348

P11–2, Concluded

8. The possibility of increasing operating income by $1,650,000 (from $43,140,000

to $44,790,000) is a positive point for the proposal. However, there are many

points against the proposal, including the following:

a. The break-even point increases by 24,000 units (from 112,400 to 136,400).

The company should determine the sales potential if the additional product is

349

P11–3

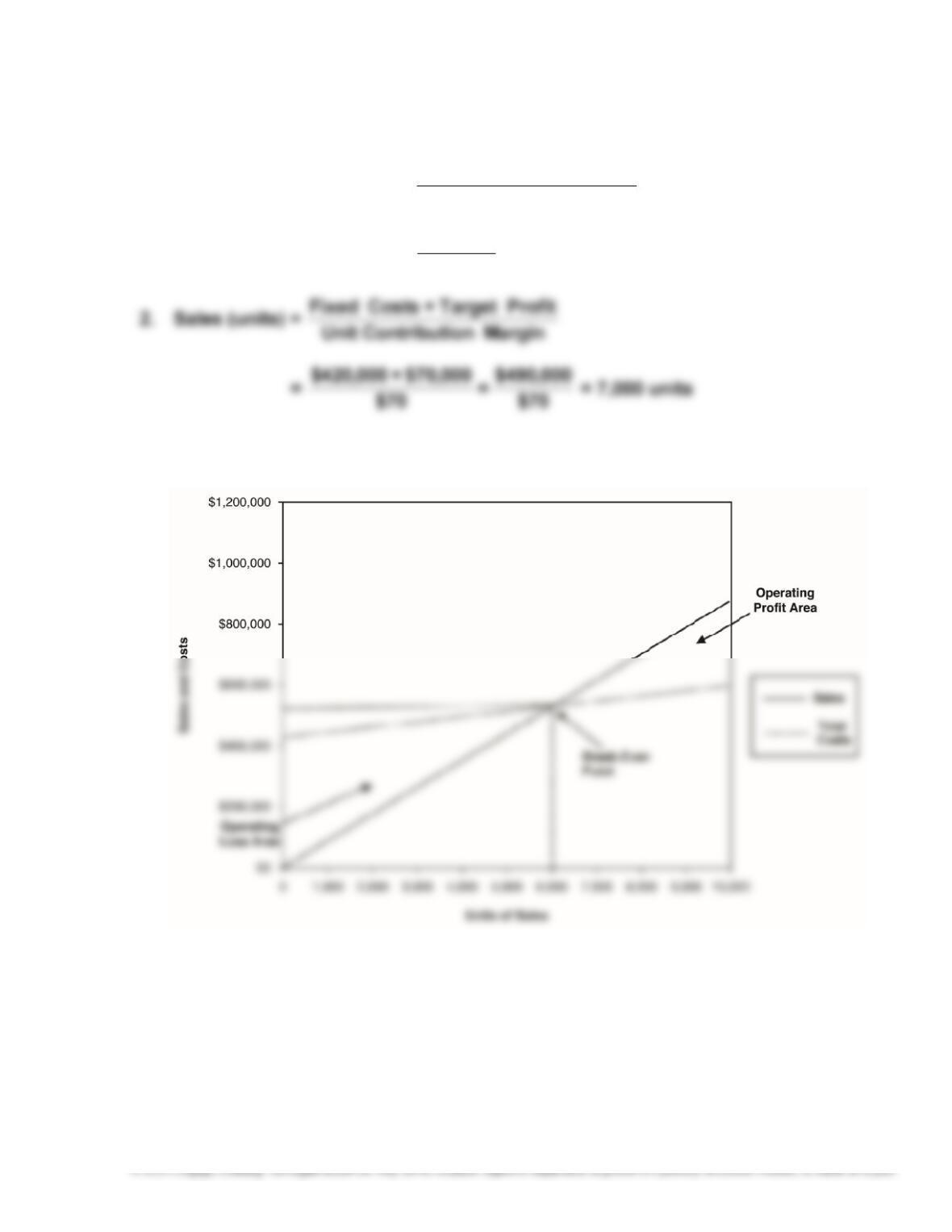

1. Break-Even Sales (units) = arginMonContributiUnit

CostsFixed

=

70$

000,420$ = 6,000 units

3.

4. $140,000 = [8,000 × ($85 – $15) – $420,000]

350

P11–4

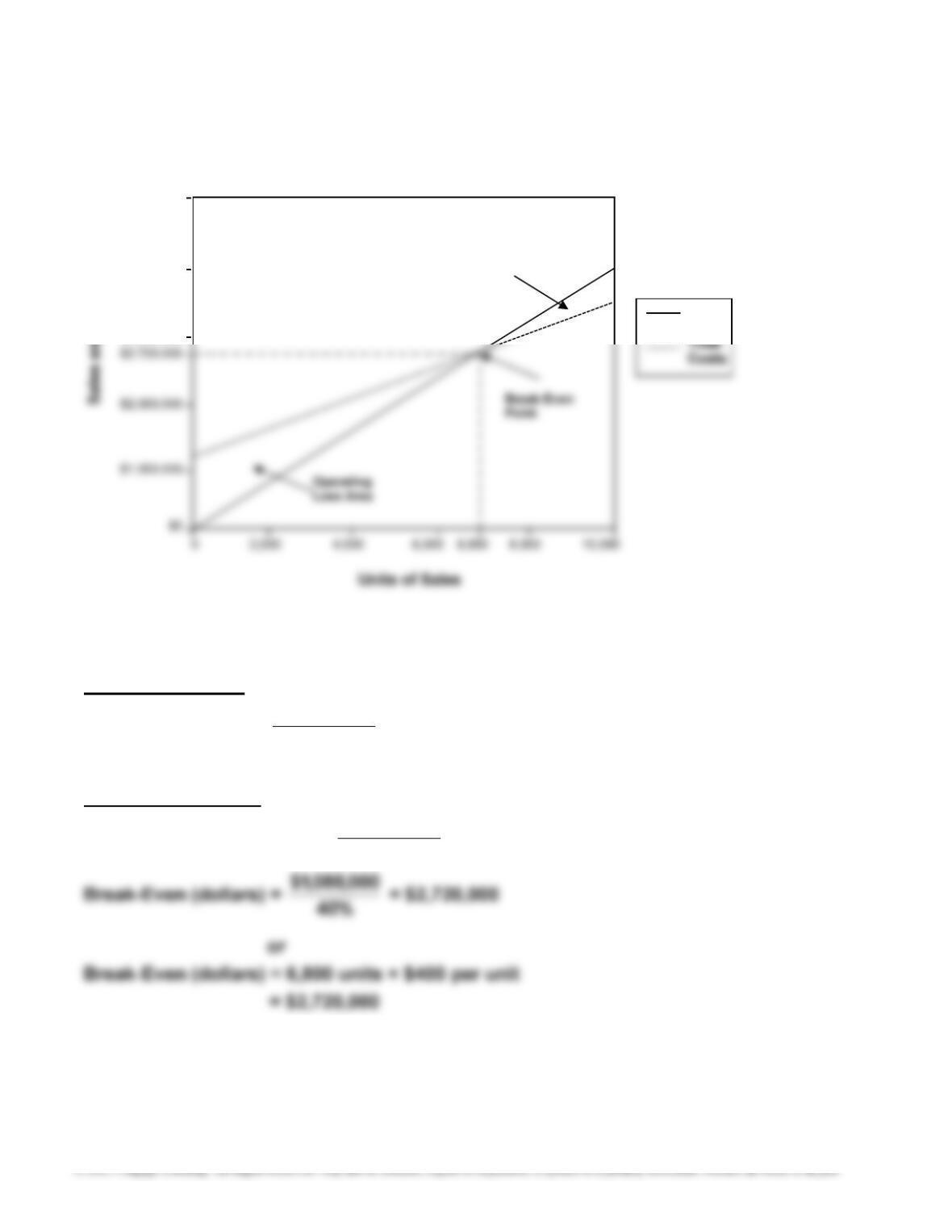

1.

Break-Even Units:

Break-Even (units) = $1,088,000

$400 – $240 = 6,800 units

Break-Even Dollars:

Contribution Margin Ratio = $400 – $240

$400 = 40%

$5,000,000

$4,000,000

$3,000,000

Operating

Profit Area

Sales

351

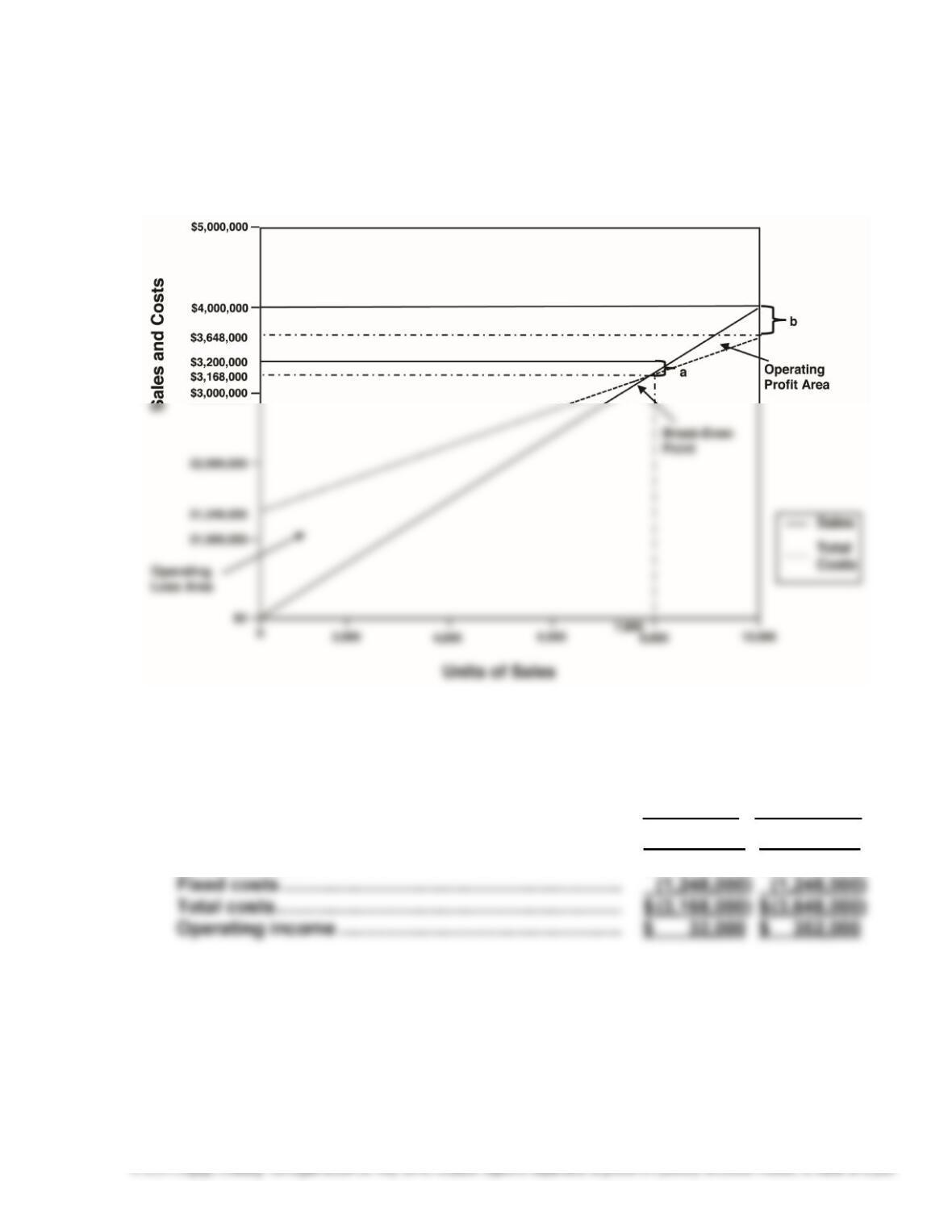

P11–4, Continued

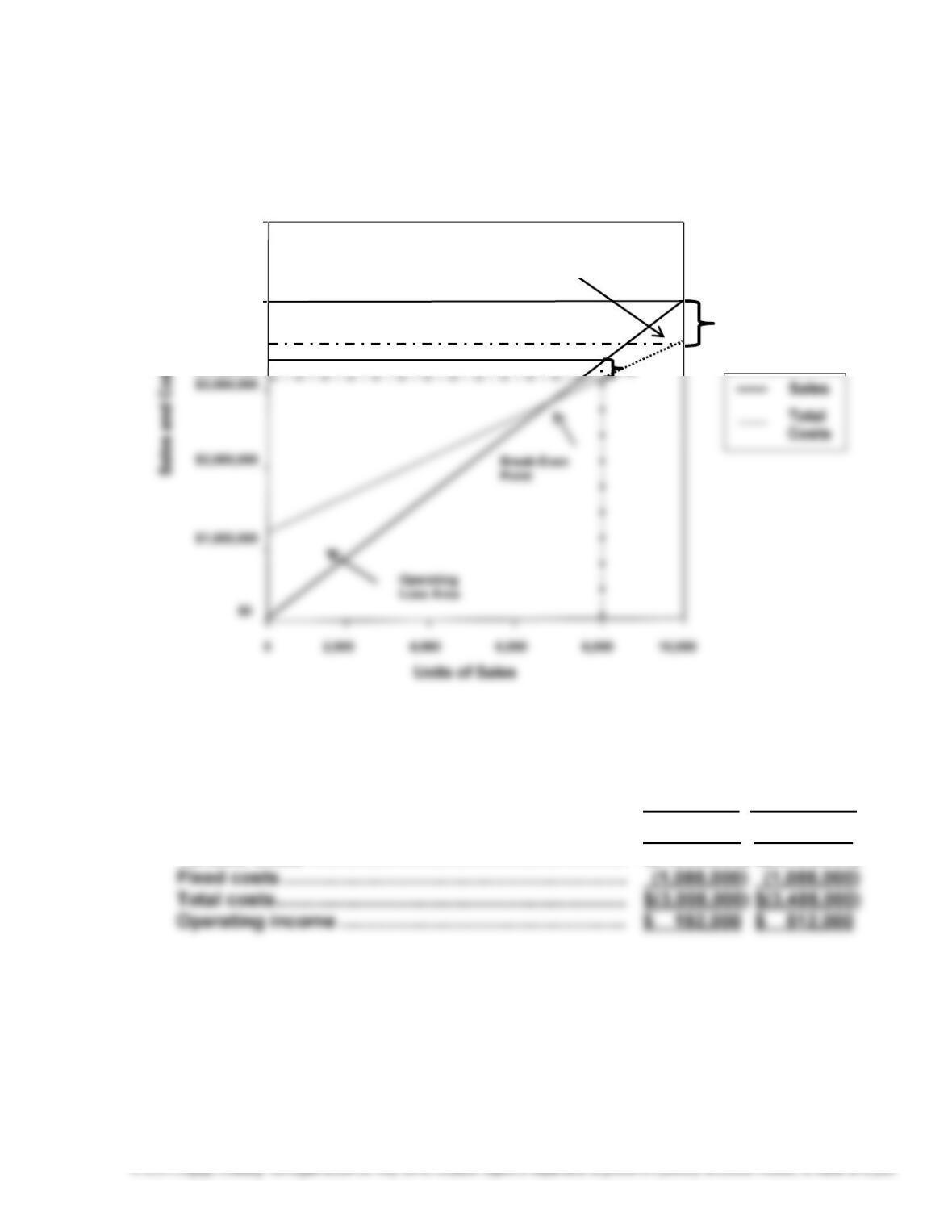

2.

Units sold: $3,200,000 ÷ $400 per unit = 8,000 units

a. b.

8,000 units 10,000 units

Sales …………………………………………………………………. $ 3,200,000 $ 4,000,000

$5,000,000

$4,000,000

$3,488,000

$3,200,000

b

Operating

Profit Area

352

P11–4, Continued

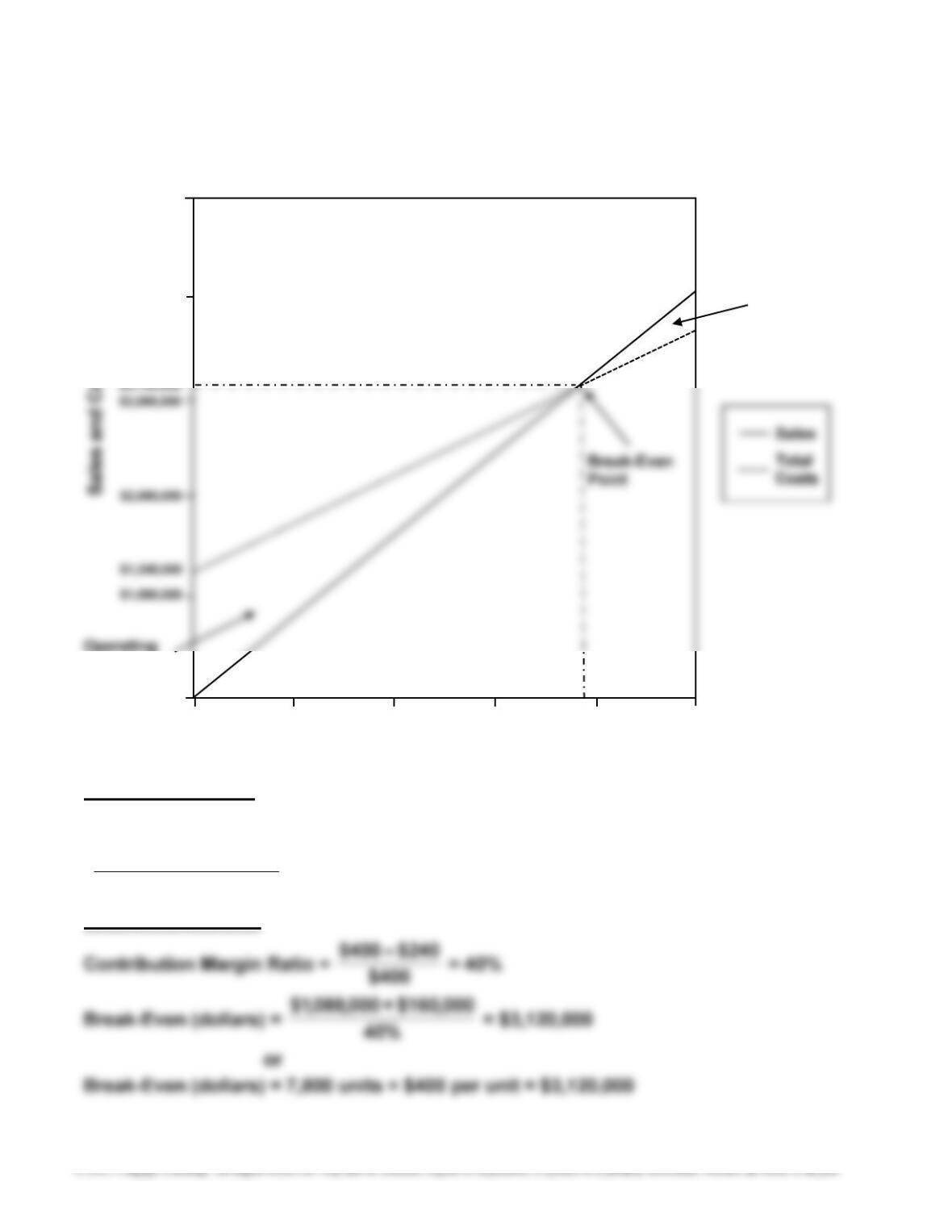

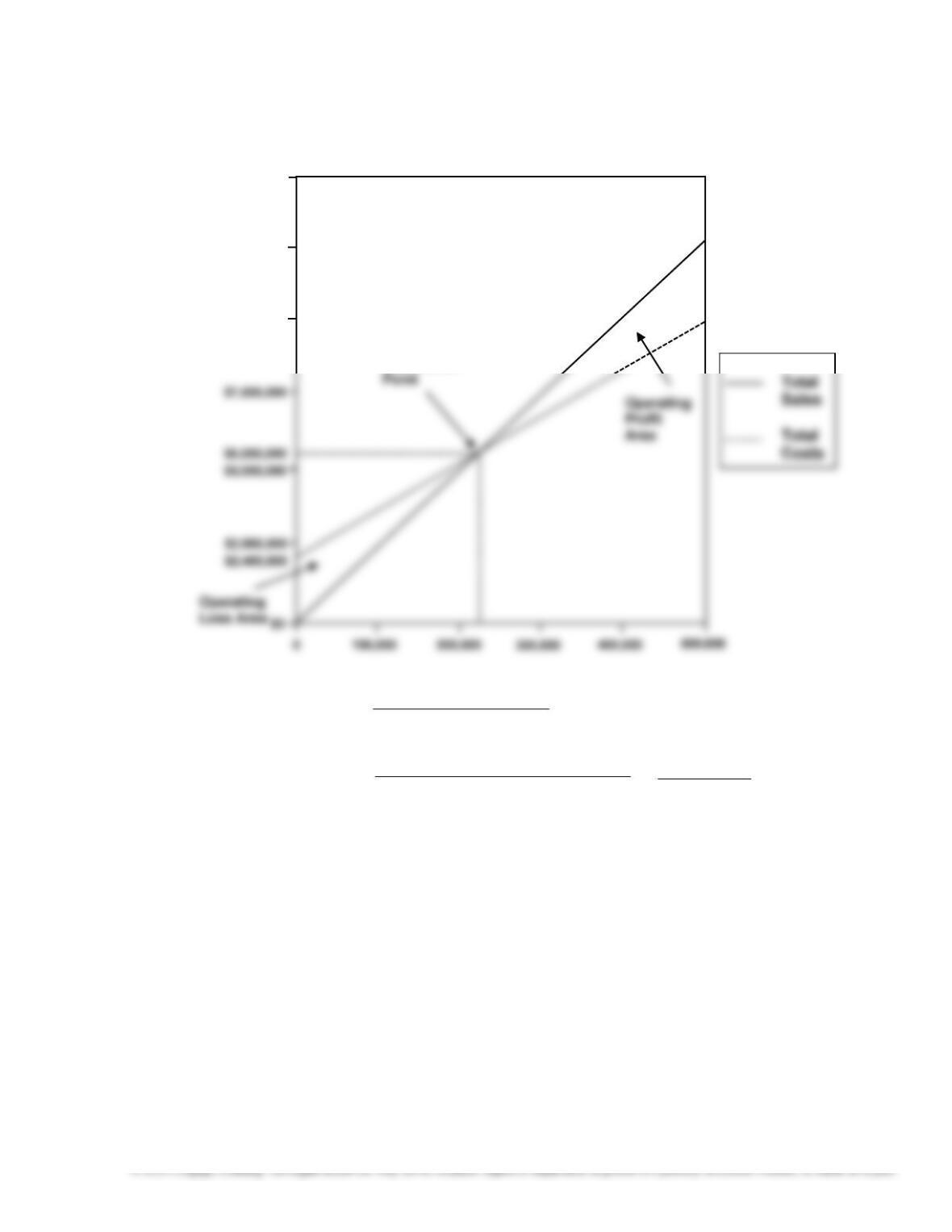

3.

Break-Even (units):

Break-even point: 7,800* units or $3,120,000

*240$–– 400$

000,160$+000,088,1$

Break-Even Dollars:

$5,000,000

$4,000,000

$0

02,000 4,000 6,000 8,000 10,000

7,800

Units of Sales

Loss Area

Operating

Profit Area

353

P11–4, Concluded

4.

a. b.

8,000 units 10,000 units

Sales ………………………………………………………………… $ 3,200,000 $ 4,000,000

Variable costs …………………………………………………… $ (1,920,000) $ (2,400,000)

354

P11–5

(Overall product is labeled E.)

1. Unit selling price of E [($400 × 80%) + ($800 × 20%)] …………….. $480

Unit variable cost of E [($240 × 80%) + ($480 × 20%)] ……………. 288

Unit contribution margin of E ……………………………………………… $192

3. Unit selling price of E [($400 × 20%) + ($800 × 80%)] …………….. $ 720

Unit variable cost of E [($240 × 20%) + ($480 × 80%)] ……………. 432

4. 5,000 units of E × 20% = 1,000 units of kayaks

5,000 units of E × 80% = 4,000 units of canoes

5. The overall enterprise break-even point decreased from 7,500 units to 5,000

units because the sales mix is weighted more toward the product with the

higher contribution margin per unit of product. Specifically, canoes have a

355

P11–6

1.

ORGANIC HEALTH CARE PRODUCTS INC.

Estimated Income Statement

For the Year Ended December 31, 20Y8

Sales (400,000 × $25) ………………………………….. $ 10,000,000

Cost of goods sold:

Direct materials (400,000 × $8) ……………….. $3,200,000

Expenses:

Selling expenses:

Advertising ………………………………………. $ 1,450,000

Sales salaries and commissions ……….. 833,0001

Travel ………………………………………………. 340,000

Miscellaneous selling expense ………….. 42,0002

Total selling expenses ………………….. $2,665,000

Administrative expenses:

Office and officers’ salaries ………………. $ 300,000

356

P11–6, Continued

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

3. Break-Even Sales (units) = Margin onContributiUnit

Costs Fixed

=

$2,400,000

$25–$15 = 240,000 units

357

P11–6, Concluded

4.

5. Operating Leverage =

Contribution Margin

Operating Income

=

[400,000 units × ($25 –– $15)]

$1,600,000 = 000,600,1$

000,000,4$ = 2.5

$12,500,000

$10,000,000

$9,900,000

$15,000,000

Break-Even

358

METRIC-BASED ANALYSIS

MBA 11–1

b. The break-even sales (dollars) is determined as follows:

Break-Even Sales (dollars) =

Total Fixed Costs

Contribution Margin Ratio

= $9,180,000

(100% –– 60%)

=

$9,180,000

40%

= $22,950,000

If the margin of safety is 15%, the actual sales are determined as follows:

MBA 11–2

If 1,250,000 units are sold and sales at the break-even point are 1,300,000 units,

there is no margin of safety.

359

MBA 11–3

1. Margin of Safety ($) = Current Sales Dollars – Break-Even Sales Dollars

= $11,003 (million) – $7,347 (million)

= $3,656 (million)

MBA 11–4

1. a. 6,300 game players (31,500 – 25,200)

b. $315,000 (6,300 players × $50)

c. 20% (6,300 players ÷ 31,500 players) or [$315,000 ÷ (31,500 players x $50)]

360

MBA 11–5

1. Margin of Safety (%) = Current Sales Dollars – Break-Even Sales Dollars

Current Sales Dollars

= $98,640,000 – (112,400 units × $246.60)

$98,640,000

=

$98,640,000 – $27,717,840

$98,640,000 = $70,922,160

$98,640,000

= 71.9%

MBA 11–6

1. Estimated unit sales …………………………………………. 400,000 units

Break-even point in units ………………………………….. 240,000

Margin of safety………………………………………………… 160,000 units

3. Margin

of Safety (%)

= Estimated Unit Sales – Break-Even Unit Sales

Estimated Unit Sales

361

CASES

Case 11–1

In an absolute sense, Phil’s actions are devious. He is clearly attempting to use

the first four-year scenario, which is favorable, as a way to market the partner-

ships. They are really longer-term investments. After the first four years, the risk

increases dramatically. The break-even occupancy becomes more difficult to

achieve at 92% than it does at 48%. Focusing on the 48% and remaining silent

about the increase to 92% is deceptive. One might argue “let the buyer beware.”

362

Case 11–2

The airline industry has a high operating leverage. This means that fixed costs

are a large part of the cost structure. The break-even volume is around 66% of

The airline strategy of raising ticket prices and consolidating routes may be a

successful strategy; however, there are a number of considerations. First, the

higher ticket prices would increase the revenue per passenger-mile and reduce

the break-even occupancy percentage only if it is assumed that there is no

change in passenger volume. However, this is unlikely. The revenue from price

The strategy of consolidating routes attacks a major cost of airlines. The number

of flights and terminals served drives fuel and airport ground- and terminal-

related costs. Therefore, consolidating routes by reducing the number of termi-

nals served and/or the number of flights is a method of achieving some econo-

mies of scale. For example, an airline could consolidate three flights departing in

the morning from Tulsa to Dallas into just two flights departing in the morning.

363

Case 11–3

Do-Nothing Strategy:

Revenue – Variable Costs – Fixed Costs = Profit

($75 × 800,000) – ($45 × 800,000) – $24,000,000 = Profit

$60,000,000 – $36,000,000 – $24,000,000 = $0

Thus, 800,000 units is the break-even volume.

Haley’s strategy, which is to maintain the current price but increase advertising

costs, will generate the highest profit.

Case 11–4

The direct labor costs are not variable to the increase in unit volume. The unit

volume is the wrong activity base for direct labor costs. The “number of impres-

sions” is a more accurate reflection of the direct labor cost. An impression is a

separate printing color application on the banners. Thus, the analysis should be

done as follows:

One Two Three Four

Color Color Color Color Total

364

Case 11–5

The Shipping Department manager should respond by pointing out that the activi-

ties performed by his department are related to sales orders and not sales volume.

The orders require inventory pulling and sorting activities as well as paperwork

Case 11–6

There are many possible applications of break-even analysis in a school envi-

ronment. Below are just a few possible ideas.

Break-Even Analysis Revenue Fixed Costs Variable Costs

1. Break-even number of

students in a class

Student tuition for

a class

Faculty salary,

space costs

Supplies, copying

2. Break-even sales in

the bookstore

Book sales Manager’s salary,

space costs

Cashier salaries,

cost of books

3. Break-even daily meal

Meal revenue Salaries, space Food costs