Financial Accounting, 9/e 11-1

Chapter 11

Reporting and Interpreting Stockholders’

Equity

ANSWERS TO QUESTIONS

1. A corporation is a legal entity separate and distinct from its owners. Owners are those

who hold stock in the corporation. The primary advantages of the corporate form are:

2. The charter of a corporation, sometimes called the articles of incorporation, is a

legal document issued by a state that authorizes the creation of a corporation as a

3. (a) Authorized shares: The maximum number of shares of stock that a corporation

can issue as specified in the charter of the corporation.

4. Common stock—the usual or normal stock of a corporation. It is the voting stock

and generally ranks after the preferred stock for dividends and assets distributed

upon dissolution. Common stock may have a par value or be no-par value common

stock.

5. Par value is a nominal value per share established in the corporate charter. The

original purpose of establishing a par value was to protect creditors by specifying a

6. When stock with a par value is issued, the par value times the number of shares is

credited to the stock account, and any “additional capital” raised is credited to the

additional paid-in capital account. Thus, the “additional paid-in capital” account

reflects capital raised in excess of a stock’s par value.

7. The stockholders’ equity section of the balance sheet reflects two kinds of capital:

contributed capital and earned capital.

Contributed capital—the amount invested by stockholders. Contributed capital is

8. Treasury stock is a corporation’s own stock that was sold (issued) and

subsequently reacquired by the corporation. Corporations frequently repurchase

shares of their own stock for sound business reasons, such as to obtain shares

needed for employees’ bonus plans, to influence the market price of the stock, to

9. Treasury stock is reported in the stockholders’ equity section of the balance sheet

as a negative amount reflecting its status as a contra-equity account. Any “gain” on

Financial Accounting, 9/e 11-3

10. The two basic requirements to support a cash dividend are: (1) cash on hand or the

11. A stock dividend involves the issuance of additional shares of stock to

stockholders. It differs from a cash dividend in that it does not distribute any assets

of the corporation to stockholders. A cash dividend also reduces total stockholders’

equity by the amount of the dividend. In contrast, a stock dividend does not change

total stockholders’ equity.

12. A stock split distributes additional shares of stock to stockholders by “splitting” their

existing shares into some multiple of additional shares. Though a stock split and a

13. With respect to dividends, the three important dates are:

Declaration date—the date on which the board of directors votes to declare a

dividend. The declaration of a cash dividend creates a liability, and must be

14. Several characteristics typically associated with preferred stock are: (1) lack of

voting rights, (2) less risky than common stock since in the event of bankruptcy

preferred stockholders have preferential rights to assets over common

stockholders, and (3) a fixed dividend rate. Preferred stock may also have a

dividend preference and it may be cumulative.

15. Cumulative preferred stock has a dividend preference such that, should the

dividends on the preferred stock for any year, or series of years, not be paid,

11-4 Solutions Manual

ANSWERS TO MULTIPLE CHOICE

Authors’ Recommended Solution Time

(Time in minutes)

Mini exercises

Exercises

Problems

Alternate

Problems

Cases and

Projects

No.

Time

No.

Time

No.

Time

No.

Time

No.

Time

15

45

45

30

15

45

30

30

30

45

30

20

30

60

35

20

20

30

20

20

30

45

30

15

45

30

20

10

10

15

10

11

20

11

30

12

20

12

45

13

20

14

30

15

30

16

30

17

20

18

30

* Due to the nature of this project, it is very difficult to estimate the amount of time

students will need to complete the assignment. As with any open-ended project, it is

possible for students to devote a large amount of time to these assignments. While

students often benefit from the extra effort, we find that some become frustrated by the

perceived difficulty of the task. You can reduce student frustration and anxiety by

MINI- EXERCISES

M11–1.

At the end of each accounting period, retained earnings is computed via the following

M11–2.

178,000 issued (168,000 outstanding + 10,000 in treasury)

M11–3.

M11–4.

Cash (+A) (170,000 $21) …………………………………………….

3,570,000

Common Stock (+SE) (170,000 $1) ………………………….

170,000

Additional Paid-in Capital (+SE) (remainder) ………………..

3,400,000

Common Stock (+SE) (170,000 $2) …………………………

Additional Paid-in Capital (+SE) (remainder) ………………..

Financial Accounting, 9/e 11-7

M11–5.

Common stock is the basic voting stock issued by a corporation, but ranks behind

M11–6.

Assets

Liabilities

Stockholders’

Equity

Net Income

$250,000

Purchased

20,000 shares

of treasury

Decrease by

$900,000

No change

Decrease by

$900,000

No change

M11–7.

200,000 shares outstanding X $0.65

=

$130,000

M11–8.

April 15:

Retained Earnings (-SE) (100,000 x $0.65) ……………………..

65,000

Dividends Payable (+L) ……………………………………………..

65,000

Dividends Payable (-L) ………………………………………………….

65,000

Cash (-A) ……………………………………………………….

65,000

M11–9.

Dividend Yield = Dividends per share / Market price per share

M11–10.

Stock Dividend

Stock Split

No change in assets

No change in assets

No change in liabilities

No change in liabilities

Increase in common stock

No change in common stock

amount.

Decreases market value

Decrease in market value

M11–11.

EVENT

EFFECT ON STATEMENT OF CASH FLOWS

Issued stock

Financing cash flow increase

Repurchased stock

Financing cash flow decrease

Declared a cash dividend

No effect (when declared)

Financial Accounting, 9/e 11-9

EXERCISES

E11–1.

Computation of end of year balance for treasury stock:

Beginning balance 7,171,269

Net increase 3,034,188

E11–2.

Req. 1 The number of authorized shares is specified in the corporate charter: 300,000.

E11–3.

Req. 1

Stockholders’ Equity

Common stock, authorized 103,000 shares,

issued and outstanding, 20,000 shares …………………………………………….

$200,000

Preferred stock, authorized 4,000 shares,

issued and outstanding, 3,000 shares ………………………………………………

Req. 2

The answer would depend on the profitability of the company and the stability of its

earnings. The preferred stock has a 9% dividend rate. If the company earns more than

E11–4.

Req. 1 ($30 x 90,000 shares issued) – $1,600,000 in common stock = $1,100,000

E11–5.

Req. 1

a.

Cash (+A) (5,600 shares x $20) ……………………………………..

112,000

Financial Accounting, 9/e 11–11

Common stock (+SE) (5,600 shares x $10) ………………….

56,000

Additional paid-in capital, common stock (+SE) …………….

56,000

Sold common stock for $20 per share.

Req. 2

Stockholders’ Equity

Common stock, $10 par value, 11,500 shares authorized,

6,600 shares outstanding …………………………………………………………..

$ 66,000

E11–6.

Req. 1

Common stock, class A at par value: 118,529,925 X $0.01 = $118,530

Req. 2

Req. 3

Retained earnings last year: $3,107,344,000 minus net income for the current year

E11–6 (continued).

Req. 4

Cash (+A) (1,000 shares x $25) …………………………………….

25,000

Common stock (+SE) (1,000 shares x $10) ………………….

10,000

Additional paid-in capital, common stock (+SE) …………….

15,000

Sold common stock for $25 per share.

As of the end of the current year, treasury stock had decreased corporate resources by

$1,846,312,000.

Req. 5

E11–7.

Req. 1

a.

Cash (+A) (50,000 shares x $50) ……………………………………

2,500,000

Common stock (+SE) (50,000 shares x $2 par value) …….

100,000

Additional paid-in capital, common stock (+SE) …………….

2,400,000

Sold common stock for $50 per share.

b.

Treasury stock (+XSE, –SE) (2,000 shares x $52) …………….

Cash (-A) …………………………..…………………………………….

104,000

Bought treasury stock for $52 per share.

50,000 shares issued ………………………………………………………………..

2,400,000

)

Financial Accounting, 9/e 11–13

E11–8.

Stockholders’ equity:

Dec. 31,

2014

Dec. 31,

2013

E11–9.

Stockholders’ Equity

Common stock, $10 par value, 98,000 shares authorized,

78,000 shares issued ………………………………………………………………..

780,000

Preferred stock, 8%, $50 par value, 59,000 shares authorized,

20,000 shares issued and outstanding …………………………………………

$1,000,000

Additional paid-in capital, common stock …………………………………………

Additional paid-in capital, preferred stock ………………………………………..

Retained earnings* …………………………………………………………………..

160,000

E11–10.

Net income: $942,000 – $800,000 – $80,000 – $15,000 = $47,000

EPS = $47,000 / 132,000 shares = $0.36

Additional paid-in capital

Accumulated deficit

(59,487,000)

11–14 Solutions Manual

E11–11.

Req. 1

a.

Cash (+A) (20,000 shares x $20) ……………………………………

400,000

Common stock, no-par (+SE) ……………………………………..

400,000

E11–12.

Req. 1

The number of shares that have been issued is computed by dividing the common stock

Retained earnings end of 2013 …………

Net income for 2014 ……………………….

Dividends for 2014 ………………………….

)

Retained earnings end of 2014 …………

b.

Cash (+A) (6,000 shares x $40) …………………………………….

Common stock, no-par (+SE) …………………………………….

c.

Cash (+A) (7,000 shares x $30) ……………………………………..

210,000

Preferred stock (+SE) (7,000 shares x $10) ………………….

Additional paid-in capital, preferred stock (+SE) ……………

140,000

Financial Accounting, 9/e 11–15

E11–13.

Req. 1

Assets will decrease by $329,000,000 ($47 x 7 million shares) and stockholders’ equity

will decrease by $329,000,000. Liabilities are not affected.

Req. 2

Treasury stock (+XSE, -SE) (7 m shares x $47) ……………….

329,000,000

E11–14.

Req. 1

Stockholders’ Equity

Common stock, $20 par value, 100,000 shares authorized,

34,000 shares issued, 32,000 shares outstanding ………………………..

$680,000

Additional paid-in capital ……………………………………………………………..

163,000

Retained earnings …………………………………………………………………….

89,000

Treasury stock …………………………………………………………………………..

(25,000)

Total Stockholders’ Equity …………………………………………………….

$907,000

Req. 2

E11–15.

Req. 1

a.

Treasury stock (+XSE, –SE) (200 shares x $20) ……………….

4,000

Cash (-A) …………………………..…………………………………….

4,000

Bought treasury stock for $20 per share.

Cash (-A) …………………………………………………………………

Bought treasury stock for $47 per share.

Treasury stock (-XSE, +SE) (40 shares x $20) ……………..

800

Additional paid-in capital (+SE) …………………………………..

200

Sold treasury stock for $25 per share.

c.

Cash (+A) (30 shares x $15) ………………………………………….

450

Additional paid-in capital (-SE) ……………………………………….

150

Treasury stock (-XSE, +SE) (30 shares x $20) …………….

600

Sold treasury stock for $15 per share.

Req. 2

Treasury stock transactions do not affect the income statement. A firm may resell

treasury shares for more or less than the original purchase price, but for accounting

purposes the difference is not a gain or loss.

E11–16.

Req. 1

Feb. 1:

Treasury stock (+XSE, –SE) (160 shares x $20) …………….

3,200

Cash (-A) ………………………………………………………………

3,200

July 15:

Cash (+A) (80 shares x $21) ……………………………………..

1,680

Treasury stock (-XSE, +SE) (50 shares x $20) …………..

1,600

Additional paid-in capital (+SE) ………………………………..

Sept. 1:

Cash (+A) (50 shares x $19) ………………………………………

950

Additional paid-in capital (-SE) …………………………..………

50

Treasury stock (-XSE, +SE) (50 shares x $20) …………..

1,000

.

Req. 3

Financial Accounting, 9/e 11–17

The sale of treasury stock for more or less than its original purchase price does not

E11–17.

Req. 1

Case 1: When the company pays the dividend, it will be recorded on the statement

of cash flows as a financing activity cash outflow.

Req. 2

Case 1: Since there is no effect on net income or the weighted number of

commons shares outstanding, EPS is not affected.

E11–18.

Req. 1

Preferred

(5,000

Shares)

Common

(50,000

Shares)

Total

a)

Noncumulative:

Preferred ($50,000 x 10%) ………………………………..

$ 5,000

$ 5,000

Balance to common ($85,000 – $5,000) ……………..

$80,000

80,000

$ 5,000

$80,000

$85,000

Per share ……………………………………………………….

$1.00

$1.60

b)

Cumulative:

Preferred, arrears ($50,000 x 10% x 2 years) ………

$ 10,000

Preferred, current year ($50,000 x 10%) ……………..

5,000

Balance to common ($85,000 – $10,000 – $5,000)

$70,000

70,000

$15,000

$70,000

$85,000

Per share ……………………………………………………….

$3.00

Req. 2

Since the total dividend ($85,000) does not change under the two assumptions, the

statement of cash flow is impacted in the same manner across the two independent

assumptions. Under both assumptions, the company would report an $85,000 financing

activities cash outflow.

E11–19.

Item

Effect of Cash Dividend (Preferred)

Effect of Stock Dividend (Common)

Assets

–No effect on declaration date.

–Decreased by the amount of the

dividend ($7,200) on payment

date.

No effect because no assets are

disbursed.

–Increased on declaration date

($7,200).

date because no contractual liability

is created (no assets are

disbursed).

dividend on declaration date

(retained earnings decreased by

$7,200).

–Retained earnings reduced and

contributed capital increased by

same amount ($120,000).

Financial Accounting, 9/e 11–19

E11–20.

February 20

Retained earnings (-SE) (191.2 m shares x $1.20) ……………

229,440,000

Dividends payable (+L) ………………………………………………

229,440,000

Declaration of dividend.

March 1

E11–21.

October 1

Retained earnings (-SE) (3 b shares x $2.45) …………………..

7,350,000,000

Dividends payable (+L) ……………………………………………..

7,350,000,000

Dividends payable (-L) ………………………………………………….

Cash (-A) ……………………………………………………….

Dividend payable (-L) …………………………..……………………….

229,440,000

Cash (-A) …………………………………………………………………

229,440,000

Payment of dividend.

Treasury stock ………………….

Shares outstanding …………..

11–20 Solutions Manual

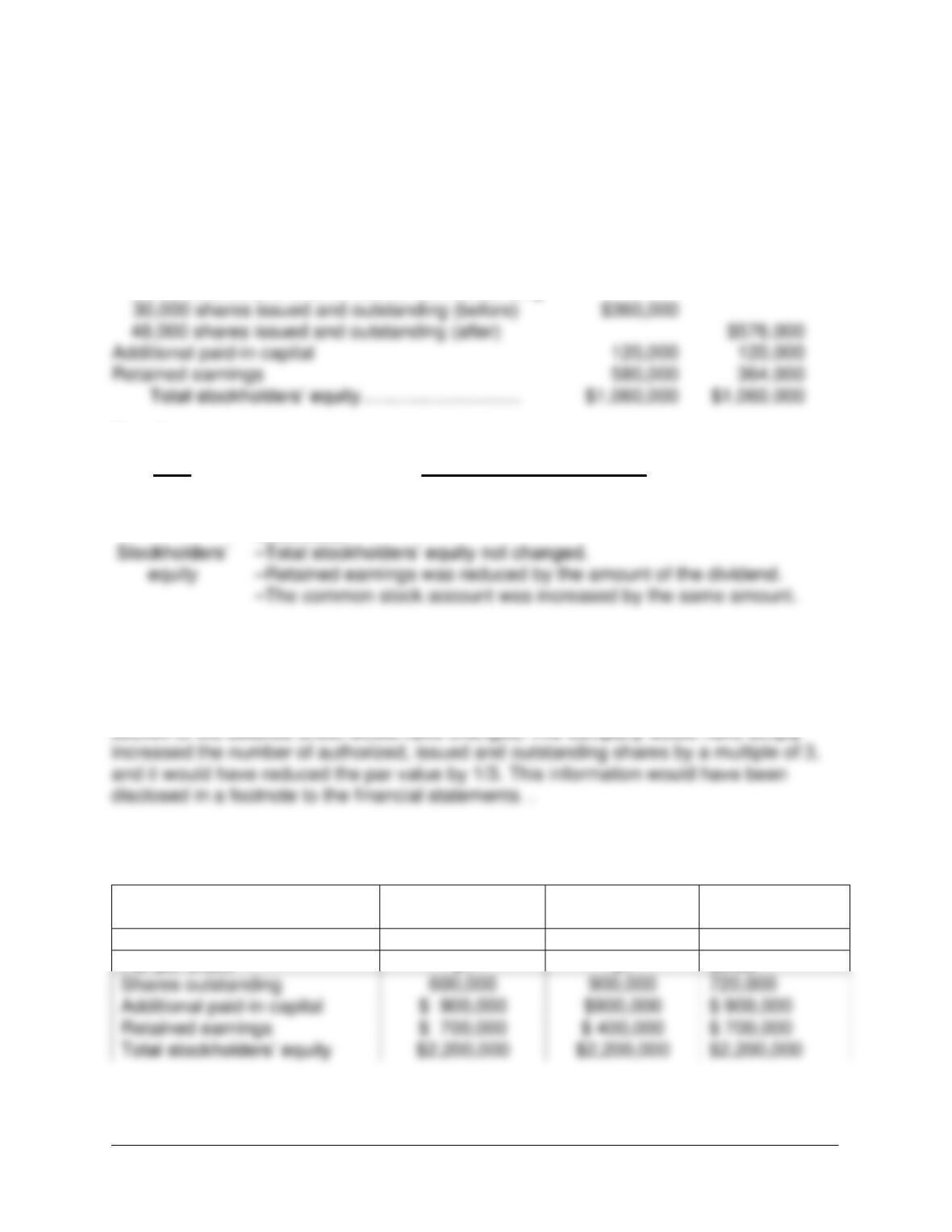

E11–22.

Req. 1

Stockholders’ Equity

Before Stock

Dividend

After Stock

Dividend

Common stock, $12 par value; 65,000 shares

authorized, 30,000 shares issued and outstanding

Req. 2

Item

Effects of Stock Dividend

Assets

No change because no assets were disbursed.

Liabilities

No change because no liability was created (no assets were to be

disbursed).

Req. 3

If the company had announced a stock split, no amounts in the stockholders’ equity

E11–23.

Comparative results:

Items

Before Dividend

and Split

After Stock

Dividend

After Stock

Split

Common stock account

$600,000

$900,000

$600,000

Par per share

$1

$1

$0.83

Shares outstanding

Additional paid-in capital

Retained earnings

$ 700,000

$2,200,000

48,000 shares issued and outstanding (after)

Additional paid-in capital

Retained earnings