Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 11

Chapter 11

Current Liabilities and Payroll Accounting

QUESTIONS

1. A current liability is expected to be paid within one year or the company’s operating

3. The three questions are: (1) Who must be paid? (2) When is payment due? (3) How

much is to be paid?

7. The employee is responsible for federal income taxes, state income taxes, local

8. An employee’s gross earnings along with the number of withholding allowances that

9. An unemployment merit rating is based on an evaluation of an employer’s

experience in creating or avoiding unemployment with its employees. The merit

10. The obligation to correct or replace defective products (or services) is created when

the products are sold with the warranties. Even though the seller does not know

11. There are no conditions in which a probable loss tied to a future event can create a

12.A A wage bracket withholding table shows for a pay period of a given length (weekly,

14. At September 26, 2015, Apple reports accounts payable of $35,490 million.

15. At December 31, 2015, Google reports the following accrued expenses:

16. At December 31, 2015, Samsung reports eleven current liabilities: Trade and other

17. Samsung’s current liabilities include one income-tax-related liability titled: Income

tax payable. This account reflects taxes that must be paid to the government in the

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 11

661

QUICK STUDIES

Quick Study 11-1 (5 minutes)

Items 1, 4, 5 and 6 are current liabilities for this company.

Quick Study 11-2 (10 minutes)

(1)

Sept. 30

Cash ………………………………………………………………..

6,300

(2)

Quick Study 11-3 (10 minutes)

Oct. 31

Cash ………………………………………………………………..

5,000,000

Unearned Ticket Revenue …………………………..

Quick Study 11-4 (15 minutes)

1. Computation of interest payable at December 31, 2017:

2. 2017

Quick Study 11-4 (concluded)

3. 2018

Feb. 5

Interest Expense ………………………………………………

1,280

Interest Payable ……………………………………………….

1,920

Notes Payable ………………………………………………….

Cash ……………………………………………………….

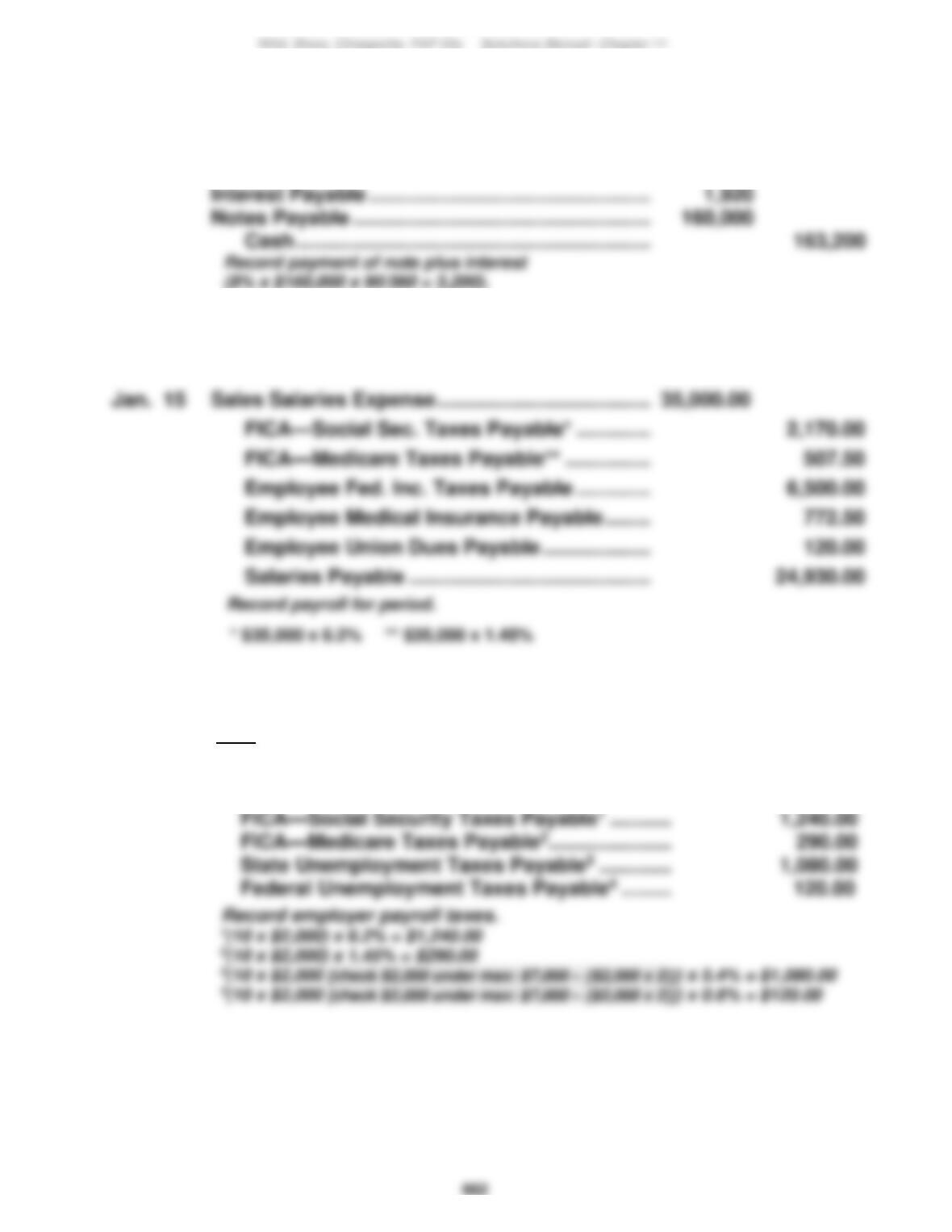

Quick Study 11-5 (15 minutes)

Sales Salaries Expense …………………………………….

FICA—Social Sec. Taxes Payable* ………………

FICA—Medicare Taxes Payable** ………………..

Employee Fed. Inc. Taxes Payable ………………

Employee Medical Insurance Payable ………….

Employee Union Dues Payable ……………………

Salaries Payable …………………………………………

Quick Study 11-6 (15 minutes)

[Note: Two months (January and February) of earnings have

already been recorded for each of the 10 employees.]

Mar. 31

Payroll Taxes Expense ……………………………………..

2,730.00

663

Quick Study 11-7 (5 minutes)

Employee Bonus Expense ………………………………..

Bonus Payable ………………………………………….

Quick Study 11-8 (5 minutes)

Vacation Benefits Expense* ……………………………..

500

Vacation Benefits Payable …………………………

Quick Study 11-9 (10 minutes)

2016

Sep 11

Cash ………………………………………………………………..

500

Sales …………………………………………………………..

500

Sep 11

Merchandise Inventory ………………………………..

Sep 11

Warranty Expense ……………………………………………

Estimated Warranty Liability ………………………..

Estimated Warranty Liability …………………………..

Repair Parts Inventory …………………………………

Quick Study 11-10 (10 minutes)

Quick Study 11-11 (10 minutes)

Quick Study 11-12A (15 minutes)

Gross Pay ……………………………………………………………………

$740.00

160.01

Quick Study 11-13B (10 minutes)

Quick Study 11-14 (10 minutes)

a. The definitions and characteristics of current liabilities are broadly

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 11

665

EXERCISES

Exercise 11-1 (10 minutes)

Exercise 11-2 (10 minutes)

[Note: All entries dated December 31, 2017]

1.

Cash ……………………………………………………………………

10,400

Exercise 11-3 (30 minutes)

2a.

May 15

Cash ………………………………………………………………..

110,000

110,000

666

Exercise 11-4 (30 minutes)

2.

3.

4a.

2017

2017

Notes Payable ………………………………………………….

667

Exercise 11-5 (20 minutes)

Subject

to Tax

Rate

Tax

Explanation

Exercise 11-6 (10 minutes)

Exercise 11-7 (10 minutes)

668

Exercise 11-8 (30 minutes)

Sales Salaries Expense …………………………………….

5,220

2,800

1,600

1,000

* $7,000 x 40% ** $4,000 x 40%

5,220

2,700

July 31

Employee Benefits Expense …………………………..

6,600

4,200

2,400

Employee Fed. Income Taxes Payable. ……………..

Employee Medical Insurance Payable ……………….

Employee Life Insurance Payable ……………………..

Employee Union Dues Payable ………………………….

669

Exercise 11-9 (30 minutes)

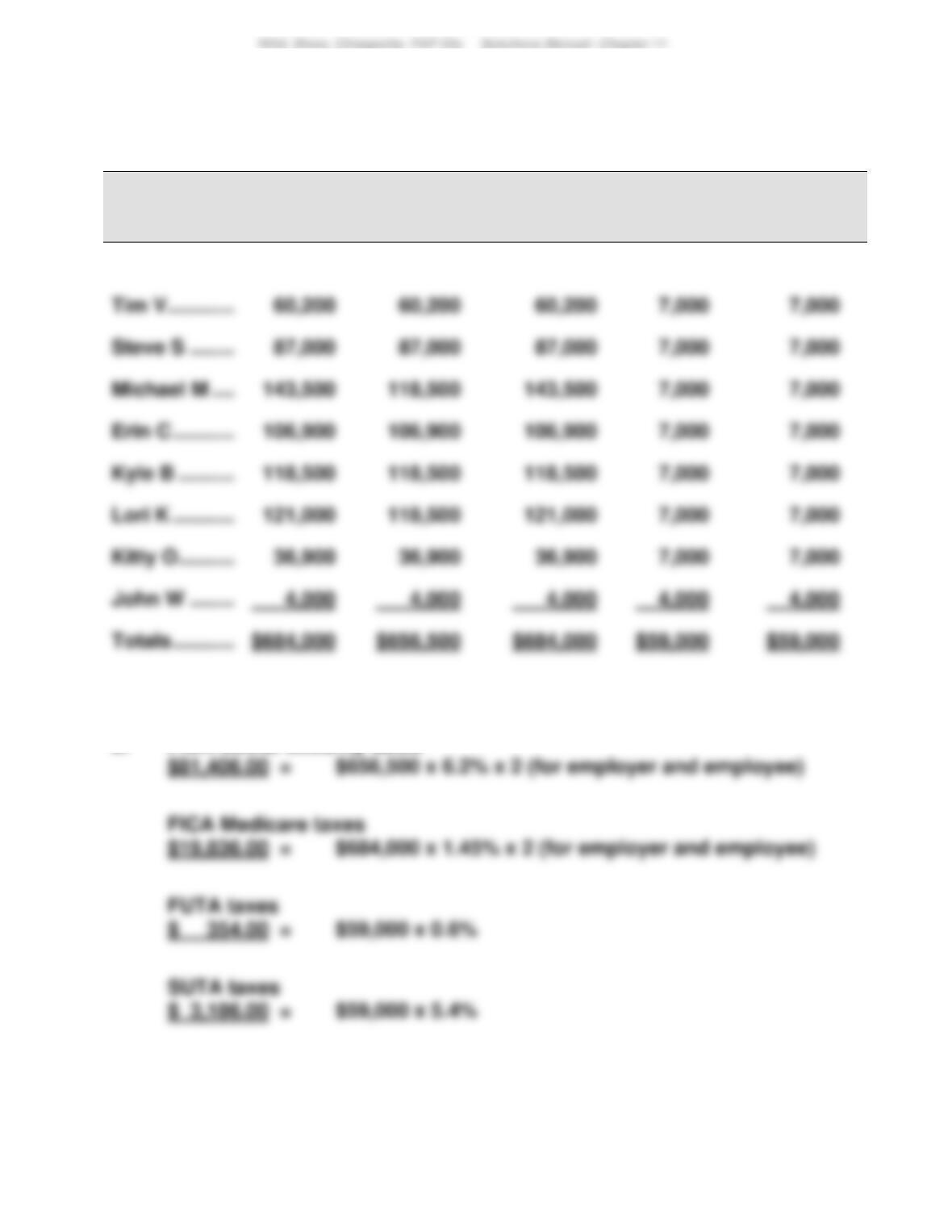

a.

Employee

Cumulative

Pay

Pay Subject to

FICA Social

Security

Pay Subject

to FICA

Medicare

Pay Subject

to FUTA

Taxes

Pay Subject

to SUTA

Taxes

Ken S ……………….

$ 6,000

$ 6,000

$ 6,000

$ 6,000

$ 6,000

106,900

121,000

b. FICA Social Security taxes

670

Exercise 11-10 (25 minutes)

5. Journal entries

2017

(a)

Aug. 16

Cash ………………………………………………………………..

6,000

Aug. 16

4,800

2018

(c)

Exercise 11-11 (15 minutes)

1.

2017

2.

2018

Exercise 11-12 (10 minutes)

[Note: All entries dated December 31, 2017.]

Exercise 11-13 (10 minutes)

[Note: All entries dated December 31, 2017.]

1. No adjusting entry is required since it is not probable that the supplier will

2. No adjusting entry can be made since the loss cannot be reasonably

672

Exercise 11-14 (15 minutes)

(a)

(b)

(c)

(d)

(e)

(f)

Numerator

interest & taxes ….

Denominator

Income before

Exercise 11-15B (25 minutes)

1.

Income Taxes Payable (target balance) ………………………………………..

Total accrued [($28,600 + $19,100 + $34,600) x .30] ……………………….

24,690

Adjustment (additional expense) ………………………………………………….

2.

2017

(a)

Dec. 31

Income Tax Expense …………………………………………

3,610

Income Taxes Payable …………………………………

2018

Jan. 20

Income Taxes Payable ………………………………………

Cash ……………………………………………………………

Exercise 11-16A (15 minutes)

Overtime premium pay (8 hours @ [$14 x 150%]) ………..

Gross pay ………………………………………………………………..

Income tax deduction (from Exhibit 11A.6) ………………….

Total deductions ………………………………………………………

673

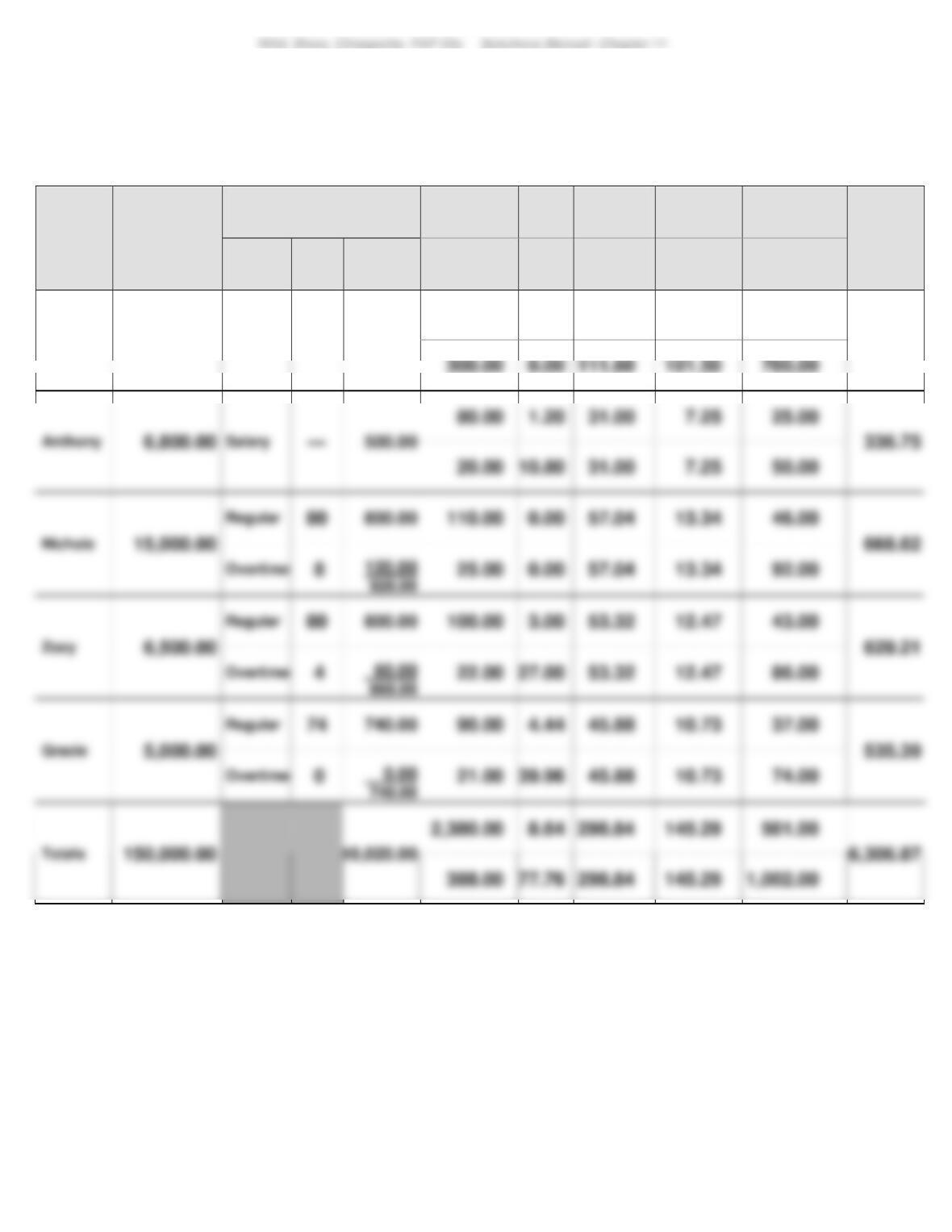

Exercise 11-17 (30 minutes)

(a)

Employee

Cumulative

Pay (Excludes

Current Period)

Current Period Gross Pay

FIT

Withholding

FUTA

FICA S.S.

Employee

FICA

Medicare

Employee

Employee—

Benefits Plan

Withholding

Employee

Net Pay

(Current

Period)

Pay

Type

Pay

Hours

Gross Pay

SIT

Withholding

SUTA

FICA S.S.

Employer

FICA

Medicare

Employer

Employer—

Benefits Plan

Expense

Kathleen

116,700.00

Salary

—

7,000.00

2,000.00

0.00

111.60

101.50

350.00

4,136.90

0.00

111.60

101.50

700.00

0.00

3.00

4.44

2,380.00

8.64

298.84

145.29

501.00

145.29

674

Exercise 11-17 (concluded)

(b)

(c)

(d)

(e)

675

Exercise 11-18 (25 minutes)

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 11

676

PROBLEM SET A

Problem 11-1A (45 minutes)

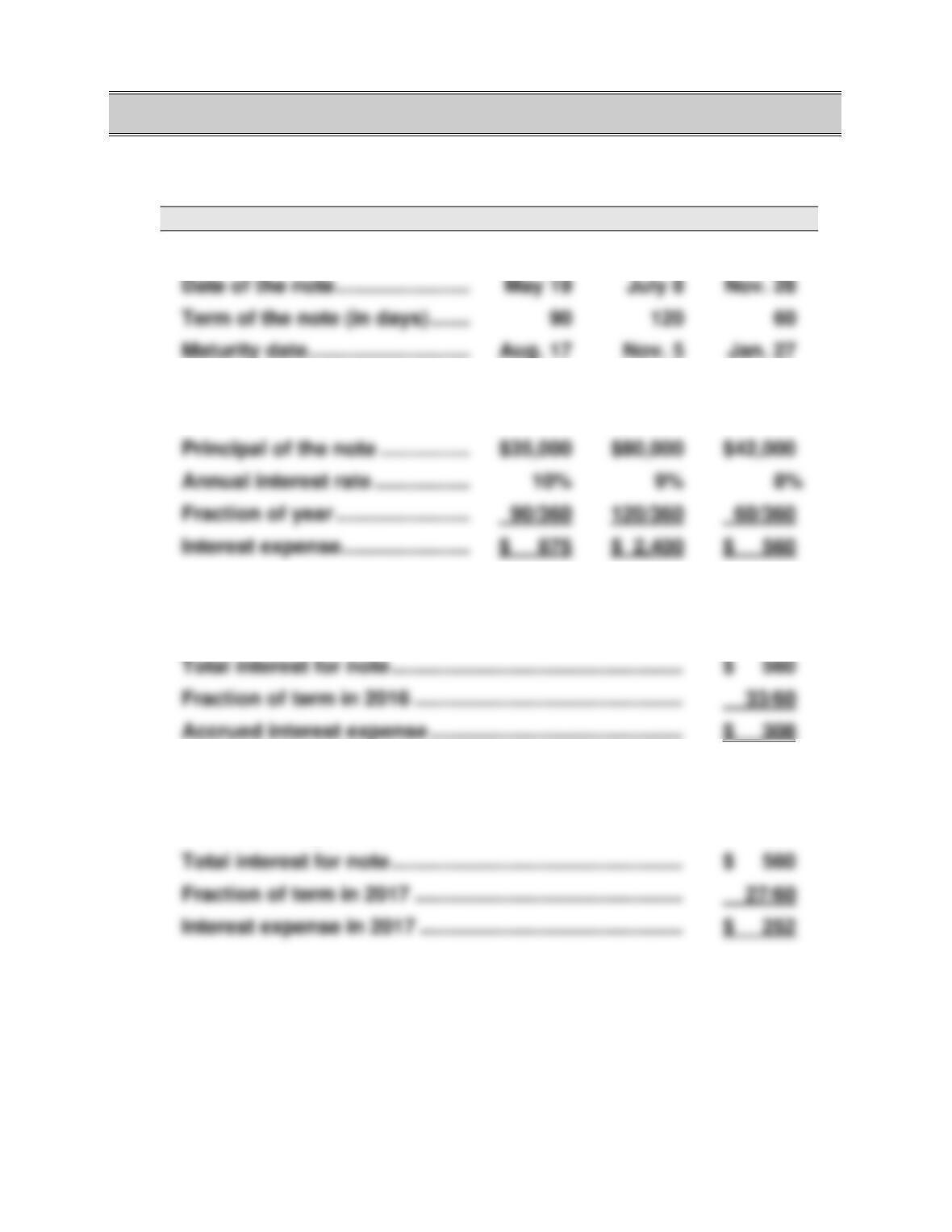

Locust

NBR Bank

Fargo Bank

1.

Maturity dates

2.

Interest due at maturity

3.

Accrued interest on Fargo note at the end of 2016

4.

Interest on Fargo note in 2017

677

Problem 11-1A (Concluded)

5.

2016

Accounts Payable—Locust …………………………

Cash …………………………………………………………..

Notes Payable—Locust ……………………………….

Notes Payable—NBR …………………………………..

Interest Expense ………………………………………………

Cash …………………………………………………………..

Nov. 5

Interest Expense ………………………………………………

2,400

Cash …………………………………………………………..

Notes Payable—Fargo Bank ………………………..

Interest Expense ………………………………………………

Interest Payable ………………………………………….

Interest Expense ………………………………………………

Interest Payable ……………………………………………….

Cash …………………………………………………………..

678

Problem 11-2A (25 minutes)

Part 1

Part 2