CHAPTER 11

SOLUTIONS TO EXERCISES—SET B

EXERCISE 11-1B

(a) Direct materials: (2,000 X 2.5) X $5 = $25,000

Direct labor: (2,000 X 1/2) X $18 = $18,000

(b) Direct materials: 2.5 X $5 = $12.50

(c) The advantages of standard costs which are carefully established and

prudently used are:

1. Management planning is facilitated.

2. Greater economy is promoted by making employees more cost–

conscious.

EXERCISE 11-2B

Ingredient

Amount

Per

Gallon

Standard

Waste

Standard

Usage

Standard

Price

Standard

Cost Per

Gallon

Water (2,500 ÷ 50)

Grape concentrate

Sugar (54 ÷ 50)

Lemons (60 ÷ 50)

66* oz.

1.08 lb.

1.2

4%

10%

20%

(a)

(b)

(c)

68.75 oz.

1.2 lb.

1.5

$.08

.30

.66

$5.50

.36

.99

*3,300 ÷ 50

EXERCISE 11-3B

Direct materials

Cost per pound [$3 – (1% X $3) + $0.25] $3.22

Pounds per unit (4.5 + 0.5) X 5 $16.10

Direct labor

Cost per hour ($10 + $3) $ 13

Hours per unit (2 + .2) X 2.2 28.60

EXERCISE 11-4B

(a)

Actual service time

Setup and downtime

Cleanup and rest periods

Standard direct labor hours per oil change

0.90 hours

0.09 hours

0.27 hours

1.26 hours

(b)

(d)

Direct labor quantity variance

Hourly wage rate

Payroll taxes ($12 X 12%)

$12.00

1.44

EXERCISE 11-5B

(a) Total materials variance:

( AQ X AP )

(27,000 X $3.80)

$102,600

–

–

( SQ X SP )

(26,000* X $4.00)

$104,000

=

$1,400 F

(b) Total materials variance:

( AQ X AP )

(25,200 X $4.20)

$105,840

–

–

( SQ X SP )

(26,000 X $4.00)

$104,000

=

$1,840 U

Materials price variance:

–

=

(25,200 X $4.00)

–

–

( SQ X SP )

(26,000 X $4.00)

=

$3,200 F

( AQ X AP )

–

( AQ X SP )

( AQ X SP )

=

(27,000 X $4.00)

$108,000

–

–

( SQ X SP )

(26,000 X $4.00)

=

$4,000 U

EXERCISE 11-6B

(a) Total labor variance:

( AH X AR )

–

( SH X SR )

(b) Labor price variance:

( AH X AR )

(30,500 X $10.10)

$308,050

–

–

( AH X SR )

(30,500 X $10.00)

$305,000

=

$3,050 U

Labor quantity variance:

(30,500 X $10.00)

–

$300,000

=

$5,000 U

( AH X SR )

–

( SH X SR )

(c) Labor price variance:

( AH X AR )

(30,500 X $10.10)

$308,050

–

–

( AH X SR )

(30,500 X $10.20)

$311,100

=

$3,050 F

Labor quantity variance:

( AH X SR )

(30,500 X $10.20)

$311,100

–

–

( SH X SR )

$326,400

=

$15,300 F

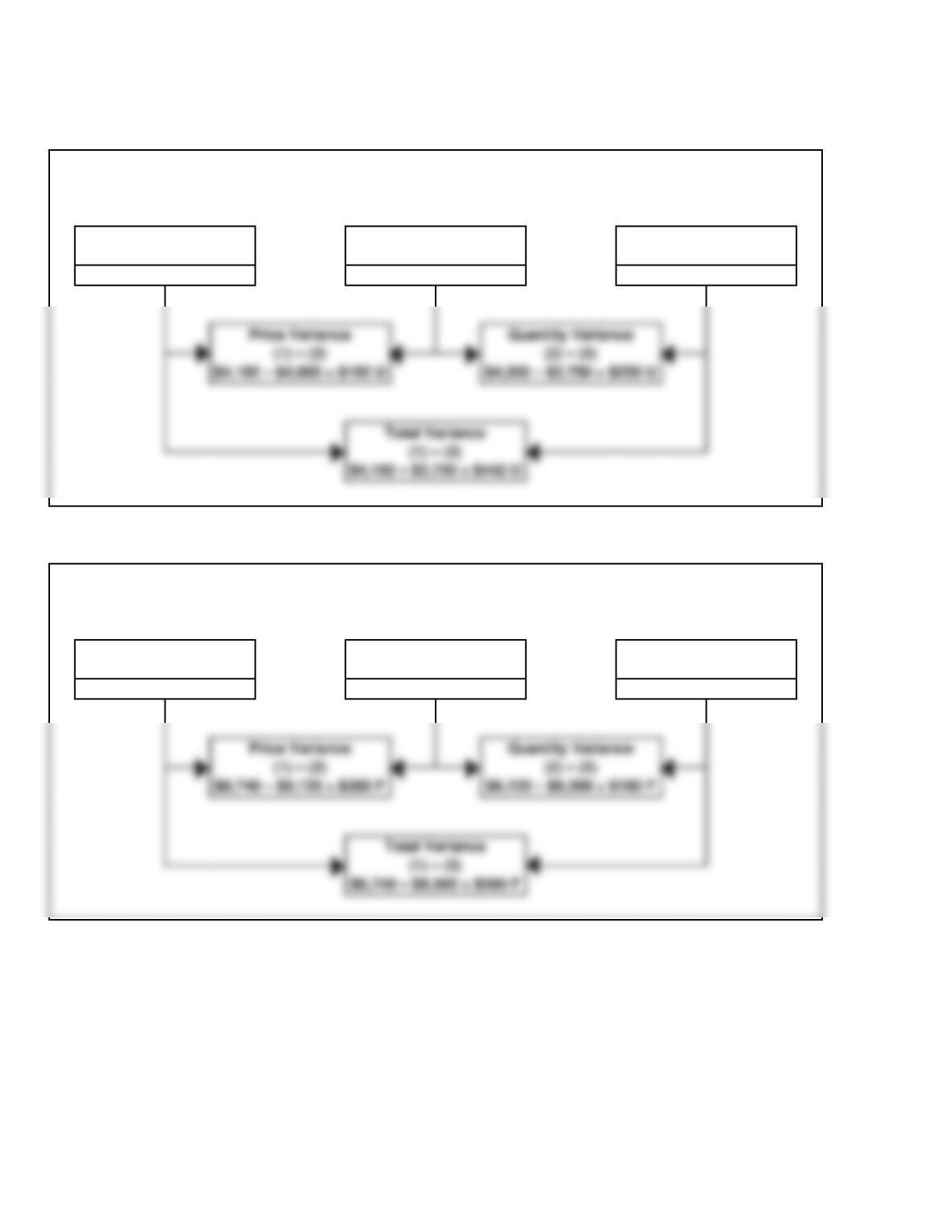

EXERCISE 11-7B

Total materials variance:

( AQ X AP )

(1,600 X $2.62*)

$4,192

–

–

( SQ X SP )

(1,500** X $2.50)

$3,750

=

$442 U

(30,500 X $10.10)

$308,050

–

=

EXERCISE 11-7B (Continued)

Materials quantity variance:

( AQ X SP )

(1,600 X $2.50)

$4,000

–

–

( SQ X SP )

(1,500 X $2.50)

$3,750

=

$250 U

Total labor variance:

( AH X AR )

(760 X $11.50*)

$8,740

–

–

( SH X SR )

(775** X $12.00)

$9,300

=

$560 F

$8,740

$9,120

=

$9,300

=

$180 F

EXERCISE 11-7B (Continued)

(Not Required)

Materials Variance Matrix

(1)

(2)

(3)

Actual Quantity

X Actual Price

Actual Quantity

X Standard Price

Standard Quantity

X Standard Price

1,600 X $2.62 = $4,192

1,600 X $2.50 = $4,000

1,500 X $2.50 = $3,750

Labor Variance Matrix

(1)

(2)

(3)

Actual Hours

X Actual Rate

Actual Hours

X Standard Rate

Standard Hours

X Standard Rate

760 X $11.50 = $8,740

760 X $12.00 = $9,120

775 X $12.00 = $9,300

EXERCISE 11-8B

(a) Total materials variance:

( AQ X AP )

(910 X $89)

$80,990

–

–

( SQ X SP )

(900 X $90)

$81,000

=

$10 F

Materials price variance:

( AQ X AP )

(910 X $89)

$80,990

–

–

( AQ X SP )

(910 X $90)

$81,900

=

$910 F

(b) The unfavorable materials quantity variance may be caused by the

carelessness or inefficiency of production workers. Alternatively, the

–

( SQ X SP )

$900 U

( AH X AR )

(3,200 X $13)

$41,600

–

–

( SH X SR )

$38,880

=

$2,720 U

$41,600

–

$38,400

=

$3,200 U

( AH X SR )

–

$480 F

EXERCISE 11-8B (Continued)

The unfavorable labor price variance may be caused by misallocation of

the work force by the production department. In this case, more

experienced workers may have been assigned to tasks normally done by

inexperienced workers. An unfavorable labor variance may also occur when

workers are paid higher wages than expected. The manager who

authorized the wage increase is responsible for this variance.

EXERCISE 11-9B

(a) Number of units = Total standard cost ÷ Standard cost per unit

Number of units = $396,000 ÷ $18.00 (6 lb X $3 per lb) = 22,000

(b) AQ = [(SQ X SP) Quantity variance] ÷ SP

AQ = ($396,000 – $9,000) ÷ $3.00 per lb = 129,000 pounds

EXERCISE 11-10B

MICKY TOOL & DIE COMPANY

Direct Labor Variance Report

For the Month Ended March 31, 2017

Job

No.

Actual

Hours

Standard

Hours

Quantity

Variance

(a)

Actual

Rate

(1)

Standard

Rate

(2)

Price

Variance

(b)

Explanation

U

F

worker

New trainee

B257

B258

B259

220

450

240

225

430

240

$125.00

(500.00

( 0

F

U

$25.00

$27.00

$25.75

$25.00

$25.00

$25.00

$ 0

900.00

180.00

U

U

Repeat job

Rush job

Replacement

±

±

±

±

EXERCISE 11-11B

Total overhead variance:

Actual Overhead

–

Overhead Applied

EXERCISE 11-12B

(a)

Overhead Budget

(at normal capacity)

÷

Direct Labor Hours

(at normal capacity)

=

Predetermined

Overhead Rate

Variable

$200,000

100,000

$2

Fixed

800,000

100,000

$8

(b)

=

(c)

$986,000

=

$94,000 F

($186,000 + $800,000)

EXERCISE 11-13B

(a)

(AQ X AP)

( $13,000)

–

–

( SQ X SP)

(3,080* X $4)

=

=

Total Materials Variance

$680 U

(AQ X AP)

( $13,000)

–

–

=

=

Materials Price Variance

–

–

( SQ X SP)

=

=

Materials Quantity Variance

(b) One possible cause of an unfavorable materials quantity variance is

the purchase of substandard materials. Such materials would

normally be purchased at a lower price than normal, which means

$4,000 U

EXERCISE 11-14B

(a) PLEASANT LANDSCAPING

Variance Report – Purchasing Department

For the Current Month

Project

Actual

Pounds

Purchased

(1)

Actual

Price

(2)

Standard

Price

Price

Variance

(a)

Explanation

Bear

500

$2.80

$3.00

$100 F

Purchased poor quality seeds

(b) PLEASANT LANDSCAPING

Variance Report – Production Department

For the Current Month

Project

Actual

Pounds

Standard

Pounds

Standard

Price

Quantity

Variance

(b)

Explanation

Bear

Kanyon

500

400

460

410

$3.00

3.00

$120 U

30 F

Purchased poor quality seeds

Purchased higher quality seeds

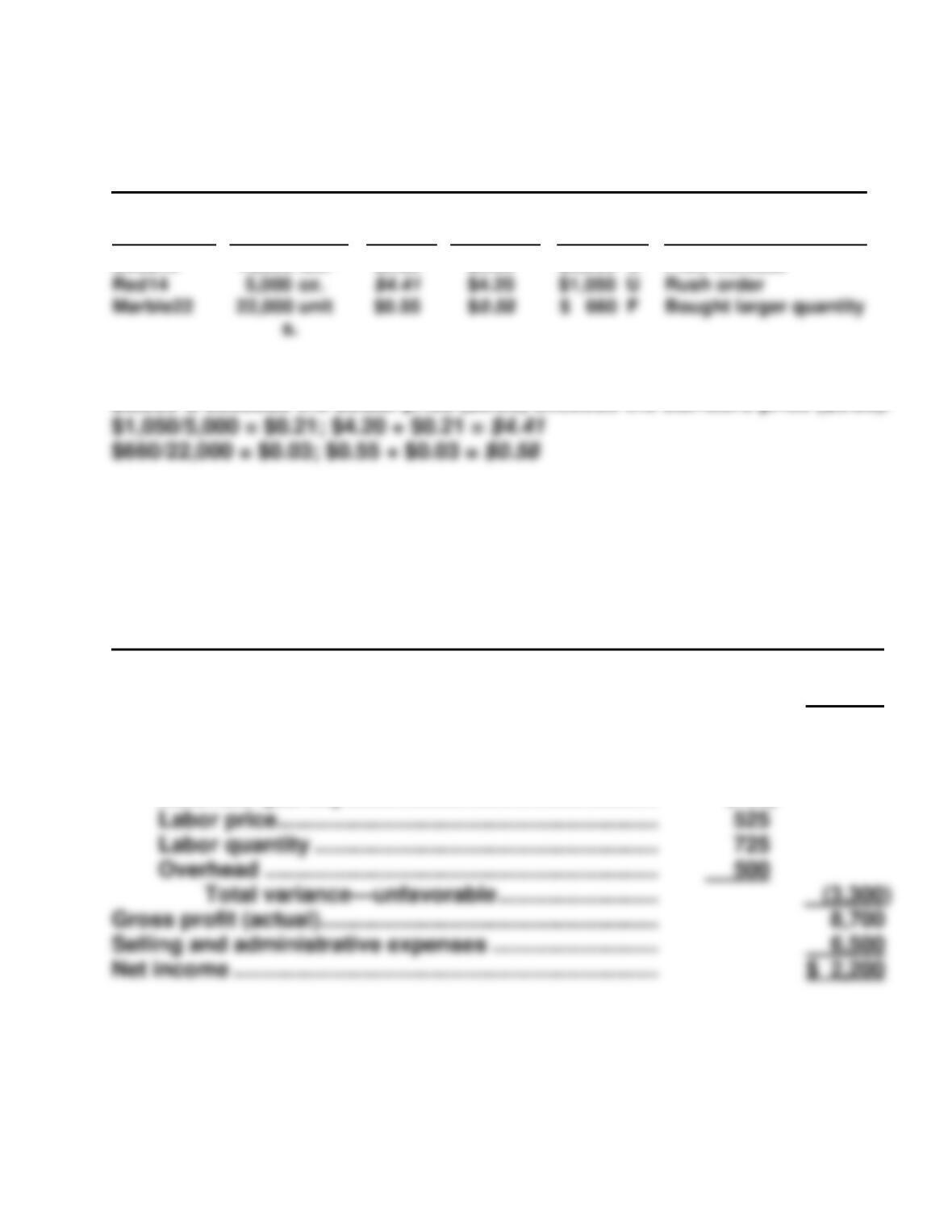

EXERCISE 11-15B

NEWMAR CORPORATION

Variance Report – Purchasing Department

For Week Ended January 9, 2017

Type of

Materials

Quantity

Purchased

Actual

Price

Standard

Price

Price

Variance

Explanation

Soda10

15,000 lbs.

$5.20

$5.00

$3,000 U

Price increase

15,000 = $3,000/($5.20 – $5.00).

$3,000 U because the actual price ($5.20) exceeds the standard price ($5.00).

EXERCISE 11-16B

POTTER COMPANY

Income Statement

For the Month Ended January 31, 2017

Sales (6,000 X $8) ………………………………………………….. $48,000

Cost of goods sold (6,000 X $6) ……………………………… 36,000

Gross profit (at standard) ………………………………………. 12,000

Variances

Materials price ……………………………………………….. $2,250

Materials quantity …………………………………………… (700)

*EXERCISE 11-17B

1. Raw Materials Inventory (25,000 X $4.30) ……………. 107,500

Materials Price Variance (25,000 X $.20) ……………… 5,000

Accounts Payable (25,000 X $4.50) ………………. 112,500

2. Work in Process Inventory (23,500 X $4.30) ………… 101,050

*EXERCISE 11-18B

(a) $151,000 ($148,000 + $3,000).

(b) $148,000 ($151,000 – $3,000).

*EXERCISE 11-19B

Raw Materials Inventory (1,600 X $2.50) ………………………. 4,000

*EXERCISE 11-19B (Continued)

Work in Process Inventory (1,500* X $2.50) …………………. 3,750

Materials Quantity Variance (100 X $2.50) ……………………. 250

Raw Materials Inventory (1,600 X $2.50) ……………….. 4,000

*250 X 6

*250 X 3.1

*EXERCISE 11-20B

(a)

Item

Amount

Hours

Rate

Total overhead …………………………………

$55,000

11,000

Variable overhead …………………………….

$33,000

11,000

$3

(b) Total overhead variance:

Actual Overhead

$54,000

–

–

Overhead Applied

$50,000

(10,000* X $5)

=

$4,000 U

$54,000

–

$52,000

=

*EXERCISE 11-20B (Continued)

(c) The overhead controllable variance is generally associated with variable

overhead costs. Thus, this variance indicates the production manager’s

inefficiency in controlling variable overhead costs.

*EXERCISE 11-21B

(a)

(1)

Total actual overhead cost

=

Overhead

Budgeted +

Overhead

Controllable

Variance

=

($16,000 + $11,500) + $1,500

=

$29,000

=

=

=

*$11,500 ÷ $5 per hour = 2,300 hours

(b)

Number of loans processed

=

Standard hours allowed ÷

Standard hours per application

*EXERCISE 11-22B

(a)

(Actual)

($21,000)

–

–

(Applied)

(1,800 X $11*)

=

=

Total Overhead Variance

$1,200 U

*$198,000/18,000

(Actual)

($21,000)

–

–

(Budgeted)

($18,600)

=

=

Overhead Controllable Variance

$2,400 U

(b) The cause of an unfavorable controllable variance could be higher than

expected use of indirect materials, indirect labor, and factory supplies, or

increases in indirect manufacturing costs, such as fuel and maintenance

=

SOLUTIONS TO EXERCISES—SET C

PROBLEM 11-1C

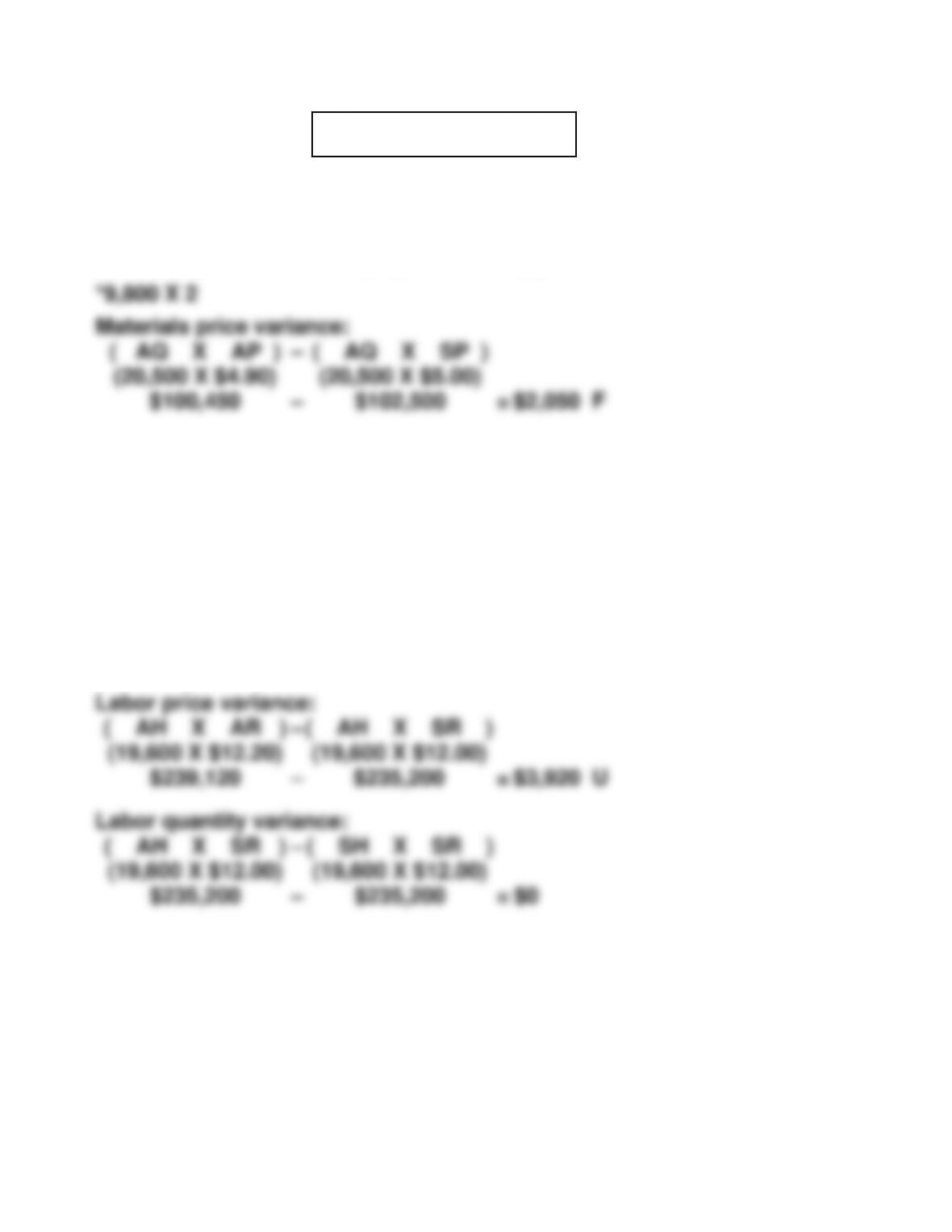

(a) Total materials variance:

( AQ X AP )

(20,500 X $4.90)

$100,450

–

–

( SQ X SP )

(19,600* X $5.00)

$98,000

=

$2,450 U

Materials quantity variance:

( AQ X SP )

(20,500 X $5.00)

$102,500

–

–

( SQ X SP )

(19,600 X $5.00)

$98,000

=

$4,500 U

Total labor variance:

( AH X AR )

(19,600 X $12.20)

$239,120

–

–

( SH X SR )

(19,600* X $12.00)

$235,200

=

$3,920 U

$239,120

–

–

$235,200

=

$3,920 U

$235,200

–

–

( SH X SR )

=

*9,800 X 2

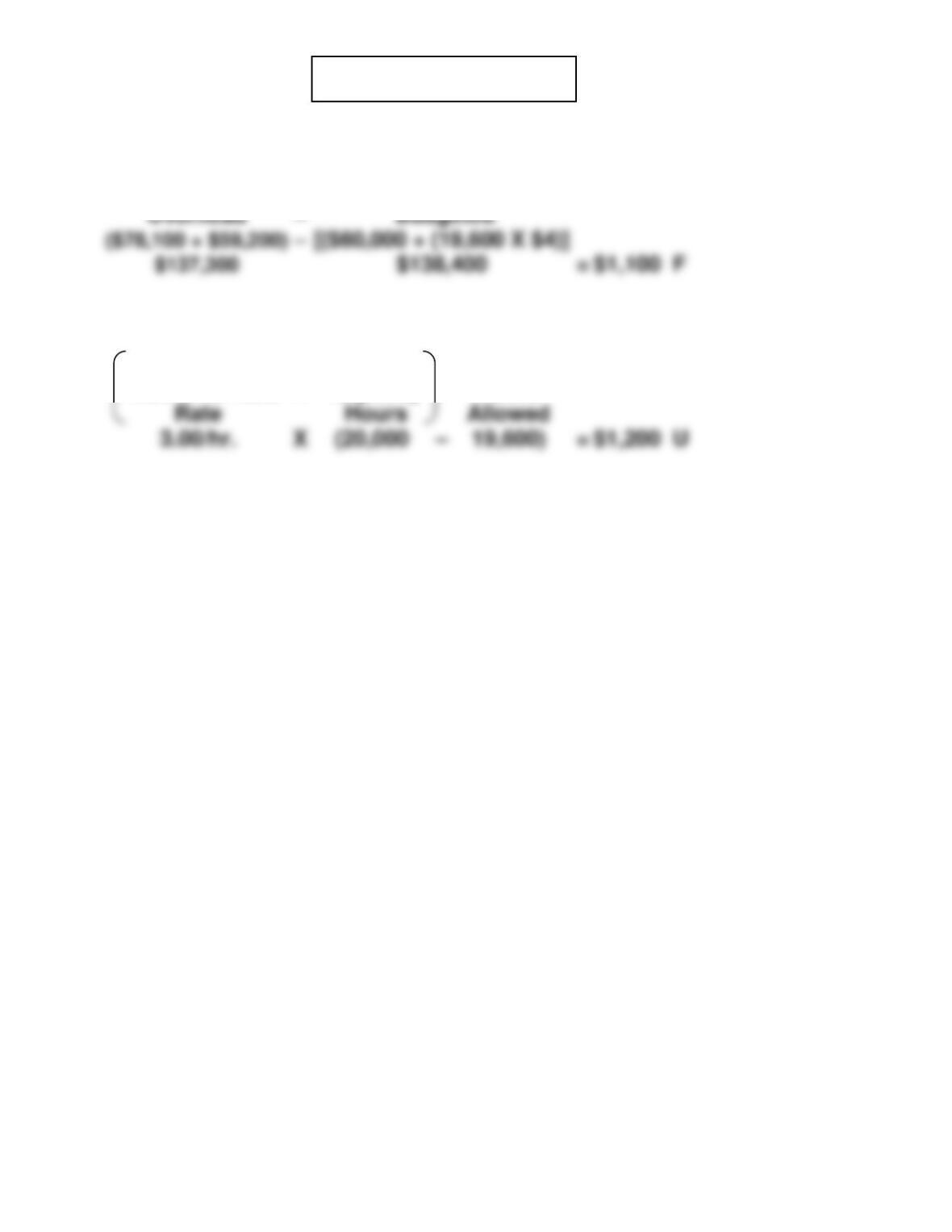

(b) Total overhead variance:

Actual

Overhead

($78,100 + $59,200)

$137,300

–

–

Overhead

Applied

(19,600 X $7.00*)

$137,200

=

$100 U

*Standard per labor hour overhead cost ($4 variable + $3 fixed).

$100,450

–

=

$2,050 F

PROBLEM 11-2C

(a) (1) Total materials variance:

( AQ X AP )

(21,000 X $3.30)

$69,300

–

–

( SQ X SP )

(22,000 X $3.00)

$66,000

=

$3,300 U

(2) Total labor variance:

( AH X AR )

(3,450 X $11.80)

$40,710

–

–

( SH X SR )

(3,600 X $12.50)

$45,000

=

$4,290 F

( AH X AR )

$40,710

–

–

$43,125

=

$2,415 F

–

( SH X SR )

(b) Total overhead variance:

Actual

Overhead

$101,500

–

–

Overhead

Applied

$104,400

(3,600 X $29*)

=

$2,900 F

( AQ X AP )

–

–

$63,000

=

$6,300 U

( AQ X SP )

–

( SQ X SP )

PROBLEM 11-2C (Continued)

(c) BORTON MANUFACTURING COMPANY

Income Statement

For the Month Ended July 31, 2017

Sales …………………………………………………………. $280,000

Cost of goods sold (at standard) …………………. 215,4001

Gross profit (at standard) …………………………... 64,600

Variances

Materials price …………………………………….. $ 6,300

Materials quantity ……………………………….. (3,000)

PROBLEM 11-3C

(a) (1) Total materials variance:

( AQ X AP )

(76,000 X $7.20)

$547,200

–

–

( SQ X SP )

(78,500* X $6.90)

$541,650

=

$5,550 U

*15,700 X 5

Materials price variance:

(2) Total labor variance

( AH X AR )

(14,900 X $11.20)

$166,880

–

–

( SH X SR )

(15,700 X $11.40)

$178,980

=

$12,100 F

( AH X AR )

(14,900 X $11.20)

$166,880

–

–

$169,860

=

$2,980 F

–

–

( SH X SR )

(15,700 X $11.40)

$178,980

=

$9,120 F

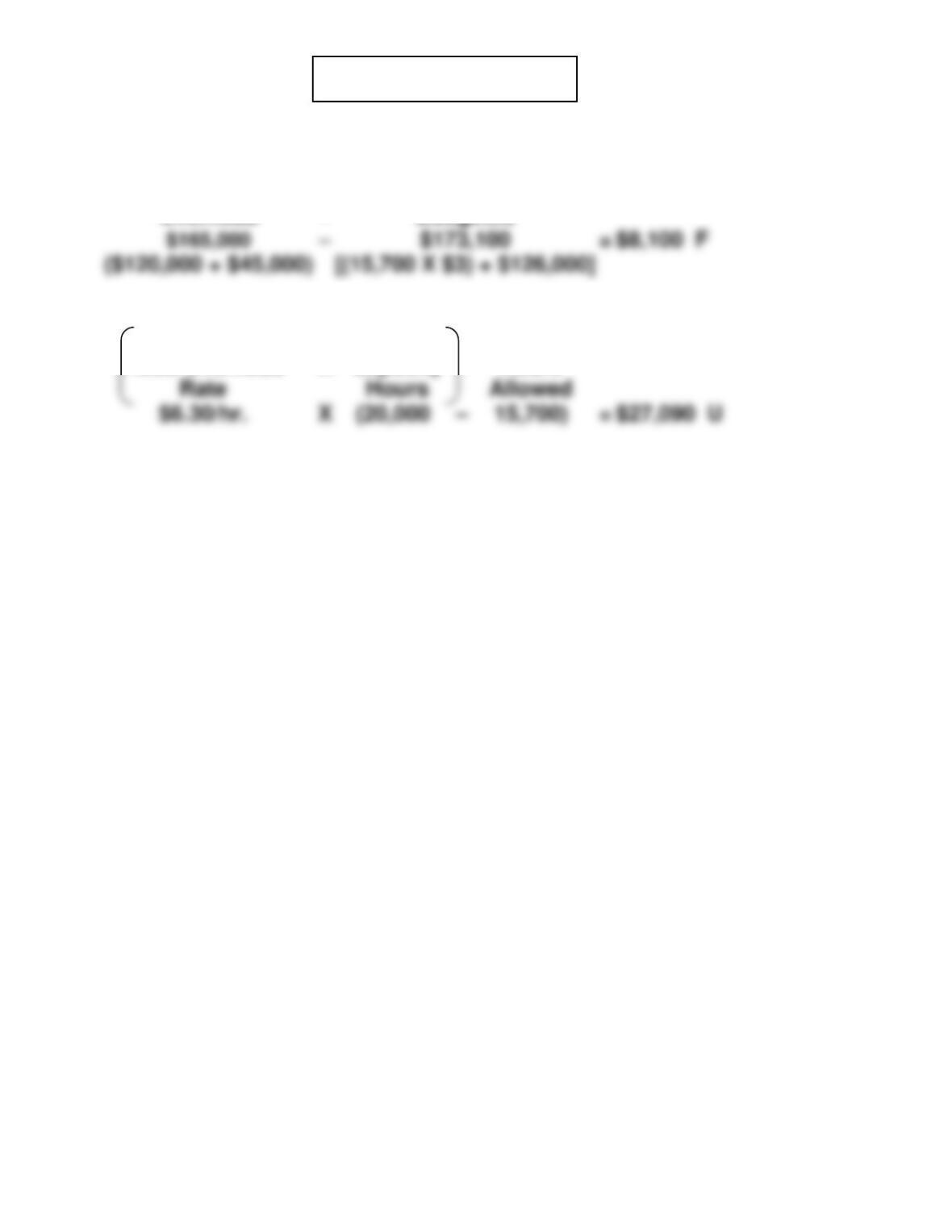

(b) Total overhead variance:

Actual

Overhead

–

Overhead

Applied

$18,990 U

$547,200

–

–

=

$22,800 U

( AQ X SP )

$524,400

–

–

( SQ X SP )

$541,650

=

$17,250 F

PROBLEM 11-3C (Continued)

(c) The only variance that is more than 5% from standard is:

Labor quantity variance. The actual hours of 14,900 is 5.1% under the

standard hours of 15,700.

PROBLEM 11-4C

(a) $10,000 ÷ 200,000 = $.05; $1.00 – $.05 = $.95 standard materials price per

pound. OR

200,000 X $1.00 = $200,000; $200,000 – $10,000 = $190,000; $190,000 ÷

200,000 = $.95.

(b) $23,750 ÷ $.95 = 25,000 pounds; 200,000 + 25,000 = 225,000 standard

quantity for 50,000 units or 4.5 pounds (225,000 ÷ 50,000) per unit. OR

$190,000 + $23,750 = $213,750; $213,750 ÷ $.95 = 225,000; 225,000 ÷

50,000 = 4.5 pounds per unit.

(g) Direct materials 4.5 pounds X $.95 = $4.275; direct labor 2 X $12.00 =

$24.00; manufacturing overhead 2 X $8.30 = $16.60. $4.275 + $24.00 +

$16.60 = $44.875 standard cost per unit.

(h) 100,000 X $8.30 = $830,000 overhead applied.

PROBLEM 11-5C

(a) Materials price variance:

( AQ X AP )

(2,540 X $2.05*)

$5,207

–

–

( AQ X SP )

(2,540 X $2.00)

$5,080

=

$127 U

*$5,207 ÷ 2,540

(b) Total overhead variance:

Actual Overhead

$16,000

–

–

Overhead Applied

$15,000

–

=

(AH X AR)

(1,240 X $21.10*)

–

–

$1,364 U

–

–

=

$200 F

PROBLEM 11-5C (Continued)

(c) ALOE LABS

Income Statement

For the Month Ended May 31, 2017

Service revenue ……………………………………………… $58,000

Cost of service provided (at standard)

($18 X 2,500) ……………………………………………….. 45,000

Gross profit (at standard) ……………………………….. 13,000

Variances

(d) The unfavorable materials price variance could be caused by price

increases, using the wrong shipping method, or rising prices.

The unfavorable materials quantity variance could be caused by inex–

perienced workers, carelessness, poor quality material, or faulty test

procedures.

*PROBLEM 11-6C

(a) 1. Raw Materials Inventory (8,200 X $4.00) ……… 32,800

2. Work in Process Inventory …………………………. 30,800

(7,700* X $4.00)

Materials Quantity Variance ……………………….. 2,000

3. Factory Labor (5,200 X $9.00) …………………….. 46,800

Labor Price Variance …………………………………. 1,300

4. Work in Process Inventory …………………………. 49,500

(5,500 X $9.00)

Factory Labor …………………………………….. 46,800

5. Manufacturing Overhead …………………………... 85,760

Accounts Payable ………………………………. 85,760

6. Work in Process Inventory …………………………. 84,700

(5,500 X $15.40)

Manufacturing Overhead …………………….. 84,700

9. Selling and Administrative Expenses ………… 65,000

Accounts Payable ……………………………… 65,000

*PROBLEM 11-6C (Continued)

(b)

Raw Materials Inventory

Materials Price Variance

Work in Process Inventory

(1) 32,800

(2) 32,800

(1) 3,280

(2) 30,800

(4) 49,500

(6) 84,700

(7) 165,000

(c) Overhead Variance (1) …………………………………………… 1,060

Manufacturing Overhead…………………………………. 1,060

(d) PLANTER MANUFACTURING COMPANY

Income Statement

For the Month Ended January 31, 2017

Sales revenue ………………………………………………… $280,000

Cost of goods sold (at standard) …………………….. 165,000

(5,500 X $30)

Gross profit (at standard) ……………………………….. 115,000

Variances

*PROBLEM 11-7C

Overhead controllable variance:

Actual

Overhead

Overhead volume variance:

Fixed Overhead

X

Normal

Capacity

–

Standard

Hours

*PROBLEM 11-8C

Overhead controllable variance:

Actual

Overhead

$101,500

–

–

Overhead

Budgeted

$102,600

=

$1,100 F

PROBLEM 11-9C

Overhead controllable variance:

Actual

Overhead

–

Overhead

Budgeted

Overhead volume variance:

Fixed Overhead

X

Normal

Capacity

–

Standard

Hours

*PROBLEM 11-10C

Overhead controllable variance:

Actual Overhead

$16,000

[($10,100 + $5,900)

–

–

–

Overhead Budgeted

$16,000

[(1,250 X $8) + $6,000]

=

$0

Overhead volume variance:

Capacity

=

$1,000 U