CHAPTER 11

COST BEHAVIOR AND

COST-VOLUME-PROFIT ANALYSIS

CLASS DISCUSSION QUESTIONS

1. Total variable costs vary in direct proportion

to changes in the level of activity. Unit varia-

ble costs remain the same with changes in

the level of activity.

4. a. Fixed costs

b. Fixed costs

c. Fixed costs

5. Mixed costs are separated into their fixed

and variable cost components.

6. (b)

7. (a)

8. (b)

10. a. No impact on the contribution margin.

b. Income from operations would decrease.

11. A high contribution margin ratio, coupled

with idle capacity, indicates a potential for

sales promotion campaign should be con-

sidered in order to expand sales to maxi-

mum capacity and to take advantage of the

low ratio of variable costs to sales.

sales than did Cheddar Company. Such a

situation resulted in a lower break-even

point for Gouda Company.

15. CVP analysis depends on five primary as-

sumptions. They are (1) total sales and total

costs can be represented by straight lines;

(2) within the relevant range of operating ac-

tivity, the efficiency of operations does not

change; (3) costs can be accurately divided

These components are weighted by the

sales mix percentages.

17. Operating leverage measures the relative

mix of a business’s variable costs and fixed

costs. It is computed as follows:

332

EXERCISES

E11–1

1. Variable

2. Variable

9. Variable

10. Mixed

E11–2

a. Cost Graph Three

d. Cost Graph Two

E11–3

1. a

2. b

E11–4

1. g

2. d

3. f *

E11–5

a. Variable

b. Fixed

g. Variable

h. Variable

334

E11–6

Components produced … 500,000 650,000 800,000

Total costs:

Total variable costs … $ 900,000 (d) $1,170,000 (j) $1,440,000

Total fixed costs ……… 1,560,000 (e) 1,560,000 (k) 1,560,000

Supporting calculations:

a. $1.80 ($900,000 ÷ 500,000 disks)

b. $3.12 ($1,560,000 ÷ 500,000 disks)

c. $4.92 ($1.80 + $3.12)

d. $1,170,000 ($1.80 × 650,000 disks)

e. $1,560,000 (fixed costs do not change with volume)

f. $2,730,000 ($1,170,000 + $1,560,000)

E11–7

a. Variable Cost per Unit =

Production in Difference

Costs Total in Difference

=

units000,45 –– units 000,70

000,535,1$–– 000,110,2$

Highest level:

$2,110,000 = ($23 × 70,000 units) + Fixed Cost

$2,110,000 = $1,610,000 + Fixed Cost

$500,000 = Fixed Cost

Lowest level:

$1,535,000 = ($23 × 45,000 units) + Fixed Cost

$1,535,000 = $1,035,000 + Fixed Cost

336

E11–8

Gross-Ton Mile =

Miles Ton–Gross in Difference

Costs Total in Difference

The fixed cost can be determined by subtracting the estimated total variable cost

from the total cost at either the highest or lowest level of gross-ton miles, as fol-

lows:

Total Cost = (Variable Cost per Gross-Ton Mile × Gross-Ton Miles) + Fixed Cost

Highest level:

$2,095,800 = ($9.56 × 180,000 gross-ton miles) + Fixed Cost

Variable Cost per

E11–9

a.

Sales ………………………………. $11,750,000

Variable costs …………………. 6,815,000

Contribution margin ………… $ 4,935,000

b.

Sales ………………………………. $6,440,000

Contribution margin ratio … × 35%

E11–10

a.

Sales ………………………………………………………………………………………… $ 27,006

Variable costs:

b.

Contribution Margin Ratio =

Sales Variable Costs

Sales

−

=

$27,006

$14,318

= 53.0%

c. Same-store sales increase …………………………………….. $800,000,000

338

E11–11

a. Break-Even Sales (units) =

Margin onContributiUnit

Costs Fixed

=

$6.25 –– $8.00

$1,750,000

= 1,000,000 units

E11–12

a. Break-Even Sales (units) =

Margin onContributiUnit

Costs Fixed

=

432

1

$13.10 –– $46.83 –– $100.46

00$970,250,0

= 23,939,057 barrels

The variable costs per unit are determined by multiplying the total amount of

each cost by the variable cost percentage (80% for production costs and 45%

for marketing and distribution costs), then dividing by the number of barrels.

339

E11–13

a. Break-Even Sales (units) =

arginM onContributiUnit

Costs Fixed

arginM onContributiUnit

Costs Fixed

E11–14

Break-Even Sales (units) =

arginM onContributiUnit

Costs Fixed

=

$X –– 40$

000,40$

= 8,000 cookbooks

340

E11–15

The cost of the promotion campaign is the fixed cost in this analysis, since we’re

trying to determine the break-even adoption rate of the campaign.

Promotional cost = $20,900,000

Note: The variable cost is for 18 months since the costs are incurred, even for the

2 free months.

The break-even number of subscribers necessary to cover the fixed cost of the

promotion would be computed as follows:

341

E11–16

a. Break-Even =

Accountper Cost Variable–– Accountper Revenue

Cost Fixed

=

21

3

$378.08 –– $722.73

$15,952.6

= 46.3 million (rounded) accounts

1Revenue per account (in millions):

$33,679 ÷ 46.6 = $722.73

3Fixed costs (in millions):

Cost of revenue ……………………………. $19,015 × 25% $ 4,753.8

Selling, general, and administrative

expenses ………………………………….. $9,592 × 65% 6,234.8

Depreciation ………………………………… $4,964 × 100% 4,964.0

Total fixed costs …………………………... $ 15,952.6

Accountper Cost Variable–– Accountper Revenue

Cost Fixed

Note to Instructors: The rate charged per minute and the number of average

minutes of digital service influence the revenue per account. An interesting

question is whether the costs are variable to the number of minutes or num-

ber of accounts. If we assume that the costs are variable to the number of

342

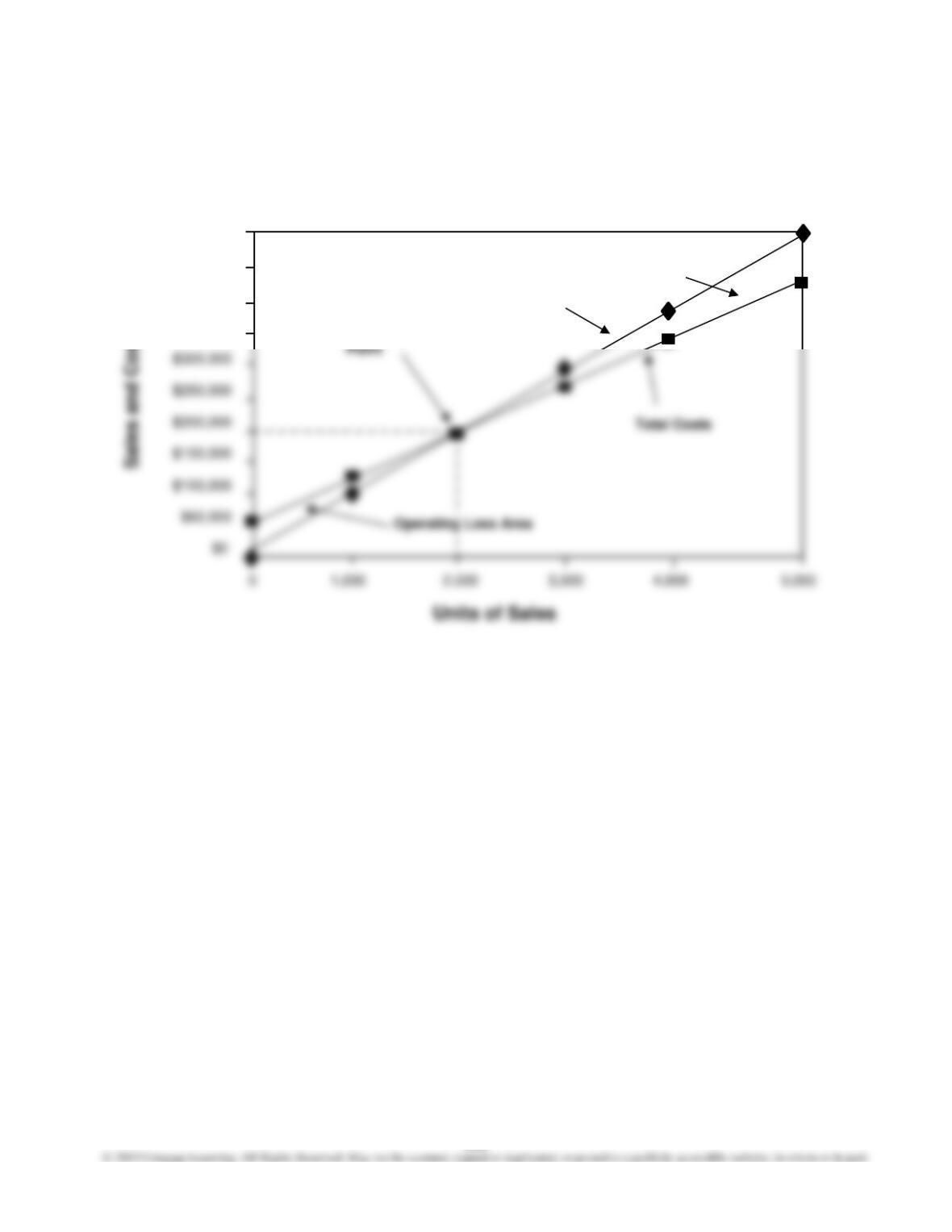

E11–17

a.

b. $200,000 (the intersection of the total sales line and the total costs line)

c. The graphic format permits the user (management) to visually determine the

break-even point and the operating profit or loss for any given level of sales.

$500,000

$450,000

$400,000

$350,000

Break-Even

Total

Sales

Operating

Profit Area

343

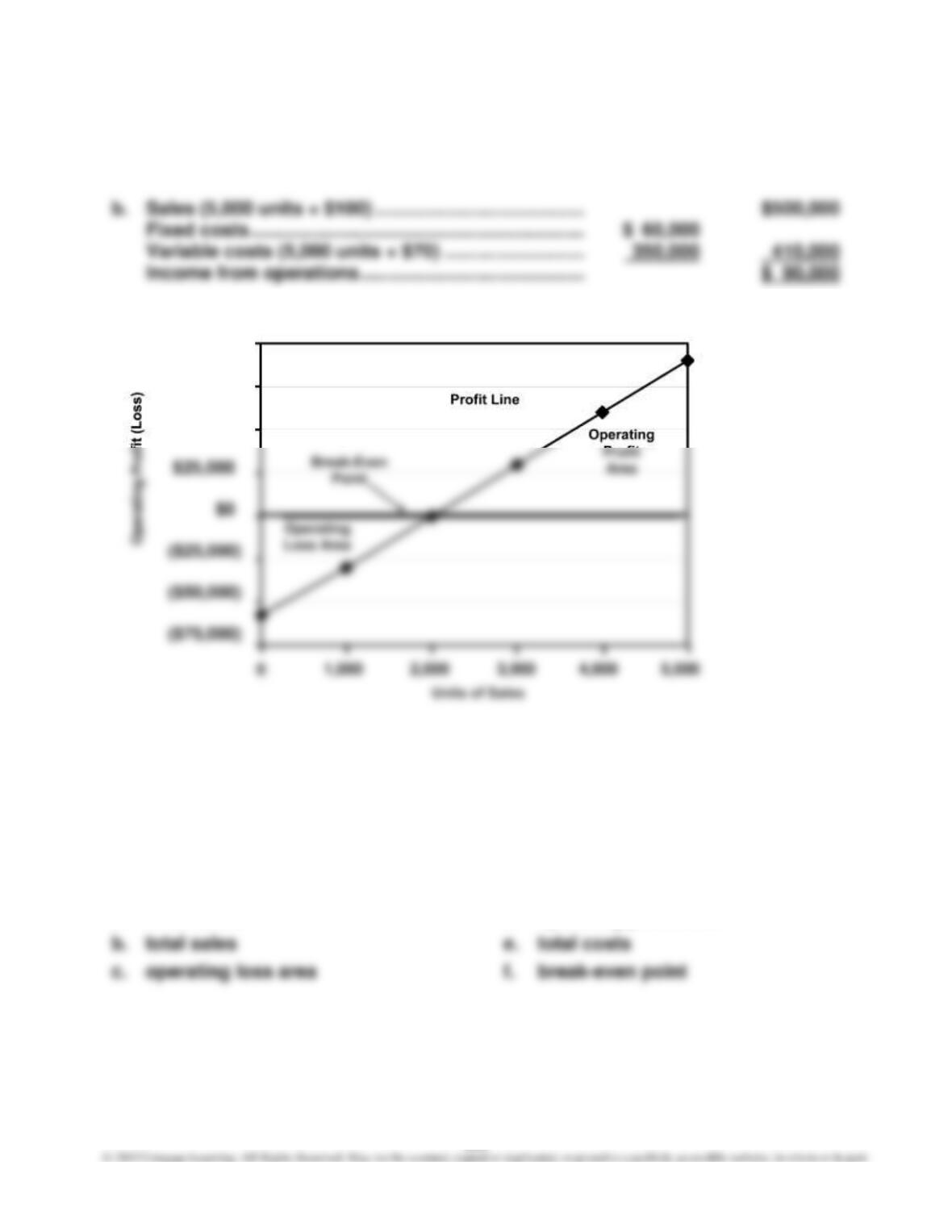

E11–18

a. $60,000 (total fixed costs)

c.

d. 2,000 units (the intersection of the profit line and the horizontal axis)

E11–19

Cost-volume-profit chart

a. fixed costs

d. operating profit area

$100,000

$75,000

$50,000

344

E11–20

Profit-volume chart

a. fixed costs

b. operating profit area

E11–21

a. Unit Selling Price of E = ($30.00 × 0.65) + ($250.00 × 0.35)

= $19.50 + $87.50 = $107.00

Unit Variable Cost of E = ($20.00 × 0.65) + ($150.00 × 0.35)

b. 104,000 game players (160,000 units × 0.65)

56,000 tablets (160,000 units × 0.35)

E11–22

a. Unit contribution margin of overall product (E):

Unit selling price of E [(10% × $750) + (90% × $300)] ………………….. $345

Unit variable cost of E [(10% × $50) + (90% × $20)] …………………….. 23

Unit contribution margin of E ……………………………………………………. $322

E11–23

a. (1) $875,000 ($4,375,000 – $3,500,000)

(2) 20% ($875,000 ÷ $4,375,000)

b. The break-even point (S) is determined as follows:

Sales = $2,800,000 + 75% Sales

346

E11–24

If 190,000 units were sold and sales at the break-even point are 215,000 units,

there is no margin of safety.

E11–25

a. Socket Inc.:

Operating Leverage =

Operations from Income

Margin onContributi

Operations from Income

Margin onContributi

b. Socket Inc.’s income from operations would increase by 90% (3.0 × 30%), or

$135,000 (90% × $150,000), and Wrench Inc.’s income from operations would

increase by 75% (2.5 × 30%), or $240,000 (75% × $320,000).