CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6B (FIN MAN); Appendix Prob. 11–6B (MAN)

1. $60,000 ($600,000 × 10%)

2.

a.

Total manufacturing costs:

Variable ($52* × 10,000 units) …………………………………………………..

$520,000

Fixed factory overhead ……………………………………………………………

180,000

Total ……………………………………………………….…………………………

$700,000

Cost amount per unit: $700,000 ÷ 10,000 units ………………………………..

$ 70

*

$32 + $12 + $8

Desired Profit +

c.

Cost amount per unit …………………………………………………………………..

$70

Markup ($70 × 30%) …………………………………………………………………….

21

Selling price ……………………………………………………………………………….

$91

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6B (FIN MAN); Appendix Prob. 11–6B (MAN) (Continued)

3.

a.

Total costs:

Variable ($59 × 10,000 units) ………………………………………………….

$590,000

Fixed ($180,000 + $80,000) ……………………………………………………..

260,000

Total ………………………………………………………………………………..

$850,000

Cost amount per unit: $850,000 ÷ 10,000 units …………………………...

$ 85.00

c.

Cost amount per unit ………………………………………………………………..

Markup ($85.00 × 7.06%) ……………………………………………………………

4.

a.

Variable cost amount per unit: $59

Total variable costs: $59 × 10,000 units = $590,000

Markup ($59 × 54.24%) ………………………………………………………………

Desired Profit + Total Fixed Costs

Markup Percentage = Total Variable Costs

$60,000 + $180,000 + $80,000

=$590,000

5. The cost-plus approach price of $91 should be viewed as a general guideline for

establishing long-run normal prices. Other considerations, such as the price of

competing products and general economic conditions of the marketplace, could

lead management to establish a short-run price more or less than $91.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6B (FIN MAN); Appendix Prob. 11–6B (MAN) (Concluded)

6. a.

Differential Analysis

Reject (Alt. 1) or Accept (Alt. 2) Order

September 5

Reject

Order

(Alternative 1)

Accept

Order

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$0

$ 91,2001

$ 91,200

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAKE A DECISION

MAD 25–1 (FIN MAN); MAD 11–1 (MAN)

a.

Contribution Margin

=

Ticket Price – Variable Costs per Passenger

per Passenger

=

$180 – $40

=

$140

c.

Contribution Margin

=

Discounted Ticket Price – Variable Costs

per Passenger

=

$90 – $40

=

$50

d. Lost contribution margin from customers who switch tickets: 8 × $140 = $1,120

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAD 25–1 (FIN MAN); MAD 11–1 (MAN) (Concluded)

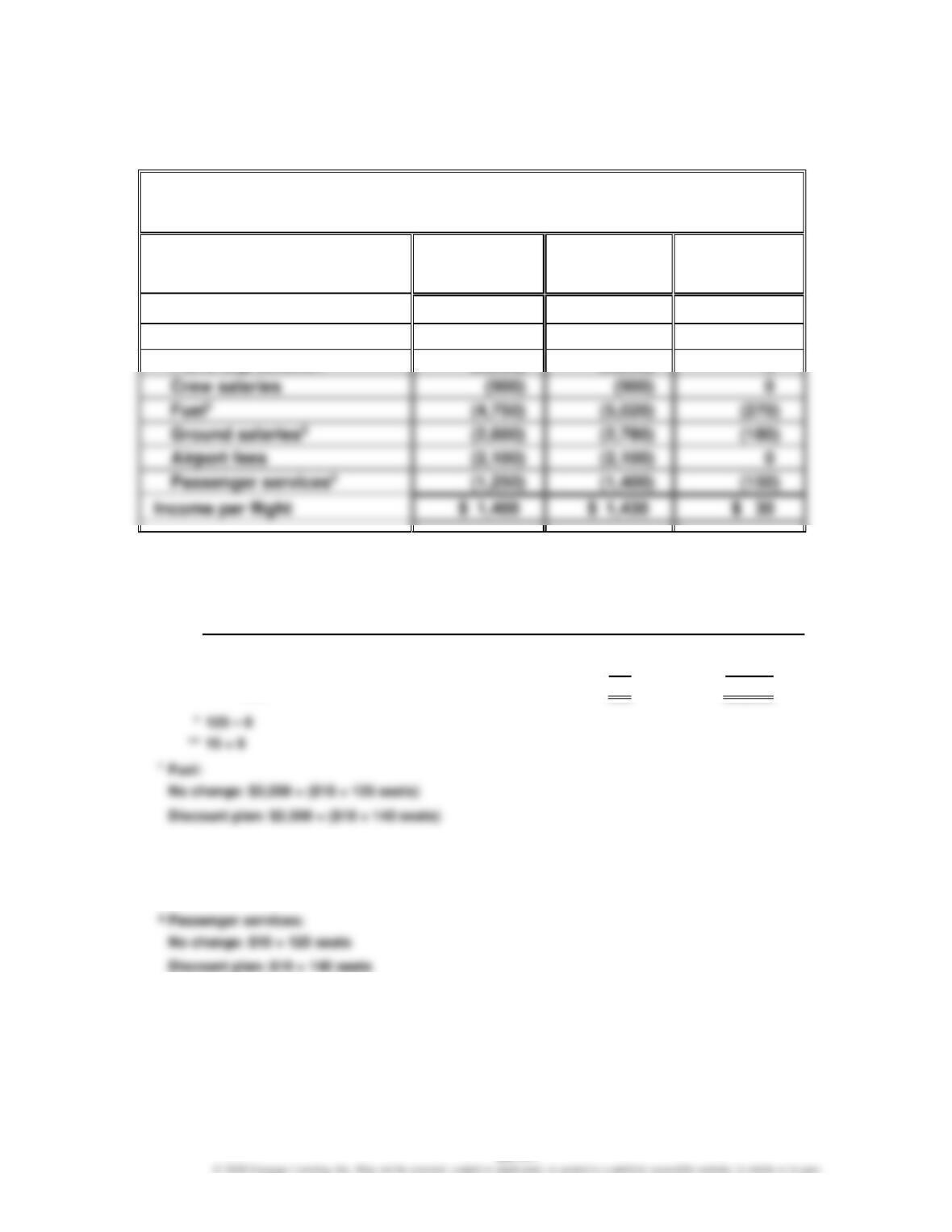

The same answer can be determined from a differential analysis table, as follows:

Differential Analysis

Continue with No Change (Alt. 1) or Offer the Discount Plan (Alt. 2)

February 5

No Change

(Alternative 1)

Discount Plan

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues per flight1

$22,500

$23,130

$ 630

Costs per flight:

Plane depreciation

(9,500)

(9,500)

0

(4,750)

(5,020)

(2,600)

(2,780)

Airport fees

(2,100)

(2,100)

0

(1,250)

(1,400)

i

1

Revenues:

No change revenues: $180 × 125 seats

Discount plan revenues:

Ticket Price

No. of Tickets

Revenue

Full price

$180

117*

$21,060

Discount price

90

23**

2,070

15 + 8

2

No change: $2,500 + ($18 × 125 seats)

Total

140

$23,130

3

Ground salaries:

No change: $1,100 + ($12 × 125 seats)

Discount plan: $1,100 + ($12 × 140 seats)

4

Passenger services:

Discount plan: $10 × 140 seats

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAD 25–2 (FIN MAN); MAD 11–2 (MAN)

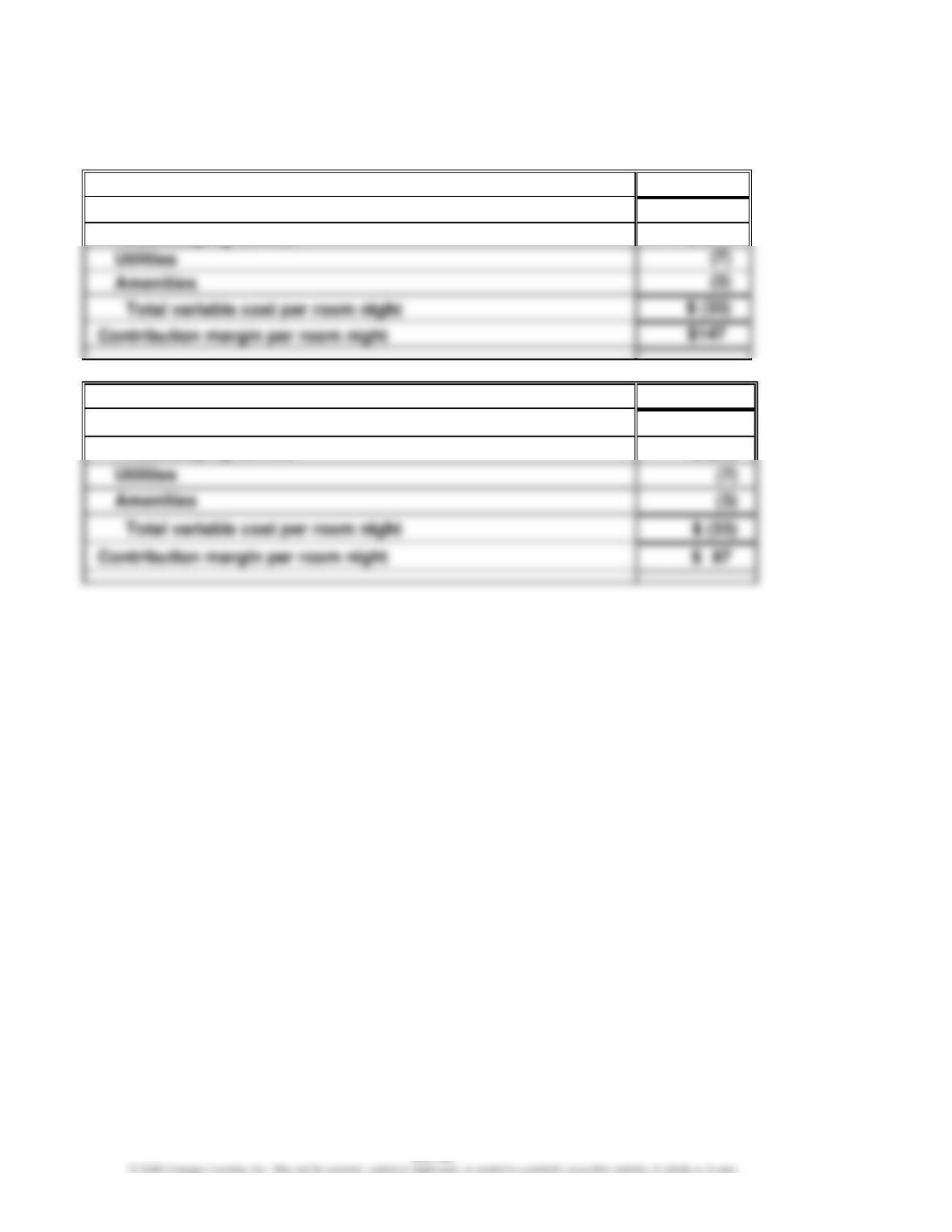

a. Contribution margin per room night:

Rate per room night

$180

Variable costs per room night:

Housekeeping service

$ (23)

$ (33)

Contribution margin per room night

$147

b.

Rate per room night

$120

Variable costs per room night:

Housekeeping service

$ (23)

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAD 25–2 (FIN MAN); MAD 11–2 (MAN) (Concluded)

c.

Differential Analysis

Continue with Existing Plan (Alt. 1) or Execute the Discount Plan (Alt. 2)

Continue with

Existing Plan

(Alternative 1)

Execute the

Discount Plan

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues per weekend1

$32,400

$36,000

$ 3,600

Variable costs per weekend:

Housekeeping service2

$ (4,140)

$ (6,900)

$(2,760)

$ (5,940)

$ (9,900)

$(3,960)

Contribution margin per weekend

$26,460

$26,100

1

Existing plan: $180 × 200 rooms × 30% × 3 weekend days = $32,400

Discount plan: $120 × 200 rooms × 50% × 3 weekend days = $36,000

2

Existing plan: $23 × 200 rooms × 30% × 3 weekend days = $4,140

Discount plan: $23 × 200 rooms × 50% × 3 weekend days = $6,900

Discount plan: $7 × 200 rooms × 50% × 3 weekend days = $2,100

d. The differential analysis indicates that the discount plan will result in a lower

contribution margin per weekend than the existing pricing plan. It is possible that other

MAD 25–3 (FIN MAN); MAD 11–3 (MAN)

a.

Operating income per megawatt hour for industrial customers:

Revenues

$150*

Variable operating costs

(80)

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAD 25–3 (FIN MAN); MAD 11–3 (MAN) (Concluded)

b. Contribution margin per megawatt hour for industrial customers:

Revenues per unit

$150

Variable operating costs per unit

(80)

Contribution margin per unit

$ 70

d. The discount pricing may become known. Thus, other industrial customers may

request a similar pricing opportunity. This may cause industrial demand to shift

from peak hours to off-peak hours. If the shifted peak hour demand could not be

MAD 25–4 (FIN MAN); MAD 11–4 (MAN)

a.

Revenues

$ 6,000,000

Expenses:

Crew

$(2,700,000)

Depreciation

Fuel

$(4,770,000)

Food

(1,500,000)

b. Divide the variable costs by the number of passengers:

Crew to serve passengers

$1,200,000

÷

1,000

passengers

=

$1,200

per passenger

Food

1,500,000

÷

1,000

passengers

=

1,500

per passenger

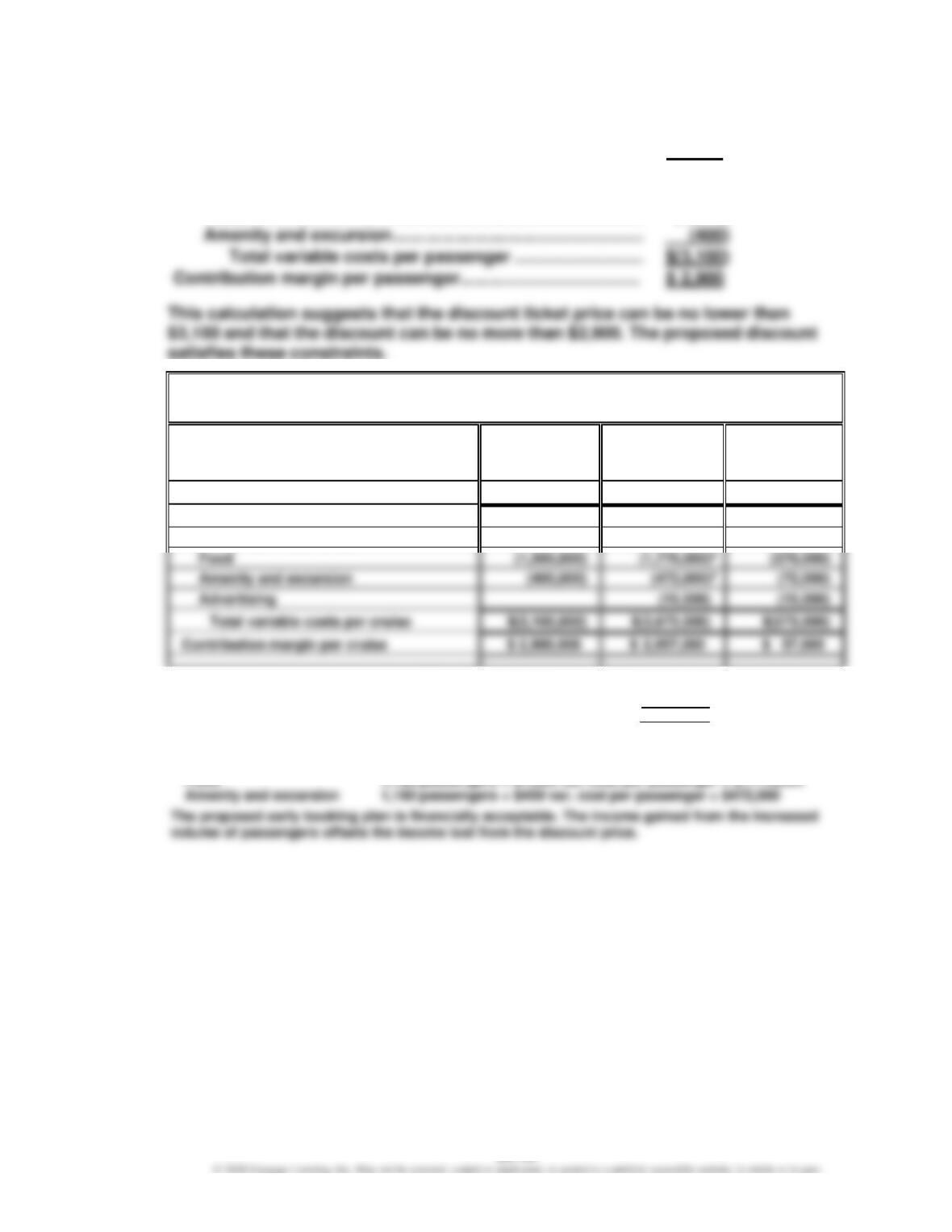

Amenity and excursion

400,000

÷

1,000

passengers

=

400

per passenger

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

MAD 25–4 (FIN MAN); MAD 11–4 (MAN) (Concluded)

c.

Ticket price ………………………………………………………………….

$ 6,000

Variable costs per passenger [from (b)]:

Crew to serve passengers …………………………………………….

$(1,200)

Food ……………………………………………………………………………

(1,500)

Amenity and excursion …………………………………………………

Total variable costs per passenger …………………………..

$(3,100)

d.

Differential Analysis

Existing Plan (Alt. 1) or Early Booking Program (Alt. 2)

Existing Plan

(Alternative 1)

Early Booking

Program

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues per cruise

$ 6,000,000

$ 6,630,0001

$ 630,000

Variable costs per cruise:

Crew to serve passengers

$(1,200,000)

$(1,416,000)2

$(216,000)

Amenity and excursion

$(3,100,000)

$(573,000)

Contribution margin per cruise

$ 2,900,000

1

Discount tickets from early booking, 300 tickets × $4,500

$1,350,000

Remaining tickets, (1,180 tickets – 300 tickets) × $6,000

5,280,000

Total revenue

$6,630,000

2

Variable costs per cruise [see (b) for variable cost per passenger]:

Crew to serve passengers

1,180 passengers × $1,200 var. cost per passenger = $1,416,000

1,180 passengers × $1,500 var. cost per passenger = $1,770,000

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

TAKE IT FURTHER

TIF 25–1 (FIN MAN); TIF 11–1 (MAN)

No, it would not be ethical for Aaron to attend the meeting. Such a meeting would be

TIF 25–2 (FIN MAN); TIF 11–2 (MAN)

This activity is designed to have students access a number of products and services on

the Internet to see their commercial potential. Each of the listed sites will provide

Delta Air Lines—Airline tickets

Fixed or Variable?

Fuel …………………………………………………………………………

V

Crew salaries ……………………………………………………………

F

Plane depreciation ……………………………………………………

F

Landing fees …………………………………………………………….

V

Lease costs (gates) …………………………………………………..

F

Ground salaries ……………………………………………………….

F

For Delta Air Lines, employee salaries are relatively fixed and only become variable when

there are significant changes to the flight schedule.

Amazon—Various consumer products

Fixed or Variable?

Cost of products (purchased for resale) …………………….

V

Web page design and programming ………………………….

F

Computer depreciation ……………………………………………..

F

Order handling and packing wages …………………………...

V

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

TIF 25–2 (FIN MAN); TIF 11–2 (MAN) (Concluded)

HP Inc.—Computers

Fixed or Variable?

Cost of computers (dl, dm, and foh) ………………………….

V (mostly)

Web page design and programming ………………………….

F

Advertising ………………………………………………………………

F

Order handling and packing wages …………………………..

Freight …………………………………………………………………….

Bundled software* ……………………………………………………

* Depends on contract terms with software vendor

The product with the largest markup on variable cost is the airline ticket. The portion

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

TIF 25–3 (FIN MAN); TIF 11–3 (MAN)

Memo

To: Juanita Jackson

From: Les Miles

Re: New Product Pricing

Thank you again for taking the time to meet with me and discuss the pricing of our new

computer. While I understand your desire to set an appropriate price for this new product,

Target costing provides a potential solution to the pricing issue. This approach treats

the market price as given and adjusts the cost in order to yield the required profitability.

Target costing is particularly effective in highly competitive product markets where

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

TIF 25–4 (FIN MAN); TIF 11–4 (MAN)

The contribution margin is $4 ($22 – $18) per dozen on the special order. Thus,

Varden’s manager can contribute to fixed costs by accepting the order. However, there

are some additional considerations the manager must consider before accepting this

order.

1. Have we ever done business overseas? Exports require additional

administrative activities. Have these additional administrative costs been

considered in the differential analysis?

4. Will the overseas customer want to do business in the future, or is this just a

single sale? If the overseas customer is expected to purchase more golf balls

in the future, then it is likely that the customer will come to expect the $22 price

in the future.

6. Will we help the overseas customer establish a presence in the overseas golf ball

market where we may want to compete in the future?

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

TIF 25–5 (FIN MAN); TIF 11–5 (MAN)

First, Marriott has excess capacity for this day, so it should be willing to accept

additional customers. The Priceline.com customer generates incremental revenue

that will not reduce other business. Given this, however, the price must at least cover

variable cost; otherwise, Marriott will incur a loss. The variable cost per room night is

as follows:

Housekeeping labor cost …………………………………………………………………..

$38

These costs are mostly avoidable or are variable to room nights. This answer assumes

Note to Instructors: There could be some discussion about the degree to which some of

these costs are fully variable. For example, it’s likely that some utility cost must be

TIF 25–6 (FIN MAN); TIF 11–6 (MAN)

The product profitability report indicates that the two products are equal in terms

of profitability (on a per-case basis). However, the additional information indicates

that there will be more activities required for Jamaican Punch than for King Kola.

Apparently, the factory overhead costs are being allocated on the basis of a single

activity base that does not capture these product differences. Because the direct

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. d. The cost of the crane to move materials would most likely be treated as a sunk

cost in differential cost analysis as this cost is not likely to differ among

alternatives.

2. c. If Johnson accepted the special order, the company’s operating income would

increase by $37,500, computed as follows.

3. d. For Aril to benefit from purchasing the units rather than making the units, the purchase

price must be less than $14, computed as follows.

Remaining fixed cost/unit

=

($150,000 × 60%) ÷ 30,000

=

$3

=

$3 + $11

4. b. Oakes should continue to process Beracyl as the incremental revenue exceeds

the incremental cost of processing; Mononate should be sold at split-off as the

incremental revenue is less than the incremental cost of further processing.