Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

SOLUTIONS TO PROBLEMS

PROBLEM 11-35 (45 MINUTES)

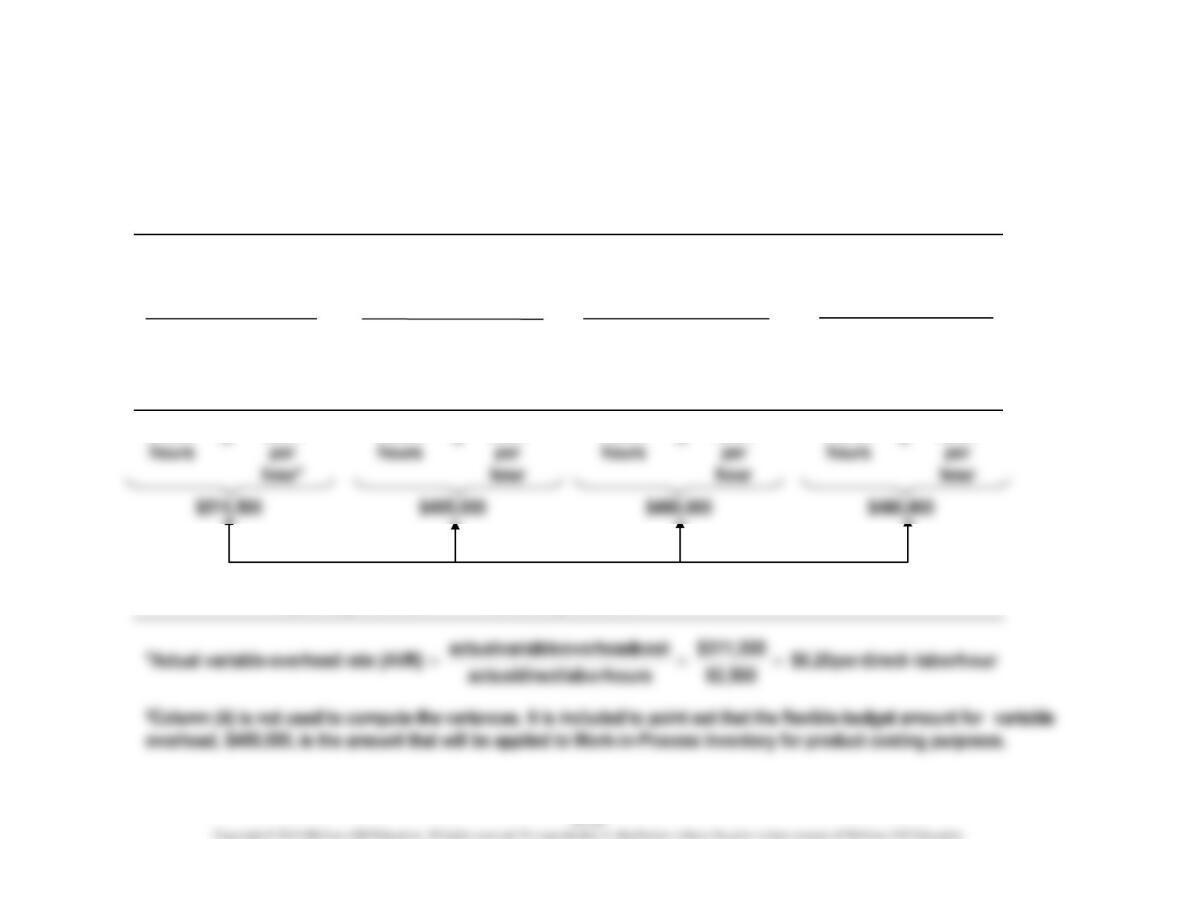

PROJECTED VARIABLE

OVERHEAD

VARIABLE-OVERHEAD SPENDING AND EFFICIENCY VARIANCES

(Hours = Direct-Labor Hours)

Actual

Hours

(AQ)

Actual

Rate

(AVR)

Actual

Hours

(AQ)

Standard

Rate

(SVR)

Standard

Rate

(SVR)

Standard

Rate

(SVR)

Standard

Allowed

Hours

(SQ)

Standard

Allowed

Hours

(SQ)

x

x

x

x

82,500

82,500

80,000

80,000

$6.20

$6.00

$6.00

$6.00

$16,500 Unfavorable

$15,000 Unfavorable

Variable-overhead

spending variance

Variable-overhead

efficiency variance

No difference

x

x

x

x

FLEXIBLE BUDGET:

VARIABLE OVERHEAD

ACTUAL VARIABLE

OVERHEAD

VARIABLE OVERHEAD

APPLIED TO

WORK-IN-PROCESS

(1)

(2)

(3)

(4)†

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-35 (CONTINUED)

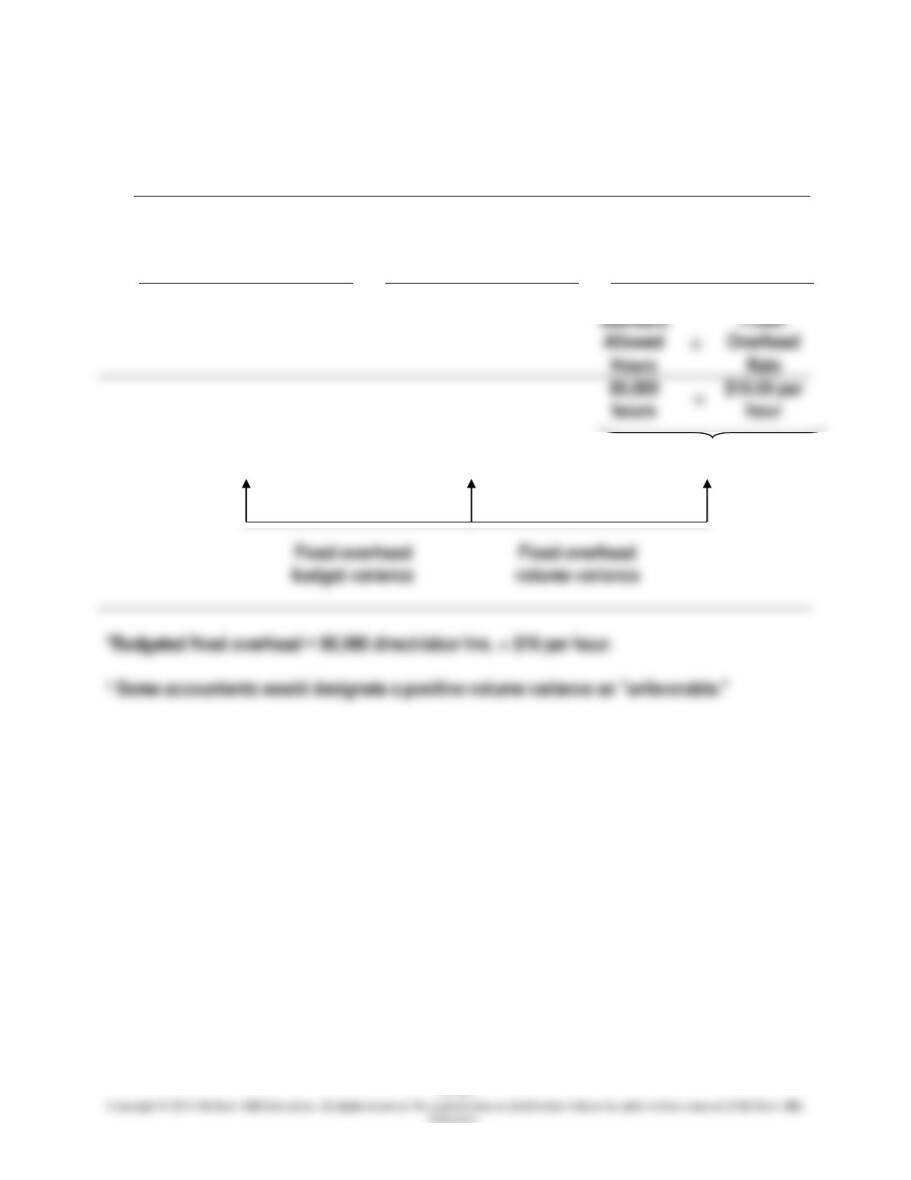

FIXED-OVERHEAD BUDGET AND VOLUME VARIANCES

(Hours = Direct-Labor Hours)

(1)

ACTUAL

FIXED

OVERHEAD

(2)

BUDGETED

FIXED

OVERHEAD

(3)

FIXED OVERHEAD

APPLIED TO

WORK IN PROCESS

Standard

$860,000

$900,000*

$800,000

$40,000 Favorable

$100,000 U†

PROBLEM 11-36 (30 MINUTES)

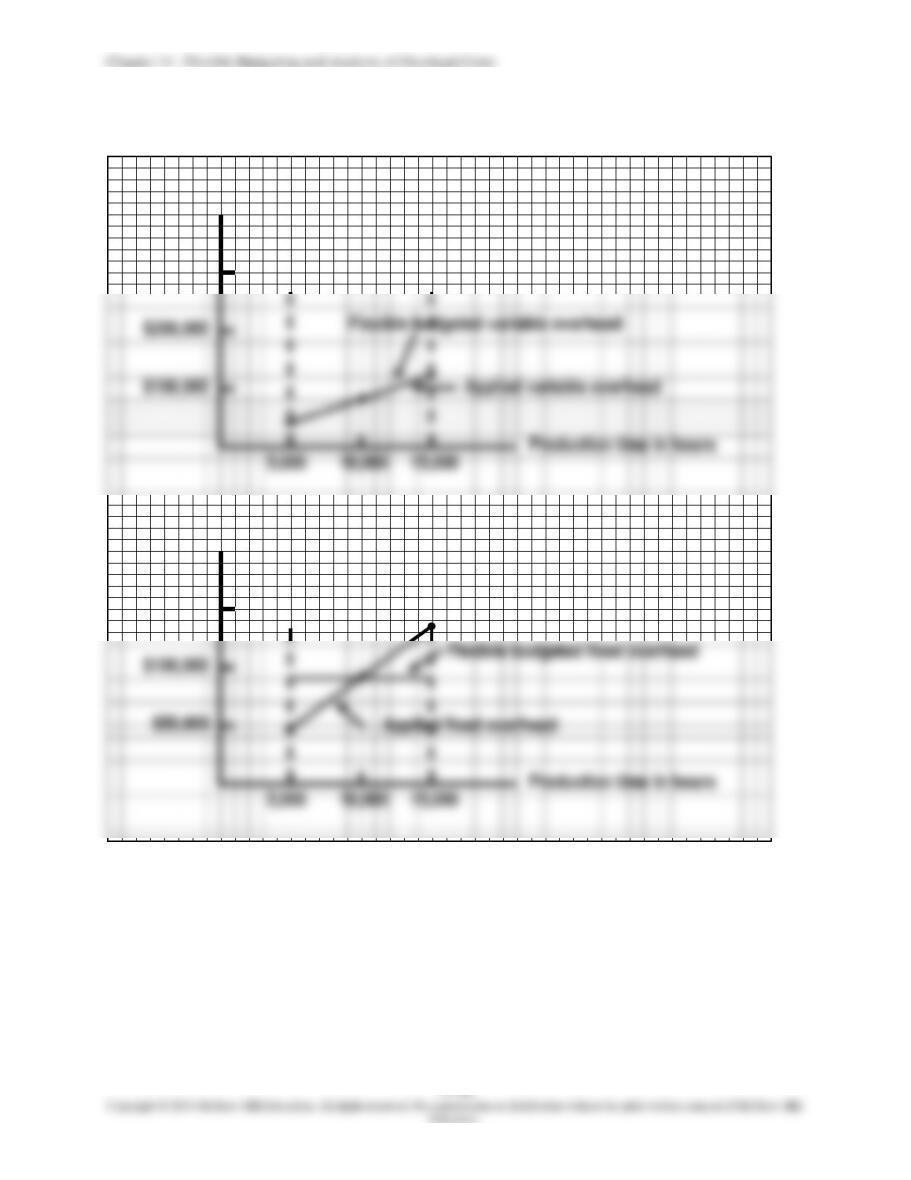

1.

The graphs are shown on the next page. On the variable overhead graph, the slope of

2.

Memorandum

Date:

Today

To:

C. D. Tune, General Manager of Countrytime Studios

From:

I. M. Student

Subject:

Overhead graphs

The variable-overhead graph shows that the flexible-budgeted variable-overhead line

and the applied variable-overhead line are the same line. Since this cost really is

PROBLEM 11-36 (CONTINUED)

$300,000

$200,000

$100,000

5,000

10,000

15,000

Variable overhead

$150,000

$100,000

$50,000

5,000

10,000

15,000

Fixed overhead

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-37 (40 MINUTES)

1.

a.

Units produced during March ……………………………………………..

66,000

Overhead application rate per unit

(budgeted overhead per unit at expected level of output) …..

$12

Applied overhead costs ……………………………………………………..

$792,000

Variable-overhead spending variance …………………………………

c.

Fixed-overhead budget variance …………………………………………

Variable-overhead efficiency variance …………………………………

e.

Fixed-overhead volume variance ………………………………………..

*U denotes unfavorable; F denotes favorable.

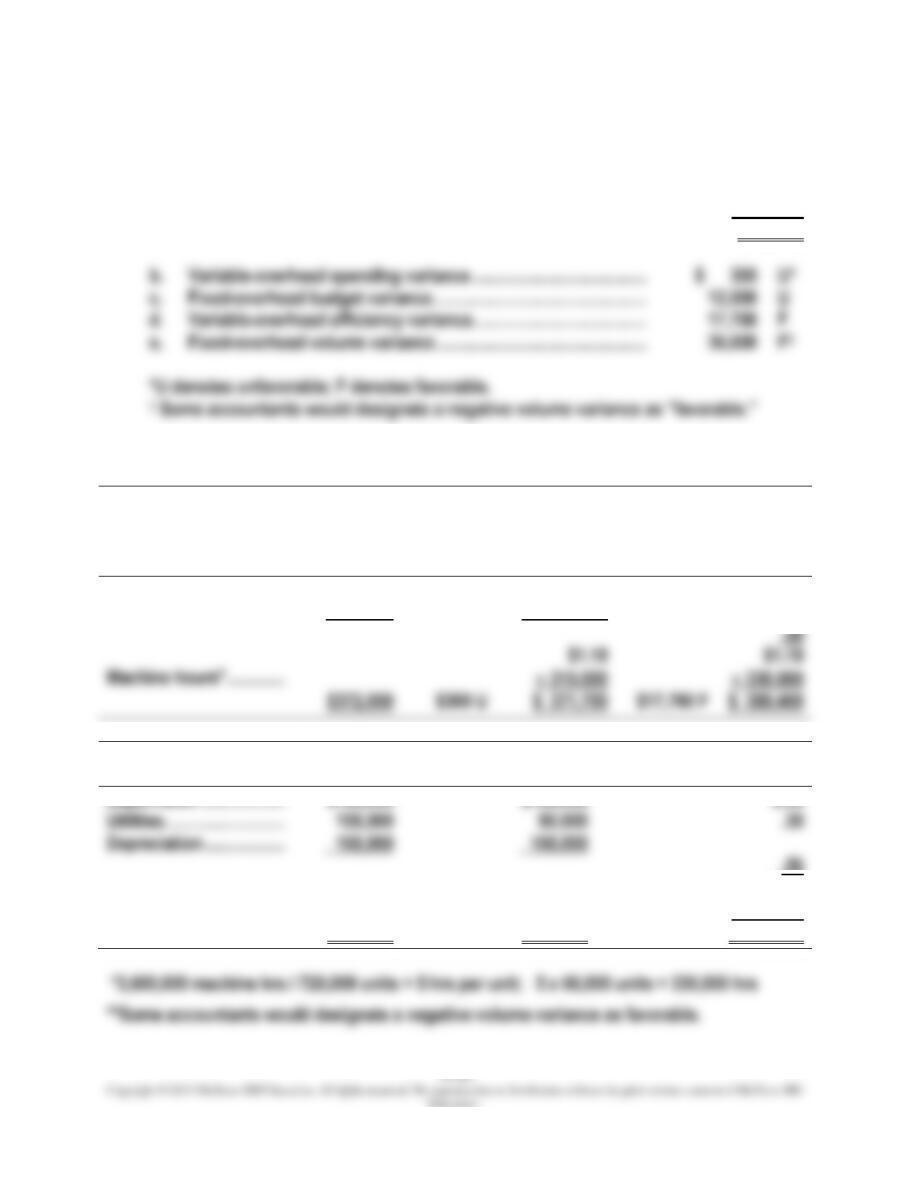

Supporting calculations are presented in the following schedule:

Variable Overhead

Actual

Overhead

Spending

Variance

Projected

Overhead

Efficiency

Variance

Flexible

Budget

(Applied

Overhead)

Indirect material …………

$222,000

$.68

$.68

Indirect labor ……………..

150,000

.50

$1.18

Machine hours* ………….

330,000

Fixed Overhead

Actual

Overhead

Budget

Variance

Flexible

Budget

Volume

Variance

Applied

Overhead

Supervision ……………….

$102,000

$.36

Utilities ………………………

.56

$1.22

Machine hours* ………….

330,000

$378,000

$12,000 U

$366,000

$36,600 F**

$ 402,600

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-37 (CONTINUED)

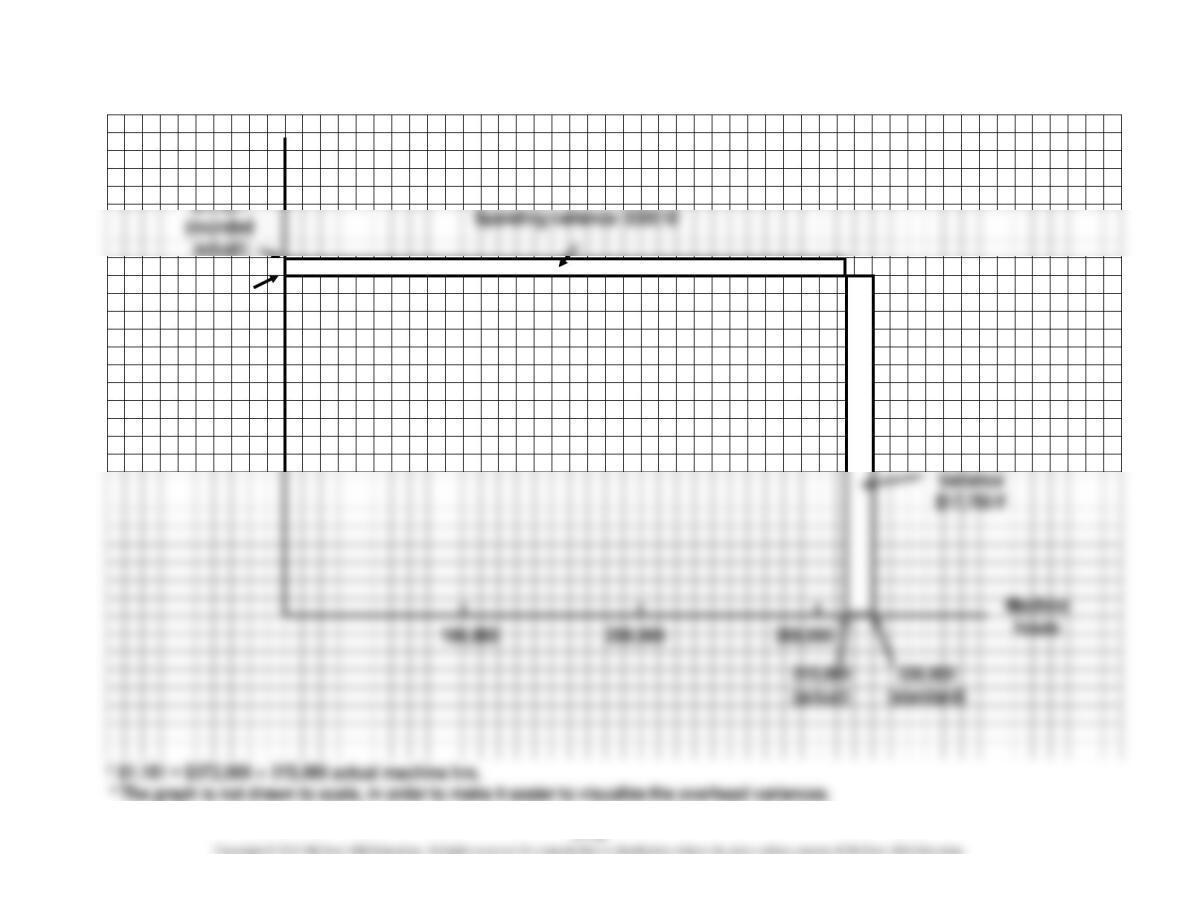

2. Graphical analysis of variable-overhead variances:*

$1.18

(standard)

Efficiency

Rate

PROBLEM 11-37 (CONTINUED)

3.

efficiency variance.

The graph differs from the exhibit in the text, because in Wilmington Composites’ case,

PROBLEM 11-38 (20 MINUTES)

1.

Policy

Type

Standard

Clerical Hours

per Application

Actual

Activity

Standard

Clerical Hours

Allowed

Automobile …………………………………

1

375

375

Renter’s ……………………………………..

1.5

300

450

Homeowner’s ……………………………..

2

150

300

Health …………………………………………

2

600

Life …………………………………………….

5

300

2.

The different types of applications require different amounts of clerical time, and variable

overhead cost is related to the use of clerical time. Therefore, basing the flexible budget on

3.

Formula flexible budget:

total

variablebudgeted

where X denotes total clerical time in hours.

=

$22,125

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-39 (25 MINUTES)

1. Let X = budgeted fixed overhead

2. Variable-overhead spending variance:

Actual machine hours x actual rate

23,100 hours x $7.20*……………………

$166,320

Actual machine hours x standard rate

23,100 hours x $7.50…………………….

$ 6,930 Favorable

* $166,320 ÷ 23,100 hours

3. Fixed-overhead volume variance:

Budgeted fixed overhead………………………………

$240,000

Standard machine hours allowed x standard rate

5,350 hours* x $12.00………………………………

64,200

$175,800 U†

* 10,700 units x .5 machine hours per unit

4. Lackawanna Licorice Company spent more than anticipated. Actual fixed overhead

5. Variable overhead is underapplied by $126,195:

Actual overhead: Actual machine hours x actual rate

23,100 hours x $7.20…………………………………………..

$166,320

5,350 hours x $7.50…………………………………………….

40,125

Underapplied variable overhead…………………………………

$126,195

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-39 (CONTINUED)

6. Without having complete information, it is difficult to be 100% certain. However, by

an analysis of data related to the volume variance, a lengthy strike appears to be a

PROBLEM 11-40 (30 MINUTES)

2. Given the focus on a range of activity, a flexible budget would be more useful

because it incorporates several different activity levels.

3. Static budget vs. actual experience:

Static

Budget:

24,000

Units

Actual:

20,000

Units

Variance

Direct material used ($40.00) ……………………

$ 960,000

$ 865,000

$ 95,000 F

Direct labor ($10.00) ………………………………..

240,000

221,200

18,800 F

Variable production overhead ($12.50) ……..

300,000

304,000

4,000 U

Depreciation ……………………………………………

48,000

—-

Supervisory salaries ……………………………….

72,000

3,600 U

Other fixed production overhead ……………..

480,000

478,000

2,000 F

$2,100,000

$1,991,800

$108,200 F

Calculations:

Direct material used: $2,880,000 ÷ 72,000 units = $40.00 per unit

PROBLEM 11-40 (CONTINUED)

4. Flexible budget vs. actual experience:

Flexible

Budget:

20,000

Units

Actual:

20,000

Units

Variance

Direct material used ($40.00)……………………..

$ 800,000

$ 865,000

$ 65,000 U

Direct labor ($10.00) ………………………………….

200,000

Variable production overhead ($12.50) ………

250,000

Depreciation …………………………………………….

48,000

Supervisory salaries …………………………………

72,000

Other fixed production overhead ……………….

480,000

478,000

$1,991,800

$141,800 U

5. A performance report based on flexible budgeting is preferred. The report compares

budgeted and actual performance at the same volume level, eliminating any

variations in activity. In essence, everything is placed on a “level playing field.”

The general manager’s warning is appropriate because of the sizable

variances that have arisen. With the static budget, performance appears favorable,

PROBLEM 11-41 (30 MINUTES)

1. Performance report:

Budget:

790

Patients

Actual:

790

Patients

Variance

Medical assistants……………

$ 5,530

$ 6,510

$ 980 U

Clinic supplies………………..

4,740

4,575

165 F

Lab tests……………………….

4,977 U

$164,320

$ 5,792 U

Calculations:

Medical assistants:

Budget: 790 patients x .5 hours/patient x $14.00/hr = $5,530

2. The variances do not reveal any significant problems. The $165 variance for clinic

PROBLEM 11-41 (CONTINUED)

3. Variances for lab tests:

Spending variance:

Actual tests conducted x actual cost

2,607 tests* x $61/test**…………………………………..

$159,027

Actual tests conducted x standard cost

2,607 tests x $65/test………………………………………..

$ 10,428 F

* 790 patients x 3.3 tests/patient

** $159,027 ÷ 2,607 tests

Efficiency variance:

Actual tests conducted x standard cost

2,607 tests x $65/test………………………………………..

$169,455

Standard tests allowed x standard cost

2,370 tests* x $65/test……………………………………….

$ 15,405 U

* 790 patients x 3 tests/patient

Yes, the hospital does appear to have some problems. The two variances computed

are fairly sizable in relation to the $154,050 budget. The efficiency variance is of

particular concern, given that it is 10% of budget ($15,405 ÷ $154,050) and

PROBLEM 11-42 (40 MINUTES)

1.

The flexible budget for LakeMaster Company for the month of June, based on 4,800

units, showing separate variable cost budgets is as follows:

LAKEMASTER COMPANY

FLEXIBLE BUDGET

FOR THE MONTH OF JUNE

Revenue [4,800 ($1,800,000/5,000)] …………………………...

$1,728,000

Deduct: Variable costs:

Direct material (4,800 $90) ……………………………………

$ 432,000

Direct labor (4,800 $66) ………………………………………..

Variable overhead (4,800 $54) ………………………………

Variable selling (4,800 $18) …………………………………..

Total variable costs …………………………………………..

Contribution margin …………………………………………………….

Deduct: Fixed costs:

Fixed overhead ………………………………………………………

Fixed general and administrative …………………………….

Operating income ………………………………………………………..

PROBLEM 11-42 (CONTINUED)

2.

For the month of June, the company’s flexible-budget variances are as follows:

LAKEMASTER COMPANY

FLEXIBLE-BUDGET VARIANCES

FOR THE MONTH OF JUNE

Actual

Flexible

Budget

Flexible-

Budget

Variance

Units ……………………………………………………………

4,800

4,800

0

Revenue ………………………………………………………

$1,728,000

$1,728,000

$ 0

Variable costs:

Direct material ………………………………………..

$ 480,000

$ 432,000

$48,000 U

Direct labor …………………………………………….

28,800 F

Variable overhead …………………………………..

Variable selling ………………………………………

Deduct: Total variable costs …………………………

$1,170,000

$1,094,400

$75,600 U

Contribution margin …………………………………….

$ 558,000

$ 633,600

$75,600 U

Fixed costs:

Fixed overhead ………………………………………

$ 270,000

$ 270,000

$ 0

Fixed general and administrative …………….

Deduct: Total fixed costs ……………………………..

$ 442,500

$ 450,000

$ 7,500 F

3.

The revised budget and variance data are likely to have the following impact on Al

Richmond’s behavior:

• Richmond is likely to be encouraged by the revised data, since the major portion of

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-42 (CONTINUED)

PROBLEM 11-43 (55 MINUTES)

1.

Activity Level (Air Miles)

32,000

35,000

38,000

Variable expenses:

Fuel ………………………………………………….

$ 48,000

$ 52,500

$ 57,000

Aircraft maintenance …………………………

72,000

78,750

85,500

Flight crew salaries …………………………...

38,400

42,000

45,600

Selling and administrative …………………

76,800

84,000

91,200

Total variable expenses ………………

$235,200

$257,250

$279,300

Fixed expenses:

Depreciation on aircraft ……………………..

$ 8,700

$ 8,700

$ 8,700

Landing fees ……………………………………..

Supervisory salaries ………………………….

27,000

27,000

27,000

Selling and administrative …………………

33,000

33,000

33,000

Total fixed expenses …………………..

$ 71,400

$ 71,400

$ 71,400

2.

First, there is a large unfavorable variance in passenger revenue, reflecting the fact

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-43 (CONTINUED)

3.

Memorandum

Date:

Today

To:

Red Leif, Manager of Aircraft Operations

From:

I. M. Student

Subject:

Variance Report

given the actual activity level.

The variance report is misleading because the expenses in the budget, which was

4.

Formula

Flexible

Budget

(per air

mile)

Actual

(32,000

air

miles)

Flexible

Budget

(32,000

air

miles)

Variance

Variable expenses:

Fuel ………………………………….

$ 1.50

$ 51,000

$ 48,000

$3,000 U

Aircraft maintenance …………

2.25

70,500

72,000

1,500 F

Flight crew salaries …………….

1.20

39,300

38,400

Selling and administrative ….

2.40

74,700

76,800

Total variable expenses ..

$235,500

$235,200

Depreciation on aircraft ………

$ 8,700

$ 0

Landing fees ………………………

Supervisory salaries …………..

25,800

27,000

1,200 F

Selling and administrative ….

37,200

33,000

Total fixed expenses ……..

$ 74,700

$ 71,400

$3,300 U

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-43 (CONTINUED)

5.

expense variance report.

Jacqueline Frost has acted properly in every way. She noticed a major conceptual

error in the way Red Leif had prepared his performance report. She pointed this out to

him, and she also provided him with a correct analysis of September’s performance.

Several ethical standards for managerial accountants apply in this situation. (See

Chapter 1 for a listing of these standards.) Among the relevant standards are the

following:

Competence

• Prepare complete and clear reports and recommendations after appropriate

analyses of relevant and reliable information.

Integrity

• Communicate unfavorable as well as favorable information and professional

judgments or opinions.

Credibility

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-44 (40 MINUTES)

1.

Susan Porter recommended that EduSoft use flexible budgeting in this situation

because a flexible budget would allow Mark Fletcher to compare EduSoft’s actual

selling expenses (based on current month’s actual activity) with budgeted selling

expenses. In general, flexible budgets:

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-44 (CONTINUED)

2.

EDUSOFT CORPORATION

REVISED MONTHLY SELLING EXPENSE REPORT FOR OCTOBER

Flexible

Budget

Actual

Variance

Advertising ……………………………………………..

$3,300,000

$3,320,000

$20,000 U

Staff salaries ……………………………………………

250,000

250,000

0

Sales salariesa …………………………………………

230,400

230,800

400 U

992,000

992,000

0

Per diem expensec …………………………………..

316,800

325,200

Office expensesd ……………………………………..

732,000

716,800

Shipping expensese …………………………………

Supporting calculations:

aMonthly salary for salesperson

$216,000 90 = $2,400.

Budgeted amount

$896,000 $22,400,000 = .04.

Budgeted amount

c($297,000 90) 15 days = $220 per day.

($220 15) 96 = $316,800.

monthly fixed expense.

$125,000 + ($6 310,000) = $1,985,000.

Chapter 11 – Flexible Budgeting and Analysis of Overhead Costs

PROBLEM 11-45 (45 MINUTES)

Missing amounts for case A:

2.

$21.00a per direct-labor hour

3.

6.

9.

$7,500 Ud

$9,000 Fe

$24,150 underappliedg

$135,000 overappliedh

6,000 unitsi

Explanatory notes for case A:

aBudgeted direct-labor hours

=

budgeted production standard direct-labor hours per unit