PROBLEM 11-2B (Continued)

(d) Payout ratio= $302,400

$408,000 =74.1%

Return on common stockholders’ equity =

PROBLEM 11-3B

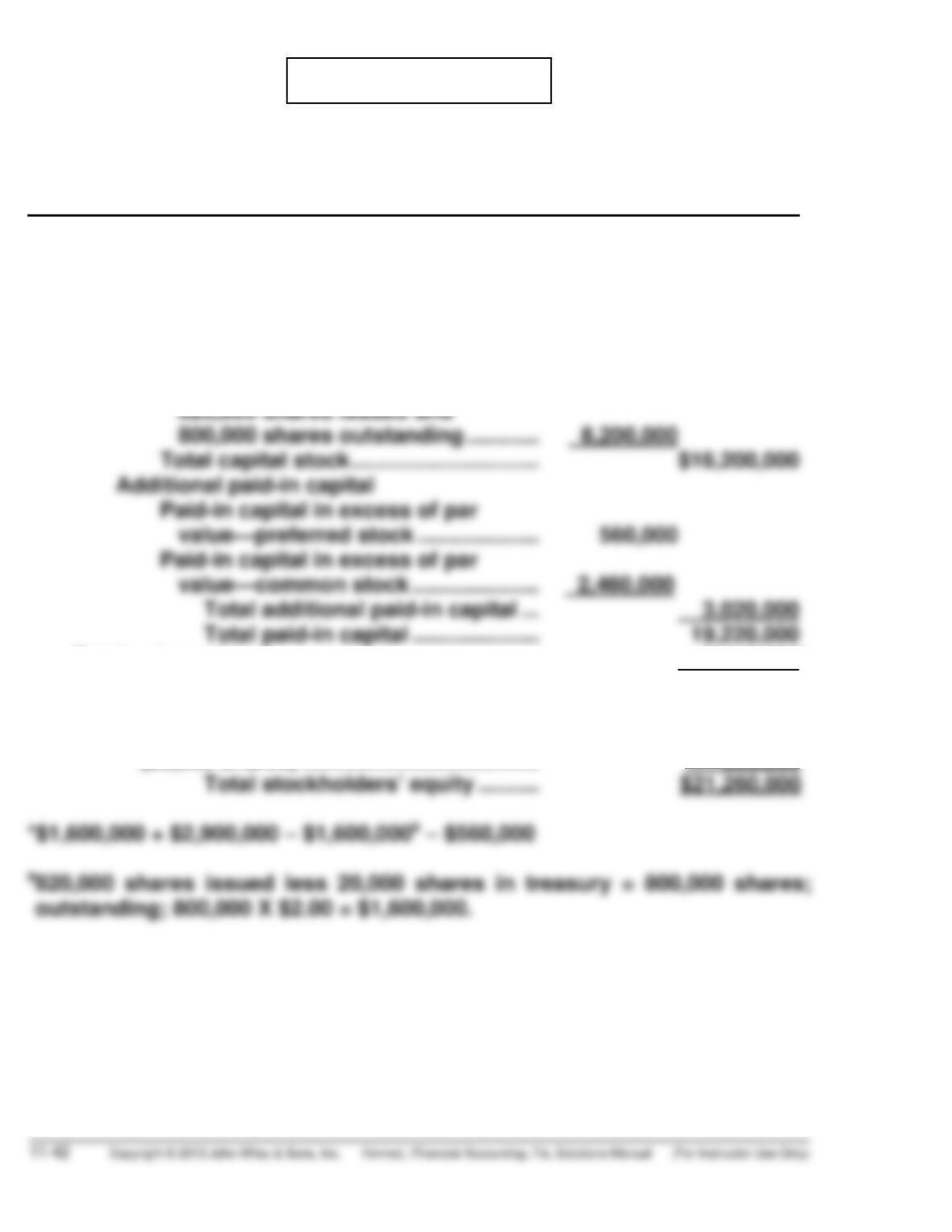

PEABODY COMPANY

Partial Balance Sheet

December 31, 2014

Stockholders’ equity

Paid-in capital

Capital stock

7% Preferred stock, $100 par value,

cumulative, 80,000 shares issued

and outstanding …………………………. $8,000,000

Common stock, $10 par value,

Retained earnings ……………………………………… 2,340,000*

Total paid-in capital and

retained earnings …………………. 21,560,000

Less: Treasury stock—common

(20,000 shares) ………………………………… 300,000

PROBLEM 11-4B

(a) Retained Earnings

Dec. 31 380,000 Jan. 1 Balance 800,000

(b) DONDEC CORPORATION

Partial Balance Sheet

December 31, 2014

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $50 par

value, cumulative, 20,000

shares authorized, 6,000 shares

Additional paid-in capital

Paid-in capital in excess of par

value—preferred stock ………………….. 250,000

Paid-in capital in excess of par

PROBLEM 11-5B

(a) (1) Cash ……………………………………………………… 452,000

Preferred Stock (4,000 X $100) …………. 400,000

PROBLEM 11-5B (Continued)

(b) HARTWELL CORPORATION

Partial Balance Sheet

December 31, 2014

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100

par value, noncumulative,

Additional paid-in capital

Paid-in capital in excess of par

value—preferred stock …………… 52,000

Paid-in capital in excess of stated

PROBLEM 11-6B

FERRIS INC.

Partial Balance Sheet

December 31, 2014

Stockholders’ equity

Paid-in capital

Common stock, $5 par value, 2,000,000 shares

authorized, 735,000* shares issued, and

710,000 shares outstanding …………………………………….. $3,675,000

Additional paid-in capital

Paid-in capital in excess of par value—

PROBLEM 11-7B

2014 2013

(a) (i) Return on assets

$800,000

$5,312,500 = 15.1% $900,000

$6,230,000 = 14.4%

(ii) Return on common

$800,000 −$40,000

(b) Hercules Company’s net income decreased $100,000 in 2014 even

though its sales remained constant. Its return on assets, 15.1%

PROBLEM 11-7B (Continued)

(d) It appears that the decision to issue bonds and purchase treasury stock

was a wise choice. The bonds require payment of 8% interest which is

less than Hercules 15.1% return on assets. This positive difference

*PROBLEM 11-8B

(a) Feb. 1 Cash Dividends (80,000 X $1.00) …… 80,000

Dividends Payable …………………. 80,000

Mar. 1 Dividends Payable ……………………….. 80,000

Cash ……………………………………… 80,000

Dec. 1 Cash Dividends (92,000 X $1) ……….. 92,000

Dividends Payable …………………. 92,000

31 Income Summary …………………………. 500,000

Retained Earnings …………………. 500,000

*PROBLEM 11-8B (Continued)

(b)

Common Stock Retained Earnings

1/1 Bal. 1,600,000 12/31 300,000 1/1 Bal. 750,000

Paid-in Capital

in Excess of Par Value

Common Stock

Dividends Distributable

1/1 Bal. 240,000 7/31 240,000 7/1 240,000

Cash Dividends Stock Dividends

2/1 80,000

7/1 300,000

*PROBLEM 11-8B (Continued)

(c) LAMAR CORPORATION

Partial Balance Sheet

December 31, 2014

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $20 par value,

92,000 shares issued and

(d) Payout ratio = $172,000a

$500,000 =34.4%

COMPREHENSIVE PROBLEM SOLUTION

(a) 1. Cash ………………………………………………………..

Preferred Stock …………………………………

49,200

48,000

2. Cash ………………………………………………………..

Common Stock ………………………………….

21,000

9,000

3. Accounts Receivable ………………………………..

Service Revenue ……………………………….

320,000

320,000

6. Supplies …………………………………………………..

Accounts Payable ……………………………..

35,100

35,100

7. Accounts Payable …………………………………….

Cash …………………………………………………

32,200

32,200

10. Cash Dividends ($3,360 + $10,200*) …………..

Dividends Payable …………………………….

13,560

13,560

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Adjusting Entries

1. Supplies Expense ($4,400 + $35,100

–

$5,900)…

Supplies …………………………………………….

33,600

33,600

–

–

(b) KLINGER CORPORATION

Adjusted Trial Balance

12/31/14

Account Debit Credit

Cash ……………………………………………………………

.

$175,200

Accounts Receivable……………………………………

.

87,800

Allowance for Doubtful Accounts …………………

.

$ 3,500

Su

pp

lies ………………………………………………………

.

5,900

.

.

Service Revenue ………………………………………….

.

347,000

Bad Debt Expense ……………………………………….

.

3,700

De

p

reciation Ex

p

ense ………………………………….

.

4,400

pp

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) Optional T Accounts

Cash

Bal. 24,600

49,200

A

32,200

11,200

Accounts Receivable

Bal. 45,500

276,000

Supplies

Bal. 4,400

35,100

33,600

A

ccum. Depreciation

—

Buildings

Bal. 22,000

4,400

32,200 Bal. 25,600

35,100

Bal. 28,500

Dividends Payable

13,560

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) (Continued)

Common Stock

Bal. 80,000

Paid-in Capital in Excess

of Par Value—C.S.

12,000

Retained Earnings

Bad Debt Expense

3,700

Supplies Expense

33,600

Other Operating Expenses

Income Tax Expense

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(d) KLINGER CORPORATION

Income Statement

For the Year ending December 31, 2014

Service revenue ……………………………………

.

$347,000

Operating expenses

Other operating expenses………………

.

$188,200

.

KLINGER CORPORATION

Statement of Retained Earnings

For the Year ending December 31, 2014

Retained earnings, 1/1/14 …………………………………….. $127,400

COMPREHENSIVE PROBLEM SOLUTION (Continued)

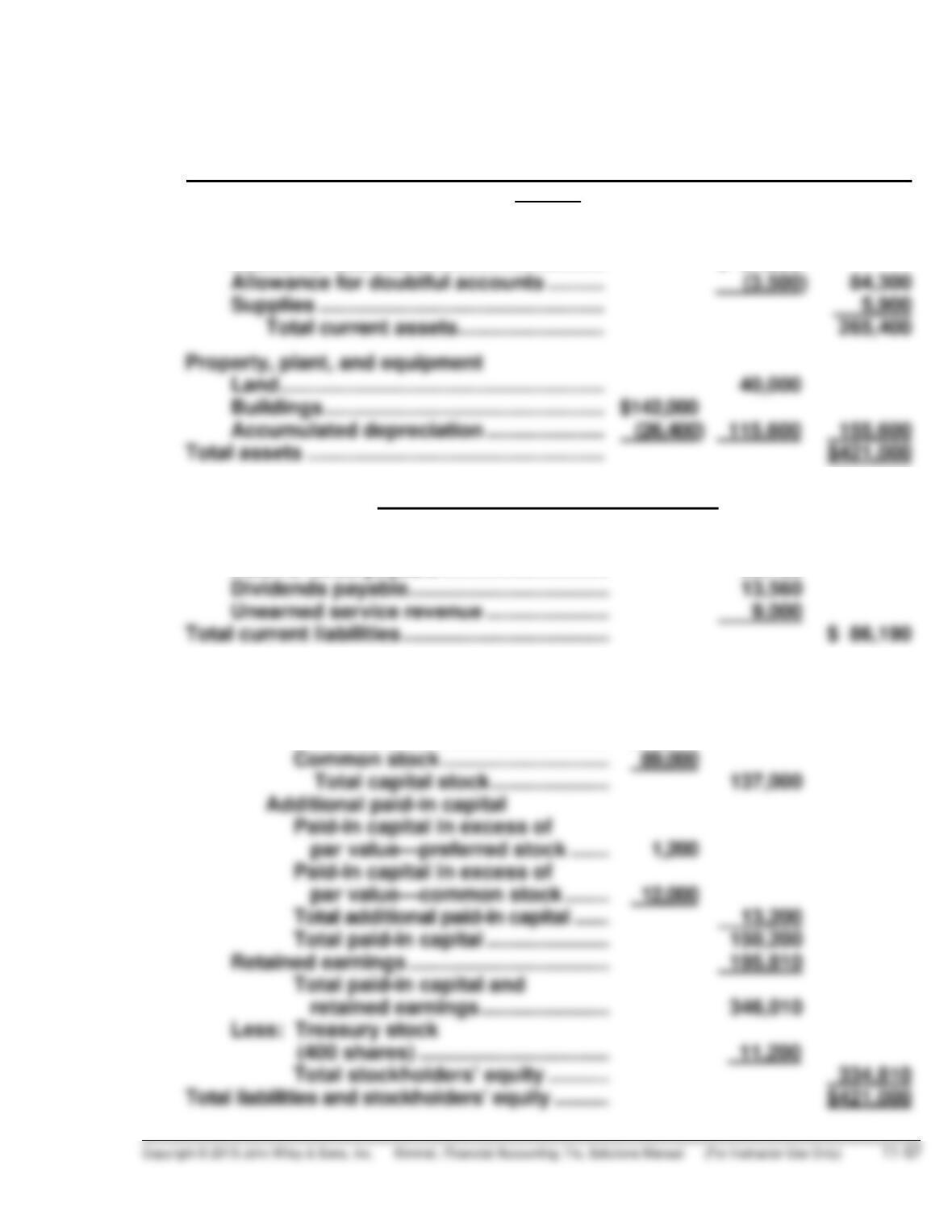

KLINGER CORPORATION

Balance Sheet

At December 31, 2014

A

ssets

Current assets

Cash ………………………………………………… $175,200

Accounts receivable …………………………. $ 87,800

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ……………………………..

.

$ 28,500

Income taxes payable………………………..

.

35,130

.

Stockholders’ equity

Paid-in capital

Capital stock

Preferred stock………………………..

.

$48,000

.

.

BYP 11-1 FINANCIAL REPORTING PROBLEM

(a) The common stock has a par value of $0.69 4/9 per share.

(d) $18,360

Payout ratio = = 41.8%

$43,938