CHAPTER 11

Standard Costs and Balanced Scorecard

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe standard costs.

1, 2, 3, 4, 5,

6, 7, 8, 9

1, 2, 3

1

1, 2, 3, 4, 17

2. Determine direct materials

variances.

10

4

2

5, 6, 7, 8, 9,

13, 14, 21

1A, 2A, 3A,

4A, 5A, 6A

3. Determine direct labor and

total manufacturing overhead

variances.

11, 12

5, 6

3

4, 6, 7, 8, 9,

10, 11, 12,

13, 21

1A, 2A, 3A,

4A, 5A, 6A

4. Prepare variance reports and

balanced scorecards.

13, 14, 15,

16, 17, 18

7

4

10, 14, 15,

16, 17, 18,

19

2A, 3A, 5A,

6A

*5. Identify the features of a

standard cost accounting

system.

19

8, 9

20, 21, 22

6A

*6. Compute overhead

controllable and volume

variance.

20, 21, 22,

23

10, 11

23, 24, 25

7A, 8A, 9A,

10A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Compute variances.

Simple

20–30

2A

Compute variances, and prepare income statement.

Simple

30–40

3A

Compute and identify significant variances.

Moderate

20–30

4A

Answer questions about variances.

Complex

30–0

5A

Compute variances, prepare an income statement, and

explain unfavorable variances.

Moderate

30–40

*6A

Journalize and post standard cost entries, and prepare

income statement.

Moderate

40–50

*7A

Compute overhead controllable and volume variances.

Simple

10–15

*8A

Compute overhead controllable and volume variances.

Simple

10–15

*9A

Compute overhead controllable and volume variances.

Moderate

10–15

*10A

Compute overhead controllable and volume variances.

Moderate

10–15

BYP11-9

Q11-5 E11-17

DI11-1 E11–17

ANSWERS TO QUESTIONS

1. (a) This is incorrect. Standard costs are predetermined unit costs.

(b) Agree. Examples of governmental regulations that establish standards for a business are

2. (a) Standards and budgets are similar in that both are predetermined costs and both contribute

significantly to management planning and control. The two terms differ in that a standard is

a unit amount and a budget is a total amount.

(b) There are important accounting differences between budgets and standards. Except in the

application of manufacturing overhead to jobs and processes, budget data are not journalized

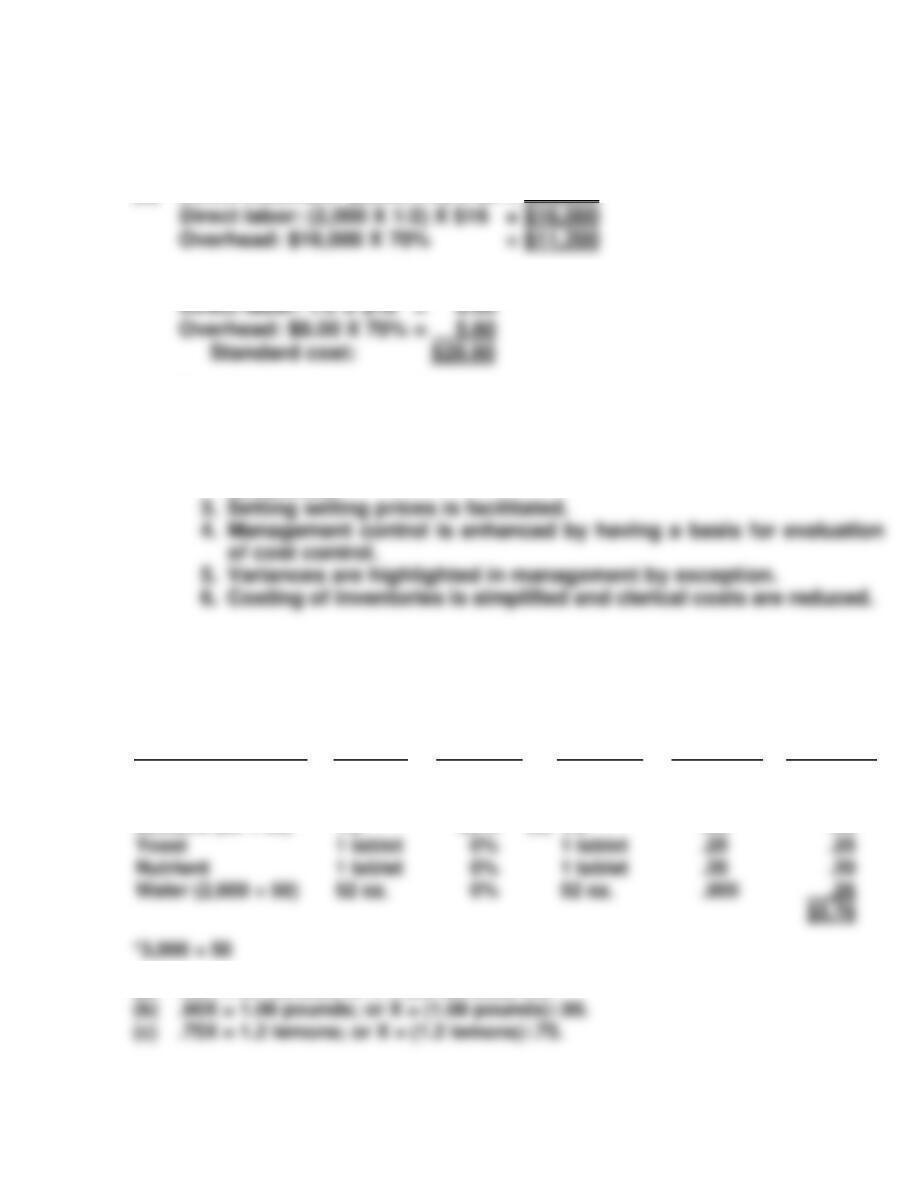

3. In addition to facilitating management planning, standard costs offer the following advantages to

an organization:

(1) They promote greater economy by making employees more “cost–conscious.”

(2) They may be useful in setting selling prices.

(3) They contribute to management control by providing a basis for evaluating cost control.

(4) They are useful in highlighting variances in “management by exception.”

(5) They simplify the costing of inventories and reduce clerical costs.

4. The management accountant provides input to the setting of standards through the accumulation

of historical cost data and knowledge of the behavior of costs in response to changes in activity

levels. Management has the responsibility for setting the standards.

5. Ideal standards represent optimum levels of performance under perfect operating conditions. Normal

standards represent efficient levels of performance that are attainable under expected operating

conditions.

6. (a) The direct materials price standard should be based on the purchasing department’s best

estimate of the cost of raw materials and an amount for related costs such as receiving,

7. Agree. The direct labor quantity standard should include allowances for rest periods, cleanup,

machine setup, and machine downtime.

8. With standard costs, the predetermined overhead rate is determined by dividing budgeted overhead

costs by an expected standard activity index.

Questions Chapter 11 (Continued)

10. (a) (1) actual price. (2) standard price.

(b) (3) actual quantity. (4) standard price.

(c) (5) standard price. (6) standard quantity.

11. (1) – (3) = total labor variance; (1) – (2) = labor price variance; and (2) – (3) = labor quantity

14. The purchasing department would be responsible for an unfavorable materials price variance

when it paid more than the standard price for the materials. The purchasing department would

also be responsible for an unfavorable materials quantity variance if it purchased materials of

inferior quality which caused an excess use of materials.

15. The four perspectives of the balanced scorecard are: financial, customer, internal process, and

learning and growth. The financial perspective employs financial measures of performance used

by most firms. The customer perspective evaluates the company from the viewpoint of those

16. Kerry James is not correct. The balanced scorecard does not replace financial measures, it

instead integrates both financial and nonfinancial measures. In fact, financial measures are very

critical to the balanced scorecard, since they represent the final “destination” of all the company’s

efforts.

17. The possibilities for nonfinancial measures are limitless. Some that were mentioned in the chapter

were: capacity utilization of plants, average age of key assets, impact of strikes, brand-loyalty statistics,

market profile of customer-end products, number of new products, employee stock ownership

18. (a) Variances are reported in income statements for management below gross profit which is

reported at standard costs. Each variance is identified and the total variance is shown.

(b) Standard costs may be used in costing inventories when there is no significant difference

between actual costs and standard costs. When there are significant differences, actual costs

must be reported.

Questions Chapter 11 (Continued)

*19. (a) A standard cost accounting system is a double-entry system of accounting in which

standard costs are used in making entries and standard cost variances are formally

*20. Overhead controllable variance = actual overhead costs ($248,000) – overhead budgeted. Overhead

budgeted is based on standard hours allowed as follows: variable costs (27,000 X $5 = $135,000) +

fixed costs (28,000 X $4 = $112,000) = total overhead budgeted ($247,000). Thus, the controllable

variance is $1,000 unfavorable.

*21. The purpose of computing the overhead volume variance is to determine whether plant facilities were

*22. Fixed costs remain the same at every level of activity within the relevant range. Since the prede-

termined overhead rate is based on normal capacity, it follows that if standard hours allowed are less

than standard hours at normal capacity, fixed overhead costs will be underapplied. The reverse is true

when production exceeds normal capacity.

*23. John should include the following points about overhead variances:

(1) Standard hours allowed are used in each of the variances.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 11-1

(a) Standards are stated as a per unit amount. Thus, the standards are

materials $2.80 ($1,400,000 ÷ 500,000) and labor $3.40 ($1,700,000 ÷

BRIEF EXERCISE 11-2

(a) Standard direct materials price per gallon = $2.60 ($2.30 + $.20 + $.10).

(b) Standard direct materials quantity per gallon = 4 pounds (3.6 + .4).

(c) Standard materials cost per gallon = $10.40 ($2.60 X 4).

BRIEF EXERCISE 11-3

(a) Standard direct labor rate per hour = $16.00 ($14.00 + $.80 + $1.20).

BRIEF EXERCISE 11-4

Total materials variance = $1,192 U (3,200 X $5.06*) – (3,000** X $5.00).

Materials price variance = $192 U (3,200 X $5.06) – (3,200 X $5.00).

BRIEF EXERCISE 11-5

Total labor variance = $1,220 U (2,150 X $10.80) – (2,000* X $11.00).

BRIEF EXERCISE 11-6

The formula is:

Actual

Overhead

–

Overhead

Applied

=

Total Overhead Variance

BRIEF EXERCISE 11-7

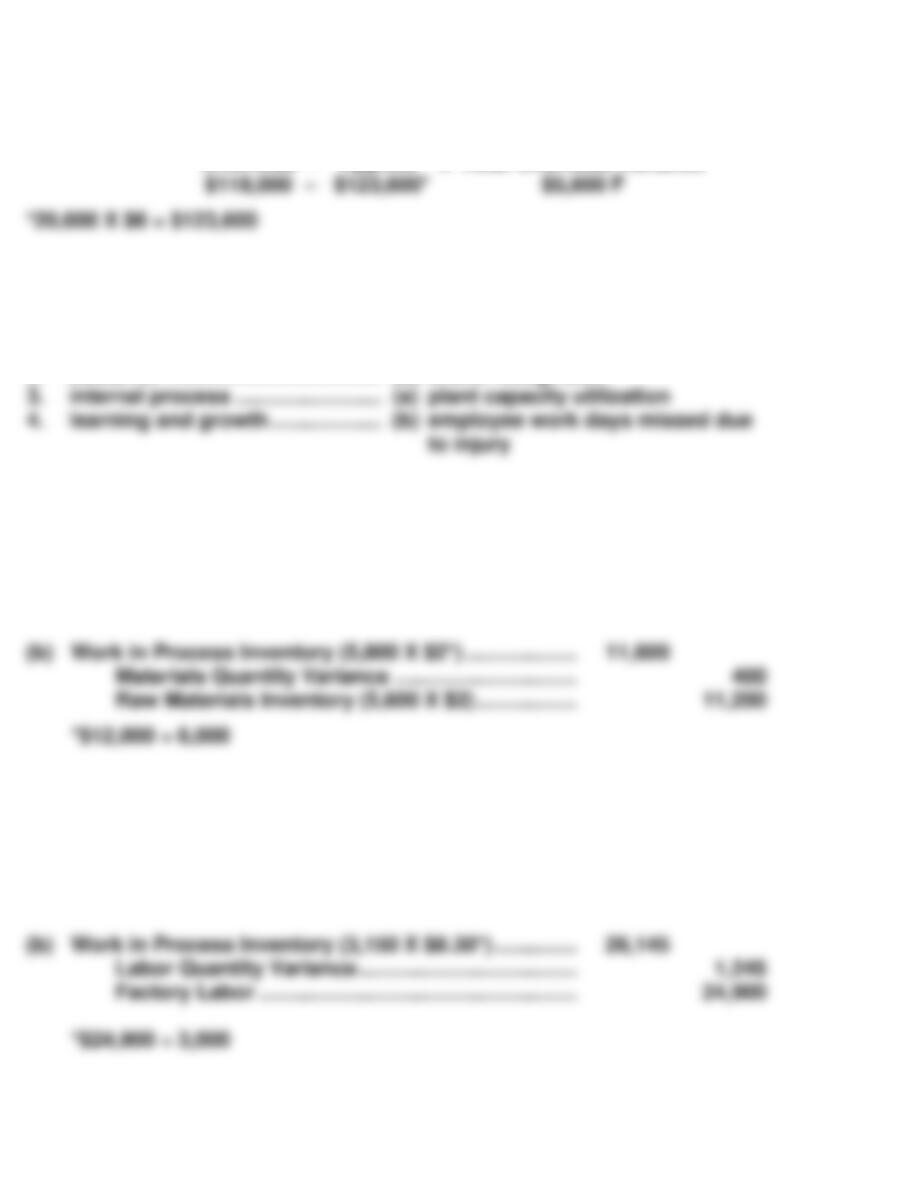

internal process …………………….

plant capacity utilization

1.

2.

financial ………………………………..

customer ……………………………….

(c)

(d)

return on assets

brand recognition

*BRIEF EXERCISE 11-8

(a) Raw Materials Inventory ……………………………………… 12,000

Materials Price Variance ………………………………. 500

Accounts Payable ……………………………………….. 11,500

*BRIEF EXERCISE 11-9

(a) Factory Labor …………………………………………………….. 24,900

Labor Price Variance …………………………..……….. 900

Factory Wages Payable ……………………………….. 24,000

*BRIEF EXERCISE 11-10

The formula is:

Actual Overhead

$118,000

–

–

Overhead

Budgeted

*$132,400*

=

Overhead

Controllable Variance

$14,400 F

*BRIEF EXERCISE 11-11

The formula is:

Fixed

Overhead

Rate

X

(Normal Capacity Hours – Standard Hours Allowed)

=

Overhead

Volume

Variance

(25,000 – 20,600)

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 11-1

Manufacturing Cost

Element

Standard Quantity

X

Standard Price

=

Standard Cost

Direct materials

2 pounds

$ 5.00

$10.00

Direct labor

Manufacturing overhead

Total

DO IT! 11-2

The variances are:

Total materials variance = (29,000 X $6.30) – (32,000* X $6.00) = $9,300 favorable

DO IT! 11-3

The variances are:

Total labor variance = (4,000 X $14.30) – (3,800* X $14.00) = $4,000 unfavorable

Labor price variance = (4,000 X $14.30) – (4,000 X $14.00) = $1,200 unfavorable

DO IT! 11-4

Sales revenue $92,100

Cost of goods sold (at standard) 51,600

Standard gross profit 40,500

Variances

Materials price $350 U

Materials quantity 1,700 F

SOLUTIONS TO EXERCISES

EXERCISE 11-1

(a) Direct materials: (2,000 X 3) X $5 = $30,000

(b) Direct materials: 3 X $5 = $15.00

(c) The advantages of standard costs which are carefully established and

prudently used are:

1. Management planning is facilitated.

2. Greater economy is promoted by making employees more cost–

conscious.

EXERCISE 11-2

Ingredient

Amount

Per

Gallon

Standard

Waste

Standard

Usage

Standard

Price

Standard

Cost Per

Gallon

Water (2,600 ÷ 50)

Grape concentrate

Sugar (54 ÷ 50)

Lemons (60 ÷ 50)

60* oz.

1.08 lb.

1.2

4%

10%

25%

(a)

(b)

(c)

62.5 oz.

1.20 lb.

1.6

$.06

.30

.60

$3.75

.36

.96

(a) .96X = 60 ounces; or X = (60 ounces)/.96.

EXERCISE 11-3

Direct materials

Cost per pound [($5 – (2% X $5)) + $0.25] $5.15

Pounds per unit (4.5 + 0.5) X 5 $25.75

Direct labor

EXERCISE 11-4

(a)

Actual service time

Setup and downtime

1.0 hours

0.2 hours

(b)

Hourly wage rate

Payroll taxes ($12 X 10%)

$12.00

1.20

(d)

Direct labor quantity variance

=

(1.60 hours X $16.20) – (1.50 hours X $16.20)

EXERCISE 11-5

(a) Total materials variance:

( AQ X AP )

(29,000 X $4.70)

–

( SQ X SP )

(28,200* X $5.00)

$4,700 F

Materials quantity variance:

(29,000 X $5.00)

$4,000 U

( AQ X SP )

–

( SQ X SP )

(b) Total materials variance:

(28,000 X $5.15)

(28,200 X $5.00)

$3,200 U

( AQ X AP )

–

( SQ X SP )

Materials price variance:

(28,000 X $5.00)

–

( SQ X SP )

( AQ X AP )

(28,000 X $5.15)

–

( AQ X SP )

(28,000 X $5.00)

$4,200 U

(29,000 X $4.70)

( AQ X SP )

(29,000 X $5.00)

EXERCISE 11-6

(a) Total labor variance:

( AH X AR )

(40,600 X $12.15)

–

( SH X SR )

(40,000* X $12.00)

(b) Labor price variance:

(40,600 X $12.15)

–

(40,600 X $12.00)

=

$6,090 U

( AH X AR )

–

( AH X SR )

Labor quantity variance:

( AH X SR )

(40,600 X $12.00)

$487,200

–

–

( SH X SR )

(40,000 X $12.00)

$480,000

=

$7,200 U

(c) Labor price variance:

$493,290

–

$497,350

=

( AH X SR )

(40,600 X $12.25)

–

–

( SH X SR )

=

$4,900 F

( AH X AR )

–

( AH X SR )

EXERCISE 11-7

Total materials variance:

( AQ X AP )

(1,900 X $2.65*)

$5,035

–

–

( SQ X SP )

(1,840** X $2.50)

$4,600

=

$435 U

Materials price variance:

–

=

( AQ X AP )

–

( AQ X SP )

$493,290

–

$480,000

=

EXERCISE 11-7 (Continued)

Materials quantity variance:

( AQ X SP )

–

( SQ X SP )

Total labor variance:

( AH X AR )

(700 X $11.60*)

$8,120

–

–

( SH X SR )

(690** X $12.00)

$8,280

=

$160 F

–

( AH X SR )

$4,600

=

$150 U

EXERCISE 11-7 (Continued)

(Not Required)

Materials Variance Matrix

(1)

(2)

(3)

Actual Quantity

X Actual Price

Actual Quantity

X Standard Price

Standard Quantity

X Standard Price

1,900 X $2.65 = $5,035

1,900 X $2.50 = $4,750

1,840 X $2.50 = $4,600

Labor Variance Matrix

(1)

(2)

(3)

Actual Hours

X Actual Rate

Actual Hours

X Standard Rate

Standard Hours

X Standard Rate

700 X $11.60 = $8,120

700 X $12.00 = $8,400

690 X $12.00 = $8,280

EXERCISE 11-8

(a) Total materials variance:

( AQ X AP )

(1,220 X $128)

$156,160

–

–

( SQ X SP )

(1,200 X $130)

$156,000

=

$160 U

Materials price variance:

( AQ X AP )

(1,220 X $128)

–

–

( AQ X SP )

(1,220 X $130)

$158,600

=

$2,440 F

Materials quantity variance:

( AQ X SP )

(1,220 X $130)

$158,600

–

–

( SQ X SP )

(1,200 X $130)

$156,000

=

$2,600 U

Total labor variance:

–

=

$200 U

–

=

$2,075 U

( AH X AR )

–

( SH X SR )

Labor quantity variance:

( AH X SR )

(4,150 X $12.50)

$51,875

–

–

( SH X SR )

(4,300 X $12.50)

$53,750

=

$1,875 F

(b) The unfavorable materials quantity variance may be caused by the

carelessness or inefficiency of production workers. Alternatively, the

excess quantities may be caused by inferior quality materials acquired

by the purchasing department.

EXERCISE 11-9

(a) Number of units = Total standard cost ÷ Standard cost per unit

Number of units = $410,000 ÷ $20.00 (5 lb X $4 per lb) = 20,500

(b) AQ = [(SQ X SP)

±

Quantity variance] ÷ SP

AQ = ($410,000 + $9,000) ÷ $4.00 per lb = 104,750 pounds

EXERCISE 11-10

TOBY TOOL & DIE COMPANY

Direct Labor Variance Report

For the Month Ended March 31, 2017

Job

No.

Actual

Hours

Standard

Hours

Quantity

Variance

(a)

Actual

Rate

(1)

Standard

Rate

(2)

Price

Variance

(b)

Explanation

$18.00

worker

A257

A258

221

450

225

430

$ 80.00

400.00

F

U

$20.00

$21.00

$20.00

$20.00

$ 0

450.00

U

Repeat job

Rush job

±

±

±

EXERCISE 11-11

Total overhead variance:

Actual Overhead

–

Overhead Applied

EXERCISE 11-12

(a)

Overhead Budget

(at normal capacity)

÷

Direct Labor Hours

(at normal capacity)

=

Predetermined

Overhead Rate

Variable

$250,000

100,000

$2.50

Fixed

600,000

100,000

$6.00

(b)

X

=

(c)

=

$856,000

=

EXERCISE 11-13

(a)

(AQ X AP)

( $10,200)

–

–

( SQ X SP)

(2,100* X $5)

=

=

Total Materials Variance

$300 F

(AQ X AP)

( $10,200)

–

–

( AQ X SP)

=

=

Materials Price Variance

(2,400 X $5)

–

–

( SQ X SP)

(2,100* X $5)

=

=

Materials Quantity Variance

(b) One possible cause of an unfavorable materials quantity variance is

the purchase of substandard materials. Such materials would normally

be purchased at a lower price than normal, which means there would

–

=

$3,000 U

EXERCISE 11-14

(a) PICARD LANDSCAPING

Variance Report – Purchasing Department

For the Current Month

Project

Actual

Pounds

Purchased

(1)

Actual

Price

Per

Pound

(2)

Standard

Price

Price

Variance

(a)

Explanation

Remington

500

$2.40

$2.50

$50 F

Purchased poor-quality seeds

(b) PICARD LANDSCAPING

Variance Report – Production Department

For the Current Month

Project

Actual

Pounds

Standard

Pounds

Standard

Price Per

Pound

Quantity

Variance

(b)

Explanation

Remington

Chang

500

400

460

410

$2.50

2.50

$100 U

25 F

Purchased poor-quality seeds

Purchased higher-quality seeds

EXERCISE 11-15

URBAN CORPORATION

Variance Report – Purchasing Department

For Week Ended January 9, 2017

Type of

Materials

Quantity

Purchased

Actual

Price

Standard

Price

Price

Variance

Explanation

Rogue 11

27,500 lbs.

$5.20

$5.00

$5,500 U

Price increase

EXERCISE 11-16

FISK COMPANY

Income Statement

For the Month Ended January 31, 2017

Sales revenue (8,000 X $8) ……………………………………… $64,000

Cost of goods sold (8,000 X $5) ……………………………… 40,000

Gross profit (at standard) ………………………………………. 24,000

Variances

Materials price ……………………………………………….. $1,200 U

Materials quantity …………………………………………… 800 F

EXERCISE 11-17

1. Balanced scorecard—(c) An approach that incorporates financial and

nonfinancial measures in an integrated system that links performance

measurement and a company’s strategic goals.

2. Variance—(a) The difference between total actual costs and total stan-

dard costs.

3. Learning and growth perspective—(d) A viewpoint employed in the

balanced scorecard to evaluate how well a company develops and retains

its employees.

EXERCISE 11-18

1. Customer perspective.

2. Learning and growth perspective.

3. Financial perspective.

4. Customer perspective.

5. Learning and growth perspective.

6. Internal process perspective.

EXERCISE 11-19

1.

Learning and growth perspective.

2.

Financial perspective.

3.

Customer perspective.

4.

Internal process perspective.

5.

Learning and growth perspective.

6.

Customer perspective.

*EXERCISE 11-20

1. Raw Materials Inventory (18,000 X $4.40) ……………. 79,200

Materials Price Variance (18,000 X $.10) ……………… 1,800

Accounts Payable (18,000 X $4.50) ………………. 81,000

2. Work in Process Inventory (17,500 X $4.40) ………… 77,000

Materials Quantity Variance (500 X $4.40) …………… 2,200

*EXERCISE 11-21

(a) $136,000 ($138,000 – $2,000).

(b) $139,000 ($136,000 + $3,000).

*EXERCISE 11-22

Raw Materials Inventory (1,900 X $2.50) ……………………… 4,750

Materials Price Variance (1,900 X $0.15) ……………………… 285

Accounts Payable (1,900 X $2.65) ………………………… 5,035

Work in Process Inventory (1,840* X $2.50) …………………. 4,600

*230 X 3

*EXERCISE 11-23

(a)

Item

Amount

Hours

Rate

Fixed overhead …………………………………

Variable overhead ……………………………..

$34,650

16,500

$2.10

(b) Total overhead variance:

Actual Overhead

–

Overhead Applied

Overhead controllable variance:

Actual Overhead

$55,500

–

–

Overhead Budgeted

$53,820

[(16,200 X $2.10) + $19,800]

=

$1,680 U

EXERCISE 11-23 (Continued)

*EXERCISE 11-24

(a)

1.

Total actual overhead cost

=

Overhead

Budgeted +

Overhead

Controllable

Variance

=

($18,000 + $12,600) + $1,200

=

$31,800

2.

Actual variable overhead cost

=

Actual Overhead – Fixed Overhead

=

$31,800 – $12,600

=

$19,200

(b)

Number of loans processed

=

Standard hours allowed ÷

Standard hours per application

=

2,000 ÷ 2

=

1,000 loans processed

3.

=

2,000 hours X $9 = $18,000

4.

=

2,000 hours X $6 = $12,000

=

EXERCISE 11-25

(a)

(Actual)

($19,500)

–

–

(Applied)

(1,800 X $10*)

=

=

Total Overhead Variance

$1,500 U

(Actual)

–

(Budgeted)

=

Overhead Controllable Variance

(b) The cause of an unfavorable controllable variance could be higher than

expected use of indirect materials, indirect labor, and factory supplies, or

increases in indirect manufacturing costs, such as fuel and maintenance

–

=

$1,900 U

=

SOLUTIONS TO PROBLEMS

PROBLEM 11-1A

(a) Total materials variance:

( AQ X AP )

(5,100 X $7.20)

$36,720

–

–

( SQ X SP )

(4,800 X $7.00)

$33,600

=

$3,120 U

Materials price variance:

( AQ X AP )

–

( AQ X SP )

Total labor variance:

( AH X AR )

(7,400 X $12.50)

$92,500

–

–

( SH X SR )

(7,680* X $12.00)

$92,160

=

$340 U

*4,800 X 1.6

Labor price variance:

( AH X AR )

$92,500

–

–

( AH X SR )

=

$92,160

(b) Total overhead variance:

Actual

Overhead

($59,700 + $21,000)

$80,700

–

–

Overhead

Applied

(7,680 X $10.00)

$76,800

=

$3,900 U

–

=

–

PROBLEM 11-2A

(a) 1. Total materials variance:

( AQ X AP )

(10,600 X $2.25)

$23,850

–

–

( SQ X SP )

(10,000 X $2.10)

$21,000

=

$2,850 U

Materials price variance:

( AQ X AP )

(10,600 X $2.25)

$23,850

–

–

( AQ X SP )

(10,600 X $2.10)

$22,260

=

$1,590 U

(b) Total overhead variance:

Actual

Overhead

$189,500

–

–

Overhead

Applied

$193,500

(45,000* X $4.30)

=

$4,000 F

*15,000 X 3

( AQ X SP )

(10,600 X $2.10)

–

–

( SQ X SP )

(10,000 X $2.10)

$21,000

=

$1,260 U

–

–

=

(14,400 X $8.40)

–

–

(14,400 X $8.00)

=

(14,400 X $8.00)

–

–

(15,000 X $8.00)

=

PROBLEM 11-2A (Continued)

(c) AYALA CORPORATION

Income Statement

For the Month Ended June 30, 2017

Sales revenue …………………………………………….. $400,000

Cost of goods sold (at standard) …………………. 334,500*

Gross profit (at standard) ……………………………. 65,500

Variances

Materials price …………………………………….. $ 1,590 U

Materials quantity ………………………………… 1,260 U

PROBLEM 11-3A

(a) 1. Total materials variance:

( AQ X AP )

(90,500 X $4.15)

$375,575

–

–

( SQ X SP )

(90,000* X $4.40)

$396,000

=

$20,425 F

*11,250 X 8

Materials price variance:

( AQ X AP )

–

( AQ X SP )

2. Total labor variance:

( AH X AR )

(14,250 X $14.10)

$200,925

–

–

( SH X SR )

(13,500* X $13.40)

$180,900

=

$20,025 U

*11,250 X 1.2

Labor price variance:

(14,250 X $13.40)

–

(13,500 X $13.40)

( AH X AR )

–

( AH X SR )

(b) Total overhead variance:

Actual

Overhead

–

Overhead

Applied

–

PROBLEM 11-3A (Continued)

(c) The materials price variance is more than 4% from standard. The actual

price for materials of $4.15 is $.25 below the standard price of $4.40 or

5.7% ($.25 ÷ $4.40). The same result can be obtained by dividing the

total price variance by the total standard price for the quantities purchased

($22,625 ÷ $398,200).

PROBLEM 11-4A

(a) $3,510 ÷ 117,000 = $.03; $.92 + $.03 = $.95 standard materials price per

(b) $4,750 ÷ $.95 = 5,000 pounds; 117,000 – 5,000 = 112,000 standard

quantity for 28,000 units or 4.0 pounds (112,000 ÷ 28,000) per unit. OR

$111,150 – $4,750 = $106,400; $106,400 ÷ $.95 = 112,000; 112,000 ÷

28,000 = 4.0 pounds per unit.

(c) Standard hours allowed are 44,800 (28,000 X 1.6).

(g) Direct materials 4.0 pounds X $.95 = $3.80; direct labor 1.6 X $12.00 =

$19.20; manufacturing overhead 1.6 X $7.20 = $11.52. $3.80 + $19.20 +

$11.52 = $34.52 standard cost per unit.

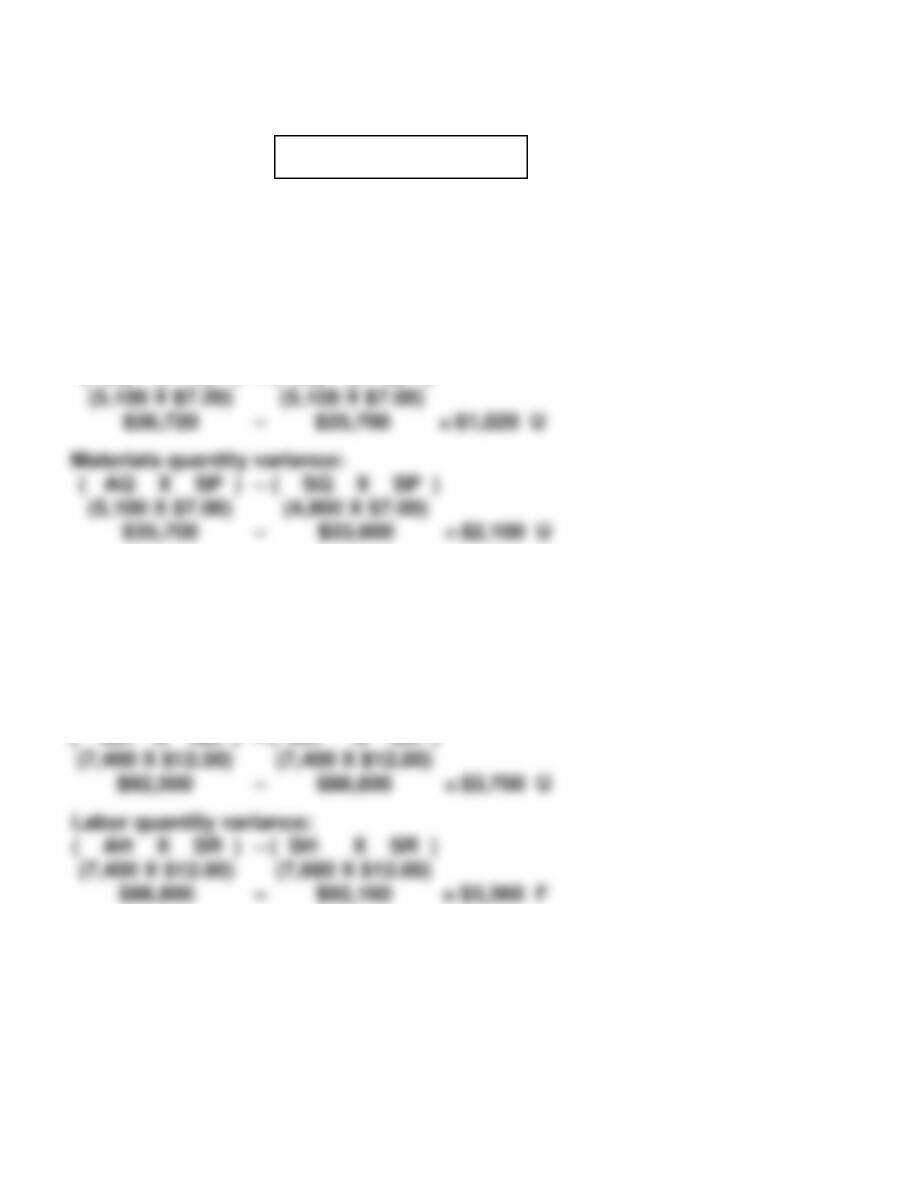

PROBLEM 11-5A

(a) Materials price variance:

( AQ X AP )

(3,050 X $1.40*)

$4,270

–

–

( AQ X SP )

(3,050 X $1.46)

$4,453

=

$183 F

*$4,270 ÷ 3,050

Materials quantity variance:

( AQ X SP )

(3,050 X $1.46)

–

( SQ X SP )

(2,950* X $1.46)

(b) Total Overhead variance:

Actual

Overhead

–

Overhead

Applied

–

=

$146 U

–

PROBLEM 11-5A (Continued)

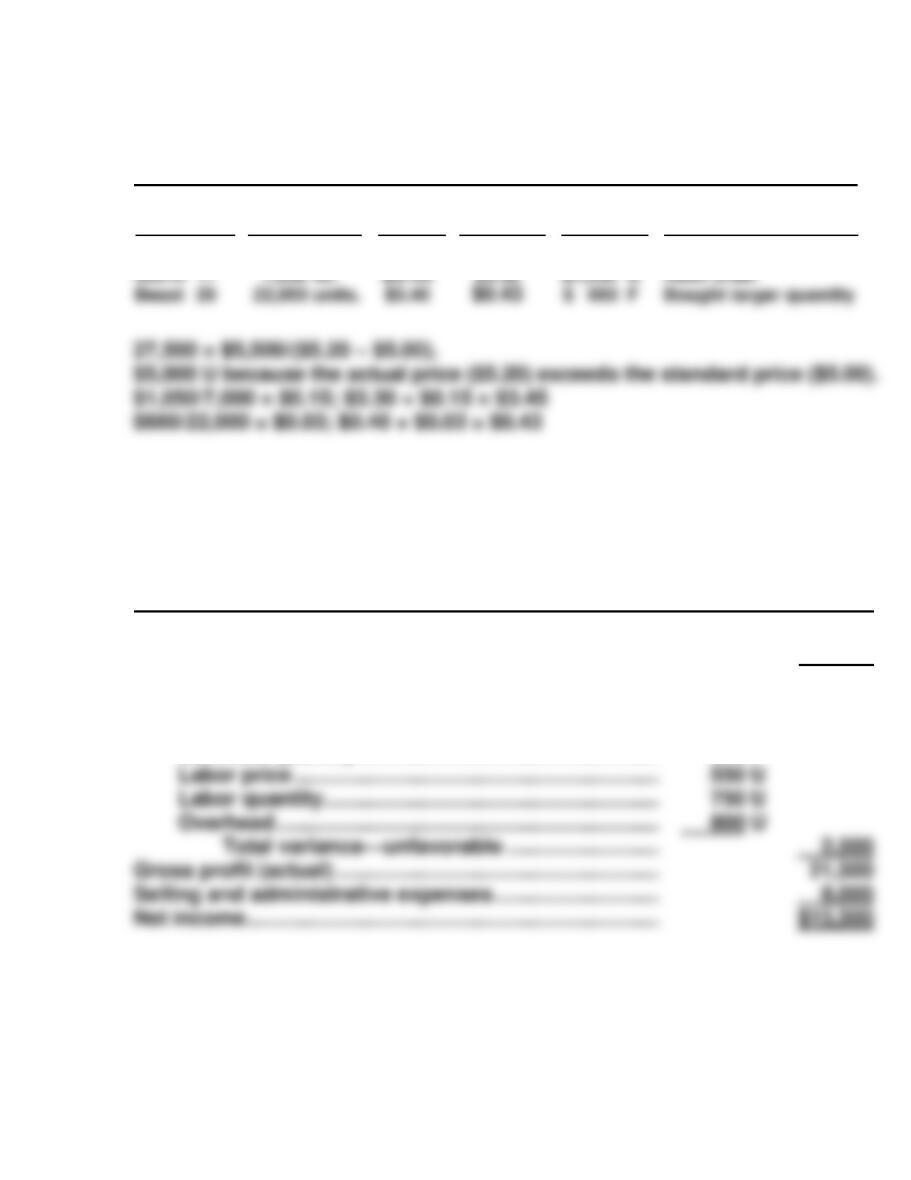

(c) HART LABS, INC.

Income Statement

For the Month Ended November 30, 2017

Service revenue ……………………………………………… $75,000

Cost of service provided (at standard)

(1,475 X $42.92) …………………………………………… 63,307

Gross profit (at standard) ………………………………… 11,693

Variances

(d) The unfavorable materials quantity variance could be caused by poor

quality materials or inexperienced workers or faulty test procedures.

*PROBLEM 11-6A

(a) 1. Raw Materials Inventory (6,200 X $1.00) ………… 6,200

2. Work in Process Inventory (5,700* X $1) ……….. 5,700

Materials Quantity Variance

3. Factory Labor (2,000 X $8) ……………………………. 16,000

Labor Price Variance

[2,000 X ($8.00 – $7.80)] ……………………… 400

Factory Wages Payable (2,000 X $7.80) ….. 15,600

4. Work in Process Inventory

(1,900 X $8.00) …………………………………………. 15,200

Labor Quantity Variance

[(2,000 – 1,900) X $8.00] ……………………………. 800

Factory Labor ………………………………………. 16,000

8. Accounts Receivable …………………………………… 65,000

Sales Revenue ……………………………………… 65,000

Cost of Goods Sold …………………………………….. 44,650

Finished Goods Inventory ……………………. 44,650

*PROBLEM 11-6A (Continued)

(b)

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory

(1) 6,200

(2) 6,200

(1) 310

(2) 5,700

(4) 15,200

(6) 23,750

(7) 44,650

(c) Overhead Variance ($25,000 – $23,750) …………… 1,250

Manufacturing Overhead …………………………. 1,250

(d) JORGENSEN CORPORATION

Income Statement

For the Month Ended January 31, 2017

Sales revenue ……………………………………………….. $65,000

Cost of goods sold (at standard)

(1,900 X $23.50) ………………………………………….. 44,650

Gross profit (at standard) ……………………………….. 20,350

(8) 44,650

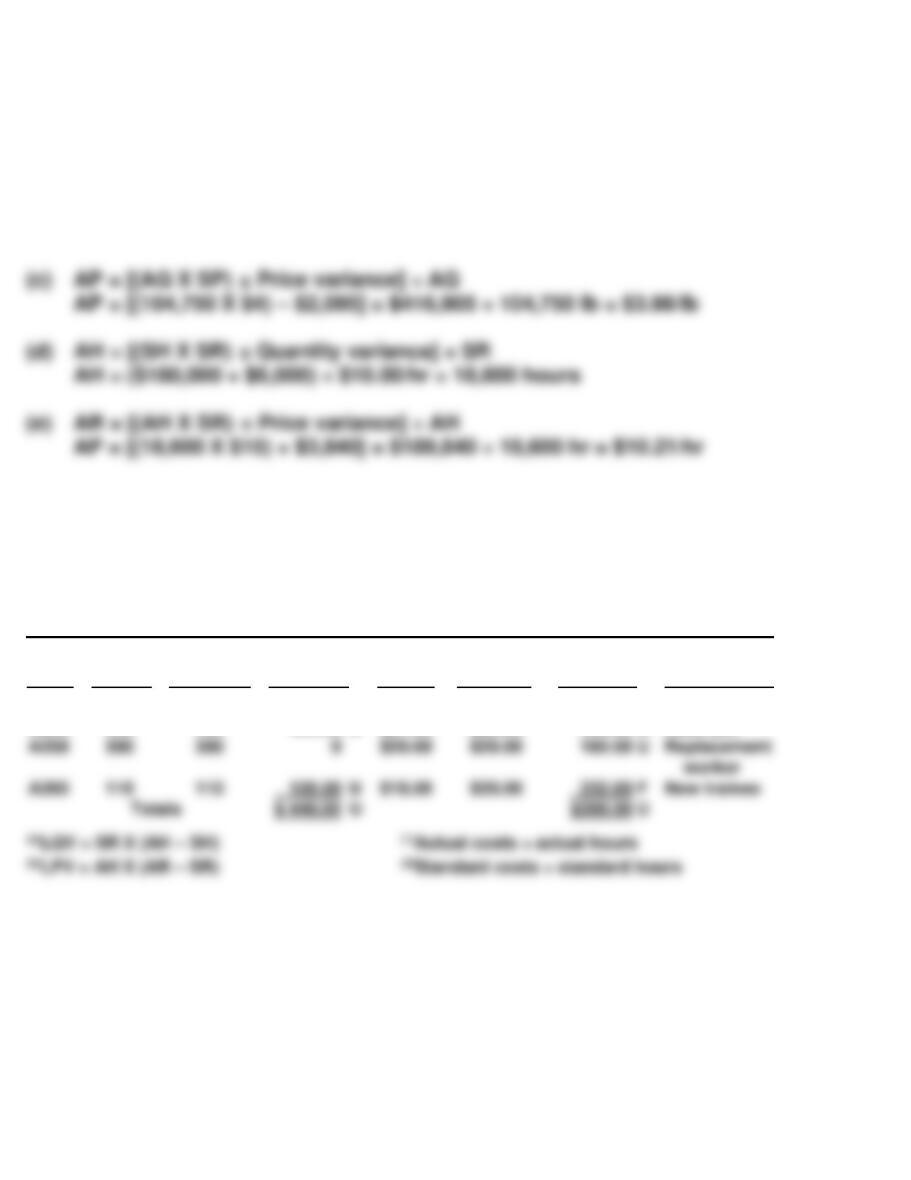

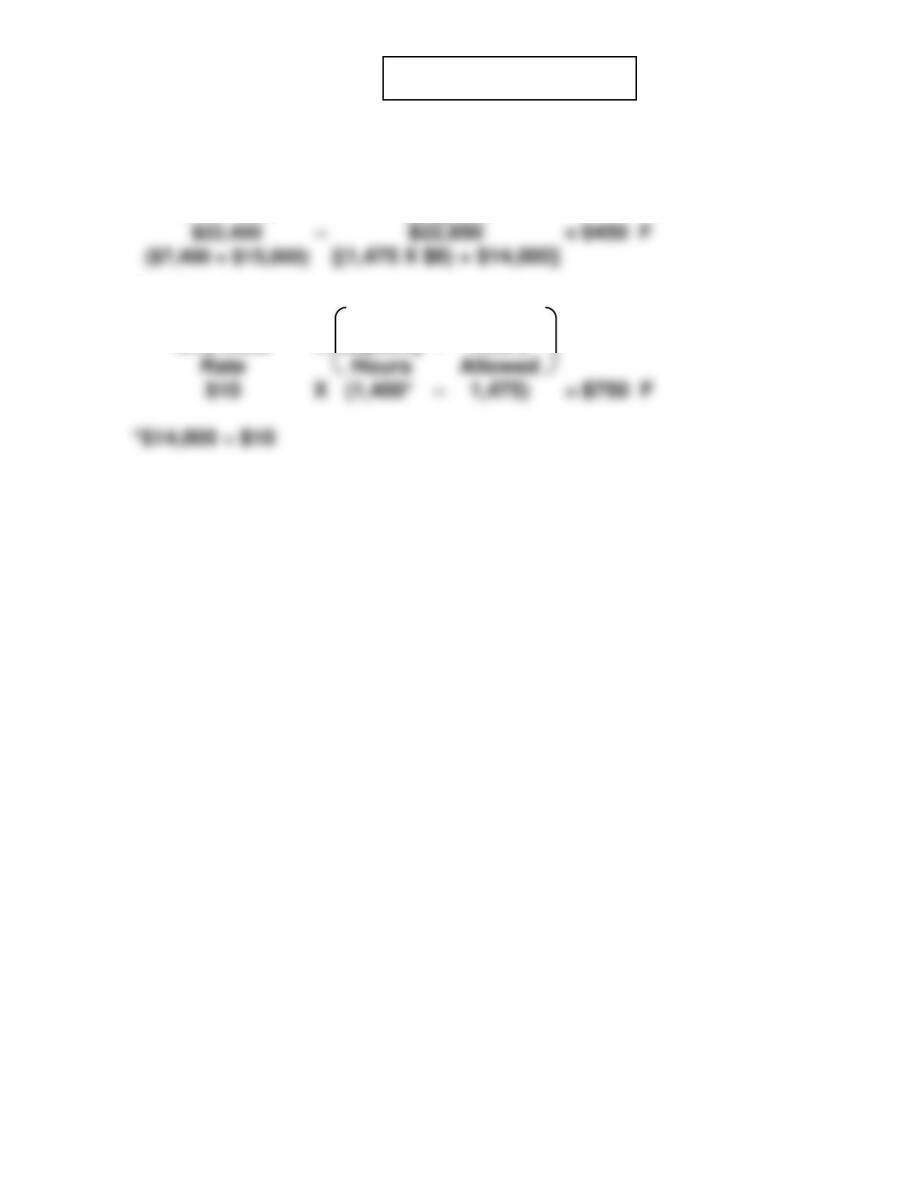

*PROBLEM 11-7A

Overhead controllable variance:

Actual

Overhead

Overhead volume variance:

Fixed

Normal

Standard

*PROBLEM 11-8A

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

Overhead volume variance:

Fixed

Normal

Standard

*PROBLEM 11-9A

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

Overhead volume variance:

Fixed

Overhead

X

Normal

Capacity

–

Standard

Hours

*PROBLEM 11-10A

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

Overhead volume variance:

Fixed

Overhead

X

Normal

Capacity

–

Standard

Hours

CD11 CURRENT DESIGNS

(a) Quantity variance for polyethylene powder Unfavorable

Price variance for polyethylene powder Unfavorable

Quantity variance for finishing kits NEI = Not enough information

(b) Quantity variance for polyethylene powder

$1,800

–

$1,620

=

$180 U

( AQ X SP )

–

( SQ X SP )

Price variance for polyethylene powder

( AQ X AP )

(1,200 X $1.70*)

$2,040

–

–

( AQ X SP )

(1,200 X $1.50)

$1,800

=

$240 U

( AQ X SP )

$3,400

–

–

( SQ X SP )

$3,400

=

*$2,040 ÷ 1,200

CD11 (Continued)

Quantity variance for type I workers

( AH X SR )

(38 X $15)

$570

–

–

( SH X SR )

(40* X $15)

$600

=

$30 F

*20 X 2

$570

–

–

( AH X SR )

$570

=

( AH X SR )

(65 X $12)

$780

–

–

( SH X SR )

(60* X $12)

$720

=

$60 U

–

$780

=

BYP 11-1 DECISION-MAKING ACROSS THE ORGANIZATION

(a) When setting a standard for computer/labor hours usage, Milton Profes–

sionals should consider the following factors:

1. A standard set conservatively high may discourage clients from

purchasing the model.

(b) Logical alternatives for the standard include:

1. 34 hours: The average number of hours used for one application

by all five financial institutions.

2. 45 hours: The conservatively high number experienced by one

financial institution.

(c) In light of earlier factors listed, the second and third choices for the

standard should be eliminated (i.e., 45 and 25 hours). The average

34 hours is probably the most representative. However, Milton Profes–

BYP 11-1 (Continued)

(d) Standard material cost for one model application:

BYP 11-2 MANAGERIAL ANALYSIS

(a) The overhead application rate is $144,000 divided by 5,000 hours, or

$28.80 per direct labor hour.

(b) The standard direct labor hours are used to apply overhead to production,

so the calculation is $28.80 X 4,500, or $129,600.

(c)

Actual Overhead

$150,000

–

Overhead Applied

$129,600

=

=

Total Overhead Variance

$20,400 U

The variances are:

(d) Both variances appear significant. The controllable variance is 9.3% of

budgeted overhead ($12,820 ÷ $137,180), and the volume variance is

5.8% of applied overhead ($7,580 ÷ $129,600).

(e) The controllable variance is caused by either spending more than ex–

pected on overhead items, or using more than expected of overhead

BYP 11-3 REAL-WORLD FOCUS

(a) Glassmaster is using standard costs because management states that

a factor that contributed to improved margins (profit) was a favorable

materials price variance.

(b) The materials price variance experienced should not lead to changes

BYP 11-4 REAL-WORLD FOCUS

(a) The objectives for each perspective are:

Financial: Increase profitability, lower costs, increase revenue

Customer: Flight is on-time, lowest prices, more customers

Internal: Improve turnaround time.

Learning: Ground crew alignment.

BYP 11-5 REAL-WORLD FOCUS

(a) The normal industry standard for plants to be considered operating at

100% capacity is two shifts working about 250 days a year.

(b) A government task force urged the company to try to operate at 120%

capacity by traditional standards.

(c) It is argued that assembly lines need too much scheduled maintenance

and restocking. This is normally done during the period that the

company is proposing to run a third shift. For example, the paint shop

BYP 11-6 COMMUNICATION ACTIVITY

To: Professor Standard

From: I. M. Smart

Subject: Setting Standard Costs

This memorandum covers two points as follows:

(a) The comparative advantages and disadvantages of ideal versus normal

standards.

Ideal standards represent optimum levels of performance under perfect

operating conditions. In contrast, normal standards represent efficient

levels of performance that are attainable under expected operating

conditions.

(b) Factors to be considered in setting standards for direct materials, direct

labor, and manufacturing overhead.

1. Direct materials. The direct materials price standard is the cost per

unit of direct materials that should be incurred. This standard should

be based on the purchasing department’s best estimate of the cost

of raw materials. The price standard should include allowances for

related costs such as receiving, storing and handling.

BYP 11-6 (Continued)

The direct materials quantity standard is the quantity of direct

materials that should be used per unit of finished goods. This

standard is a physical measure and it should include allowances

for unavoidable waste and normal spoilage.

BYP 11-7 ETHICS CASE

(a) Bill and his fellow painters in the painting department will benefit from

Bill’s slow action. The company and its customers are harmed. The

company will incur higher costs on the product and therefore will have

to set a higher selling price or suffer a smaller gross profit. Customers

will have to pay a greater price for the product or stockholders will

obtain less benefit from their investment.

BYP 11-8 ALL ABOUT YOU

(a) The panel made recommendations regarding a number of areas of

concern in higher education. For example, it suggested that new

approaches should be used to control costs, and it stated that the cost

of tuition should grow no faster than median family income. It made

recommendations to strengthen the Pell Grant program, which is the

core of the federal financial aid program. It also recommended that

public universities should use standardized tests to measure student

learning.

(b) As discussed in the chapter, standards provide a mechanism for evalu–

ating performance and, if used properly, can be used as a motivational

BYP 11-9 CONSIDERING YOUR COSTS AND BENEFITS

Discussion Guide: The practice of medicine holds an unusual place in

society. On the one hand, it provides a critical, life-sustaining service. We

expect and demand the highest-quality service. We measure its success in

terms of health improvement and lives saved. On the other hand, it is a

business, and like other businesses, it must operate profitably. Some

healthcare providers characterize this delicate balance as “The Business of

Caring.” How should we balance providing quality health-care and