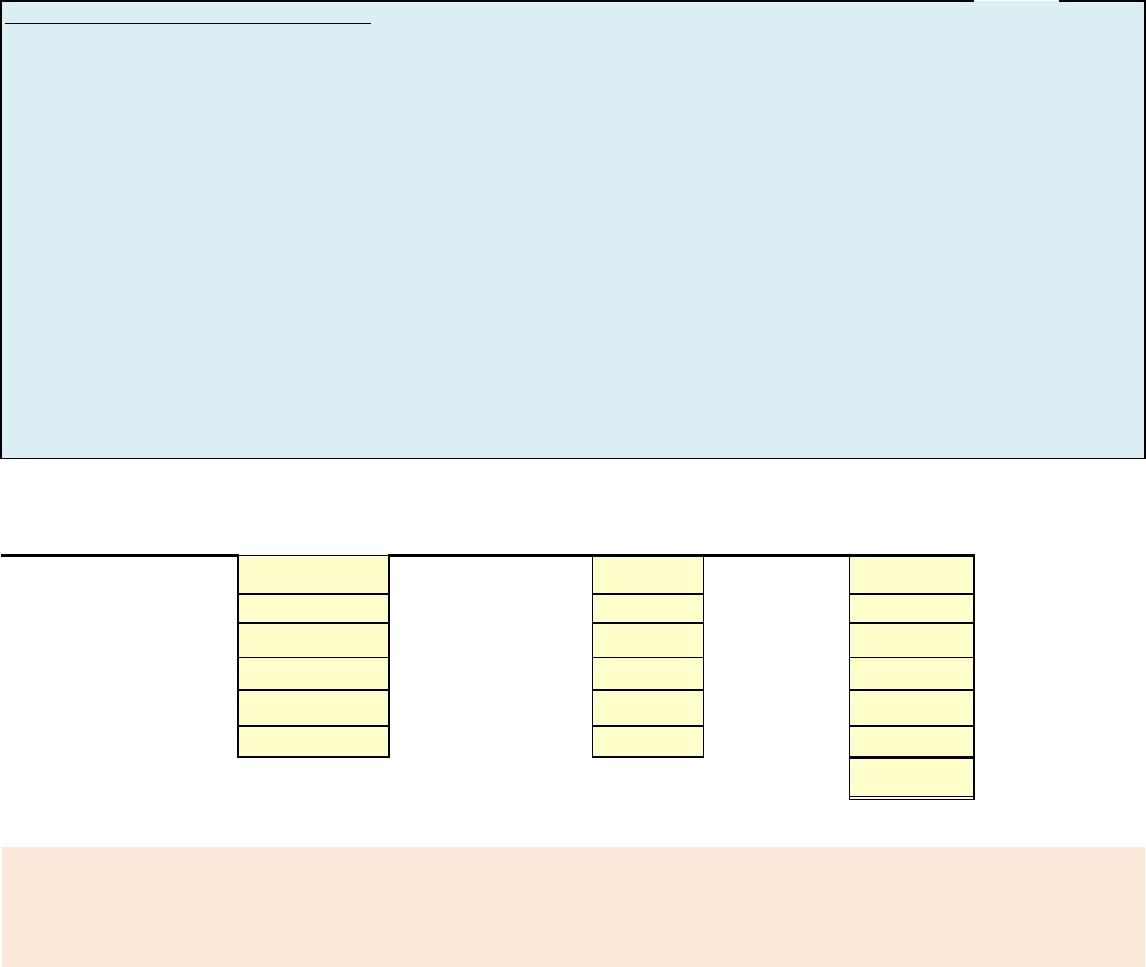

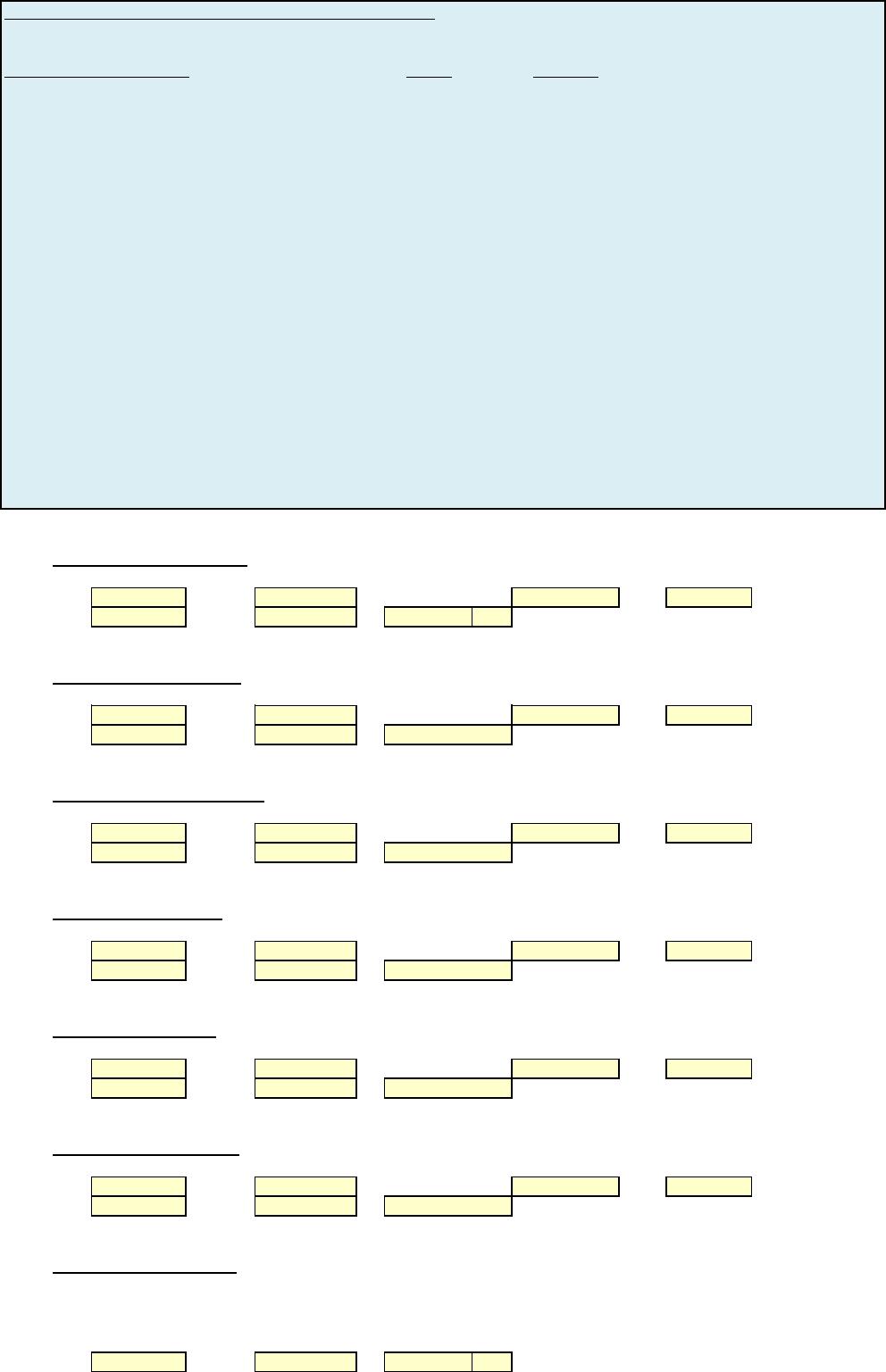

E11-2 Compute standard materials costs

Hank Itzek manufactures and sells homemade wine, and he wants to develop a standard cost

per gallon. The following are required for production of a 50-gallon batch.

3,000 ounces of grape concentrate at $0.06 per ounce

54 pounds of granulated sugar at $0.30 per pound

60 lemons at $0.60 each

50 yeast tablets at $0.25 each

50 nutrient tablets at $0.20 each

2,600 ounces of water at $0.005 per ounce

Hank estimates that 4% of the grape concentrate is wasted, 10% of the sugar is lost, and 25%

of the lemons cannot be used.

Instructions

Compute the standard cost of the ingredients for one gallon of wine. (Carry computations to

two decimal places.)

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

Amount per Standard Standard Standard Standard Cost

gallon Waste Usage Price per Gallon

Grape concentrate Value oz. 4% ?$0.06 ?

Sugar Value lb. 10% ?0.30 ?

Lemons Value lemons 25% ?0.60 ?

Yeast Value tablet 0% ?0.25 ?

Nutrient Value tablet 0% ?0.20 ?

Water Value oz. 0% ?0.005 ?

Standard cost for one gallon of wine

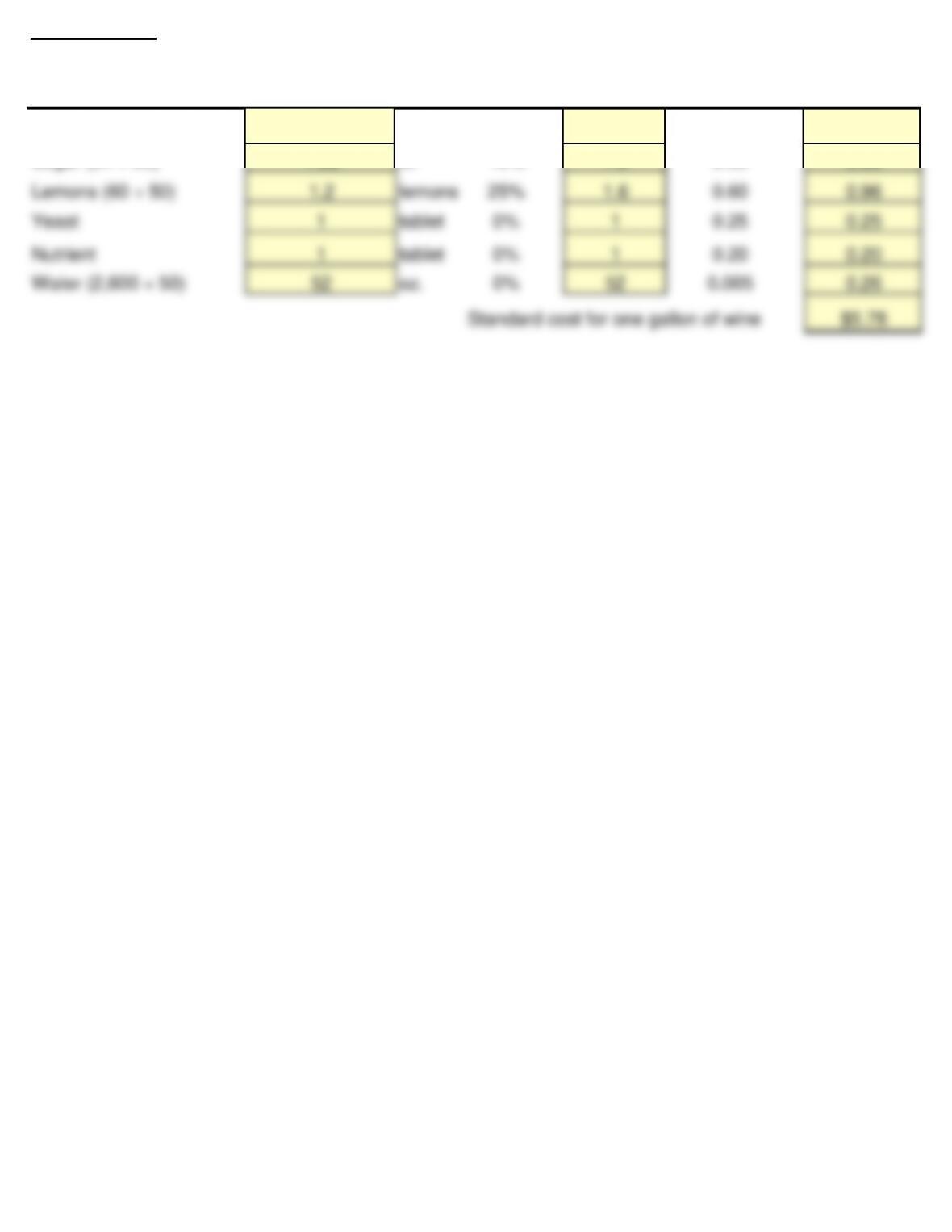

After you have completed the requirements of E11-2, consider this additional question.

1. Assume the standard waste for grape concentrate, sugar and lemons changed to 5%, 8% and 20% respectively.

How will these changes impact the standard cost of one gallon of wine?

Ingredient

E11-2 Solution

Amount per Standard Standard Standard Standard Cost

gallon Waste Usage Price per Gallon

Grape concentrate 60 oz. 4% 62.5 $0.06 $3.75

Sugar (54 ÷ 50) 1.08 lb. 10% 1.2 0.30 0.36

Ingredient

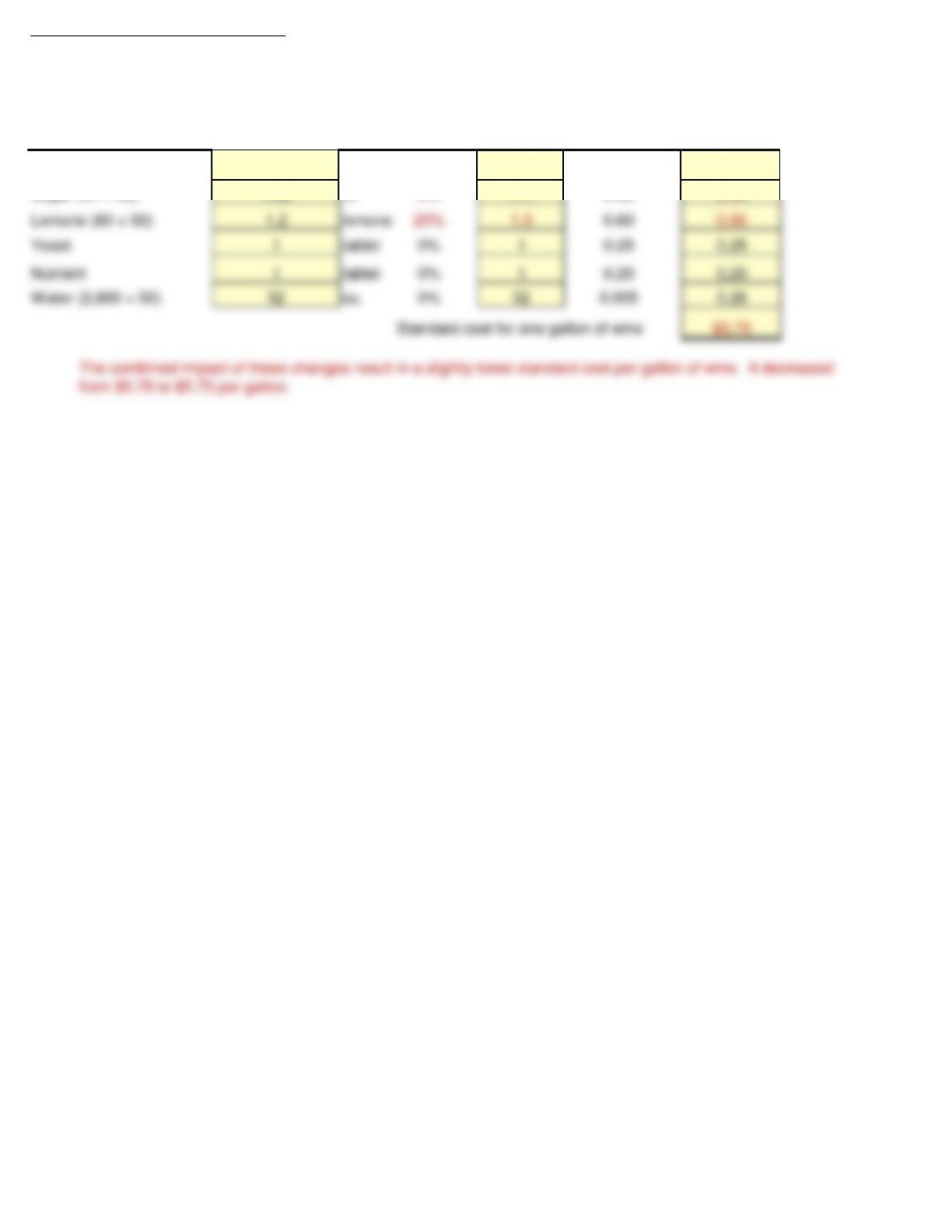

E11-2 Solution to additional question

1. Assume the standard waste for grape concentrate, sugar and lemons changed to 5%, 8% and 20% respectively.

How will these changes impact the standard cost of one gallon of wine?

Amount per

Standard

Standard Standard Standard Cost

gallon Waste Usage Price per Gallon

Grape concentrate 60 oz. 5% 63.16 $0.06 $3.79

Sugar (54 ÷ 50) 1.08 lb. 8% 1.17 0.30 0.35

Ingredient

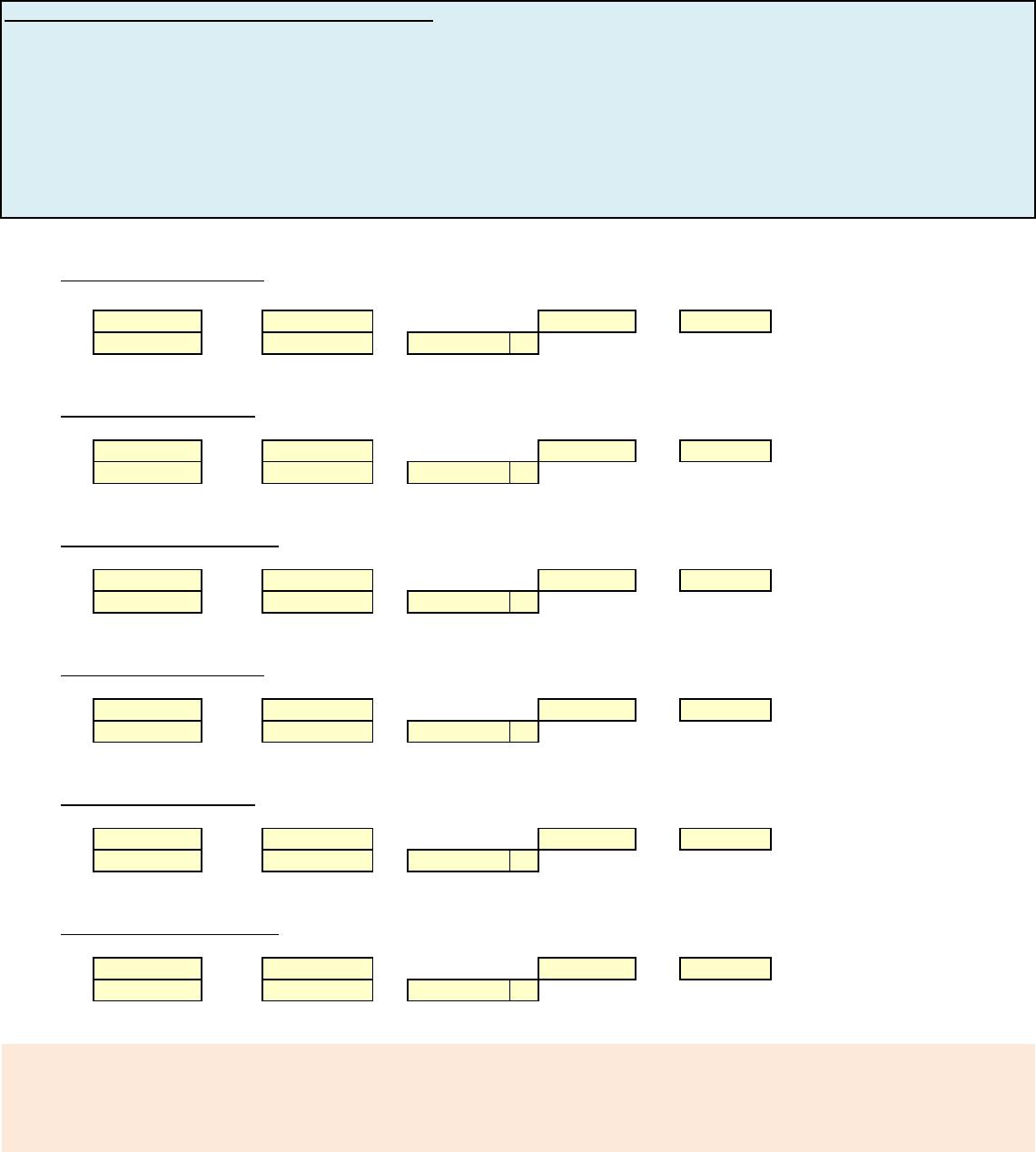

E11-5 Compute materials price and quantity variance

The standard cost of Product B manufactured by Pharrell Company includes three units of direct materials at

$5.00 per unit. During June, 29,000 units of direct materials are purchased at a cost of $4.70 per unit, and

29,000 units of direct materials are used to produce 9,400 units of Product B.

Instructions

(a) Compute the total materials variance and the price and quantity variances.

(b) Repeat (a), assuming the purchase price is $5.15 and the quantity purchased and used is 28,000 units

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

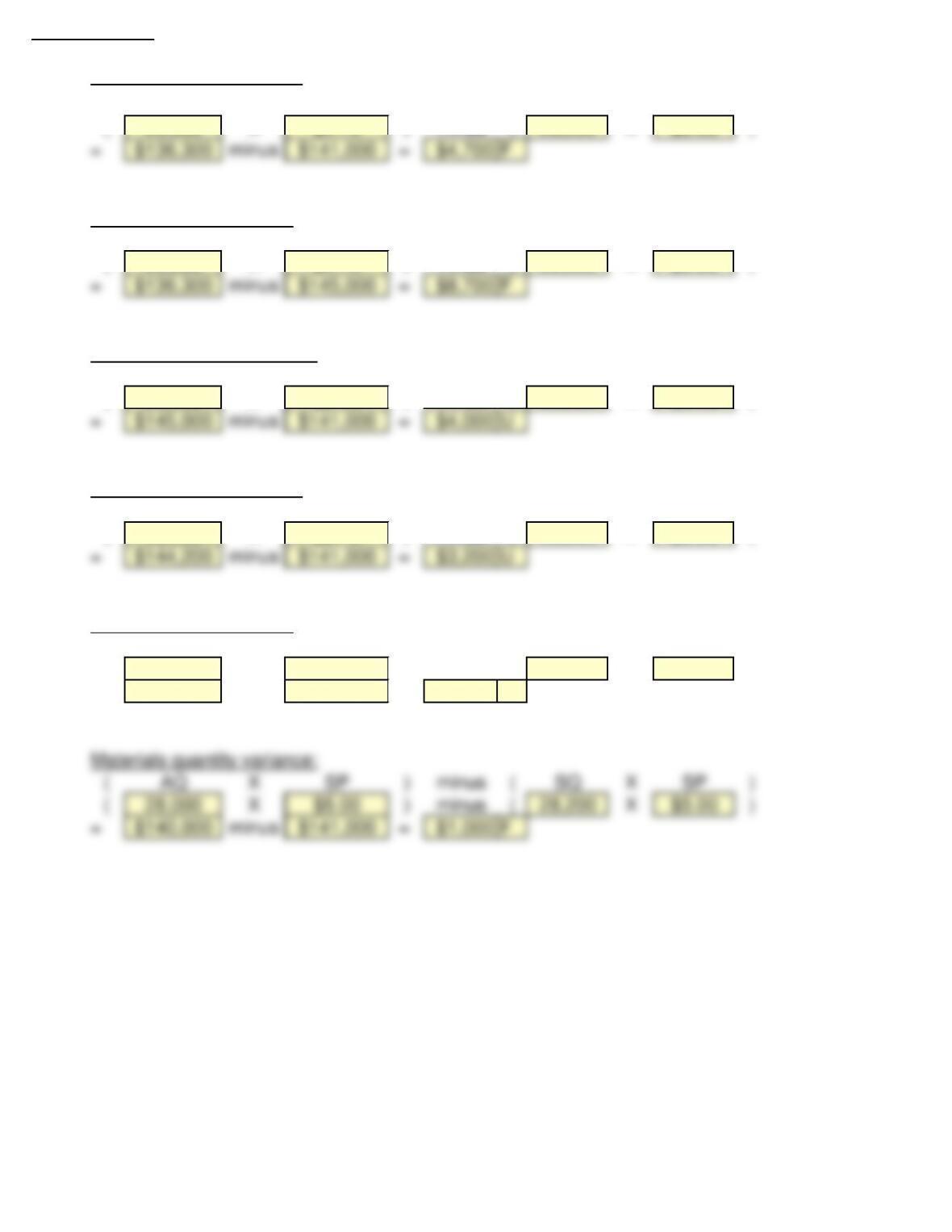

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

(b) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

After you have completed the requirements of E11-5, consider this additional question.

1. Assume in part (a) that the purchase price of direct materials changed to $4.80 and the quantity purchased

and used also changed to 30,000 units. Recalculate total materials variance and price and quantity variances.

E11-5 Solution

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP )

( 29,000 X $4.70 ) minus ( 28,200 X $5.00 )

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( 29,000 X $4.70 ) minus ( 29,000 X $5.00 )

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( 29,000 X $5.00 ) minus ( 28,200 X $5.00 )

(b) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP )

( 28,000 X $5.15 ) minus ( 28,200 X $5.00 )

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( 28,000 X $5.15 ) minus ( 28,000 X $5.00 )

= $144,200 minus $140,000 = $4,200 U

E11-5 Solution to additional question

1. Assume in part (a) that the purchase price of direct materials changed to $4.80 and the quantity purchased

and used also changed to 30,000 units. Recalculate total materials variance and price and quantity variances.

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP )

(30,000 X$4.80 ) minus ( 28,200 X $5.00 )

=$144,000 minus $141,000 = $3,000 U

E11-7 Compute materials and labor variances

Levine Inc. which produces a single product, has prepared the following standard cost sheet

for one unit of the product.

Direct materials (8 pounds at $2.50 per pound) $20

Direct labor (3 hours at $12 per hour) $36

During the month of April, the company manufactures 230 units and incurs the following

actual costs.

Direct materials purchased and used (1,900 pounds)

$5,035

Direct labor (700 hours) $8,120

Instructions

Compute the total, price, and quantity variances for materials and labor.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

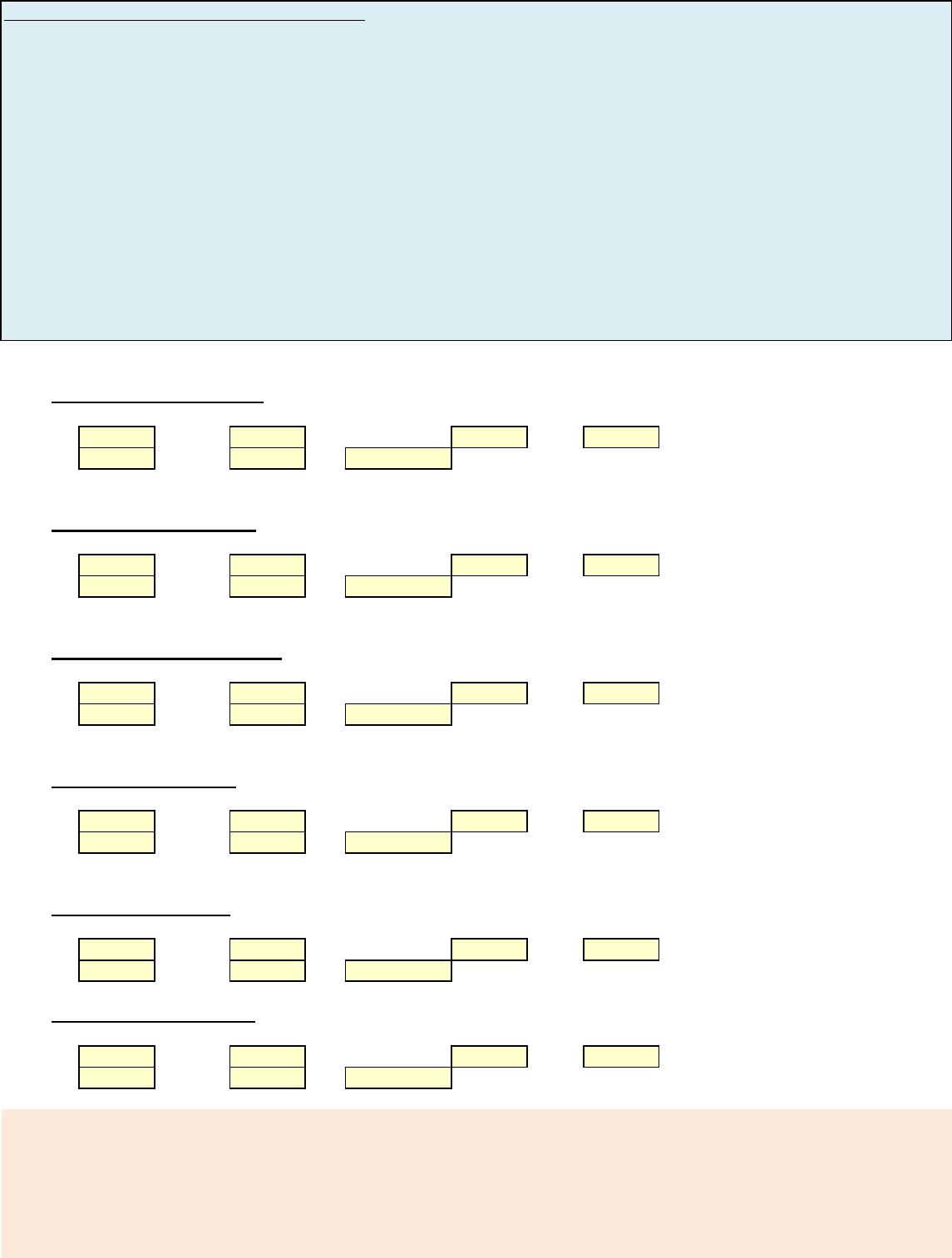

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

(b) Total Labor Variance:

(AH XAR ) minus ( SH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Labor Price variance:

(AH XAR ) minus ( AH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Labor quantity variance:

(AH XSR ) minus ( SH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

After you have completed the requirements of E11-7, consider this additional question.

1. Assume that the actual quantity and price paid for direct material and labor changed to the following:

Direct materials purchased and used (2,000 pounds)

Direct labor (720 hours)

Recalculate total variance, price and quantity variances for both direct materials and labor.

Value

Value

Value

Value

Value

Value

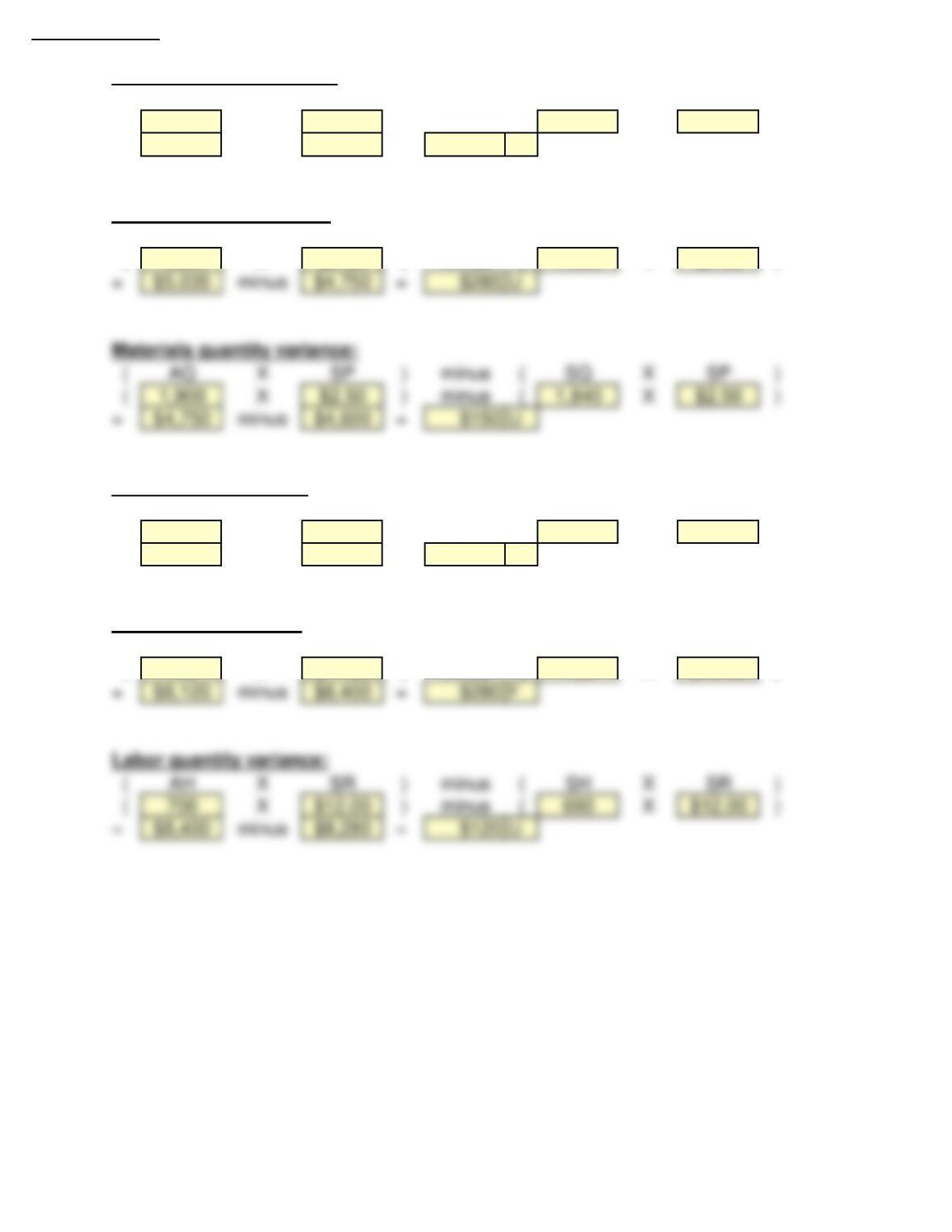

E11-7 Solution

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

( 1,900 X $2.65 ) minus ( 1,840 X $2.50 )

=$5,035 minus $4,600 = $435 U

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( 1,900 X $2.65 ) minus ( 1,900 X $2.50 )

(b) Total Labor Variance:

(AH XAR ) minus ( SH XSR )

(700 X $11.60 ) minus ( 690 X $12.00 )

= $8,120 minus $8,280 = $160 F

Labor Price variance:

(AH XAR ) minus ( AH XSR )

(700 X $11.60 ) minus ( 700 X $12.00 )

E11-7 Solution to additional question

1. Assume that the actual quantity and price paid for direct material and labor changed to the following:

Direct materials purchased and used (2,000 pounds)

Direct labor (720 hours)

Recalculate total variance, price and quantity variances for both direct materials and labor.

(a) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

(b) Total Labor Variance:

(AH XAR ) minus ( SH XSR )

(720 X$11.28 ) minus ( 690 X$12.00 )

=$8,120 minus $8,280 = $160 F

Labor Price variance:

P11-2A Compute variances, and prepare income statement

Ayala Corporation accumulates the following data relative to jobs started and finished during the month of June 2017.

Actual Standard

Raw materials unit cost $2.25 $2.10

Raw materials units used

10,600 10,000

Direct labor payroll $120,960 $120,000

Direct labor hours worked 14,400 15,000

Manufacturing overhead incurred $189,500

Manufacturing overhead applied $189,000

Machine hours expected to be used at normal capacity 42,500

Budgeted fixed overhead for June $55,250

Variable overhead rate per machine hour $3.00

Fixed overhead rate per machine hour $1.30

Overhead is applied on the basis of standard machine hours. Three hours of machine time are

required for each direct labor hour. The jobs were sold for $400,000. Selling and administrative

expenses were $40,000. Assume that the amount of raw materials purchased equaled the amount

used.

Instructions

(a) Compute all of the variances for (1) direct materials and (2) direct labor.

(b) Compute the total overhead variance.

(c) Prepare an income statement for management. (Ignore income taxes.)

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

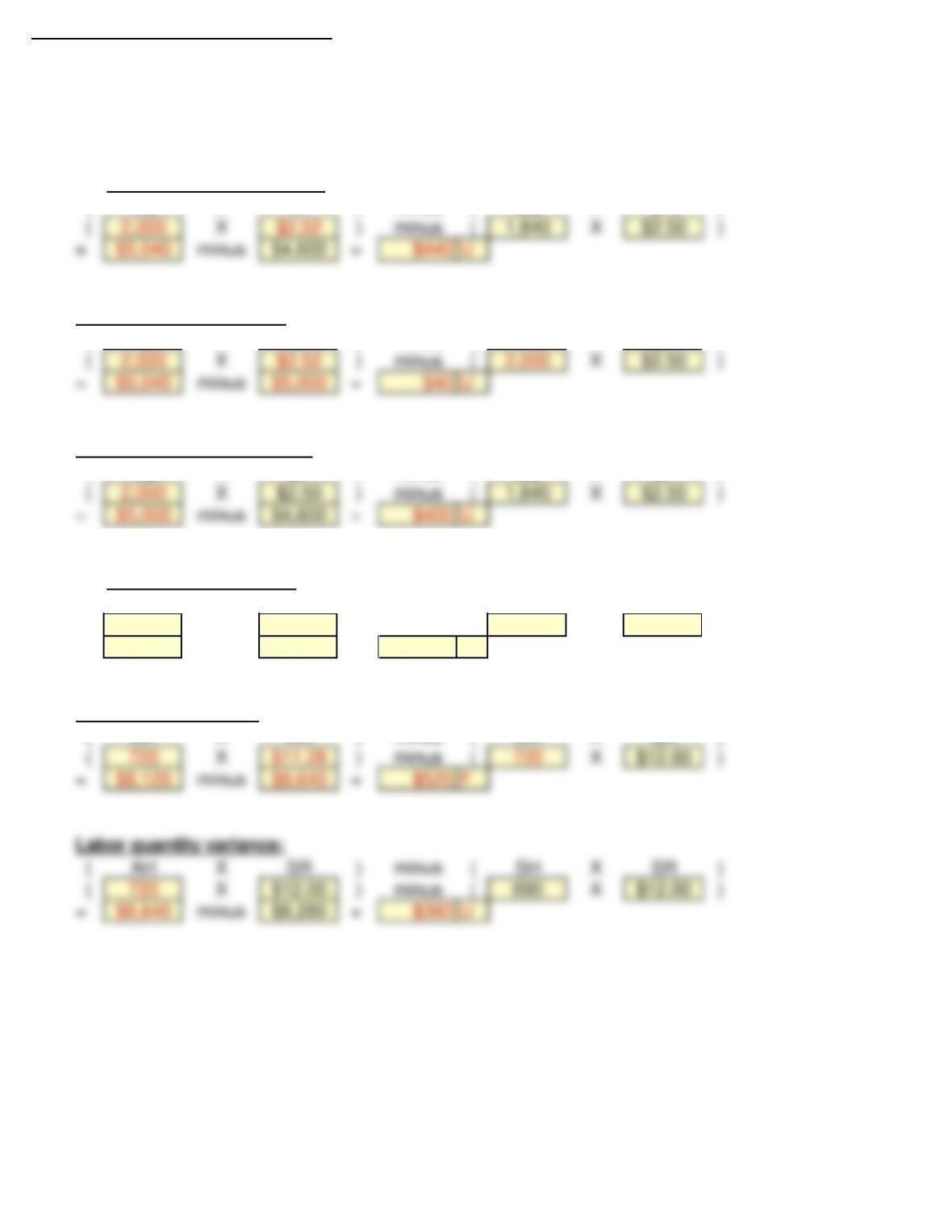

(a)(1)

Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

( Value X Value ) minus ( Value X Value )

= ? minus ? = Value

Materials price variance:

(AQ XAP ) minus ( AQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

(a)(2)

Total Labor Variance:

(AH XAR ) minus ( SH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Labor Price variance:

(AH XAR ) minus ( AH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

Labor quantity variance:

(AH XSR ) minus ( SH XSR )

( Value X Value ) minus ( Value X Value )

= ? minus ? =

(b) Total Overhead Variance:

= Actual minus Overhead

Overhead Applied

= Value minus Value = Value

Value

Cost and Production Data

Value

Value

Value

Value

(c )

Sales revenue Value

Cost of goods sold (at standard) ?

Gross profit (at standard) ?

Variances

Material price Value

Materials quantity Value

Labor price Value

Labor quantity Value

Overhead Value

Total variance – favorable ?

Gross profit (actual) ?

Selling and administrative expenses Value

Net income ?

After you have completed the requirements of P11-2A, consider this additional questions.

1. Assume that the actual price for raw materials changed to $2.30 and actual quantity of raw materials used changed to 11,000 units.

Recompute total materials variance and price and quantity variances for materials.

2. Show the impact of the changes above on the income statement.

AYALA CORPORATION

Income Statement

For the Month Ended June 30, 2017

P11-2A Solution

(a)(1) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

( 10,600 X $2.25 ) minus ( 10,000 X $2.10 )

= $23,850 minus $21,000 = $2,850 U

Materials price variance:

Materials quantity variance:

(AQ XSP ) minus ( SQ XSP )

( 10,600 X $2.10 ) minus ( 10,000 X $2.10 )

= $22,260 minus $21,000 = $1,260 U

(a)(2) Total Labor Variance:

Labor Price variance:

(AH XAR ) minus ( AH XSR )

( 14,400 X $8.40 ) minus ( 14,400 X $8.00 )

= $120,960 minus $115,200 = $5,760 U

Labor quantity variance:

(b) Total Overhead Variance:

= Actual minus Overhead

Overhead Applied

(c )

Sales revenue $400,000

AYALA CORPORATION

Income Statement

For the Month Ended June 30, 2017

Material price $1,590 U

Materials quantity 1,260 U

P11-2A Solution to additional questions

1. Assume that the actual price for raw materials changed to $2.30 and actual quantity of raw materials used changed to 11,000 units.

Recompute total materials variance and price and quantity variances for materials.

2. Show the impact of the changes above on the income statement.

(a)(1) Total Materials Variance:

(AQ XAP ) minus ( SQ XSP) )

(11,000 X$2.30 ) minus ( 10,000 X $2.10 )

=$25,300 minus $21,000 = $4,300 U

(a)(2) Total Labor Variance:

(AH XAR ) minus ( SH XSR )

( 14,400 X $8.40 ) minus ( 15,000 X $8.00 )

= $120,960 minus $120,000 = $960 U

Labor quantity variance:

(AH XSR ) minus ( SH XSR )

( 14,400 X $8.00 ) minus ( 15,000 X $8.00 )

= $115,200 minus $120,000 = $4,800 F

(b) Total Overhead Variance:

(c )

Sales revenue $400,000

Cost of goods sold (at standard) 334,500

Gross profit (at standard) 65,500

Variances

Material price $2,200 U

Materials quantity 2,100 U

AYALA CORPORATION

Income Statement

For the Month Ended June 30, 2017

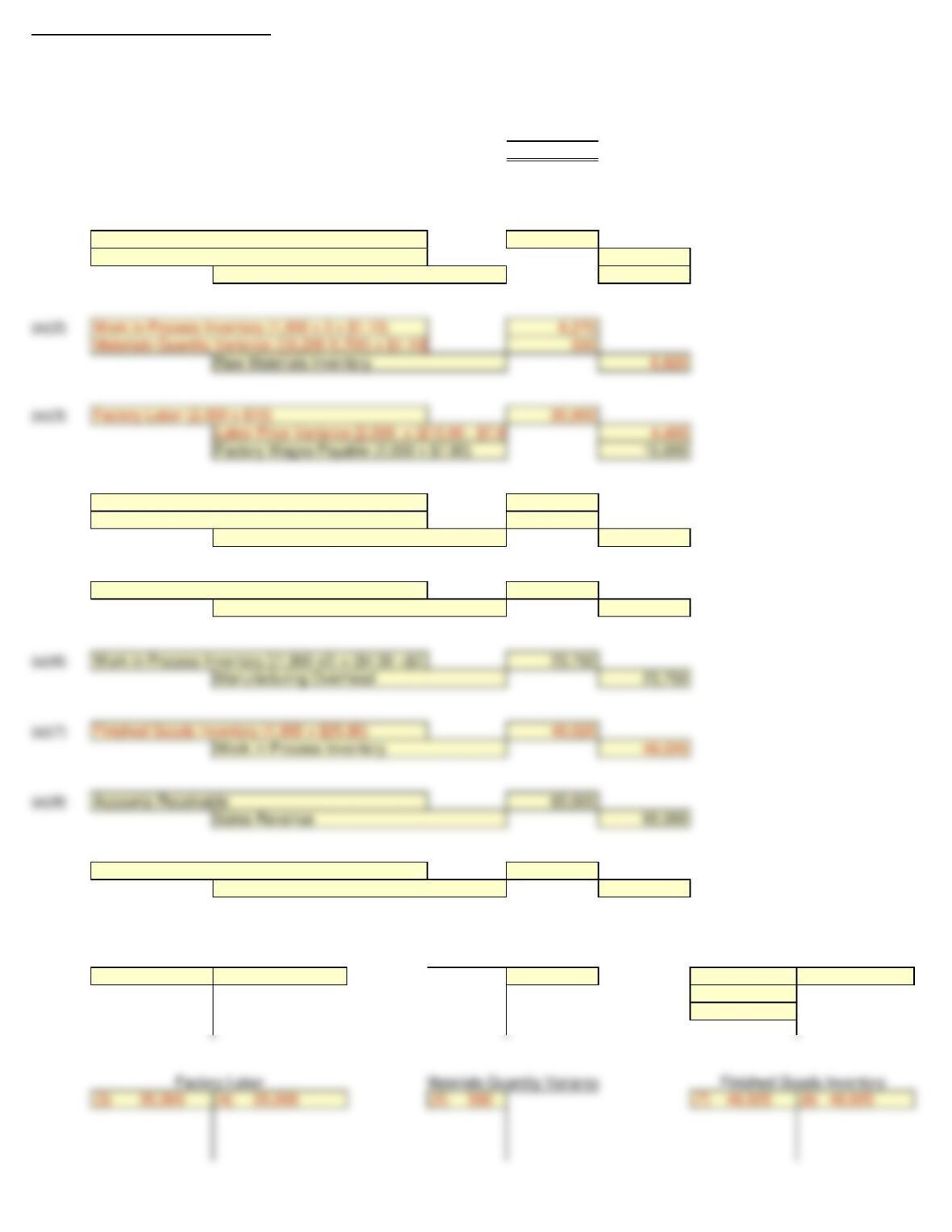

P11-6A Journalize and post standard cost entries, and prepare income statement

Jorgensen Corporation uses standard costs with its job order cost accounting system.

In January, an order (Job No. 12) for 1,900 units of Product B was received. The standard

cost of one unit of Product B is as follows.

Direct materials 3 pounds at $1.00 per pound $3.00

Direct labor 1 hour at $8.00 per hour 8.00

Overhead 2 hours (variable $4.00 per machine hour;

fixed $2.25 per machine hour)

12.50

Standard cost per unit $23.50

Normal capacity for the month was 4,200 machine hours. During January, the following

transactions applicable to Job No. 12 occurred.

1. Purchased 6,200 pounds of raw materials on account at $1.05 per pound.

2. Requisitioned 6,200 pounds of raw materials for Job No. 12.

3. Incurred 2,000 hours of direct labor at a rate of $7.80 per hour.

4. Worked 2,000 hours of direct labor on Job No.12.

5. Incurred manufacturing overhead on account $25,000.

6. Applied overhead to Job No. 12 on basis of standard machine hour allowed.

7. Completed Job No. 12.

8. Billed customer for Job No. 12 at a selling price of $65,000.

Instructions

(a) Journalize the transactions.

(b) Post to the job order cost accounts.

(c ) Prepare the entry to recognize the total overhead variance.

(d) Prepare the January 2017 income statement for management. Assume selling and

administrative expenses were $2,000.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a)(1) Value

Value Value

(a)(2) Value

Value Value

(a)(3) Value Value

Value

(a)(4) Value

Value Value

(a)(5) Value Value

(a)(6) Value Value

(a)(7) Value Value

(a)(8) Value Value

Value

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Account

Value

(b) Value Value Value Value Value

Value

Value

Value Value Value Value Value

Value Value Value Value

Value

(c ) Value Value

(d)

Sales revenue Value

Cost of goods sold (at standard) Value

Gross profit (at standard) ?

Variances

Material price Value

Materials quantity Value

Labor price Value

Labor quantity Value

Overhead Value

Total variance – unfavorable ?

Gross profit (actual) ?

Selling and administrative expenses Value

Net income ?

After you have completed the requirements of P11-6A, consider this additional question.

1. Assume that the standard costs changed as follows:

Direct materials 3 pounds at $1.10 per pound $3.30

Direct labor 1 hour at $10.00 per hour 10.00

Overhead 2 hours (variable $4.00 per machine hour;

fixed $2.25 per machine hour)

12.50

Standard cost per unit $25.80

Revise journals entries to reflect these changes and show posting to job order T-accounts.

Account

For the Month Ended January 31, 2017

Work in Process Inventory

Factory Labor

Materials Quantity Variance

Finished Goods Inventory

Manufacturing Overhead

Labor Price Variance

Cost of Goods Sold

Raw Materials Inventory

Materials Price Variance

Labor Quantity Variance

Account

Account

JORGENSEN CORPORATION

Income Statement

Work in Process Inventory

Finished Goods Inventory (1,900 x $23.50)

Accounts Receivable

Sales Revenue

Cost of Goods Sold

Finished Goods Inventory

P11-6 Solution

(a)(1) 6,200

310 6,510

(a)(4) 15,200

800 16,000

(a)(5) 25,000 25,000

(a)(6) 23,750 23,750

(b) (1) 6,200 (2) 6,200 (1) 310 (2) 5,700 (7) 44,650

(4) 15,200

(6) 23,750

(3) 16,000 (4) 16,000 (2) 500 (7) 44,650 (8) 44,650

(5) 25,000 (6) 23,750 (3) 400 (8) 44,650

(4) 800

Raw Materials Inventory (6,200 x $1.00)

Materials Price Variance[6,200 x ($1.05 – $1.00)]

Accounts Payable (6,200 x $1.05)

Work in Process Inventory (1,900 x $8.00)

Labor Quantity Variance [(2,000 – 1,900) x $8]

Factory Labor

Manufacturing Overhead

Accounts Payable

Work in Process Inventory [(1,900 x2) x ($4.00 +$2.25)]

Manufacturing Overhead

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory

Factory Labor

Materials Quantity Variance

Finished Goods Inventory

Manufacturing Overhead

Labor Price Variance

Cost of Goods Sold

Labor Quantity Variance

Raw Materials Inventory

Work in Process Inventory (1,900 x 3 x $1)

Materials Quantity Variance ([(6,200-5,700) x $1.00]

Factory Labor (2,000 x $8)

Labor Price Variance [2,000 x ($8.00 – $7.80)]

Factory Wages Payable (2,000 x $7.80)

(c ) 1,250 1,250

(d)

Sales revenue $65,000

Cost of goods sold (at standard) (1,900 x $23.50) 44,650

Gross profit (at standard) $20,350

Variances

Material price $310 U

For the Month Ended January 31, 2017

Overhead Variance ($25,000 – $23,750)

Manufacturing Overhead

JORGENSEN CORPORATION

Income Statement

Accounts Receivable

Sales Revenue

Work in Process Inventory

Work in Process Inventory [(1,900 x2) x ($4.00 +$2.25)]

Manufacturing Overhead

Finished Goods Inventory (1,900 x $25.80)

P11-6 Solution to additional question

1. Assume that the standard costs changed as follows:

Direct materials 3 pounds at $1.10 per pound $3.30

Direct labor 1 hour at $10.00 per hour 10.00

Overhead 2 hours (variable $4.00 per machine hour;

fixed $2.25 per machine hour) 12.50

Standard cost per unit $25.80

Revise journals entries to reflect these changes and show posting to job order T-accounts.

(a)(1) 6,820 310

6,510

(a)(4) 19,000

1,000 20,000

(a)(5) 25,000 25,000

49,020 49,020

(b) (1) 6,820 (2) 6,820 (1) 310 (2) 6,270 (7) 49,020

(4) 19,000

(6) 23,750

Work in Process Inventory

Cost of Goods Sold

Finished Goods Inventory

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory (1,900 x $10.00)

Labor Quantity Variance [(2,000 – 1,900) x $10]

Factory Labor

Manufacturing Overhead

Accounts Payable

Raw Materials Inventory (6,200 x $1.10)

Materials Price Variance[6,200 x ($1.05 – $1.10)]

Accounts Payable (6,200 x $1.05)

Factory Labor (2,000 x $10)

Labor Price Variance [2,000 x ($10.00 – $7.80)]

Factory Wages Payable (2,000 x $7.80)

Raw Materials Inventory

Work in Process Inventory (1,900 x 3 x $1.10)

Materials Quantity Variance ([(6,200-5,700) x $1.10]

(5) 25,000 (6) 23,750 (3) 4,400 (8) 49,020

(d)

Sales revenue $65,000

Cost of goods sold (at standard) (1,900 x $25.80) 49,020

Gross profit (at standard) $15,980

For the Month Ended January 31, 2017

Manufacturing Overhead

Labor Price Variance

Cost of Goods Sold

JORGENSEN CORPORATION

Income Statement

CD11 Current Designs

The executive team at Current Designs has gathered to evaluate the company‘s operations for the last month.

One of the topics on the agenda is the special order from Huegel Hollow, which was presented in CD2. Recall that

Current Designs had a special order to produce a batch of 20 kayaks for a client, and you were asked to determine

the cost of the order and the cost per kayak.

Mike Cichanowski asked the others if the special order caused any particular problems in the production process.

Dave Thill, the production manager, made the following comments: “Since we wanted to complete this order quickly

and make a good first impression on this new customer, we had some of our most experienced type I workers run the

rotomold oven and do the trimming. They were very efficient and were able to determine that part of the manufacturing

process even more quickly than the regular crew. However, the finishing on these kayaks required a different technique

than what we usually use, so our type II workers took a little longer than usual for that part of the process.”

Deb Welch, who is in charge of the purchasing function, said, “We had to pay a little more for the polyethylene

powder for this order because the customer wanted a color that we don‘t usually stock. We also ordered a little extra

since we wanted to make sure that we had enough to allow us to calibrate the equipment. The calibration was a little

tricky, and we used all of the powder that we had purchased. Since the number of kayaks in the order was fairly small,

we were able to use some rope and other parts that were left over from last year’s production in the finishing kits.

We’ve seen a price increase for these components in the last year, so using the parts that we already had in inventory

cut our costs for the finishing kits.”

Instructions

(a) Based on the comments above, predict whether each of the following variances will be favorable or unfavorable.

If you don’t have enough information to make a prediction, use “NEI” to indicate “Not Enough Information.”

(1) Quantity variance for polyethylene powder.

(2) Price variance for polyethylene powder.

(3) Quantity variance for finishing kits.

(4) Price variance for finishing kits

(5) Quantity variance for type I workers.

(6) Price variance for type I workers.

(7) Quantity variance for type II workers.

(8) Price variance for type II workers.

(b) Diane Buswell examined some of the accounting records and reported that Current Designs purchased 1,200 pounds

of powder for this order at a total cost of $2,040. Twenty (20) finishing kits were assembled at a total cost of $3,240.

The payroll records showed that the type I employees worked 38 hours on this project at a total cost of $570. The

type II finishing employees worked 65 hours at a total cost of $796.25. A total of 20 kayaks were produced for this

order.

The standards that had been developed for this model of kayak were used in CD2 and are reproduced here. For

each kayak:

54 pounds of polyethylene powder at $1.50 per pound

1 finishing kit (rope, seat, hardware, etc.) at $170

2 hours of type I labor from people who run the oven and trim the plastic at a standard wage rate of $15 per hour

3 hours of type II labor from people who attach the hatches and seat and other hardware at a standard wage rate

of $12 per hour

Calculate the eight variances that are listed in part (a) of this problem.

NOTE: Enter a number in cells requesting a value; enter either a number or a formula in cells with a “?” .

(a) Based on the comments above, predict whether each of the following variances will be favorable or unfavorable.

If you don’t have enough information to make a prediction, use “NEI” to indicate “Not Enough Information.”

(1) Quantity variance for polyethylene powder. Response

(2) Price variance for polyethylene powder. Response

(3) Quantity variance for finishing kits. Response

(4) Price variance for finishing kits Response

(5) Quantity variance for type I workers. Response

(6) Price variance for type I workers. Response

(7) Quantity variance for type II workers. Response

(8) Price variance for type II workers. Response

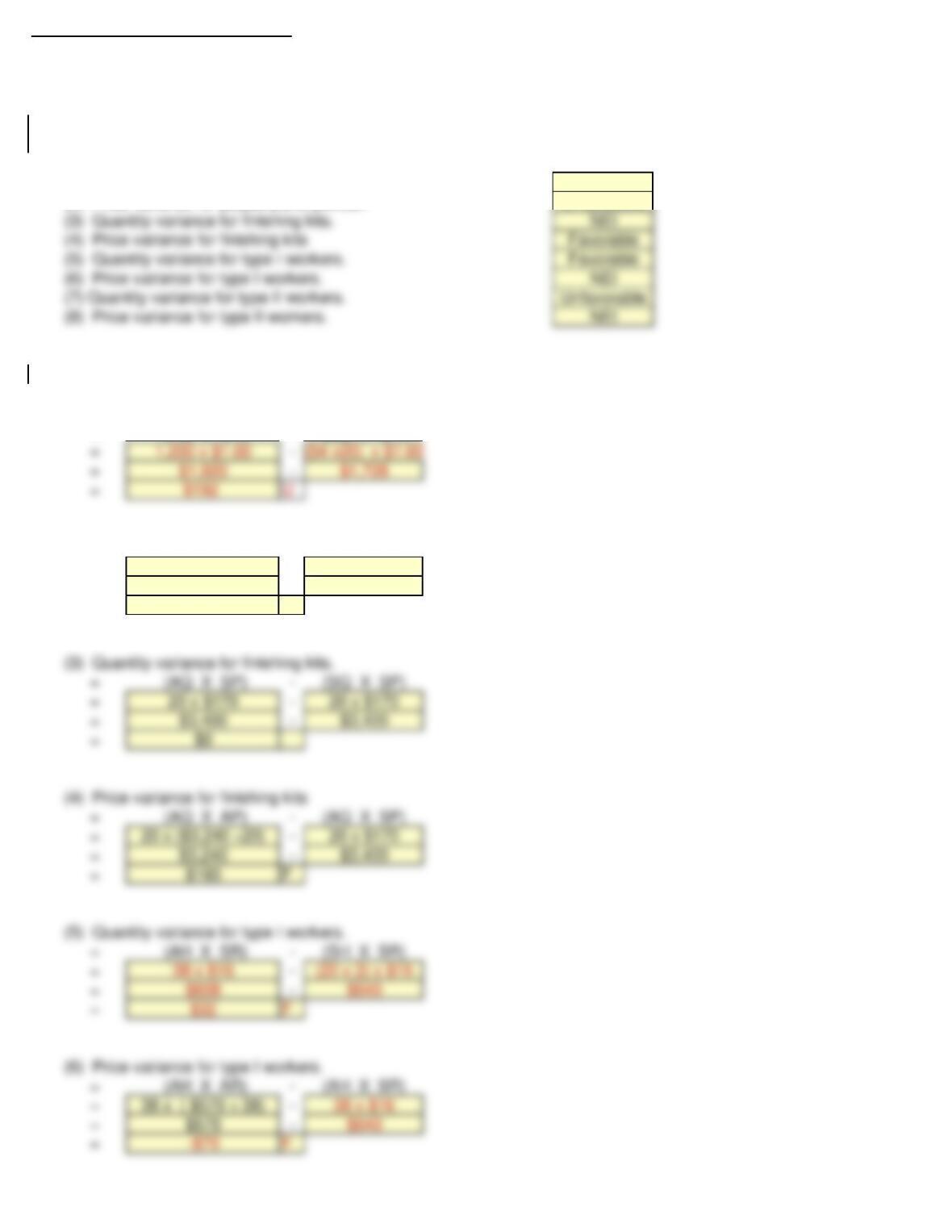

(b) Calculate the eight variances that are listed in part (a) of this problem.

(1) Quantity variance for polyethylene powder.

= (AQ X SP) – (SQ X SP)

= Value – Value

= ? – ?

= ?

(2) Price variance for polyethylene powder.

= (AQ X AP) – (AQ X SP)

= Value – Value

= ? – ?

= ?

(3) Quantity variance for finishing kits.

= (AQ X SP) – (SQ X SP)

= Value – Value

= ? – ?

= ?

(4) Price variance for finishing kits

= (AQ X AP) – (AQ X SP)

= Value – Value

= ? – ?

= ?

(5) Quantity variance for type I workers.

= (AH X SR) – (SH X SR)

= Value – Value

= ? – ?

= ?

(6) Price variance for type I workers.

= (AH X AR) – (AH X SR)

= Value – Value

= ? – ?

= ?

(7) Quantity variance for type II workers.

= (AH X SR) – (SH X SR)

= Value – Value

= ? – ?

= ?

(8) Price variance for type II workers. (Round to 2 decimal points)

= (AH X AR) – (AH X SR)

= Value – Value

= ? – ?

= ?

After you have completed the requirements of CD11, consider this additional question.

1. Assume the standard price for polyethylene powder and type I labor changed to $1.60 and

$16 respectively. Revise variance calculations to reflect these changes.

CD11 Solution

(a) Based on the comments above, predict whether each of the following variances will be favorable or unfavorable.

If you don’t have enough information to make a prediction, use “NEI” to indicate “Not Enough Information.”

(1) Quantity variance for polyethylene powder. Unfavorable

(2) Price variance for polyethylene powder. Unfavorable

(b) Calculate the eight variances that are listed in part (a) of this problem.

(1) Quantity variance for polyethylene powder.

= (AQ X SP) – (SQ X SP)

(2) Price variance for polyethylene powder.

= (AQ X AP) – (AQ X SP)

=

1,200 x ($2,040 ÷1200)

– 1,200 x $1.50

= $2,040 – $1,800

=$240 U

(3) Quantity variance for finishing kits.

(4) Price variance for finishing kits

= (AQ X AP) – (AQ X SP)

= 20 x ($3,240 ÷20) – 20 x $170

= $3,240 – $3,400

=$160 F

(7) Quantity variance for type II workers.

= (AH X SR) – (SH X SR)

= 65 x $12 – (20 x 3) x $12

=$780 –$720

=$60 U

(8) Price variance for type II workers. (Round to 2 decimal points)

= (AH X AR) – (AH X SR)

= 65 x ($796.25 ÷ 65) – 65 x $12

CD11 Solution to additional question

1. Assume the standard price for polyethylene powder and type I labor changed to $1.60 and

$16 respectively. Revise variance calculations to reflect these changes.

(a) Based on the comments above, predict whether each of the following variances will be favorable or unfavorable.

If you don’t have enough information to make a prediction, use “NEI” to indicate “Not Enough Information.”

(1) Quantity variance for polyethylene powder. Unfavorable

(2) Price variance for polyethylene powder. Unfavorable

(b) Calculate the eight variances that are listed in part (a) of this problem.

(1) Quantity variance for polyethylene powder.

= (AQ X SP) – (SQ X SP)

(2) Price variance for polyethylene powder.

= (AQ X AP) – (AQ X SP)

=

1,200 x ($2,040 ÷1200)

–1,200 x $1.60

= $2,040 – $1,920

=$120 U

(7) Quantity variance for type II workers.

= (AH X SR) – (SH X SR)

= 65 x $12 – (20 x 3) x $12

=$780 –$720

=$60 U