1. No. A discounted note payable has no stated interest rate, but provides interest by discounting the

note proceeds. The discount, which is the difference between the proceeds and the face of the

note, is the interest and is accounted for as such.

2. a. Employee’s federal income taxes, social security, and Medicare

b. Employees Federal Income Tax Payable, Social Security Tax Payable, and Medicare Tax

Payable

6. a. Constants are data that remain unchanged from payroll to payroll. These include employee

names, social security numbers, marital status, number of income tax withholding

allowances, rates of pay, tax rates, and withholding tables.

b. Variables are data that change from payroll to payroll. These include number of hours or

days worked for each employee, accrued days of sick leave, vacation credits, total earnings

to date, and total taxes withheld.

7. The vacation pay expense should be recorded during the period in which the vacation privilege

is earned.

8. In a defined contribution pension plan, the company invests contributions on behalf of the employee

during the employee’s working years. Normally, the employee and employer contribute to the

p

lan. The employee’s pension depends on the total contributions and the investment returns

earned on those contributions.

b

CHAPTER 11

CURRENT LIABILITIES AND PAYROLL

DISCUSSION QUESTIONS

b

b

p

CHAPTER 11 Current Liabilities and Payroll

PE 11-1A

PE 11-1B

a. $324,000

b. $319,950 [$324,000 – ($324,000 × 10% × 45 ÷ 360)]

PE 11-2A

…

…

Multiplied by allowances claimed on Form W-4…………………

…

2162.00

…

…

PE 11-2B

Total wage payment……………………………………………………

…

$1,370.00

One allowance …………………………………………………………

…

$81.00

Multiplied by allowances claimed on Form W-4…………………

…

181.00

Amount subject to withholding……………………………………… $1,289.00

Initial withholding from wage bracket in Exhibit 2………………

…

$ 87.34

Plus additional withholding: 22% of excess over $832*………… 100.54

Federal income tax withholding……………………………………

…

$ 187.88

* ($1,289 – $832) × 22%

PRACTICE EXERCISES

×

×

CHAPTER 11 Current Liabilities and Payroll

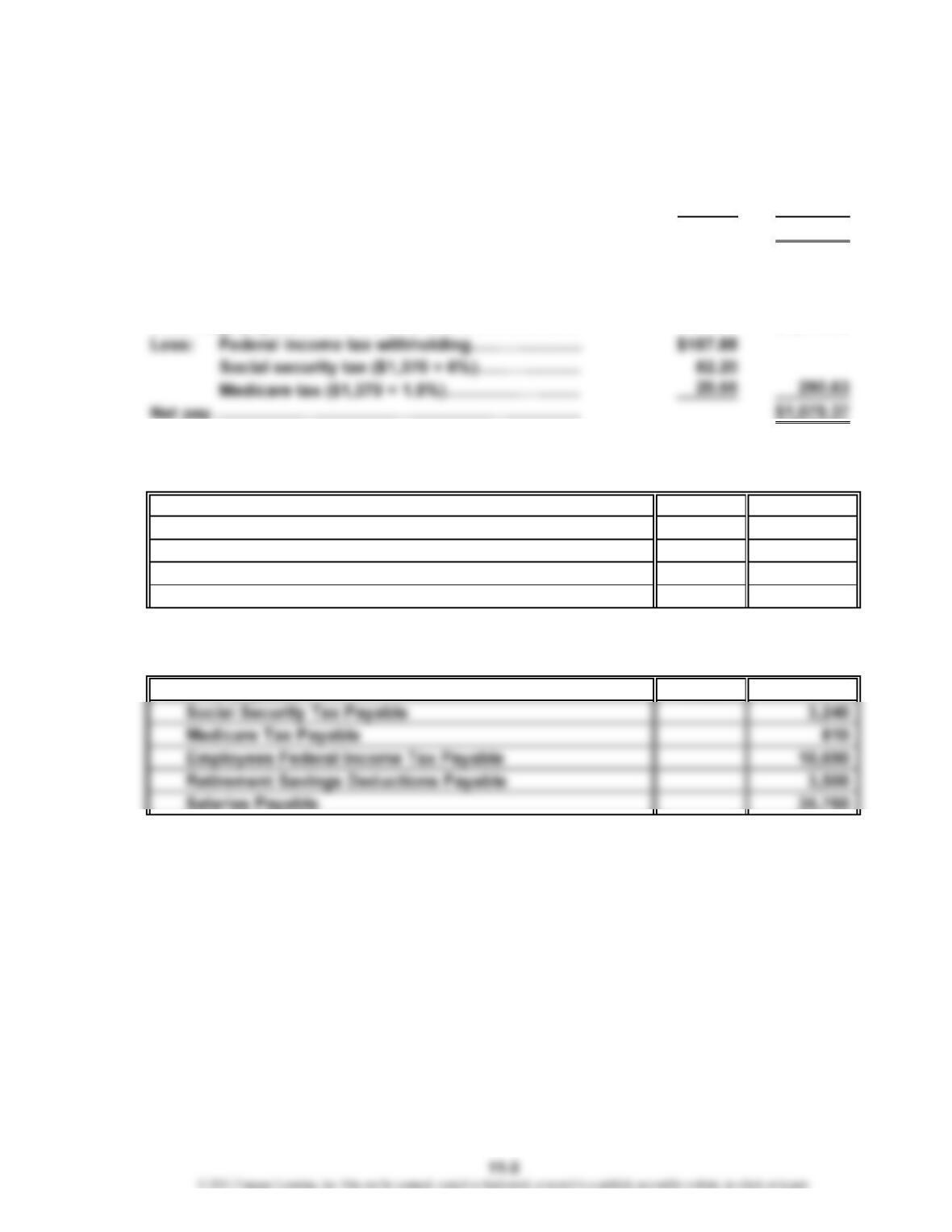

PE 11-3A

Total wage payment………………………………………… $2,400.00

Less: Federal income tax withholding………………

…

$407.58

Social security tax ($2,400 × 6%)………………

…

144.00

Medicare tax ($2,400 × 1.5%)…………………… 36.00 587.58

Net pay………………………………………………………… $1,812.42

PE 11-3B

Total wage payment………………………………………… $1,370.00

PE 11-4A

Salaries Expense 189,000

Social Security Tax Payable 11,340

Medicare Tax Payable 2,835

Employees Federal Income Tax Payable 37,420

Salaries Payable 137,405

PE 11-4B

Salaries Expense 54,000

…

…

CHAPTER 11 Current Liabilities and Payroll

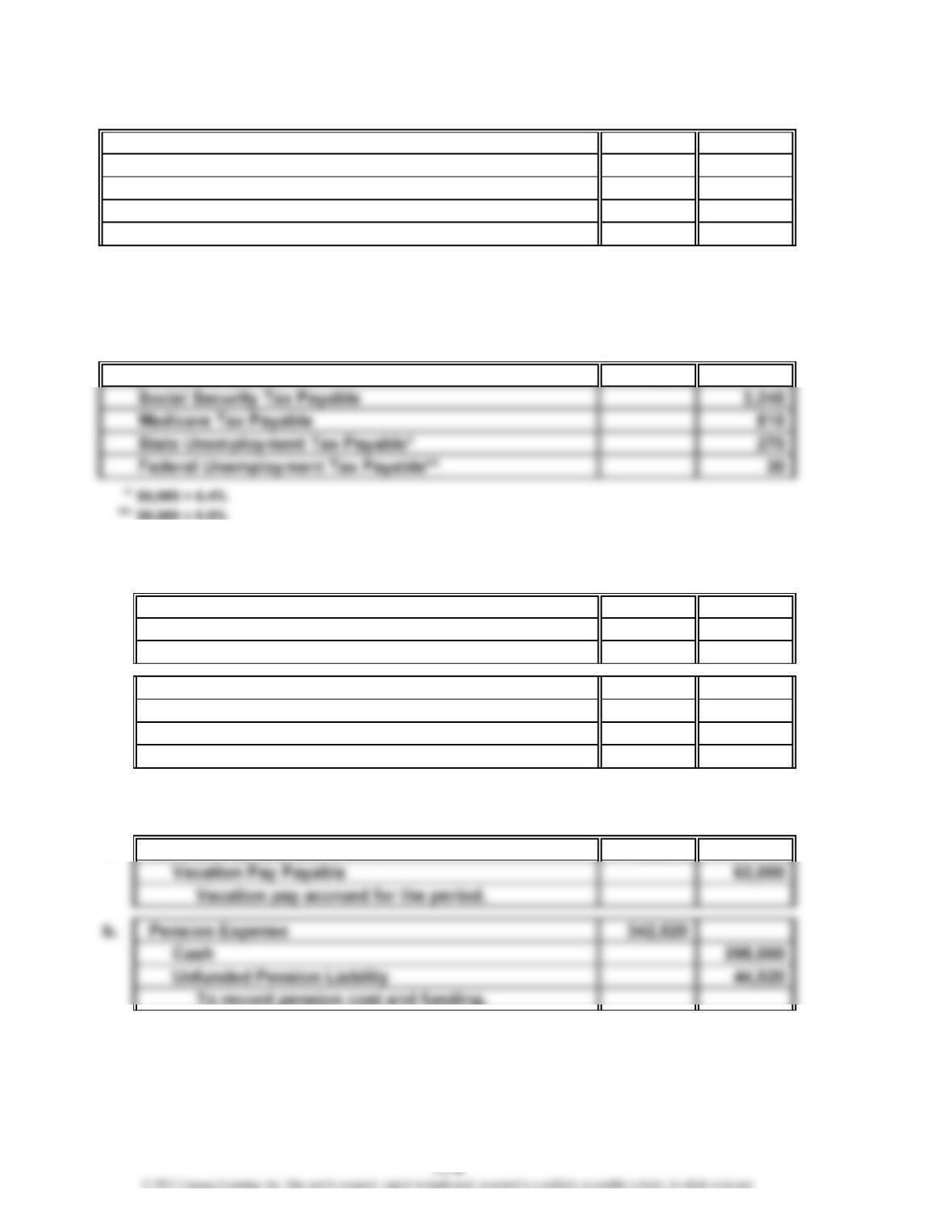

PE 11-5A

Payroll Tax Expense 15,315

Social Security Tax Payable 11,340

Medicare Tax Payable 2,835

State Unemployment Tax Payable* 1,026

Federal Unemployment Tax Payable** 114

*$19,000 × 5.4%

** $19,000 × 0.6%

PE 11-5B

Payroll Tax Expense 4,350

PE 11-6A

a. Vacation Pay Expense 25,500

Vacation Pay Payable 25,500

Vacation pay accrued for the period.

b. Pension Expense 20,400

Cash 20,400

To record pension contribution

(6% × $340,000).

PE 11-6B

a. Vacation Pay Expense 62,000

CHAPTER 11 Current Liabilities and Payroll

PE 11-7A

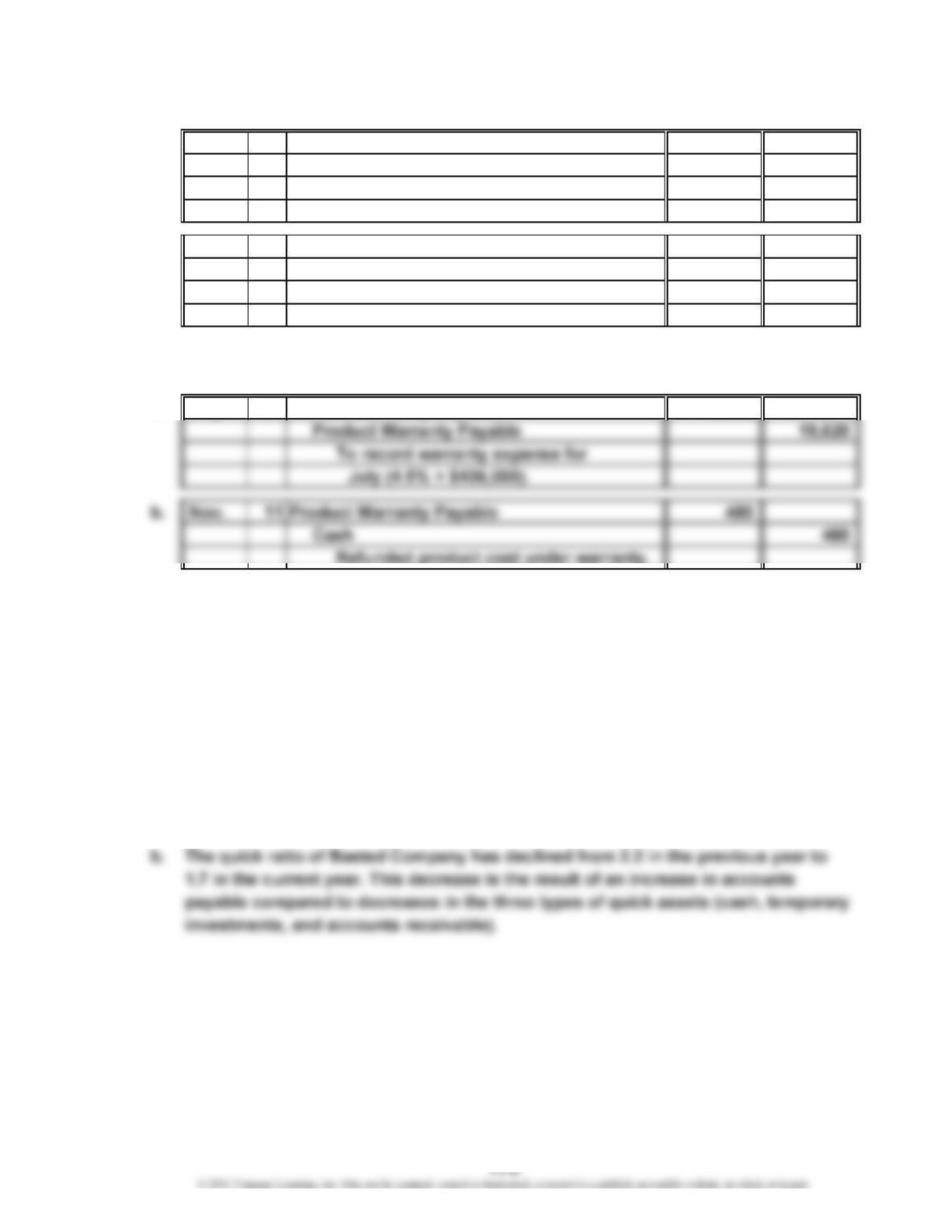

a. Jan. 31 Product Warranty Expense 11,730

Product Warranty Payable 11,730

To record warranty expense for

January (3% × $391,000).

b. Aug. 15 Product Warranty Payable 165

Supplies 110

Wages Payable 55

Replaced defective part under warranty.

PE 11-7B

a. July 31 Product Warranty Expense 19,620

PE 11-8A

a. December 31, current year:

Quick Ratio = Quick Assets ÷ Current Liabilities

= ($2,070 + $4,780 + $2,160) ÷ $5,300

= 1.7

December 31, previous year:

Quick Ratio = Quick Assets ÷ Current Liabilities

= ($2,230 + $5,030 + $2,420) ÷ $4,400

= 2.2

CHAPTER 11 Current Liabilities and Payroll

PE 11-8B

a. December 31, current year:

Quick Ratio = Quick Assets ÷ Current Liabilities

= ($1,760 + $2,130 + $1,430) ÷ $2,800

= 1.9

December 31, previous year:

Quick Ratio = Quick Assets ÷ Current Liabilities

= ($1,680 + $2,090 + $1,330) ÷ $3,400

= 1.5

b. The quick ratio of Aloha Company has improved from 1.5 in the previous year to 1.9

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-1

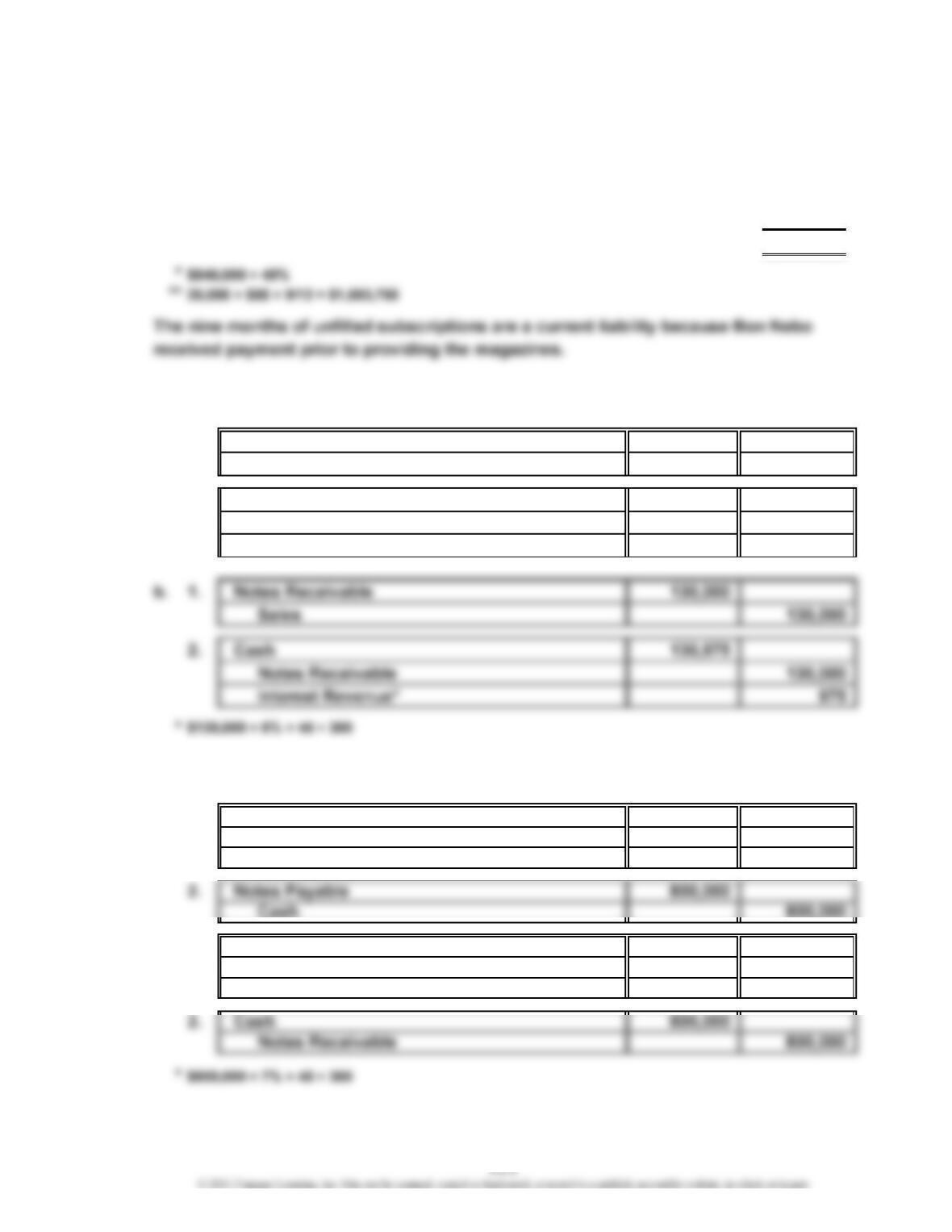

Current liabilities:

Federal income taxes payable*………………………………………………

…

$ 336,000

Advances on magazine subscriptions**……………………………………

…

1,593,750

Total current liabilities………………………………………………………

…

$1,929,750

Ex. 11-2

a. 1. Merchandise Inventory 130,000

Notes Payable 130,000

2. Notes Payable 130,000

Interest Expense* 975

Cash 130,975

Ex. 11-3

a. 1. Merchandise Inventory 793,000

Interest Expense* 7,000

Notes Payable 800,000

b. 1. Notes Receivable 800,000

Sales 793,000

Interest Revenue* 7,000

EXERCISES

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-4

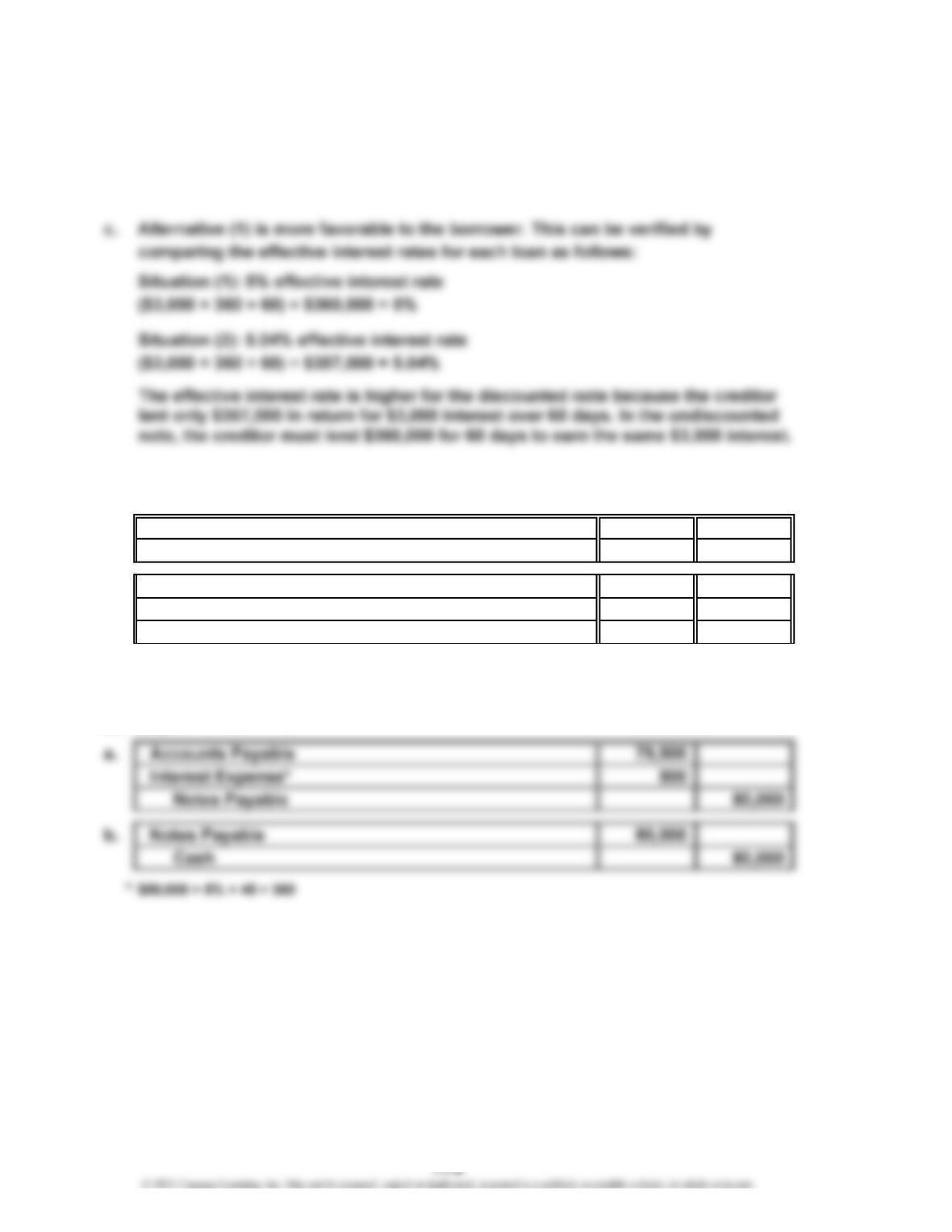

a. $360,000 × 5% × 60 ÷ 360 = $3,000 for each alternative.

b. (1) $360,000 simple-interest note: $360,000 proceeds

(2) $360,000 discounted note: $360,000 – $3,000 interest = $357,000 proceeds

Ex. 11-5

a. Accounts Payable 210,000

Notes Payable 210,000

b. Notes Payable 210,000

Interest Expense* 1,575

Cash 211,575

*$210,000 × 6% × 45 ÷ 360

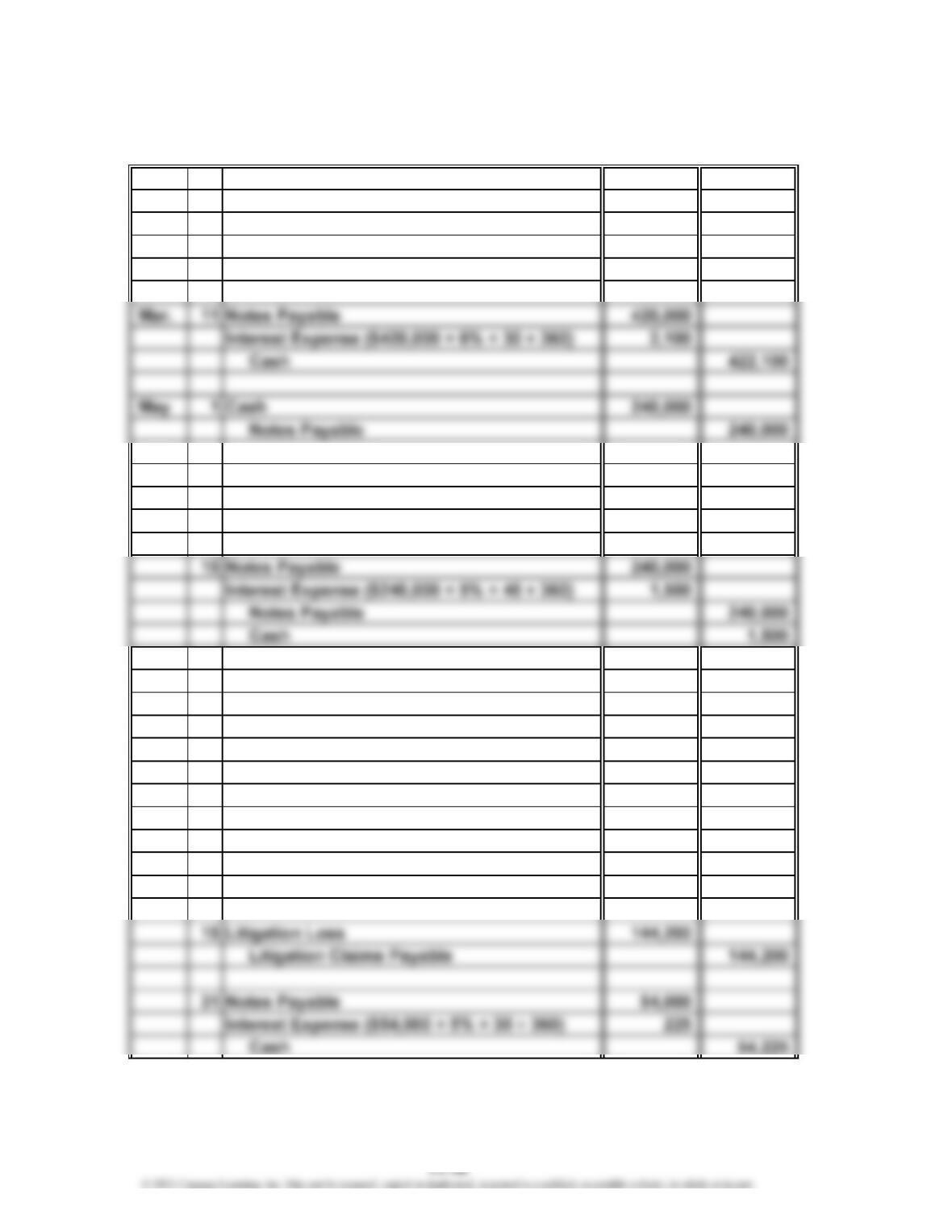

Ex. 11-6

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-7

2. Notes Payable 100,000

Interest Expense* 875

Cash 100,875

b. 1. Accounts Payable 100,000

Notes Payable 100,000

Ex. 11-8

a. $3,953 is the amount disclosed as the current portion of long-term debt.

b. The current liabilities decreased by $67 ($3,953 – $4,020).

c. $28,295 ($32,248 – $3,953)

Ex. 11-9

a. Regular pay (40 hrs. × $22)…………………………………

…

$ 880.00

Overtime pay (10 hrs. × $44)…………………………………

…

440.00

Gross pay………………………………………………………

…

$1,320.00

…

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-10

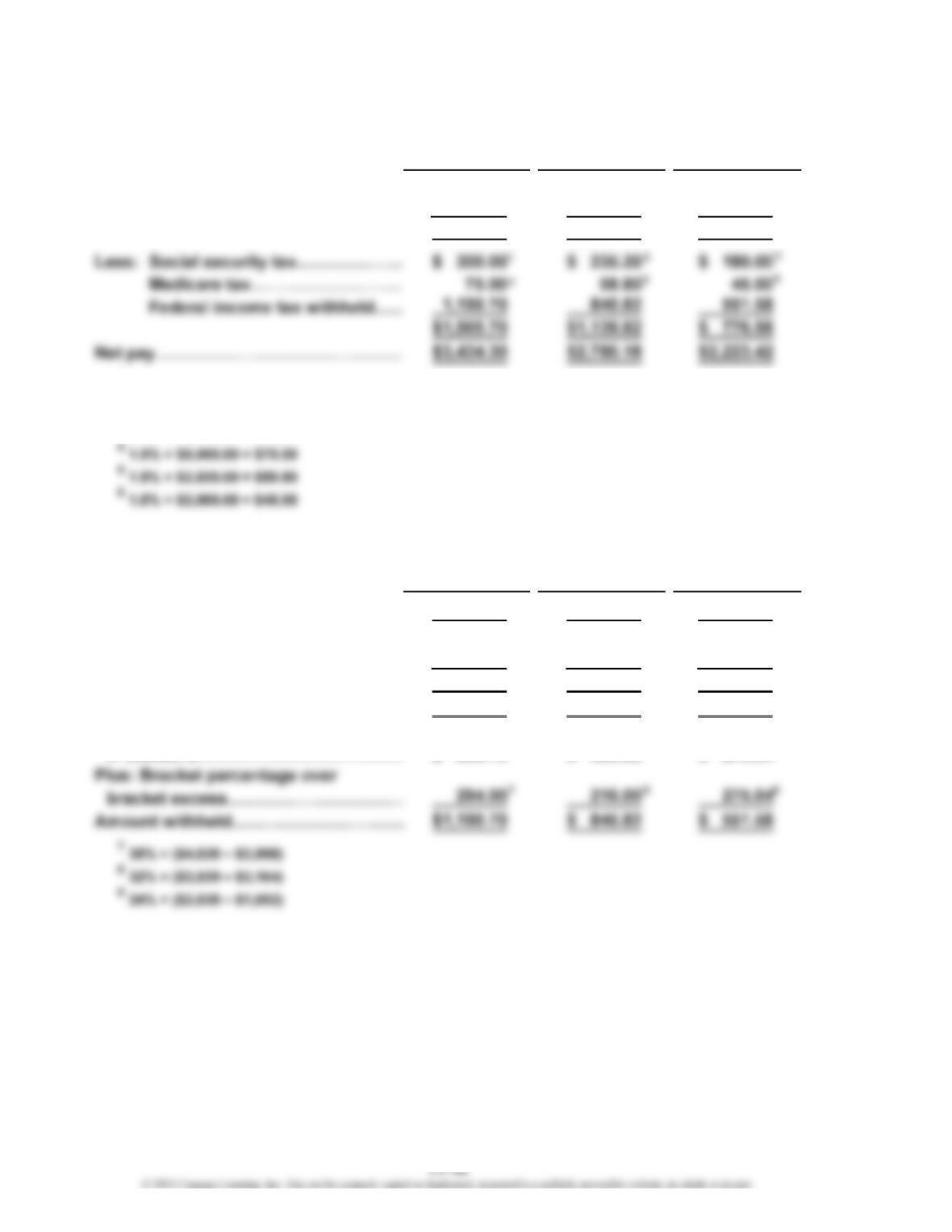

Regular earnings…………………………

…

$5,000.00 $3,200.00 $2,000.00

Overtime earnings………………………

…

720.00 1,000.00

Gross pay…………………………………

…

$5,000.00 $3,920.00 $3,000.00

1

6.0% × $5,000.00 = $300.00

2

6.0% × $3,920.00 = $235.20

3

6.0% × $3,000.00 = $180.00

Withholding supporting calculations:

Gross weekly pay………………………… $5,000.00 $3,920.00 $3,000.00

Number of withholding allowances…

…

212

Multiplied by: Value of one allowance

…

× $81.00 × $81.00 × $81.00

Amount to be deducted…………………

…

$ 162.00 $ 81.00 $ 162.00

Amount subject to withholding………

…

$4,838.00 $3,839.00 $2,838.00

Initial withholding from wage bracket

…

Computer

Consultant Programmer Administrator

Consultant Programmer

Computer

Administrator

…

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-11

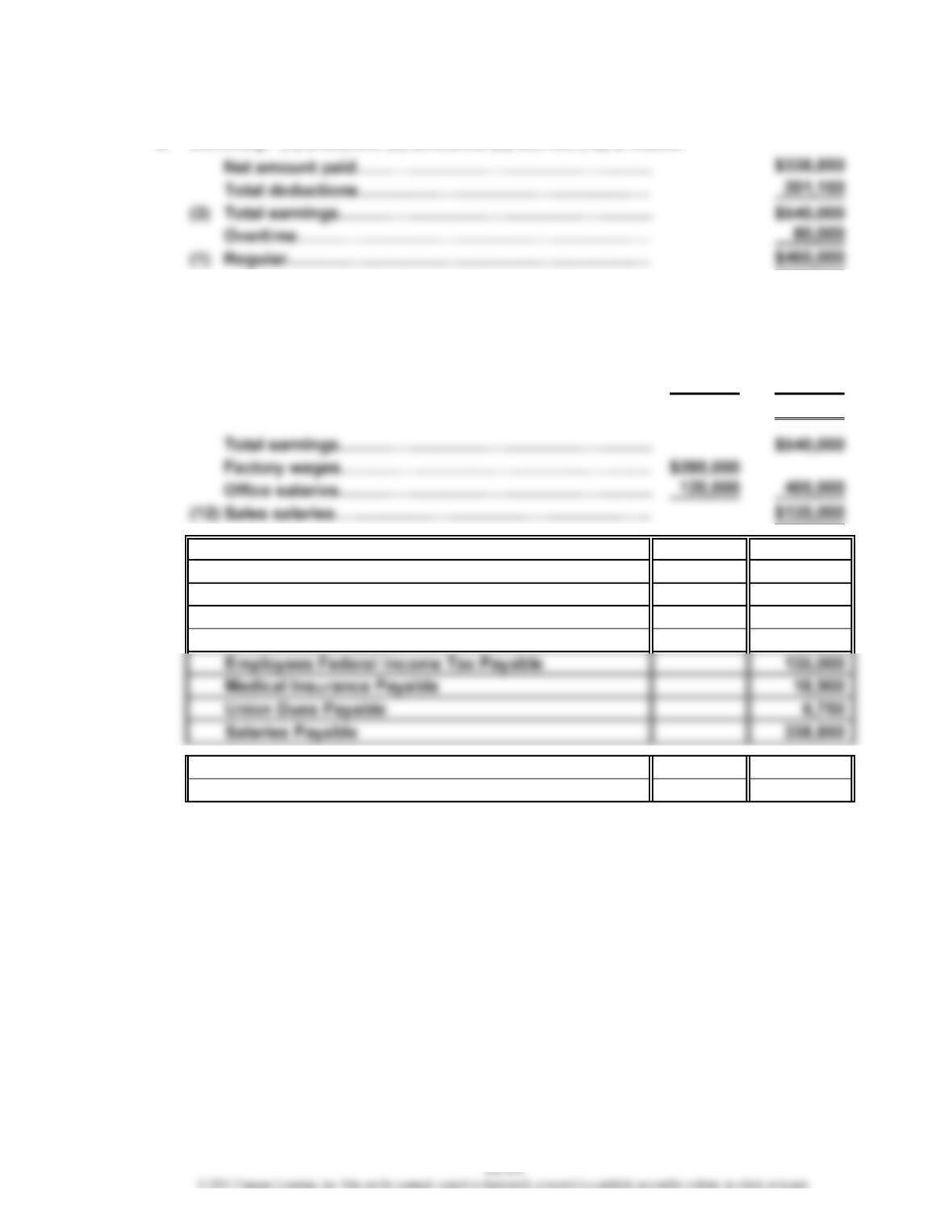

Total deductions……………………………………………

…

$201,150

Social security tax…………………………………………

…

$ 32,400

Medicare tax…………………………………………………

…

8,100

Income tax withheld………………………………………

…

135,000

Medical insurance…………………………………………

…

18,900 194,400

(8) Union dues…………………………………………………… $ 6,750

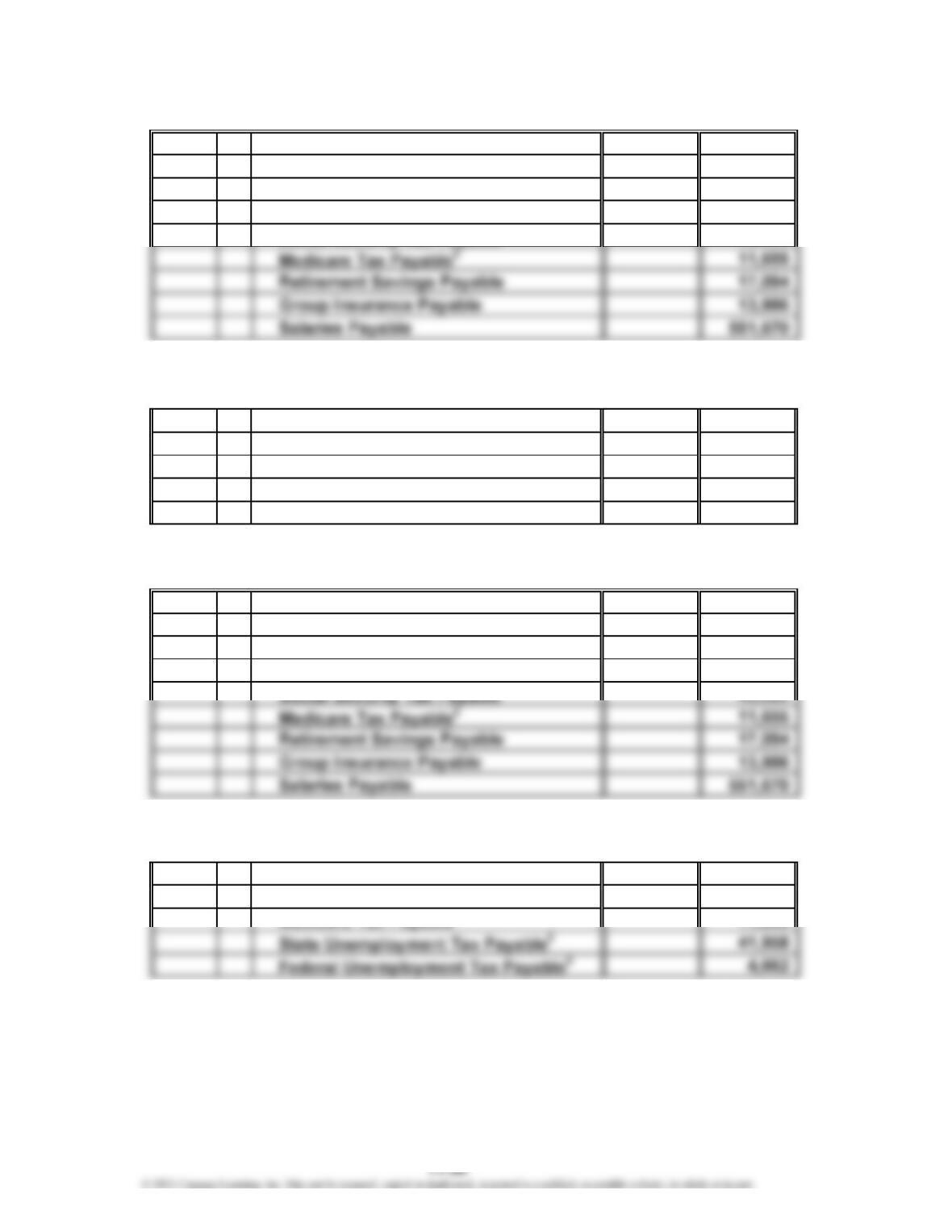

b. Factory Wages Expense 285,000

Sales Salaries Expense 135,000

Office Salaries Expense 120,000

Social Security Tax Payable 32,400

Medicare Tax Payable 8,100

c. Salaries Payable 338,850

Cash 338,850

…

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-12

a. Social security tax (6% × $560,000)…………………………………………

…

$33,600

Medicare tax (1.5% × $560,000)………………………………………………

…

8,400

State unemployment tax (5.4% × $60,000)…………………………………

…

3,240

Federal unemployment (0.6% × $60,000)……………………………………

…

360

$45,600

Ex. 11-13

a. Salaries Expense 1,380,000

Social Security Tax Payable 82,800

Medicare Tax Payable 20,700

Employees Federal Income Tax Payable 276,000

Salaries Payable 1,000,500

*5.4% × $245,000

** 0.6% × $245,000

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-14

*6.0% × $320,000

** 1.5% × $320,000

b. Payroll Tax Expense 26,400

Social Security Tax Payable 19,200

Medicare Tax Payable 4,800

State Unemployment Tax Payable* 2,160

Federal Unemployment Tax Payable** 240

Ex. 11-15

Big Howie’s Hot Dog Stand does have an internal control procedure that should detect

the payroll error. Before funds are transferred from the regular bank account to the

payroll account, the owner authorizes the total amount of the week’s payroll. The

owner should catch the error, since the extra 60 hours will cause the weekly payroll to

be substantially higher than usual. The owner should sign the paychecks, thereby

restricting access to cash by employees who are responsible for record keeping.

Ex. 11-16

a. Appropriate. All changes to the payroll system, including wage rate increases,

should be authorized by someone outside the Payroll Department.

b. Inappropriate. Each employee should record his or her own time out for lunch.

Under the current procedures, one employee could clock in several employees

who are still out to lunch. The company would be paying employees for more time

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-17

a. Vacation Pay Expense 11,500

Vacation Pay Payable 11,500

Vacation pay accrued for January ($138,000 ÷ 12 ).

Ex. 11-18

a. Dec. 31 Pension Expense 365,000

Unfunded Pension Liability 365,000

To record quarterly pension cost.

b. In a defined contribution plan, the company invests contributions on behalf of the

employee during the employee’s working years. Normally, the employee and

employer contribute to the plan. The employee’s pension depends on the total

contributions and the investment return on those contributions. In a defined benefit

plan, the company pays the employee a fixed annual amount based on a formula.

The employer is obligated to pay for (fund) the employee’s future pension benefits.

Ex. 11-19

The $4,391 million unfunded pension liability is the approximate amount of the pension

obligation that exceeds the value of the net assets of the pension plan. Apparently,

Procter & Gamble has underfunded its plan relative to the obligation that has accrued

over time. This can occur when the company contributes less to the plan than the

annual pension cost.

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-20

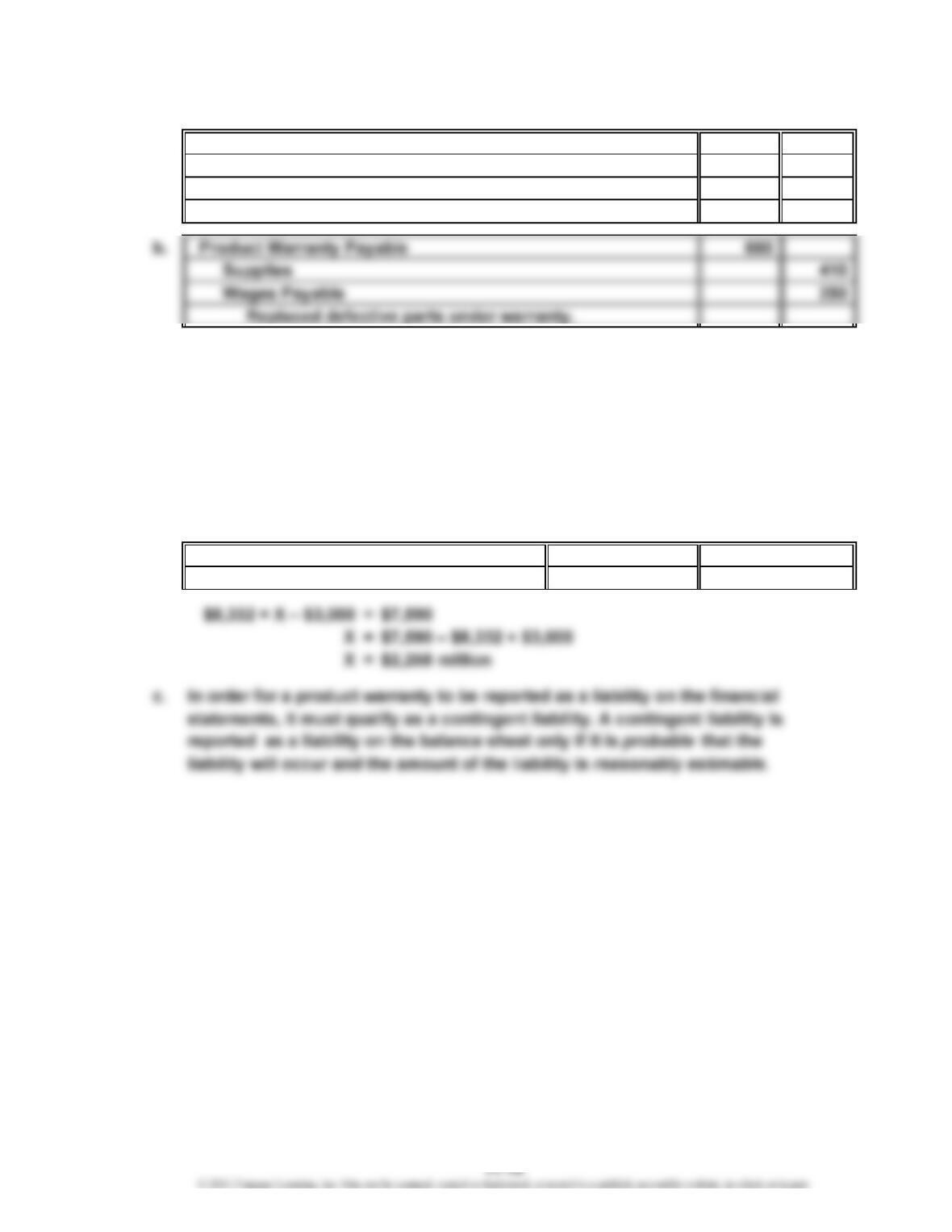

a. Product Warranty Expense 9,950

Product Warranty Payable 9,950

To record warranty expense for January

(2.5% × $398,000).

Ex. 11-21

a. The warranty liability represents estimated outstanding automobile warranty

claims. Of these claims, $2,994 million is estimated to be due during Year 2, while

the remainder ($5,338 million) is expected to be paid after Year 2. The distinction

between short- and long-term liabilities is important to creditors in order to

accurately evaluate the near-term cash demands on the business relative to the

quick current assets and other longer-term demands.

b. Product Warranty Expense

Product Warranty Payable

2,258,000,000

2,258,000,000

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-22

a. Damage Awards and Fines 365,000

EPA Fines Payable 240,000

Litigation Claims Payable 125,000

Note to Instructors: The “damage awards and fines” would be disclosed on the

income statement under “Other expenses.”

Ex. 11-23

Quick Assets

Current Liabilities

$500,000 + $200,000

$500,000

$486,000 + $210,000

$580,000

b. The quick ratio decreased between the two balance sheet dates. The major reason

is a significant increase in inventory that likely drove the increase in accounts

Current year: = 1.2

Previous year:

a. Quick Ratio =

= 1.4

CHAPTER 11 Current Liabilities and Payroll

Ex. 11-24

Quick Assets

Current Liabilities

b. It is clear that Apple Inc.’s short-term liquidity is stronger than HP’s. Apple’s quick

ratio is 150% [(1.0 – 0.4) ÷ 0.4] higher. Apple has a much stronger relative

short-term investment position than does HP. Apple’s cash, accounts receivable,

and short-term investments are 88% of total current assets (and almost 100% of

a. Quick Ratio =

CHAPTER 11 Current Liabilities and Payroll

Prob. 11-1A

1. Jan. 10 Merchandise Inventory 420,000

Accounts Payable—Beckham Co. 420,000

Feb. 9 Accounts Payable—Beckham Co. 420,000

Notes Payable 420,000

June 1 Tools 309,400

Interest Expense ($312,000 × 5% × 60 ÷ 360) 2,600

Notes Payable 312,000

July 30 Notes Payable 240,000

Interest Expense ($240,000 × 7% × 45 ÷ 360) 2,100

Cash 242,100

30 Notes Payable 312,000

Cash 312,000

Dec. 1 Office Equipment 700,500

Notes Payable 540,000

Cash 160,500

PROBLEMS

CHAPTER 11 Current Liabilities and Payroll

Prob. 11-1A (Concluded)

2. a. Product Warranty Expense 19,500

Product Warranty Payable 19,500

CHAPTER 11 Current Liabilities and Payroll

Prob. 11-2A

1. a. Dec. 30 Sales Salaries Expense 402,000

Warehouse Salaries Expense 210,000

Office Salaries Expense 165,000

Employees Federal Income Tax Payable 135,975

1

$777,000 × 6%

2

$777,000 × 1.5%

b. Dec. 30 Payroll Tax Expense 60,675

Social Security Tax Payable 46,620

Medicare Tax Payable 11,655

State Unem

p

lo

y

ment Tax Pa

y

able32,160

Federal Unem

p

lo

y

ment Tax Pa

y

able4240

3

$40,000 × 5.4%

4

$40,000 × 0.6%

2. a. Dec. 30 Sales Salaries Expense 402,000

Warehouse Salaries Expense 210,000

Office Salaries Expense 165,000

Employees Federal Income Tax Payable 135,975

1

$777,000 × 6%

2

$777,000 × 1.5%

b. Jan. 5 Payroll Tax Expense 104,895

Social Security Tax Payable 46,620

3

$777,000 × 5.4%

4

$777,000 × 0.6%

y