CHAPTER 11

UNDERSTANDING THE ISSUES

1. If major cash inflows and/or outflows are

not denominated in the entity’s domestic

currency, this is a strong indicator that

another currency is the functional currency.

2. Because the French company’s functional

currency is the euro, it is not exposed to

risk associated with exchange rate changes

between the euro and the U.S. dollar (the

parent’s currency). Changes in the ex-

change rates will not have a current or

3. Because the euro is the subsidiary’s func-

tional currency, its financial statements will

4. In order for there to be a remeasurement

loss, the foreign currency (FC) would have

to weaken against the dollar (a strengthen-

ing dollar). The remeasurement loss would

be included in current-period earnings, and

the U.S. parent would want to hedge

remeasurement loss. Given a weakening

FC, an FC-denominated loan receivable

would not be an effective hedge of the net

investment in the subsidiary.

5. If a foreign entity’s functional currency is

highly inflationary, there is an assumption

order to overcome these unusual results,

two possible approaches have been

proposed. The first approach would adjust

tional currency (dollars).

Ch. 11—Exercises 11–2

EXERCISES

EXERCISE 11-1

(1) Debit Debit

(Credit) (Credit)

December 31, 1 FC = December 31,

2015 2015

Current Assets ………………………………………. 165,000 FC $1.92 $ 316,800

Long-Lived Assets (net) ………………………….. 420,000 1.92 806,400

Other Assets …………………………………………. 170,000 1.92 326,400

Cost of Sales …………………………………………. 525,000 1.96 1,029,000

Other Expenses …………………………………….. 205,000 1.96 401,800

Note A: Translation of Retained Earnings

In FC 1 FC = In U.S.$

December 31, 2014 balance ………. 140,000 Given $227,300

2015 income …………………………….. 180,000 $1.92 345,600

(2) Cumulative Translation Adjustment Traceable to Years Prior to 2015

Debit

(Credit)

11–3 Ch. 11—Exercises

Exercise 11-1, Concluded

Year 2015 Translation Adjustment

Debit

(Credit)

In U.S.$

Net assets at beginning of 2015 multiplied by change in exchange

rates during the period:

$12,800

(3) Debit Debit

(Credit) (Credit)

December 31, 1 FC = December 31,

2014 2014

Current Assets ………………………………………. 185,000 FC $1.95 $ 360,750

Long-Lived Assets (net) ………………………….. 400,000 1.95 780,000

Other Assets …………………………………………. 165,000 1.95 321,750

Cost of Sales …………………………………………. 425,000 1.92 816,000

(4) Reduction in 2015 Translation Adjustment Due to Hedge

Value of loan payable at December 31, 2015 (100,000 FC × $1.92) ….. $192,000

Value of loan payable at March 1, 2015 (100,000 FC × $2.02) …………. 202,000

Change in value of loan payable …………………………………………………… $ (10,000)

Debit

(Credit)

In U.S.$

EXERCISE 11-2

Remeasured no par common stock:

Exchange Remeasured

FC Value Rate Value

Common stock at January 1, 2014……………… 200,000 $1.61 $322,000

Remeasured retained earnings (Excluding Remeasurement Gain or Loss):

Exchange Remeasured

FC Value Rate Value

Retained earnings at January 1, 2014 …………. 150,000 $1.61 $241,500

2014 net income:

Net sales …………………………………………. 1,350,000 $1.63 2,200,500

Cost of sales:

Most recent purchase ……………………. (500,000) $1.64 (820,000)

Next most recent purchase ……………. (400,000) $1.62 (648,000)

Depreciation expense:

July 1, 2013 equipment …………………. (20,000) $1.61 (32,200)

September 30, 2014 equipment ……… (1,000) $1.65 (1,650)

2015 net income:

Net sales …………………………………………. 2,240,000 $1.70 $3,808,000

Cost of sales:

Most recent purchase ……………………. (500,000) $1.68 (840,000)

Next most recent purchase ……………. (300,000) $1.75 (525,000)

Next most recent purchase ……………. (600,000) $1.73 (1,038,000)

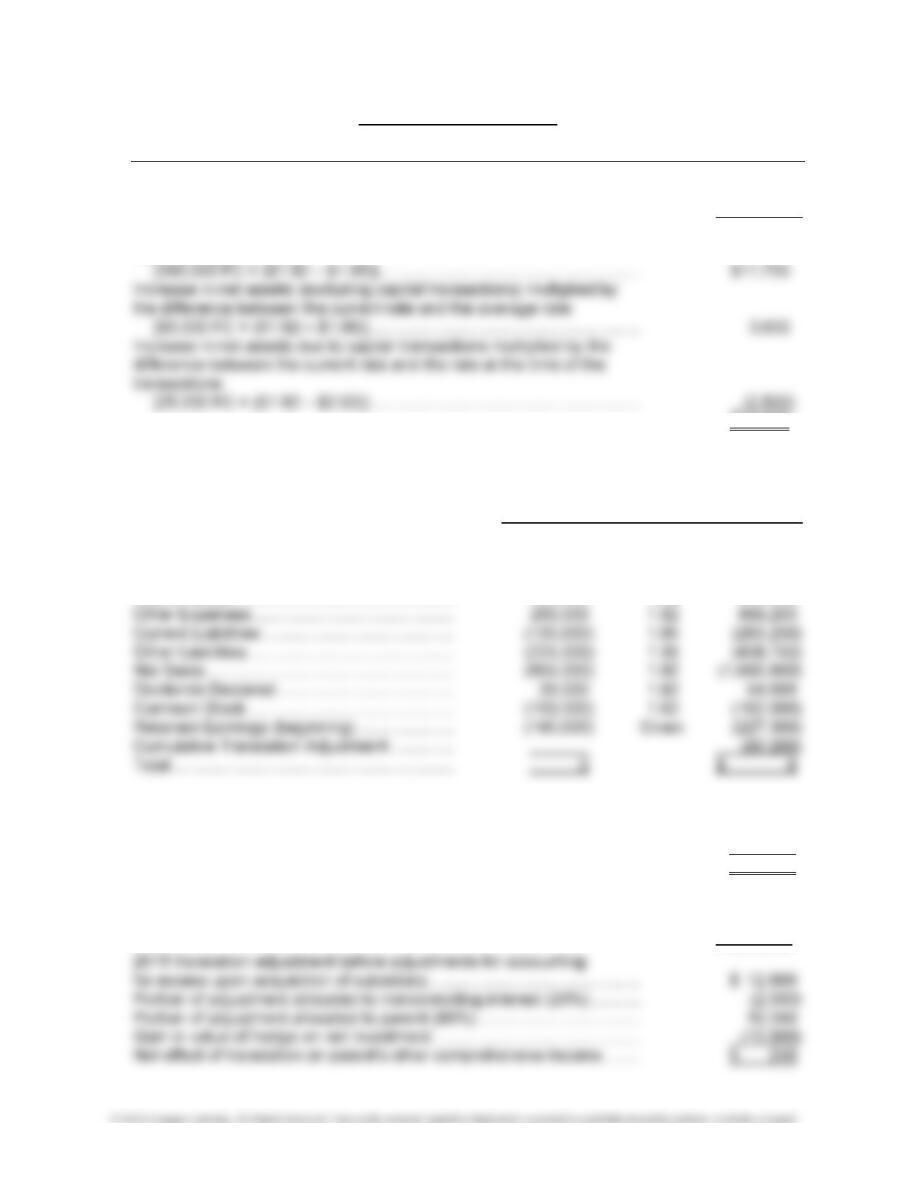

EXERCISE 11-3

June 30 Investment in Fabinet ………………………………………….. 3,120,000

Cash ……………………………………………………………. 3,120,000

To record purchase of 40% interest in Fabinet.

Dec 31 Investment in Fabinet ………………………………………….. 565,712

Subsidiary Income …………………………………………. 210,560

Translation Adjustment …………………………………… 355,152

Schedule A—Calculation of Investor’s Share of Adjusted Equity Income

Price paid ($3,120,000/$0.60) …………………………………………………. 5,200,000 FC

Equity purchased …………………………………………….. 10,500,000 FC

40% Interest acquired ………………………………………. × 40% 4,200,000

Excess cost ………………………………………………………………………….. 1,000,000 FC

Allocation of excess cost:

Equipment ($240,000/$0.60) ……………………………………………… 400,000 FC

Schedule B—Recomputation of Annual Translation Adjustment

Net assets owned by the investee at the beginning of period multiplied by

the change in the exchange rates during the period [10,500,000 FC ×

($0.68 – $0.60)] ……………………………………………………………………………….. $840,000

Increase in net assets (excluding capital transactions) multiplied by the

difference between the current rate and the average rate used to

EXERCISE 11-4

Translated net income: Exchange

Debit (Credit) In FC Rate In U.S.$

Sales Revenue ………………………………………. (1,022,000) FC $1.19 $(1,216,180)

Cost of Inventory Sold …………………………….. 480,000 Note A 564,100

Remeasurement gain (loss): In FC Rate In U.S.$

Net assets at December 31, 2016:

Monetary net assets ………………………….. 732,000 FC $1.23 $ 900,360

Inventory …………………………………………. 100,000 1.20 120,000

Depreciable assets (net) ……………………. 870,000 1.15 1,000,500

Net investment under the sophisticated equity method:

Initial investment ………………………………………………………………………………….. $700,000

Share of subsidiary net income (30% × $488,680) ……………………………………. 146,604

Share of remeasurement gain (30% × $37,180) ……………………………………….. 11,154

Amortization of excess of cost over book value (Note B) ……………………………. (6,000)

Net investment as of December 31, 2016 ………………………………………………… $851,758

Note B

Cost ………………………………………………………………………….. $700,000

Book value:

11–7 Ch. 11—Exercises

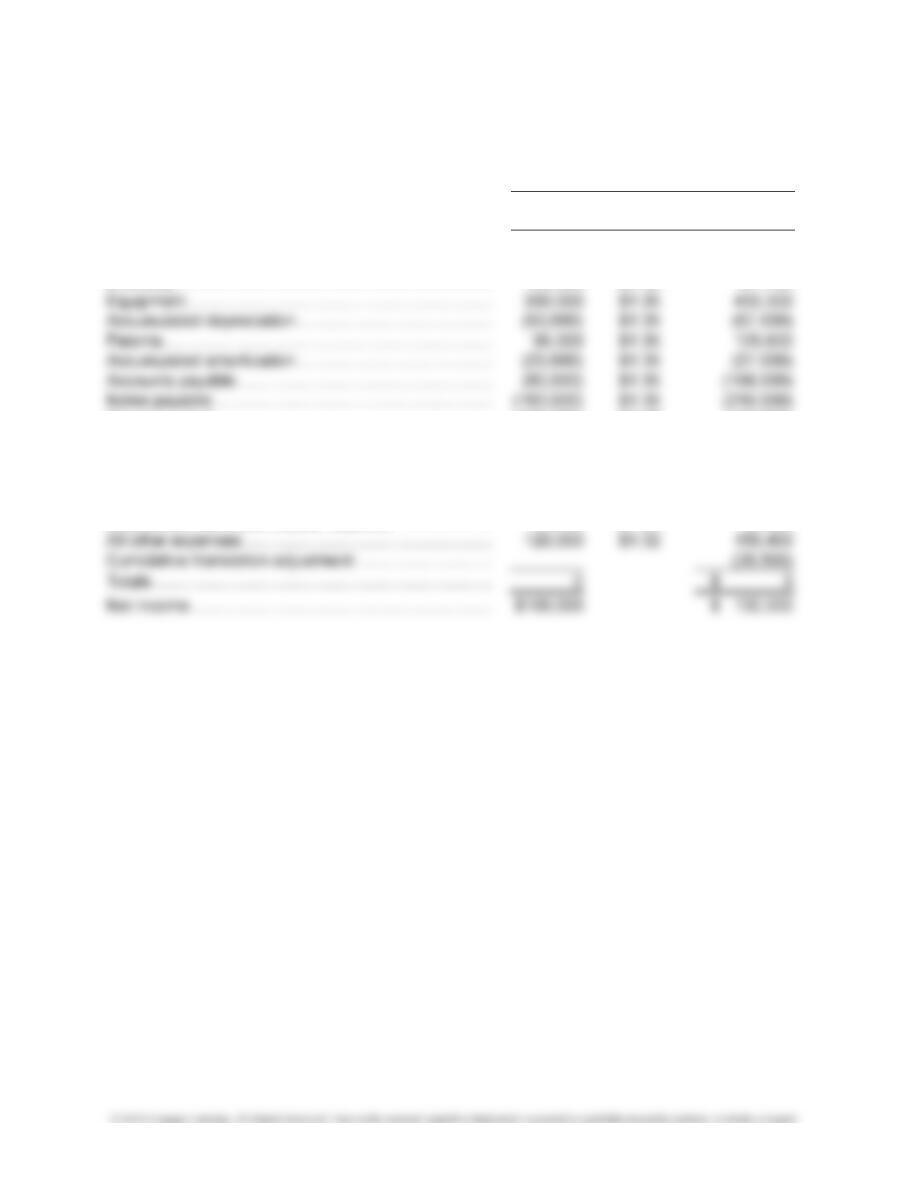

EXERCISE 11-5

Calculation of cumulative translation as of yearend 2014:

December 31, 2014

In FC

Exchange

Rate In $

Cash and cash equivalents ………………………………….. 71,000 $1.35 $ 95,850

Accounts receivables ………………………………………….. 148,000 $1.35 199,800

Inventory …………………………………………………………… 105,000 $1.35 141,750

Common stock …………………………………………………… (106,000) $1.25 (132,500)

Retained earnings – beginning ……………………………… (254,000) $1.25 (317,500)

Retained earnings – dividend ……………………………….. 50,000 $1.30 65,000

Net sales …………………………………………………………… (620,000) $1.32 (818,400)

Cost of sales ……………………………………………………… 372,000 $1.32 491,040

Depreciation and amortization expense …………………. 28,000 $1.32 36,960

Ch. 11—Exercises 11–8

Calculation of cumulative translation as of yearend 2015:

December 31, 2015

In FC

Exchange

Rate In $

Cash and cash equivalents ………………………………….. 52,000 $1.21 $ 62,920

Accounts receivables ………………………………………….. 120,000 $1.21 145,200

Inventory …………………………………………………………… 140,000 $1.21 169,400

Equipment …………………………………………………………. 360,000 $1.21 435,600

Accumulated depreciation ……………………………………. (73,000) $1.21 (88,330)

Patents ……………………………………………………………… 96,000 $1.21 116,160

Cumulative translation adjustment ………………………… 23,250

Totals ……………………………………………………………….. 0 $ 0

Net income ………………………………………………………… $103,000 $ 129,780

Note A: The beginning retained earnings balance is the translated value of beginning 2014

retained earnings, the 2014 net income, and the 2014 dividend.

Analysis of Excess of cost over book value at acquisition expressed in FC:

Company

Value

Parent 80%

Value

NCI 20%

Value

Fair value of subsidiary ( 400,000 FC / 80%) …… 500,000 400,000 100,000

Less book value of interest acquired:

Common stock ………………………………………. 106,000

11–9 Ch. 11—Exercises

Allocation of income to NCI:

2014 2015

Internally generated net income ………………………………………………….. $ 132,000 $129,780

Amortization of patent portion of excess:

EXERCISE 11-6

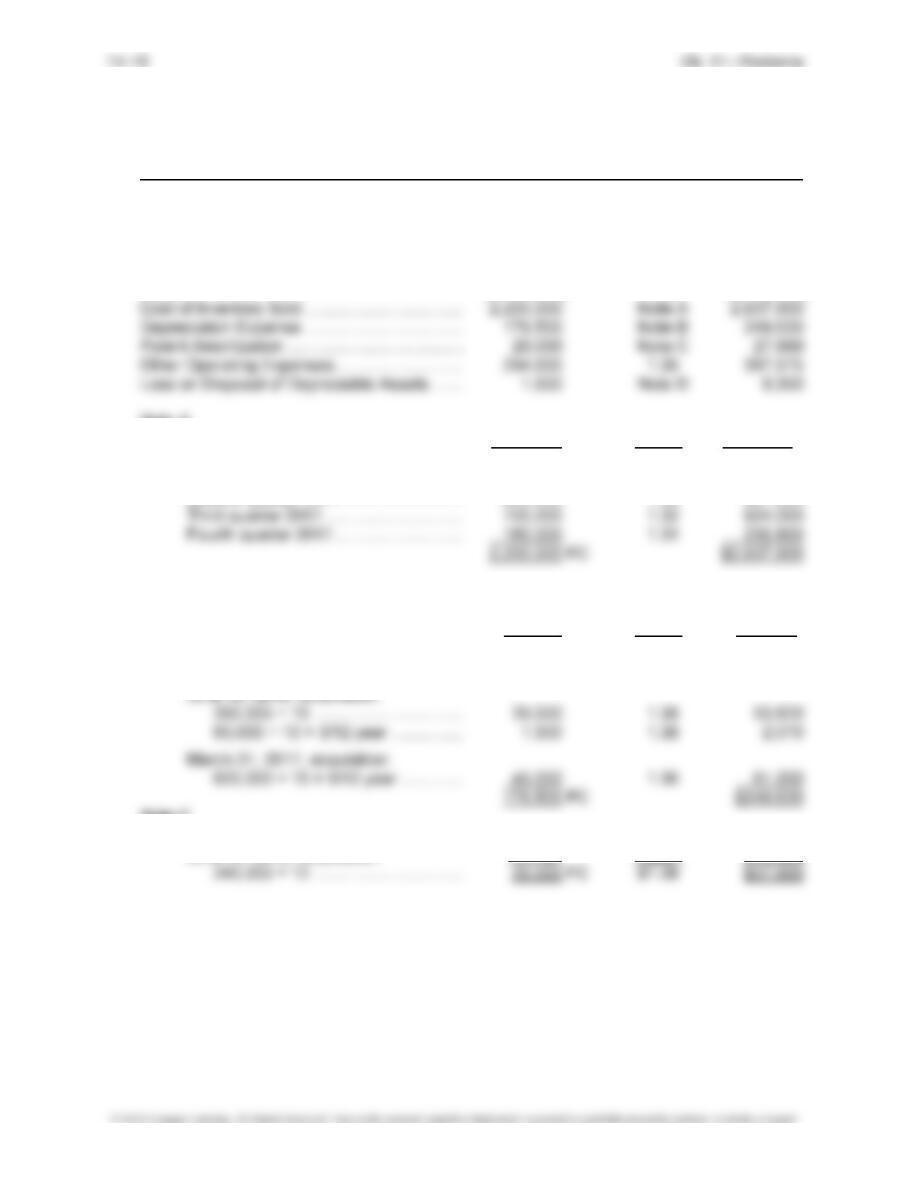

(1) Several factors that might explain why the U.S. dollar is the functional currency include:

• The subsidiary’s equity capital has been provided in U.S. dollars.

(2) (a) Remeasurement of Cost of Sales for Product A:

Exchange

Time of Number of FC Cost Total Rate Balance

Purchase Units per Unit FC Cost ($/FC) in Dollars

Third quarter 2014 400 53 21,200 $1.62 $ 34,344

Fourth quarter 2014 900 55 49,500 $1.65 81,675

(b) Remeasurement of Depreciation Expense:

Exchange

Time of Annual Rate Balance

Purchase FC Cost Depreciation ($/FC) in Dollars

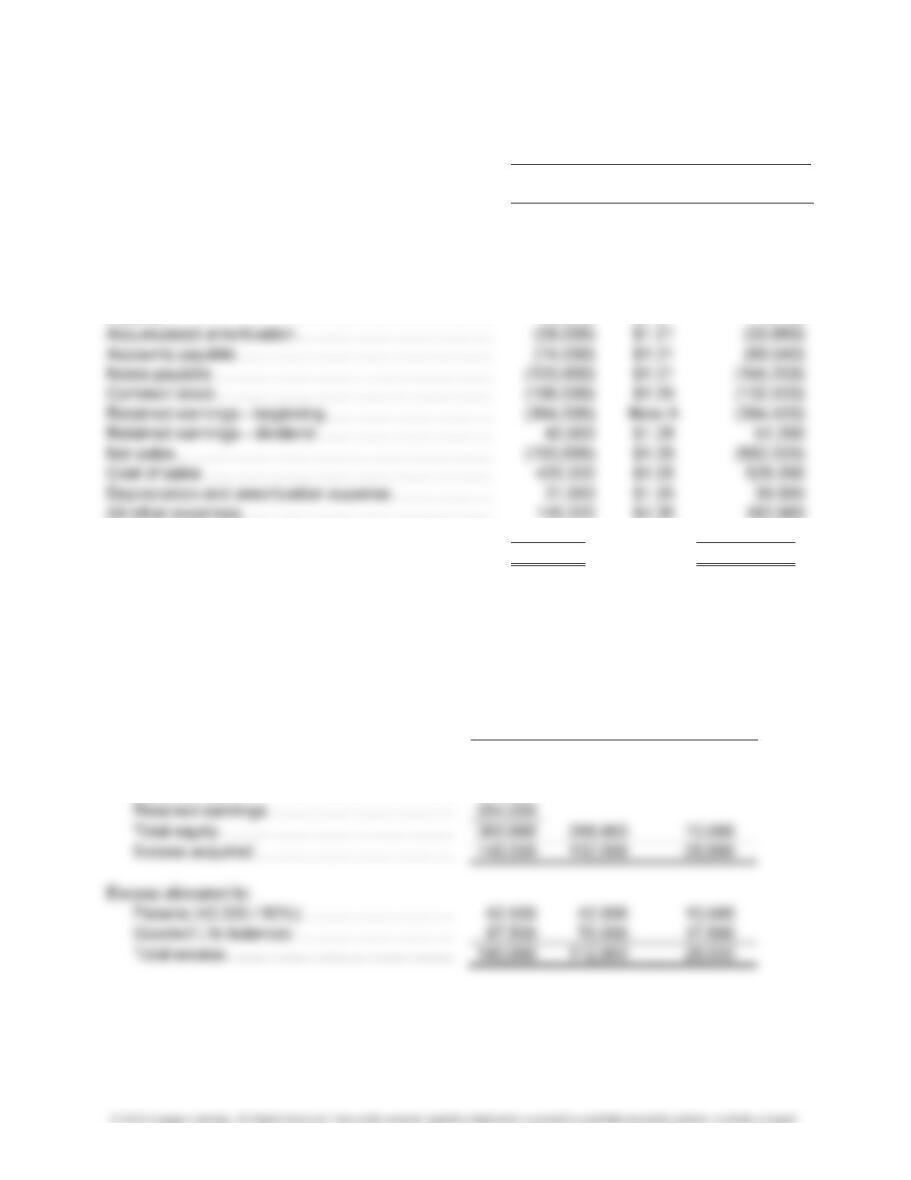

Exercise 11-6, Concluded

(c) Remeasurement of Patent Amortization Expense:

Half-Year

Time of 20X6

Purchase $ Cost Amortization

March 1, 2013 $108,000 $4,500

Remeasurement of Impairment Loss on Patent:

Book value of patent at June 30, 2015:

Original cost. …………………………………… $108,000

Less amortization:

2013 ………………………………………………. (7,500)

(d) Interest Expense and Transaction Exchange Gain/Loss on Borrowing:

Interest expense (10,000 FCA × 6% × ½ year).. 300 FCA

Transaction Exchange Gain/Loss on Borrowing:

In FCA 1 FCA = In FC 1 FC =

Principal balance:

At June 30, 2015 …………. 10,000 1.20 FC 12,000

11–11 Ch. 11—Exercises

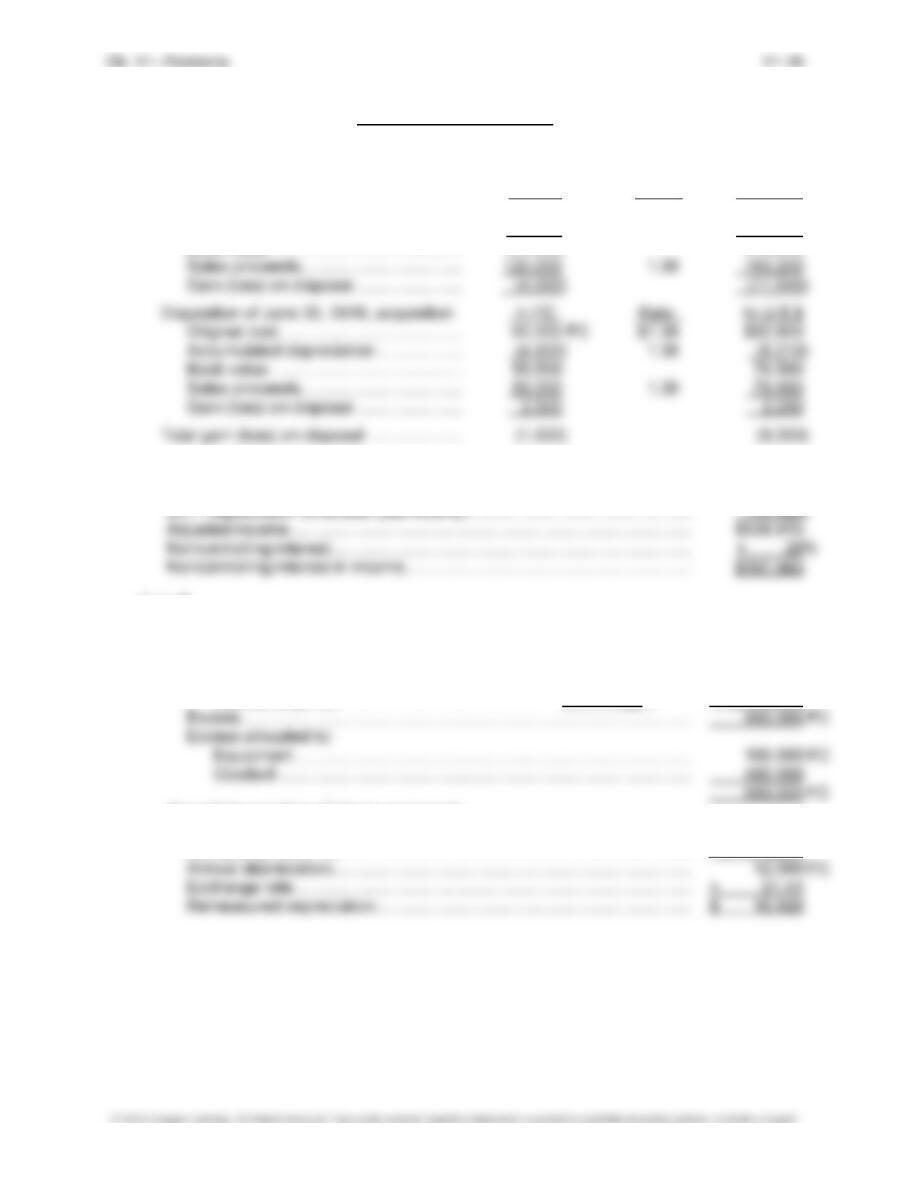

EXERCISE 11-7

Composition of Techno’s Account “Investment in Prefabco:”

Exchange

Rate

In FC (Dollars/FC) In U.S.$ In U.S.$

March 31, 2013, initial investment ……… 400,000 $2.08 $ 832,000

Last 9 months of 2013:

Income × 70% ……………………….. 168,000 2.10 352,800

Dividends × 70% ……………………. (50,400) 2.18 (109,872)

Entries to eliminate the investment account:

1. Subsidiary Income …………………………………………………….. 687,960

Dividends Declared (subsidiary account) ………………… 211,680

2. Capital Stock (140,000 FC × $2.08 × 70%) …………………… 203,840

Retained Earnings …………………………………………………….. 909,353

Investment in Subsidiary ……………………………………….. 1,113,193

To eliminate beginning equity balances against

investment in subsidiary.

Translated Balance of Retained Earnings: In FC (Dollars/FC) In U.S.$

March 31, 2013, pre-closing balance ….. 134,000 $2.08 $ 278,720

First quarter 2013 net income:

Sales ………………………………………… 720,000 2.08 1,497,600

Cost of sales. …………………………….. (504,000) 2.08 (1,048,320)

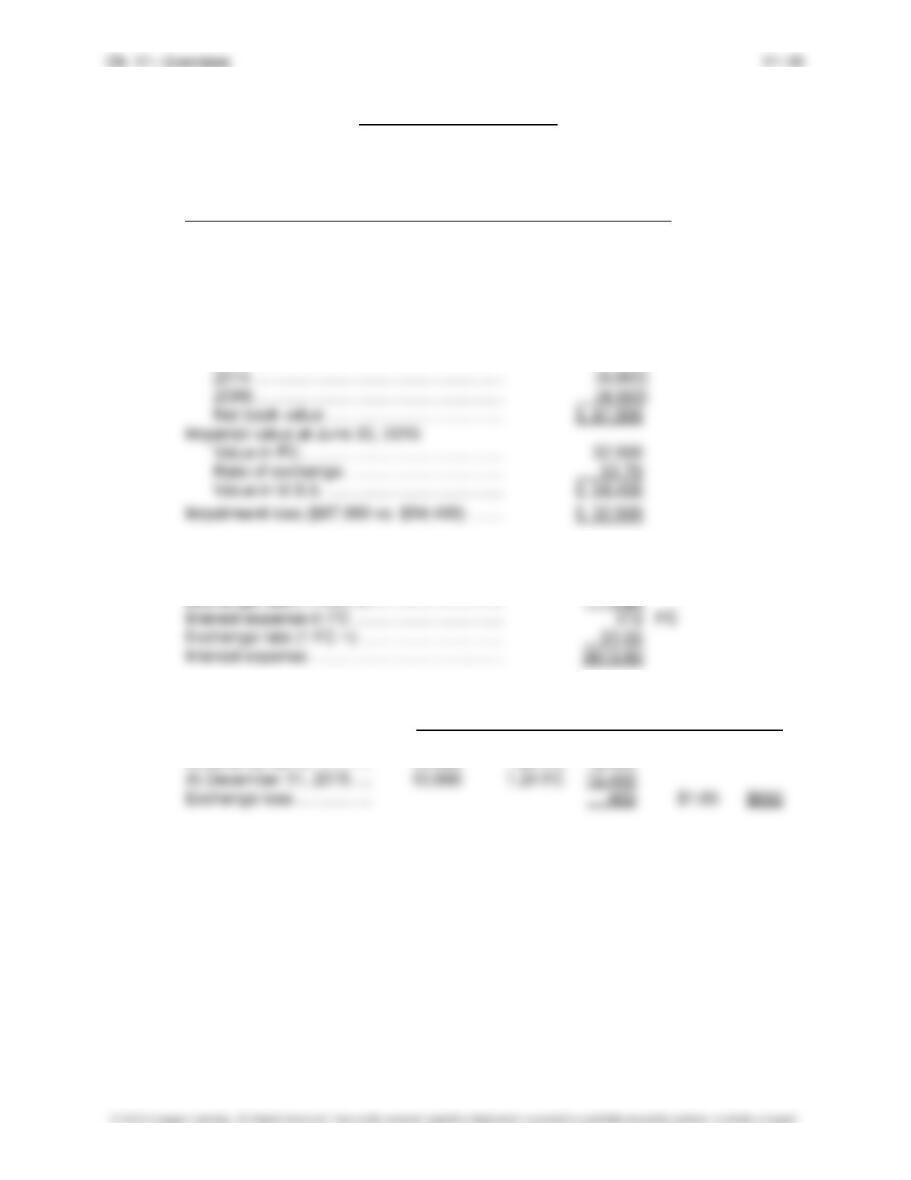

Exercise 11-7, Concluded

3. Other Assets (206,429 × $2.40) ………………………………….. 495,429

Retained Earnings ……………………………………………….. 128,811

Cumulative Translation Adjustment ………………………… 66,057

Investment in Subsidiary ……………………………………….. 300,560

To distribute the excess of cost over book

value—includes exchange rate adjustment.

Allocation of Excess:

To Parent To NCI Total in FC

Other assets …………………………………… 144,500 61,929 206,429

11–13 Ch. 11—Problems

PROBLEMS

PROBLEM 11-1

(1) Entries to record transactions—Debit (Credit):

In FCA In FCB

Cash …………………………………… 1,250,000 100,000

Common Stock …………………. 1,250,000 100,000

Land ……………………………………. 625,000 50,000

Inventory ……………………………… 625,000 50,000

Trial balance:

Trial Balance: In FCA In FCB

Receivable …………………………….. 400,000 FCA 40,000 FCB

Inventory ……………………………….. 312,500 25,000

Land …………………………………….. 625,000 50,000

Problem 11-1, Concluded

(2) Remeasurement and translation of trial balance:

Rate Rate

In FCA

FCB/FCA In FCB U.S.$/FCB In U.S.$

Trial Balance:

Receivable ……………….. 400,000 FCA 0.10 40,000 FCB $3.00 $ 120,000

Inventory ………………….. 312,500 0.08 25,000 3.00 75,000

Land ………………………… 625,000 0.08 50,000 3.00 150,000

(3) Translation adjustment traceable to the current year:

Net assets at beginning of year multiplied by the change in exchange rates

during the period:

100,000 FCB × ($3.00 – $2.50) ……………………………………………………….. $(50,000)

Increase in net assets (excluding capital transactions) multiplied by the

difference between the current rate and the average rates used to translate

(4) The remeasured FCB trial balance is the same as the trial balance that would have resulted

had the transactions been originally recorded in FCB. FCB is the functional currency in

which the company operates, and the remeasurement process should produce a trial bal-

PROBLEM 11-2

(1) Balance Exchange Remeasured

Debit (Credit) in FC Rate into U.S.$

Common Stock ………………………………………. (1,200,000) FC $1.41 $(1,692,000)

Contributed Capital in Excess of

Par Value ………………………………………….. (1,800,000) 1.41 (2,538,000)

Retained Earnings as of

December 31, 2016 …………………………….. (1,000,000) given (1,390,000)

Sales …………………………………………………….. (3,100,000) 1.35 (4,185,000)

Note A

Cost of inventory sold per FIFO: In FC Rate In U.S.$

Fourth quarter 2016 ……………………….. 300,000 FC $1.35 $ 405,000

First quarter 2017 ………………………….. 400,000 1.34 536,000

Second quarter 2017 ……………………… 620,000 1.35 837,000

Note B

Depreciation expense:

January 1, 2015, acquisition: In FC Rate In U.S.$

900,000 ÷ 10 …………………………… 90,000 FC $1.41 $126,900

160,000 ÷ 10 × 3/12 year ………….. 4,000 1.41 5,640

Note C

Patent amortization:

June 30, 2016, acquisition: In FC Rate In U.S.$

Problem 11-2, Concluded

Note D

Loss on disposal of asset:

Disposition of January 1, 2015, acquisition: In FC Rate In U.S.$

Original cost …………………………………. 160,000 FC $1.41 $225,600

Accumulated depreciation ………………. (36,000) 1.41 (50,760)

Book value ……………………………………. 124,000 174,840

(2) Consolidated income traceable to noncontrolling interest:

Income as remeasured …………………………………………………………………… $556,835

Note E

Distribution of excess of cost over book value:

Cost at date of acquisition …………………………………………………………… 3,600,000 FC

Book value at date of acquisition:

Book value ……………………………………………. 3,800,000 FC

Interest acquired ……………………………………. × 80% 3,040,000

Annual depreciation of above equipment:

Allocated excess ……………………………………………………………………….. 100,000 FC

Remaining useful life ………………………………………………………………….. ÷ 8 1/3 years

PROBLEM 11-3

Sorenson Company

Trial Balance Translation

December 31, 2018

Relevant

Balance Exchange Balance

Account in FC Rate in Dollars

Cash ……………………………………………………………. 2,840,000 FC $1.31 $ 3,720,400

Accounts Receivable …………………………………….. 3,990,000 1.31 5,226,900

Inventory ……………………………………………………… 5,800,000 1.31 7,598,000

Fixed Assets ………………………………………………… 15,000,000 1.31 19,650,000

Accumulated Depreciation ……………………………… (6,800,000) 1.31 (8,908,000)

Problem 11-3, Continued

Pueblo Corporation and Sorenson Company

Worksheet for Consolidated Financial Statements (in dollars)

For Year Ended December 31, 2018

Eliminations Consolidated Consolidated

Trial Balance

and Adjustments Income Balance

Pueblo

Sorenson Dr Cr Statement Sheet

Fixed Assets ………………………………………………… 21,000,000 19,650,000 (D) 655,000 …………….. ………………. 41,305,000

Accumulated Depreciation ……………………………… (12,560,000) (8,908,000) …………….. (A) 196,500 ………………. (21,664,500)

Additional Equipment …………………………………….. ……………… ………………. (D) 3,013,000 (A) 451,950 ………………. 2,561,050

Accounts Payable …………………………………………. (3,450,000) (2,069,800) …………….. ………..…… ………………. (5,519,800)

Long-Term Debt ……………………………………………. (10,000,000) (6,550,000) …………….. ……….……. ………………. (16,550,000)

Common Stock—Parent ………………………………… (4,000,000) ………………. …………….. …………….. ………………. (4,000,000)

Common Stock—Subsidiary …………………………… ……………… (3,600,000) (EL) 3,600,000 …………….. ………………. ……………….

11–19 Ch. 11—Problems

Problem 11-3, Concluded

Eliminations and Adjustments:

(CY1) Eliminate the subsidiary income account ($1,729,000) against the investment account.

(EL) Eliminate the subsidiary’s January 1, 2018, equity balances against the investment

account.

(D) Distribute the excess of cost over book value.

Cost to acquire subsidiary ………………………………………………………. 12,000,000 FC

Book value of subsidiary ………………………………………………………… 9,200,000

Excess of cost over book value ……………………………………………….. 2,800,000 FC

(A) Record appropriate depreciation of excess.

Annual depreciation of excess:

Equipment (500,000 FC ÷ 10) ……………………………………………. 50,000 FC

Additional equipment (2,300,000 FC ÷ 20) …………………………… 115,000

Total …………………………………………………………………………. 165,000 FC

Accumulated depreciation at December 31, 2018, in dollars:

Equipment (50,000 × 3 years × $1.31) ………………………………… $196,500