1. and 2.

Jan. 1 Bal. 3,100,000

Apr. 13 1,000,000

July 16 123,000

Common Stock

11-32

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4B (Continued)

2.

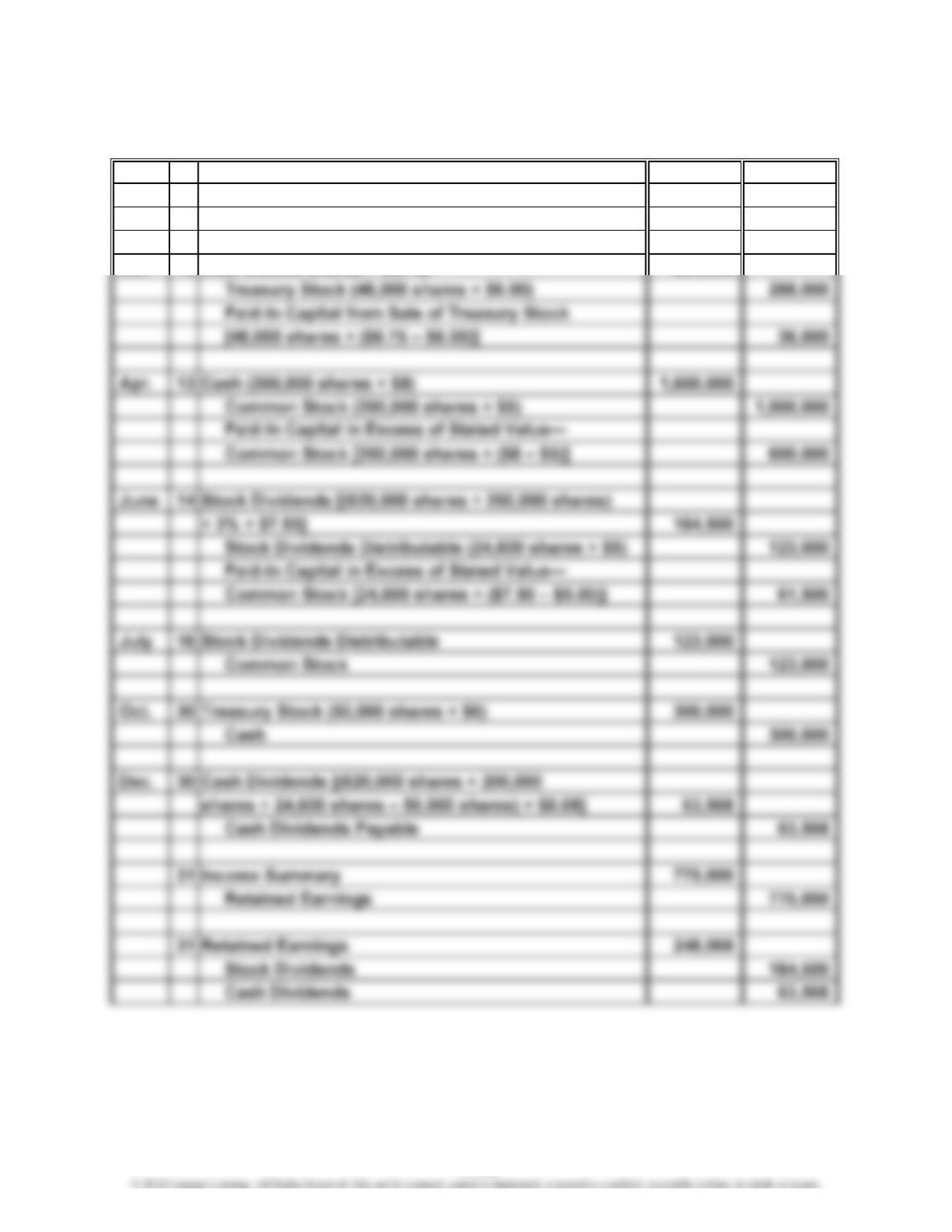

Jan. 15 Cash Dividends Payable [(620,000 shares – 48,000

shares) × $0.06] 34,320

Cash 34,320

Mar. 15 Cash (48,000 shares × $6.75) 324,000

11-33

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4B (Concluded)

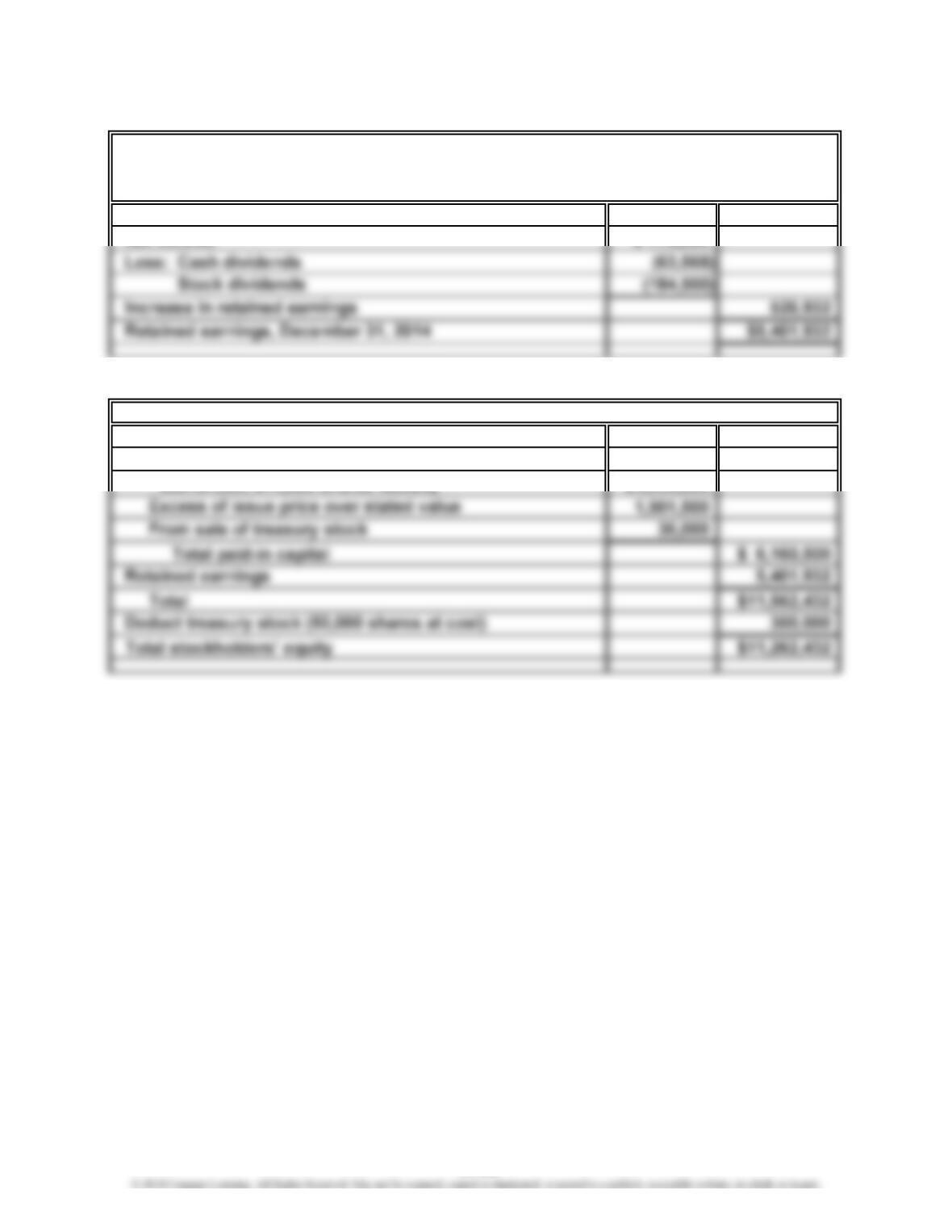

Retained earnings, January 1, 2014 $4,875,000

Net income $ 775,000

4.

Paid-in capital:

Common stock, $5 stated value (900,000 shares

authorized, 844,600 shares issued) $4,223,000

Stockholders’ Equity

NAV-GO ENTERPRISES INC.

Retained Earnings Statement

For the Year Ended December 31, 2014

11-34

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–5B

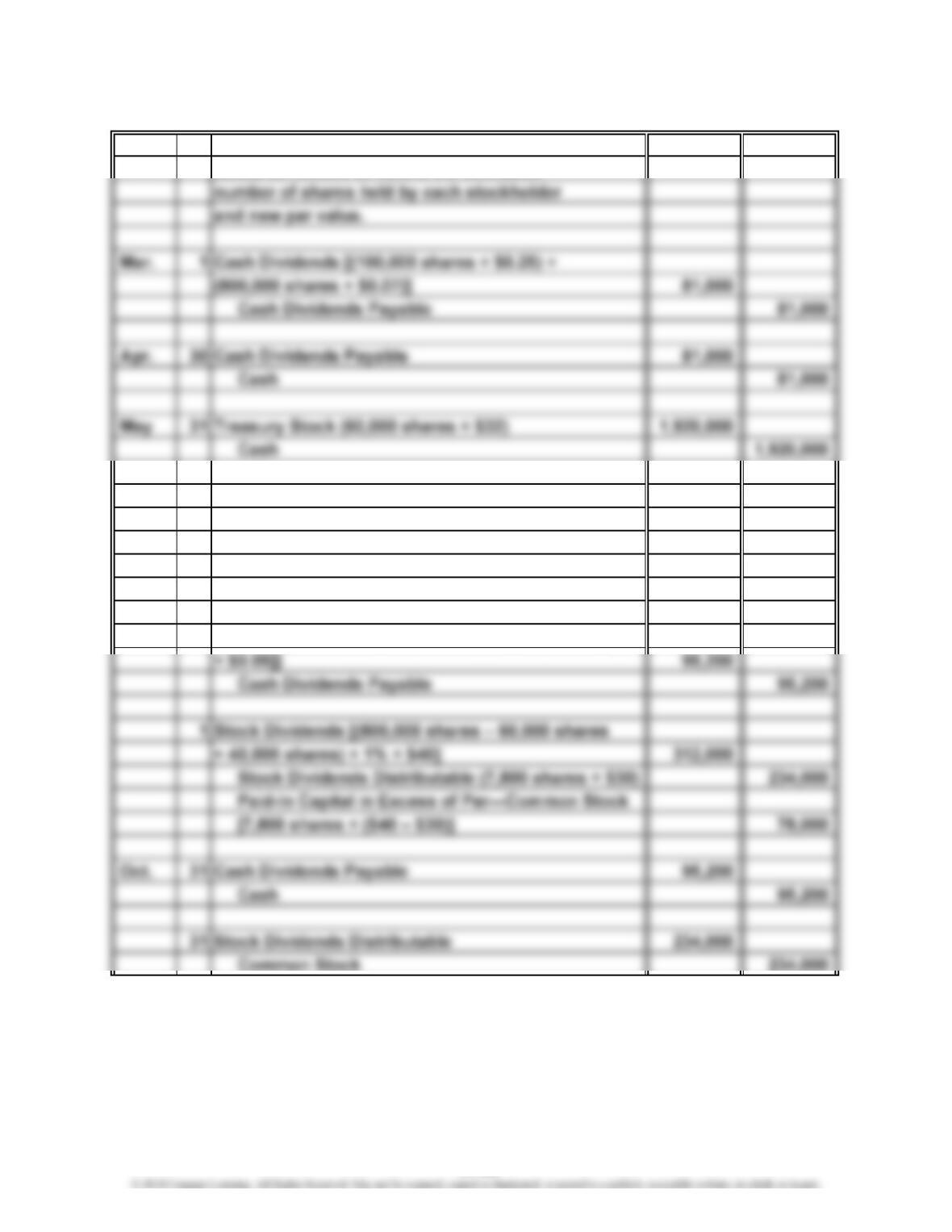

Jan. 15 No entry required. The stockholders’ ledger

would be revised to record the increased

Aug. 17 Cash (40,000 shares × $38) 1,520,000

Treasury Stock (40,000 shares × $32) 1,280,000

Paid-In Capital from Sale of Treasury

Stock [40,000 shares × ($38 – $32)] 240,000

Sept. 1 Cash Dividends {(100,000 shares × $0.25) +

[(800,000 shares – 60,000 shares+ 40,000 shares)

11-35

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–1

At the time of this decision, the WorldCom board had come under intense scrutiny.

This was the largest loan by a company to its CEO in history. The SEC began an

investigation into this loan, and Bernie Ebbers was eventually terminated as the

Some press comments:

1. When he borrowed money personally, he used his WorldCom stock as

collateral. As these loans came due, he was unwilling to sell at “depressed

2. It was astonishing to read the other day that the board of directors of the

United States’ second-largest telecommunications company claims to have

had its shareholders’ interests in mind when it agreed to grant more than $430

million in low-interest loans to the company’s CEO, mainly to meet margin

calls on his stock.

CASES & PROJECTS

11-36

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–1 (Concluded)

best one by far—at least from the point of view of the shareholders—was to

CP 11–2

Lou and Shirley are behaving in a professional manner as long as full and

CP 11–3

1. This case involves a transaction in which a security has been issued that has

characteristics of both stock and debt. The primary argument for classifying

the issuance of the common stock as debt is that the investors have a legal

right to an amount equal to the purchase price (face value) of the security.

2. In practice, the $25 million stock issuance would probably be classified as

common stock. However, full disclosure should be made of the 5% of net

sales and $120 per share payment obligations in the notes to the financial

11-37

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–4

a. 500 shares × ($0.80 ÷ 4) = $100

CP 11–5

1. Before a cash dividend is declared, there must be sufficient retained earnings

and cash. On December 31, 2014, the retained earnings balance of $4,630,000

is available for use in declaring a dividend. This balance is sufficient for the

Other factors that should be considered include the company’s working capital

(current assets – current liabilities) position and the loan provision pertaining

to the current ratio, resources needed for plant expansion or replacement of

facilities, future business prospects of the company, and forecasts for the

2. Given the cash and working capital position of Motion Designs Inc. on

11-38

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–5 (Concluded)

a. From the point of view of a stockholder, the declaration of a stock

dividend would continue the dividend declaration trend of Motion Designs

Inc. In addition, although the amount of the stockholders’ equity and

CP 11–6

Note to Instructors: The purpose of this activity is to familiarize students with

sources of information about corporations and how that information is useful in

evaluating the corporation’s activities.

CP 11–6 (Continued)

7. Convertible preferred stock, $0.001 par value, 100,000 shares authorized; no

shares issued and outstanding.

Class A and Class B common stock and additional paid-in capital, $0.001 par value

per share: 9,000,000 shares authorized; 321,301 (Class A 250,413, Class B 70,888)

11-40

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–6 (Concluded)

10. Google Inc. does not pay dividends. In its SEC 10-K filing for the year ending

December 31, 2011, Google states:

“We have never declared or paid any cash dividend on our common stock. We

11-41