CHAPTER 11

SOLUTIONS TO PROBLEMS: SET B

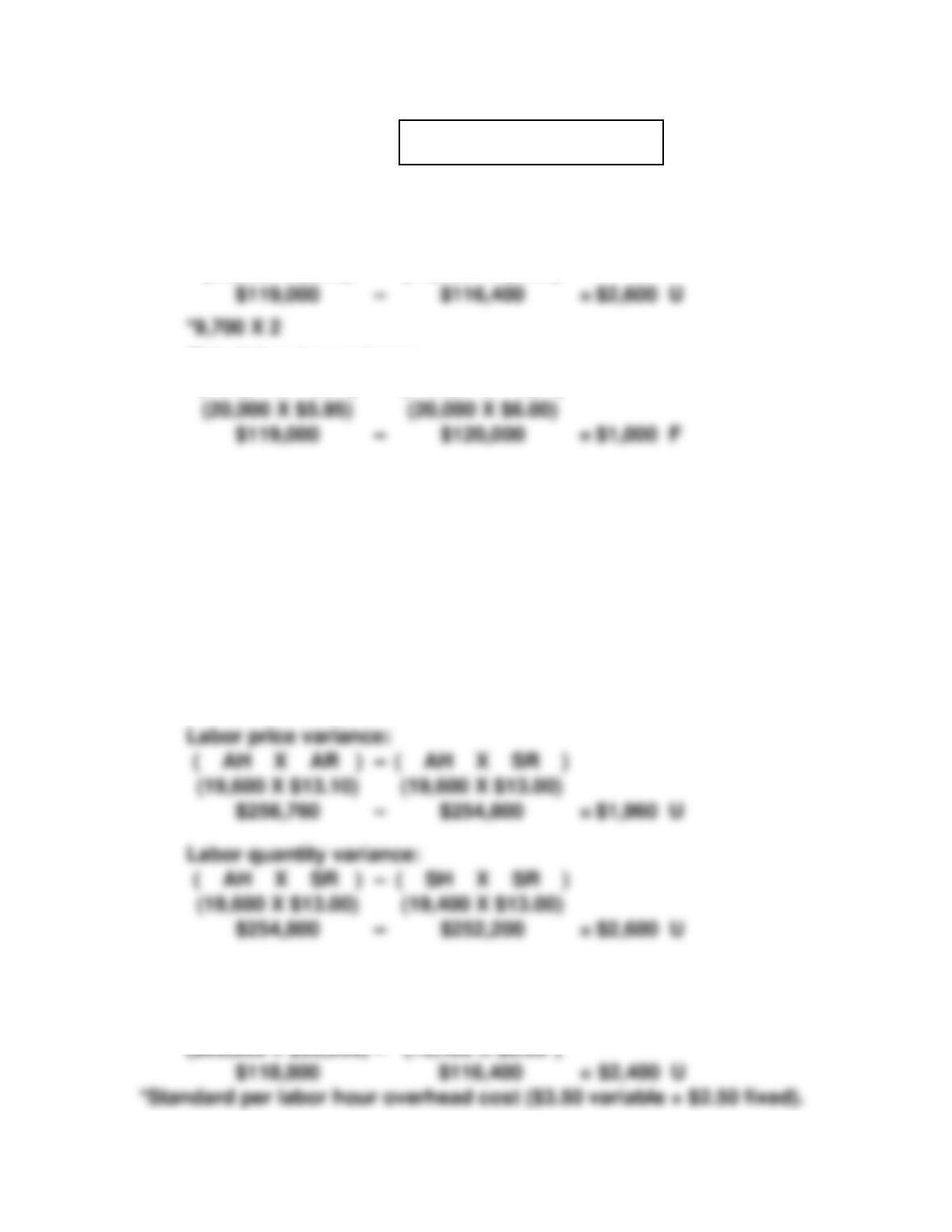

(a) Total materials variance:

( AQ X AP )

(20,000 X $5.95)

–

( SQ X SP )

(19,400* X $6.00)

Materials price variance:

(20,000 X $5.95)

(20,000 X $6.00)

( AQ X AP )

–

( AQ X SP )

Materials quantity variance:

( AQ X SP )

(20,000 X $6.00)

$120,000

–

–

( SQ X SP )

(19,400 X $6.00)

$116,400

=

$3,600 U

Total labor variance:

( AH X AR )

(19,600 X $13.10)

$256,760

–

–

( SH X SR )

(19,400* X $13.00)

$252,200

=

$4,560 U

–

–

=

$1,960 U

( AH X SR )

–

*9,700 X 2

(b) Total overhead variance:

=

Actual

Overhead

–

Overhead

Applied

PROBLEM 11-1B

PROBLEM 11-2B

(a) 1. Total materials variance:

( AQ X AP )

(21,000 X $3.70)

$77,700

–

–

( SQ X SP )

(22,000 X $3.50)

$77,000

=

$700 U

Materials price variance:

2. Total labor variance:

( AH X AR )

(3,450 X $11.50)

$39,675

–

–

( SH X SR )

(3,600 X $12.00)

$43,200

=

$3,525 F

( AH X AR )

$39,675

–

–

=

$1,725 F

–

( SH X SR )

(b) Total overhead variance:

Actual

Overhead

$94,800

–

–

Overhead

Applied

$100,800

=

$6,000 F

$77,700

–

=

$4,200 U

( AQ X SP )

–

( SQ X SP )

PROBLEM 11-2B (Continued)

(c) HUANG COMPANY

Income Statement

For the Month Ended July 31, 2017

Sales revenue ……………………………………………. $270,000

Cost of goods sold (at standard) …………………. 221,0001

Gross profit (at standard) ……………………………. 49,000

Variances

Materials price …………………………………….. $ 4,200 U

Materials quantity ………………………………… 3,500 F

Labor price …………………………………………. 1,725 F

PROBLEM 11-3B

(a) 1. Total materials variance:

( AQ X AP )

(76,000 X $7.20)

$547,200

–

–

( SQ X SP )

(78,500* X $6.75)

$529,875

=

$17,325 U

*15,700 X 5

2. Total labor variance

( AH X AR )

(14,800 X $11.20)

$165,760

–

–

( SH X SR )

(15,700 X $11.45)

$179,765

=

$14,005 F

Labor price variance:

$165,760

–

$169,460

=

$3,700 F

( AH X AR )

(14,800 X $11.20)

–

( AH X SR )

(14,800 X $11.45)

(b) Total overhead variance:

Actual

Overhead

–

Overhead

Applied

$21,420 U

$547,200

–

$513,000

=

$34,200 U

( AQ X SP )

$513,000

–

–

( SQ X SP )

$529,875

=

$16,875 F

PROBLEM 11-3B (Continued)

(c) The following variances are more than 5% from standard:

Materials price variance. The actual price of $7.20 is 6.7% higher than

the standard price of $6.75.

The unfavorable materials price variance was caused by paying more

than the standard cost for the materials purchased. This unfavorable

PROBLEM 11-4B

(a) $10,000 ÷ 200,000 = $.05; $1.00 – $.05 = $.95 standard materials price

(b) $23,750 ÷ $.95 = 25,000 pounds; 200,000 + 25,000 = 225,000 standard

(c) Standard hours allowed are 90,000 (45,000 X 2).

(d) $10,080 ÷ $12 = 840 hours over standard; 90,000 standard hours +

840 hours = 90,840 actual hours worked. OR

(e) $18,168 ÷ 90,840 = $.20; $12.00 – $.20 = $11.80 actual rate per hour.

(h) 90,000 X $8.30 = $747,000 overhead applied.

PROBLEM 11-5B

(a) Materials price variance:

( AQ X AP )

(2,530 X $2.00*)

$5,060

–

–

( AQ X SP )

(2,530 X $1.80)

$4,554

=

$506 U

*$5,060 ÷ 2,530

(b) Total overhead variance:

Actual Overhead

$15,800

[($10,100 + $5,700)

–

–

–

Overhead Applied

$16,250

(1,250 X $13*)

=

$450 F

–

$54 U

(AH X AR)

–

–

$620 U

(1,240 X $20.50)

–

–

$205 F

PROBLEM 11-5B (Continued)

(c) BONITA LABS

Income Statement

For the Month Ended May 31, 2017

Service revenue …………………………………………….. $55,000

Cost of service provided (at standard)

($18.55 X 2,500) …………………………..……………… 46,375

Gross profit (at standard) ……………………………….. 8,625

Variances

Materials price ………………………………………… $ 506 U

(d) The unfavorable materials price variance could be caused by using the

wrong shipping method or rising prices.

The unfavorable materials quantity variance could be caused by inex-

*PROBLEM 11-6B

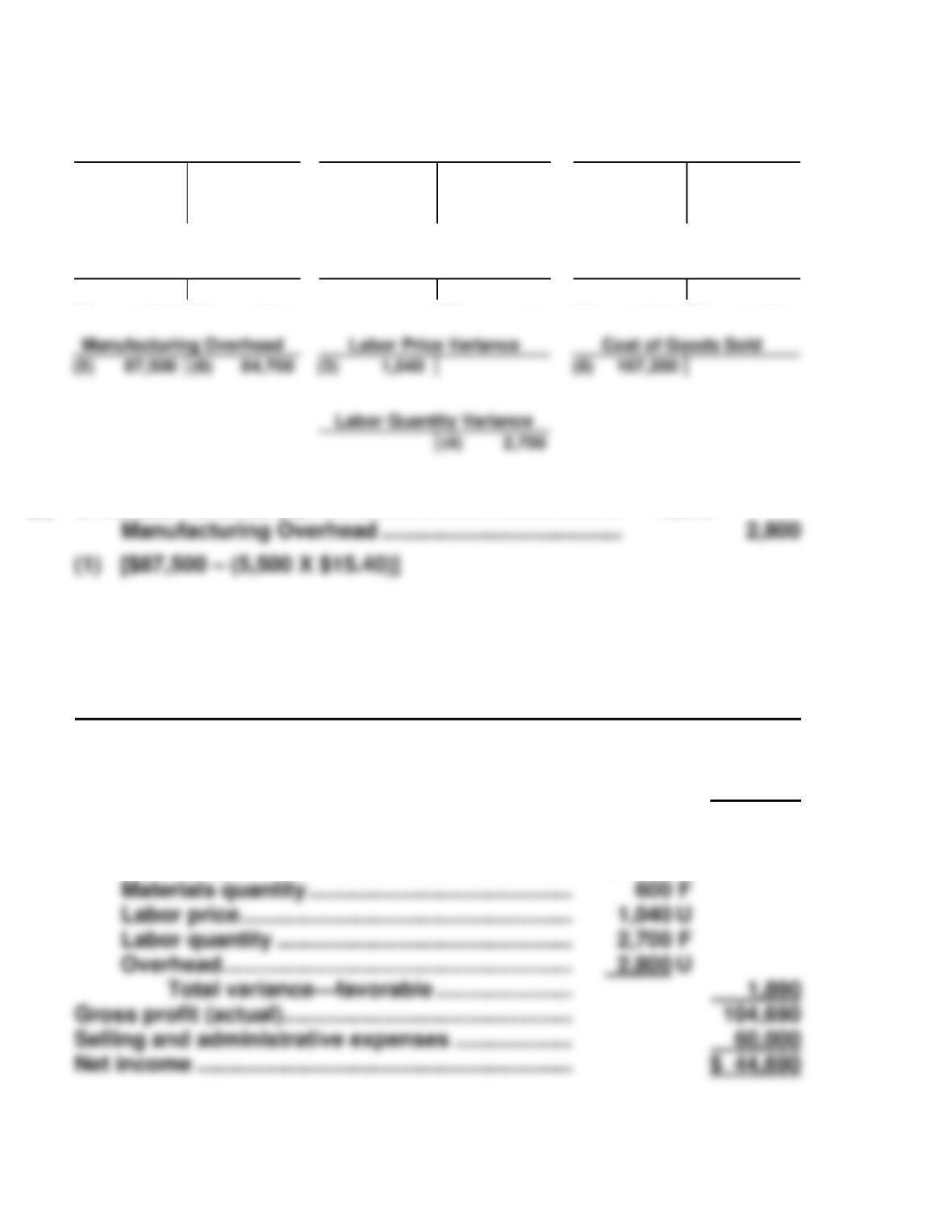

(a) 1. Raw Materials Inventory (8,100 X $4.00) ……… 32,400

Materials Price Variance

[8,100 X ($3.70 – $4.00)] ………………….. 2,430

Accounts Payable (8,100 X $3.70) ……….. 29,970

2. Work in Process Inventory

(8,250* X $4.00) ……………………………………… 33,000

3. Factory Labor (5,200 X $9.00) ……………………. 46,800

Labor Price Variance

[5,200 X ($9.20 – $9.00)] …………………………. 1,040

Factory Wages Payable

(5,200 X $9.20) ………………………………… 47,840

4. Work in Process Inventory

(5,500 X $9.00) ………………………………………. 49,500

5. Manufacturing Overhead …………………………... 87,500

Accounts Payable ……………………………… 87,500

6. Work in Process Inventory

(5,500 X $15.40) …………………………..………… 84,700

Manufacturing Overhead ……………………. 84,700

*PROBLEM 11-6B (Continued)

(b)

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory

(1) 32,400

(2) 32,400

(1) 2,430

(2) 33,000

(4) 49,500

(6) 84,700

(7) 167,200

Factory Labor

Materials Quantity Variance

Finished Goods Inventory

(3) 46,800

(4) 46,800

(2) 600

(7) 167,200

(8) 167,200

(c) Overhead Variance (1) …………………………………………… 2,800

(d) FRIO MANUFACTURING COMPANY

Income Statement

For the Month Ended January 31, 2017

Sales revenue ………………………………………………… $270,000

Cost of goods sold (at standard)

(5,500 X $30.40) ………………………………………….. 167,200

Gross profit (at standard) ……………………………….. 102,800

Variances

Materials price ………………………………………… $2,430 F

Manufacturing Overhead

(5) 87,500

(8) 167,200

(4) 2,700

*PROBLEM 11-7B

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

Overhead volume variance:

Fixed Overhead

X

Normal

Capacity

–

Standard

Hours

*PROBLEM 11-8B

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

–

*PROBLEM 11-9B

Overhead controllable variance:

Actual

Overhead

$169,000

–

–

Overhead

Budgeted

$174,455

=

$5,455 F

*PROBLEM 11-10B

Overhead controllable variance:

Actual Overhead

$15,800

–

–

Overhead Budgeted

$16,000