Ch. 11: Auditing Computer-Based Information Systems

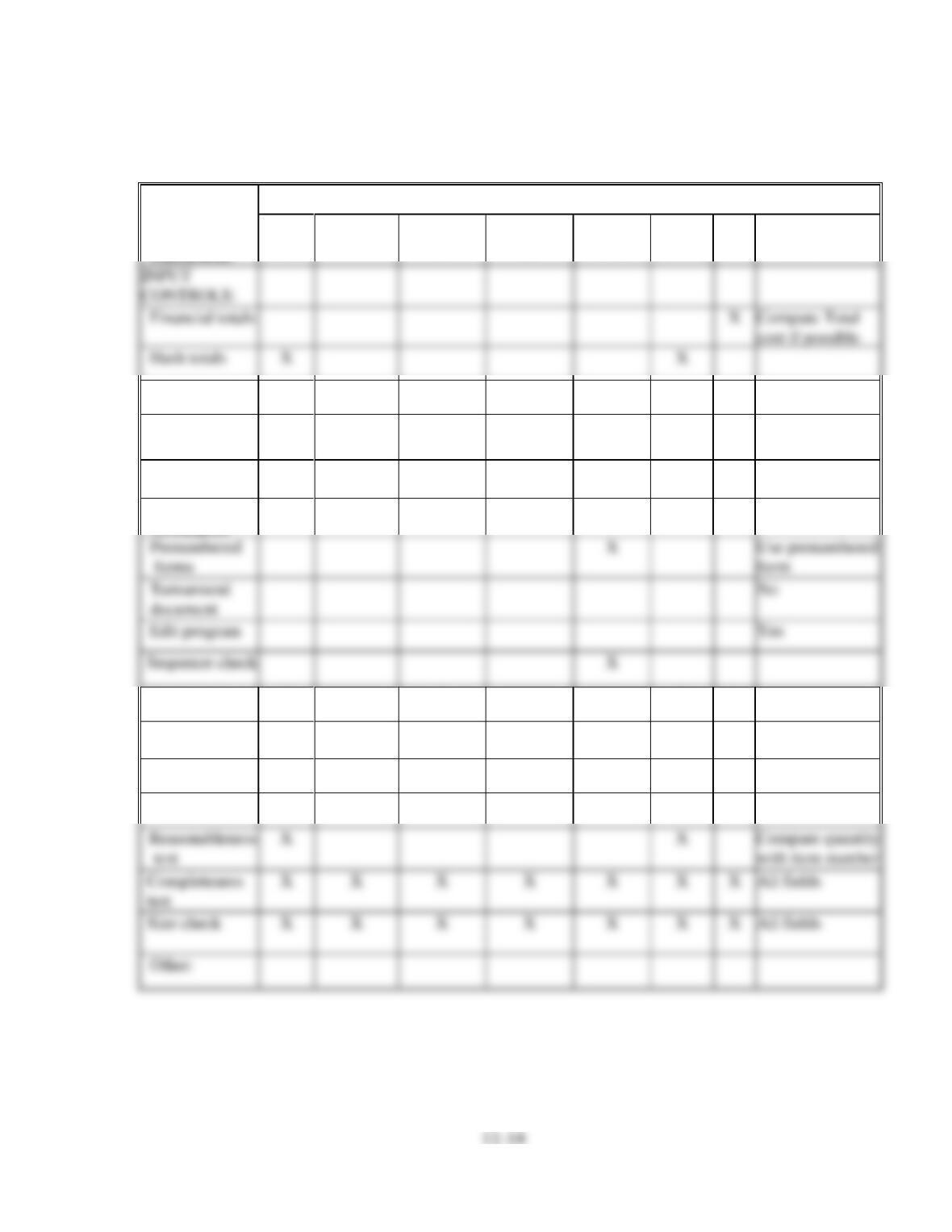

Inventory transactions input control matrix:

RECORD

NAME:

Parts inventory

transactions

FIELD NAMES

Item

number

Description

Transaction

date

Transaction

type

Document

number

Quantity

Unit

cost

Comments

Hash totals

Record counts

Yes

Cross-footing

balance

No

Visual

inspection

X

X

X

X

X

X

X

All fields

Check digit

verification

X

Field check

X

X

X

X

Sign check

X

X

Also for balance

on hand

Validity check

X

X

X

Limit check

Other:

Accounting Information Systems

11-15

11.8 As an internal auditor for the state auditor’s office, you are assigned to review the implementation of a

new computer system in the state welfare agency. The agency is installing an online computer system to

maintain the state’s database of welfare recipients. Under the old system, applicants for welfare

assistance completed a form giving their name, address, and other personal data, plus details about

their income, assets, dependents, and other data needed to establish eligibility. The data are checked by

welfare examiners to verify their authenticity, certify the applicant’s eligibility for assistance, and

determine the form and amount of aid.

a. Describe how to employ concurrent audit techniques to reduce the risks of fraud and

abuse.

Audits should be concerned about a dishonest welfare examiner or unauthorized person

submitting fictitious transactions into the system. Fictitious transactions could cause

excessive welfare benefits to be paid to a valid welfare recipient, or payments made to an

ineligible or fictitious recipient.

The concurrent audit techniques needed most deal with submitting changes in record status

from “pending” to “approved” and modifying welfare records to reflect changes in the

recipient’s circumstances. The auditor should verify that the system is set up to:

• check the password of every person who uses the system

Ch. 11: Auditing Computer-Based Information Systems

11-16

• Any welfare record status change or modification that is entered into the system by

someone other than one of the authorized welfare examiners.

• Assuming that it takes a minimum of n days for a welfare examiner to verify the

• Any attempt to access the system by someone not able to supply a valid welfare clerk or

welfare examiner password.

• Any record entered into the system at a time of day other than during the agency’s normal

business hours, or one that is entered during a weekend or holiday period.

Undoubtedly, other useful audit hooks could be identified. The audit staff should

Accounting Information Systems

11-17

b. Describe how to use computer audit software to review the work welfare examiners do to

verify applicant eligibility data. Assume that the state auditor’s office has access to other

state and local government agency databases.

Computer audit software can process the welfare recipient database against other databases that

contain data about welfare recipients, identify any discrepancies in the data items used to determine

eligibility for benefits and/or calculate the amount of benefits, and report these discrepancies to the

audit staff. Other possible databases that might be used for this purpose would include:

• State income tax records, which contain data on the income and dependents of welfare

recipients.

• Property tax records, which might contain data about valuable assets owned.

• Death records, which would reflect changes in eligibility for benefits. The reason it is

important to review these is that a very common fraud scheme involves failure to enter a death

record, followed by the diversion of subsequent benefit checks.

If a welfare recipient does not appear in any of the first four databases listed above, it would raise

the issue of whether the person exists at all (e.g., is the welfare recipient a fictitious person?). To

investigate this, driver license registration records and voter registration records could also be

checked. If the recipient does not show up there, the audit staff should probably insist that a

Ch. 11: Auditing Computer-Based Information Systems

11-18

11.9 Melinda Robinson, the director of internal auditing at Sachem Manufacturing Company,

believes the company should purchase software to assist in the financial and procedural

audits her department conducts. Robinson is considering the following software packages:

• A generalized audit software package to assist in basic audit work, such as the retrieval of

live data from large computer files. The department would review this information using

conventional audit investigation techniques. The department could perform criteria

selection, sampling, basic computations for quantitative analysis, record handling,

graphical analysis, and print output (i.e., confirmations).

a. Without regard to any specific computer audit software, identify the general advantages

of using computer audit software to assist with audits.

• Audits can be more efficient, saving labor time spent on routine calculations. The routine

operations of footing extensions, transcription between reports, report generation, etc., are

performed by the computer.

b. Describe the audit purpose facilitated and the procedural steps to be followed by the

internal auditor in using the following:

Generalized audit software package. The purpose of generalized audit software programs

is to perform a variety of auditing operations on the computer files used to store the

information. The steps to be followed by the internal auditor to use generalized computer

audit software would include things such as planning and designing the audit application.

Accounting Information Systems

Flowcharting package The purpose of a control flowcharting package is to interpret the

program source code and generate a program flowchart corresponding to it in order to

facilitate the review of internal controls. To use a control flowcharting package, the internal

auditor should:

Parallel simulation and modeling package The purpose of a parallel simulation package is

to ensure that organizational objectives are being met, ensure compliance to technical

standards, and detect unauthorized program changes. To use a parallel simulation package:

• Run the same data used in the company’s current application program using the

“simulated” application program.

Ch. 11: Auditing Computer-Based Information Systems

11-20

11.10 The fixed-asset master file at Thermo-Bond includes the following data items:

Asset number

Date of retirement (99/99/2099 for assets still in service)

Description

Depreciation method code

Explain several ways auditors can use computer audit software in performing a financial

audit of Thermo-Bond’s fixed assets.

• Edit the file for obvious errors or inconsistencies such as:

o Retired assets that have a non-zero net value.

• Recalculate year-to-date depreciation for each asset record, compare to the amount in the

record, and list all asset records for which a discrepancy exists.

• Prepare a list of all assets retired during the current year for comparison to supporting

documents.

Type code

Depreciation rate

Location code

Useful life (years)

Date of acquisition

Accumulated depreciation at beginning of year

Accounting Information Systems

11-21

11.11 You are auditing the financial statements of a cosmetics distributor that sells thousands of

individual items. The distributor keeps its inventory in its distribution center and in two

public warehouses. At the end of each business day, it updates its inventory file, whose

records contain the following data:

Item number

Cost per item

You will use audit software to examine inventory data as of the date of the distributor’s

physical inventory count. You will perform the following audit procedures:

1. Observe the distributor’s physical inventory count at year-end and test a sample for

accuracy.

2. Compare the auditor’s test counts with the inventory records.

3. Compare the company’s physical count data with the inventory records.

Describe how the use of the audit software package and a copy of the inventory file data

might be helpful to the auditor in performing each of these auditing procedures.

(CPA Examination, adapted)

Item description

Date of last purchase

Date of last sale

Item location

Quantity sold during year

Ch. 11: Auditing Computer-Based Information Systems

11-22

Audit Procedure

How Audit Software Can Help

1. Observe the distributor’s physical count

of inventories as of a given date, and

test a sample of the distributor’s

inventory counts for accuracy.

Determine which items are to be test counted by

taking a random sample of a representative

number of items from the inventory file as of the

date of the physical count.

4. Test the mathematical accuracy of the

distributors’ final inventory valuation.

Calculate the dollar value of each inventory item

counted by multiplying the quantity on hand by

the cost per unit, and then verify the addition of

the extended dollar values.

5. Test the pricing of the inventory by

obtaining a list of costs per item from

7. Ascertain the propriety of items of

inventory located in public warehouses.

Prepare a list of items located in public

warehouses.

8. Analyze inventory for evidence of

possible obsolescence.

Prepare a list of items on the inventory file for

which the date of last sale indicates a lack of

recent transactions.

9. Analyze inventory for evidence of

possible overstocking or slow-moving

items.

Prepare a list of items on the inventory file for

which the quantity on hand is excessive in

relation to the quantity sold during the year.

of each inventory item counted, to the inventory

Accounting Information Systems

11–23

11.12 Which of the following should have the primary responsibility to detect and correct data

processing errors? Explain why that function should have primary responsibility and why

the others should not. (CPA Examination, adapted)

a. The data processing manager – The data processing manager should have primary

responsibility to detect and correct data processing errors. The data processing manager has

b. The computer operator – Although the computer operator is responsible for the operation of the

hardware and software of the organization, he is not responsible for detecting and correcting data

c. The corporate controller – The corporate controller has overall responsibility for the operation

of the accounting function, but would not have primary responsibility to detect and correct data

processing errors.

d. The independent public accountant – The independent auditor has no responsibility to detect

Ch. 11: Auditing Computer-Based Information Systems

11-24

SUGGESTED SOLUTIONS TO THE CASES

11.1 You are performing a financial audit of the general ledger accounts of Preston

Manufacturing. As transactions are processed, summary journal entries are added to the

general ledger file at the end of the day. At the end of each day, the general journal file is

processed against the general ledger control file to compute a new current balance for each

account and to print a trial balance.

The following resources are available as you complete the audit:

• Your firm’s generalized computer audit software

Create an audit program for Preston Manufacturing. For each audit step, list the audit

objectives and the procedures you would use to accomplish the audit program step.

General Journal

Field Name

Field Type

Account number

Numeric

Amount

Monetary

Debit/credit code

Alphanumeric

Date (MM/DD/YY)

Date

Reference document type

Alphanumeric

Numeric

General Ledger

Control

Field Name

Field Type

Account number

Numeric

Account name

Alphanumeric

Beginning balance/year

Monetary

Beg-bal-debit/credit code

Alphanumeric

Current balance

Monetary

Cur-bal-debit/credit code

Alphanumeric

Accounting Information Systems

AUDIT PROGRAM

AUDIT OBJECTIVES AND PROCEDURES

a. Edit the general journal file for errors and

inconsistencies such as:

• Invalid debit/credit code or document type.

amount, or document number fields.

Objective: Evaluate the quality of the file data.

Procedures: Review error listing for common

error patterns; initiate correction of the errors;

b. Edit the general ledger file for errors and

exceptions such as:

• Invalid debit/credit codes.

Objective: Evaluate the quality of the file data

Procedures: Review errors listing for common

error patterns; initiate error correction; trace

c. Select a sample of general journal

transactions, stratified by dollar value. Sort

and list by document type.

files by account number, and list all

unmatched general journal entries. (or look

them up in the appropriate tables)

Procedures: Compare unmatched transaction

data values to source documents; initiate errors

Objective: Test the transaction data entry

accuracy.

Procedures: Compare transaction data values to

source documents and identify discrepancies.

e. Recalculate each ledger account’s current

balance from the beginning balance and the

general journal amounts, and list any

discrepancies between the recalculated

balance and the file balance.

Objective: Test current ledger balance

accuracy.

Procedures: Review discrepancies to see if the

transaction amounts or ledger balances are

erroneous; initiate appropriate corrections.

f. Prepare comparative financial statements for

the current and prior year, including

selected liquidity, profitability, and capital

structure ratios.

Objective: Identify accounts to be investigated

in detail.

Procedures: Analytical review of ratios and

trends to search for unusual account balances.