in millions) …………………………………………………… $12,719

Variable costs (in millions):

338

E11–10, Concluded

c. Same-store sales increase (in millions) ………………….. $ 250

Contribution margin ratio [from part (b)] ………………… × 34.4%

Increase in operating income (in millions) ……………… $ 86

d. Operating income $1,326 million ($1,240 million + $86 million)

E11–11

a. Break-Even Sales (units) = Margin onContributiUnit

Costs Fixed

=

$930,000

$63 – $53 = 93,000 units

339

E11–12

a. Break-Even Sales (units) = Margin onContributiUnit

Costs Fixed

*Rounded 160,229,545.46 barrels up to next barrel so that break-even will be

achieved.

The variable costs per unit are determined by multiplying the total amount of

each cost by the variable cost percentage (75% for cost of goods sold and

35% for selling, general and administrative costs), then dividing by the

number of barrels.

E11–13

a. Break-Even Sales (units) = arginM onContributiUnit

Costs Fixed

=

$405,000

$675 – $450 = 1,800 units

340

E11–14

Break-Even Sales (units) = arginM onContributiUnit

Costs Fixed

=

$40,000

$40 – $X = 8,000 cookbooks

E11–15

The cost of the promotion campaign is the fixed cost in this analysis since we

want to determine the break-even adoption rate of the campaign.

Promotional cost = $20,900,000

Note: The variable cost is for 18 months since the costs are incurred even for the

2 free months.

The break-even number of subscribers necessary to cover the fixed cost of the

promotion would be computed as follows:

341

E11–16

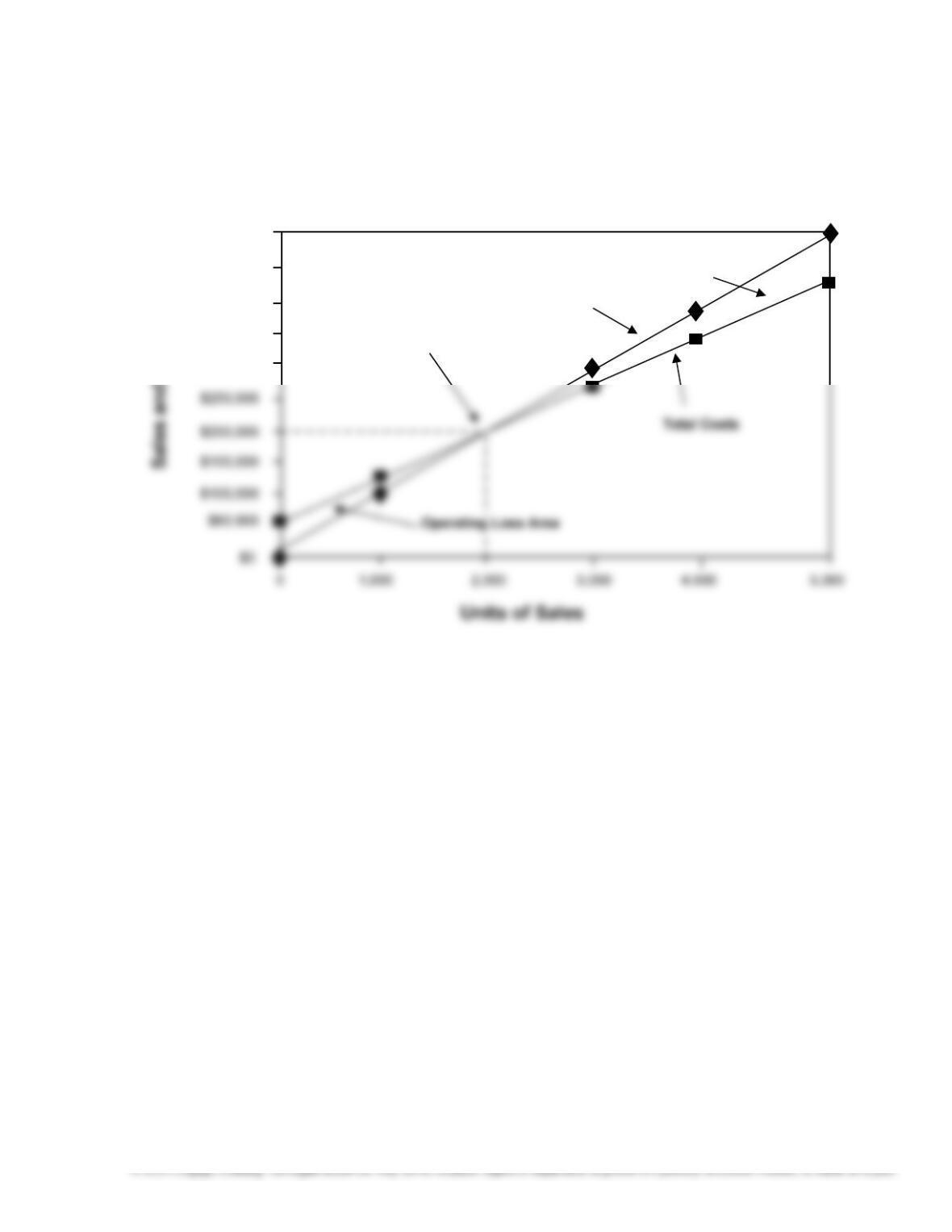

a.

b. $200,000 (the intersection of the total sales line and the total costs line)

c. The graphic format permits the user (management) to visually determine the

break-even point and the operating profit or loss for any given level of sales.

$500,000

$450,000

$400,000

$350,000

$300,000

Break-Even

Point

Total

Sales

Operating

Profit Area

342

E11–17

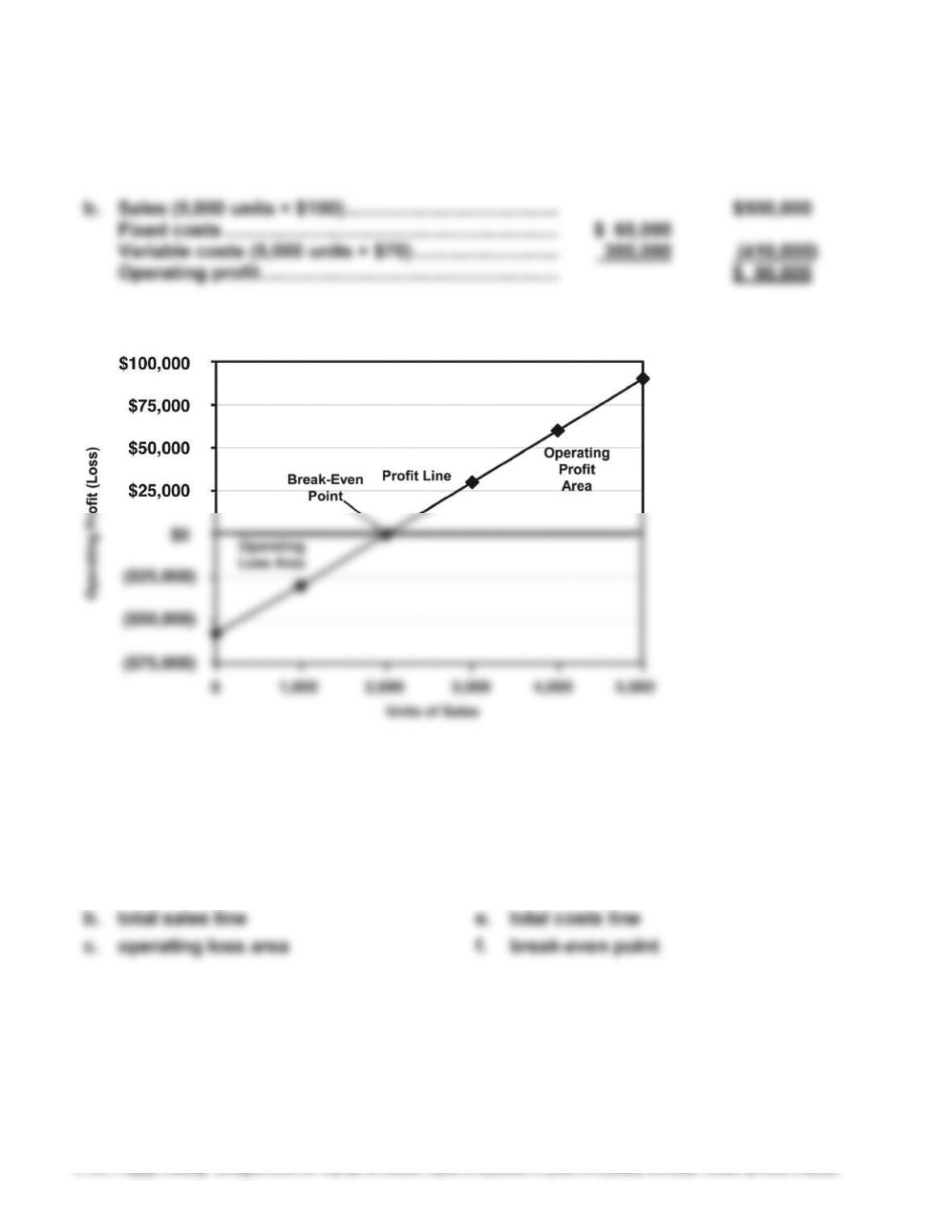

a. $60,000 (total fixed costs)

c.

d. 2,000 units (the intersection of the profit line and the horizontal axis)

E11–18

Cost-volume-profit graph

a. fixed costs

d. operating profit area

343

E11–19

Profit-volume graph

a. fixed costs or maximum operating loss

b. operating profit area

E11–20

a. Unit Selling Price of E = ($50 × 70%) + ($120 × 30%)

= $35 + $36 = $71

Unit Variable Cost of E = ($30 × 70%) + ($80 × 30%)

= $21 + $24 = $45

344

E11–21

a. Unit contribution margin of overall product (E):

Unit selling price of E [(10% × $750) + (90% × $300)] ………………….. $345

Unit variable cost of E [(10% × $50) + (90% × $20)] …………………….. 23

Unit contribution margin of E …………………………………………………… $322

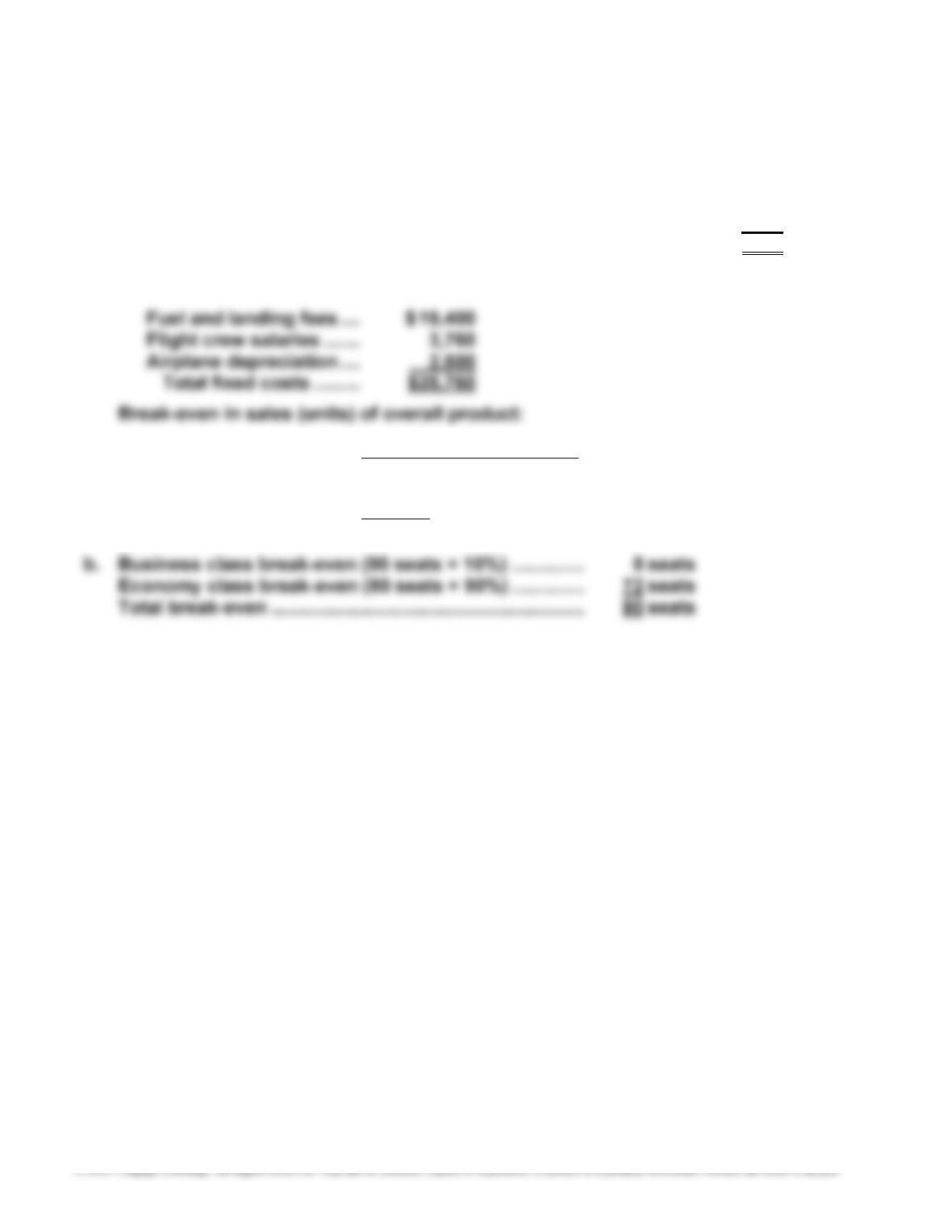

Fixed costs of the Portland to Minneapolis round-trip flight:

Break-Even Sales (units) = Margin onContributiUnit

Costs Fixed

=

322$

760,25$ = 80 seats (tickets)

345

E11–22

a. SunRise Inc.:

Operating Leverage =

Contribution Margin

Operating Income

=

$1,250,000

$500,000 = 2.5

b. SunRise Inc.’s operating income would increase by 62.5% (2.5 × 25%), or

$312,500 (62.5% × $500,000), and SunSet Inc.’s operating income would

increase by 85% (3.4 × 25%), or $850,000 (85% × $1,000,000).

346

P11–1

Fixed Variable Mixed

Cost Cost Cost Cost

a. X

g. X

h. X

i. X

j. X

k. X

l. X

r. X

s. X

t. X

347

P11–2

1. Fixed Costs Variable Costs

Cost of goods sold ………………………………….. $12,460,000 $ 32,040,000

Selling expenses …………………………………….. 2,000,000 6,000,000

Administrative expenses …………………………. 2,400,000 600,000

Total ……………………………………………………….. $ 16,860,000 $ 38,640,000

4. Break-Even Sales (units) = arginMnontributioCUnit

CostsFixed

=

150$

000,600,3$+000,860,16$

=

150$

000,460,20$ = 136,400 units

7. Present operating income ………………………………… $ 43,140,000

Less additional fixed costs ………………………………. (3,600,000)

Operating income …………………………………………….. $ 39,540,000