CHAPTER 11 Current Liabilities and Payroll

1. Jan. 3 Petty Cash 4,500

Cash 4,500

Feb. 26 Office Supplies 1,680

Miscellaneous Selling Expense 570

Miscellaneous Administrative Expense 880

Cash 3,130

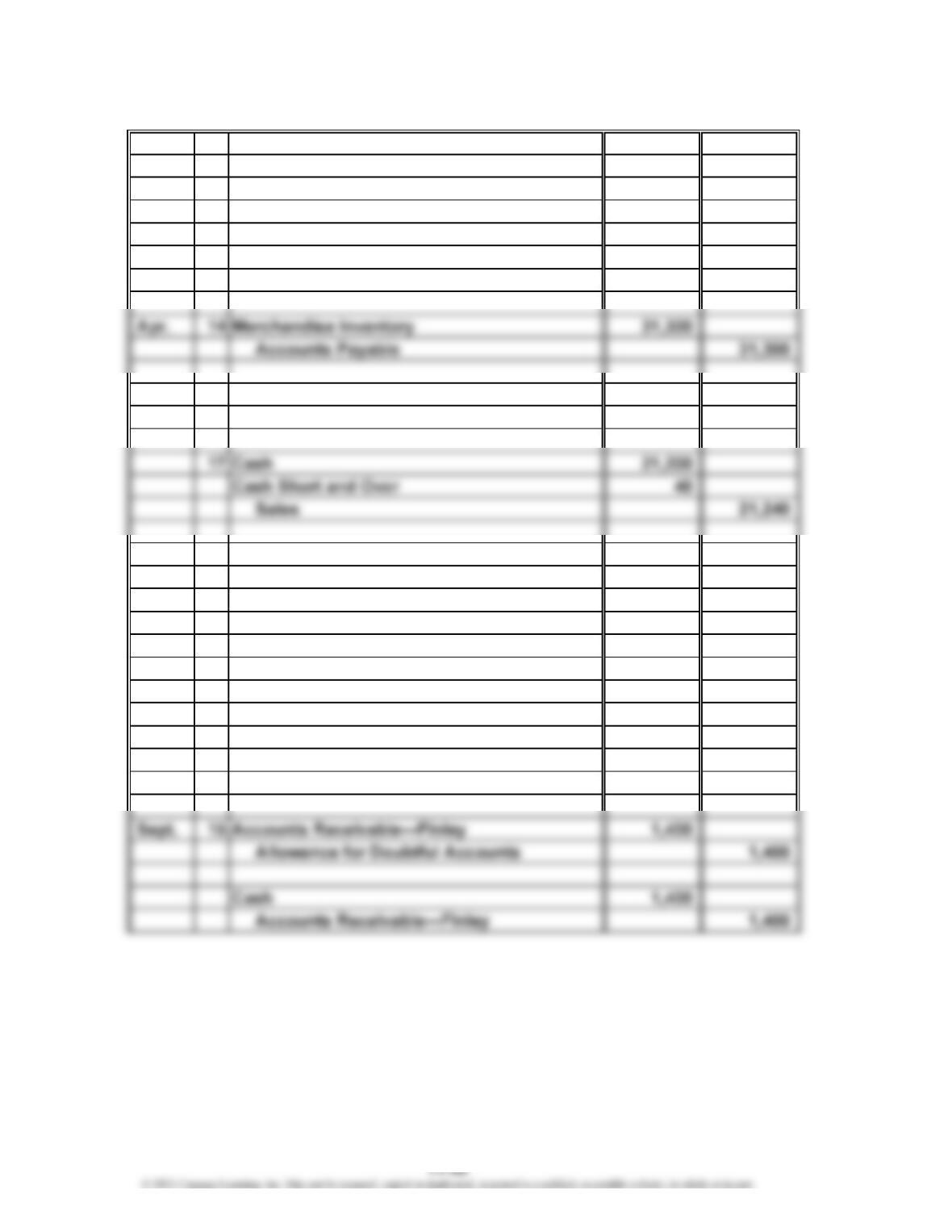

May 13 Accounts Payable 31,300

Cash 31,300

June 2 Notes Receivable 180,000

Accounts Receivable—Ryanair 180,000

Aug. 1 Cash 182,400

Notes Receivable 180,000

Interest Revenue 2,400

($180,000 × 8% × 60 ÷ 360).

24 Cash 7,600

Allowance for Doubtful Accounts 1,400

Accounts Receivable—Finley 9,000

COMPREHENSIVE PROBLEM 3

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

Sept. 15 Land 654,925

Interest Expense 15,075

Notes Payable 670,000

($670,000 × 90 ÷ 360 × 9%).

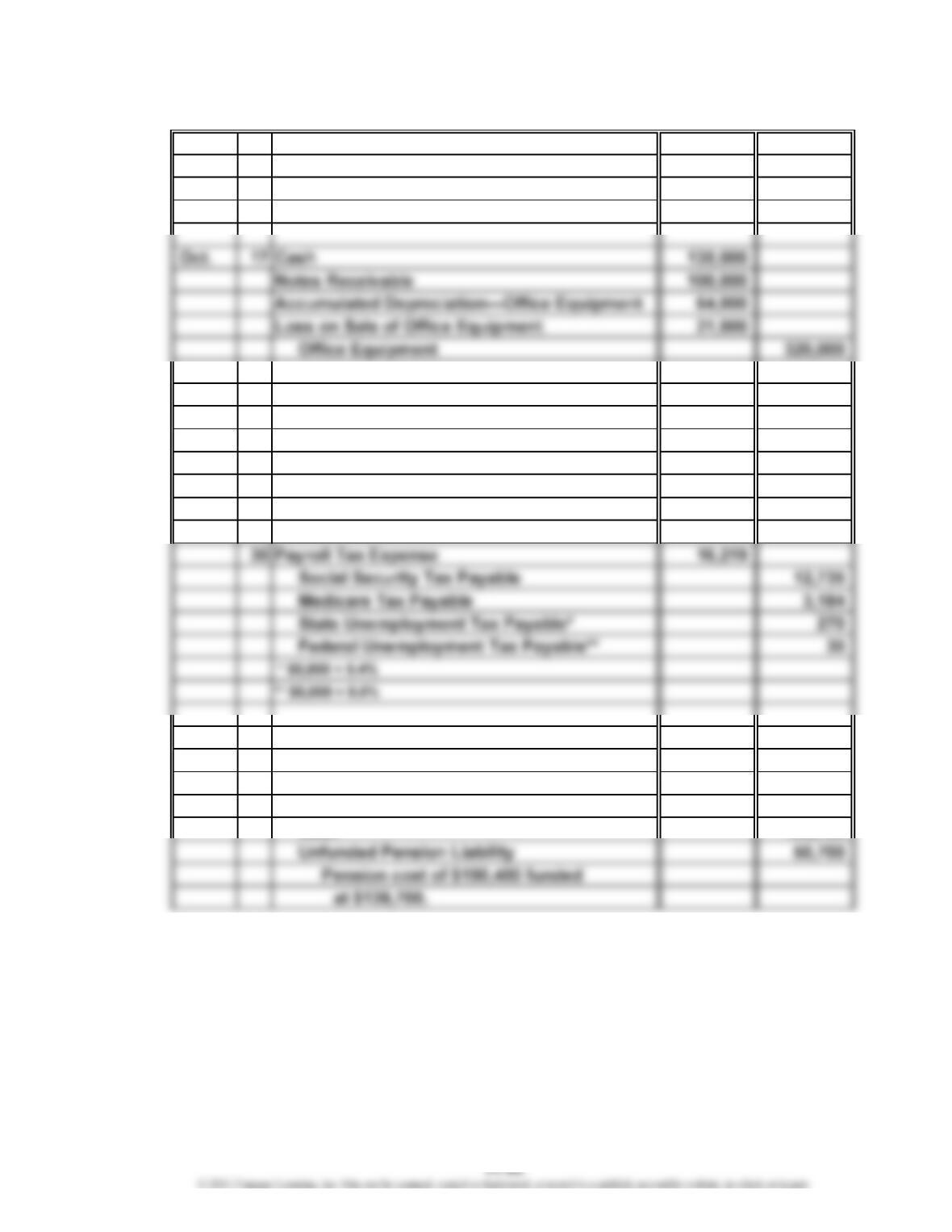

Nov. 30 Sales Salaries Expense 135,000

Office Salaries Expense 77,250

Employees Federal Income Tax Payable 39,266

Social Security Tax Payable 12,735

Medicare Tax Payable 3,184

Salaries Payable 157,065

Dec. 14 Notes Payable 670,000

Cash 670,000

31 Pension Expense 190,400

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

2.

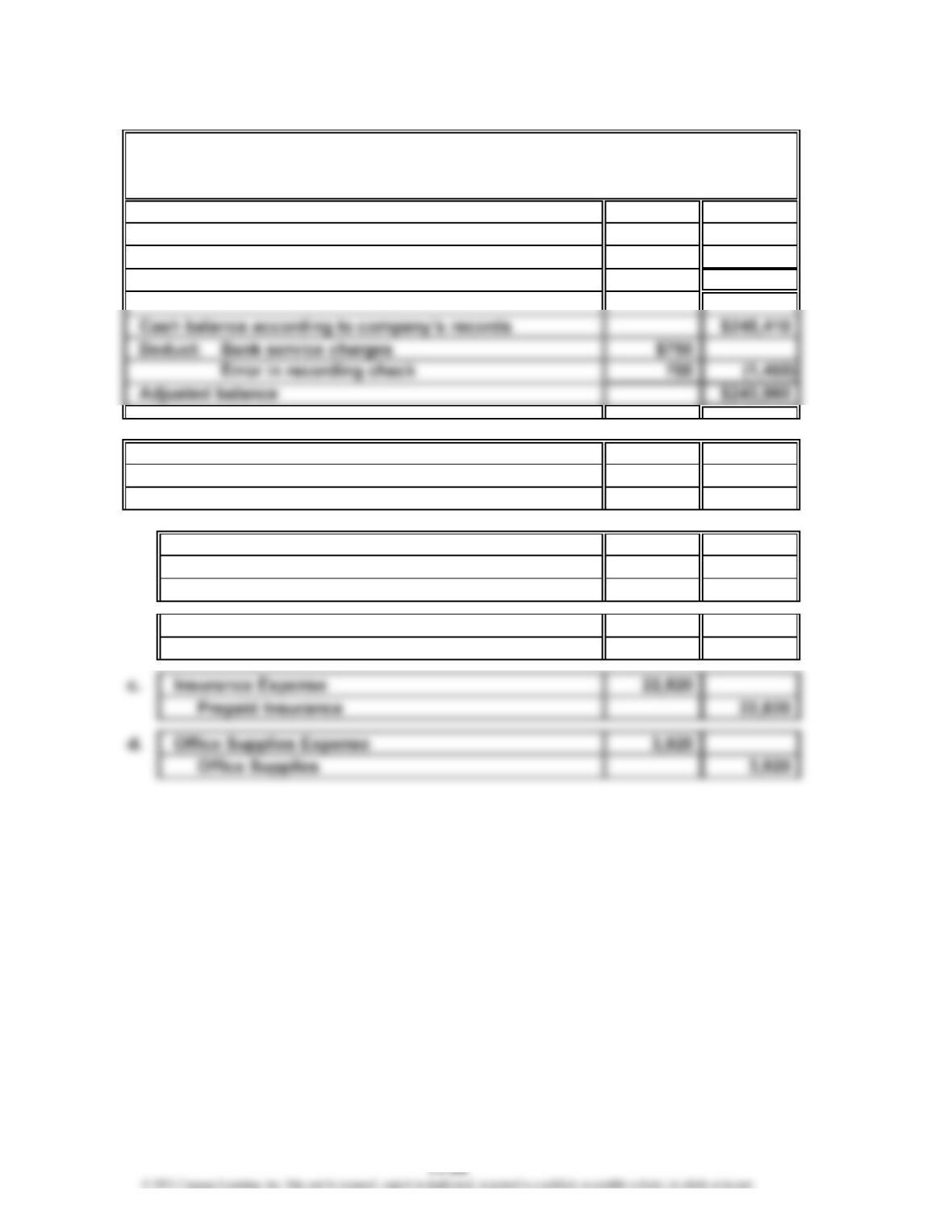

Cash balance according to bank statement $283,000

Add deposit in transit, not recorded by bank 29,500

Deduct outstanding checks (68,540)

Adjusted balance $243,960

3. Miscellaneous Expense 750

Accounts Payable 700

Cash 1,450

4. a. Bad Debt Expense 18,000

Allowance for Doubtful Accounts 18,000

($16,000 + $2,000).

b. Cost of Merchandise Sold 3,300

Merchandise Inventory 3,300

Kornett Company

Bank Reconciliation

December 31, 20Y8

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

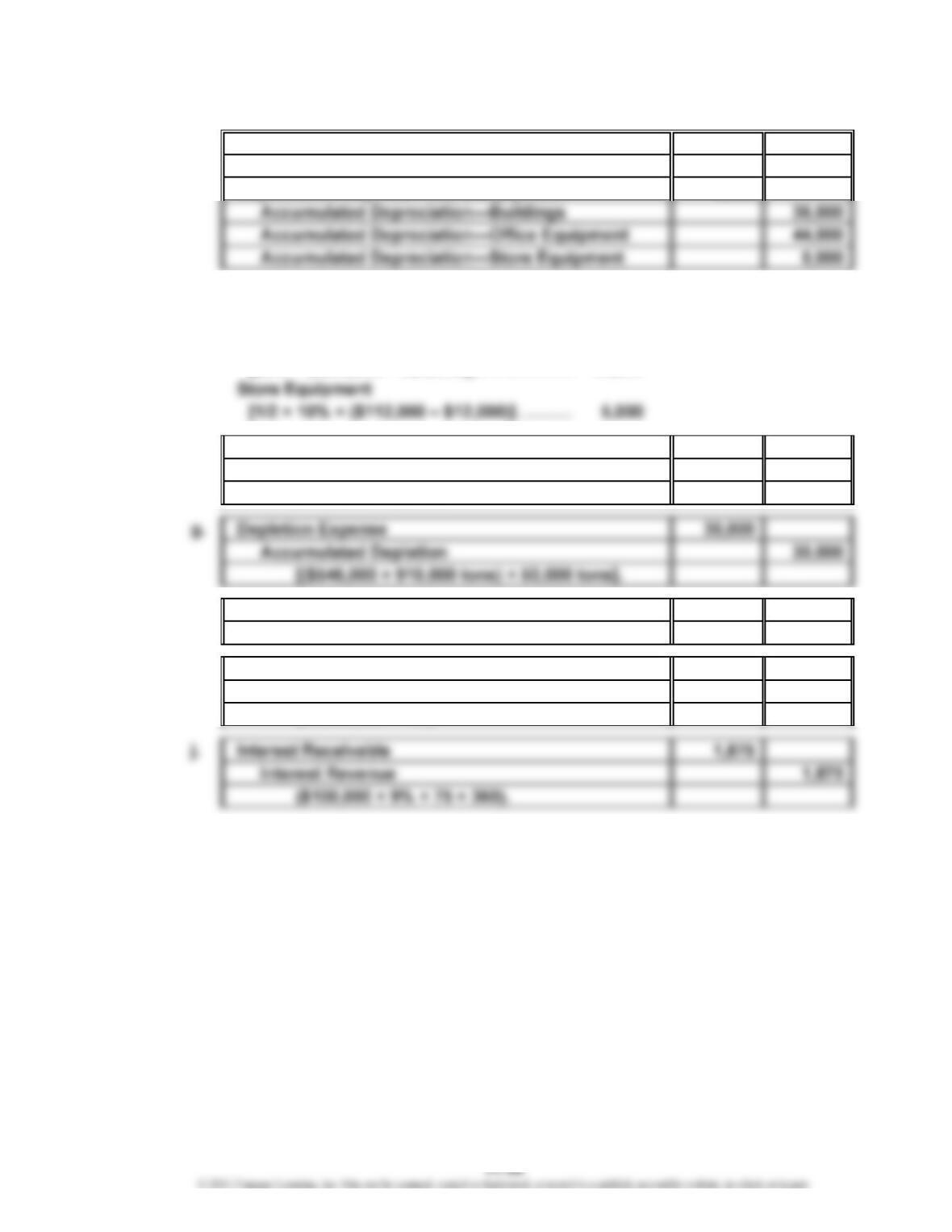

e. Depreciation Expense—Buildings 36,000

Depreciation Expense—Office Equipment 44,000

Depreciation Expense—Store Equipment 5,000

Computations:

Buildings ($900,000 × 4%)…………………

…

$36,000

Office Equipment

[20% × ($246,000 – $26,000)]……………… 44,000

f. Amortization Expense—Patents 6,000

Patents 6,000

($48,000 ÷ 8 years).

h. Vacation Pay Expense 10,500

Vacation Pay Payable 10,500

i. Product Warranty Expense 76,000

Product Warranty Payable 76,000

($1,900,000 × 4%).

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

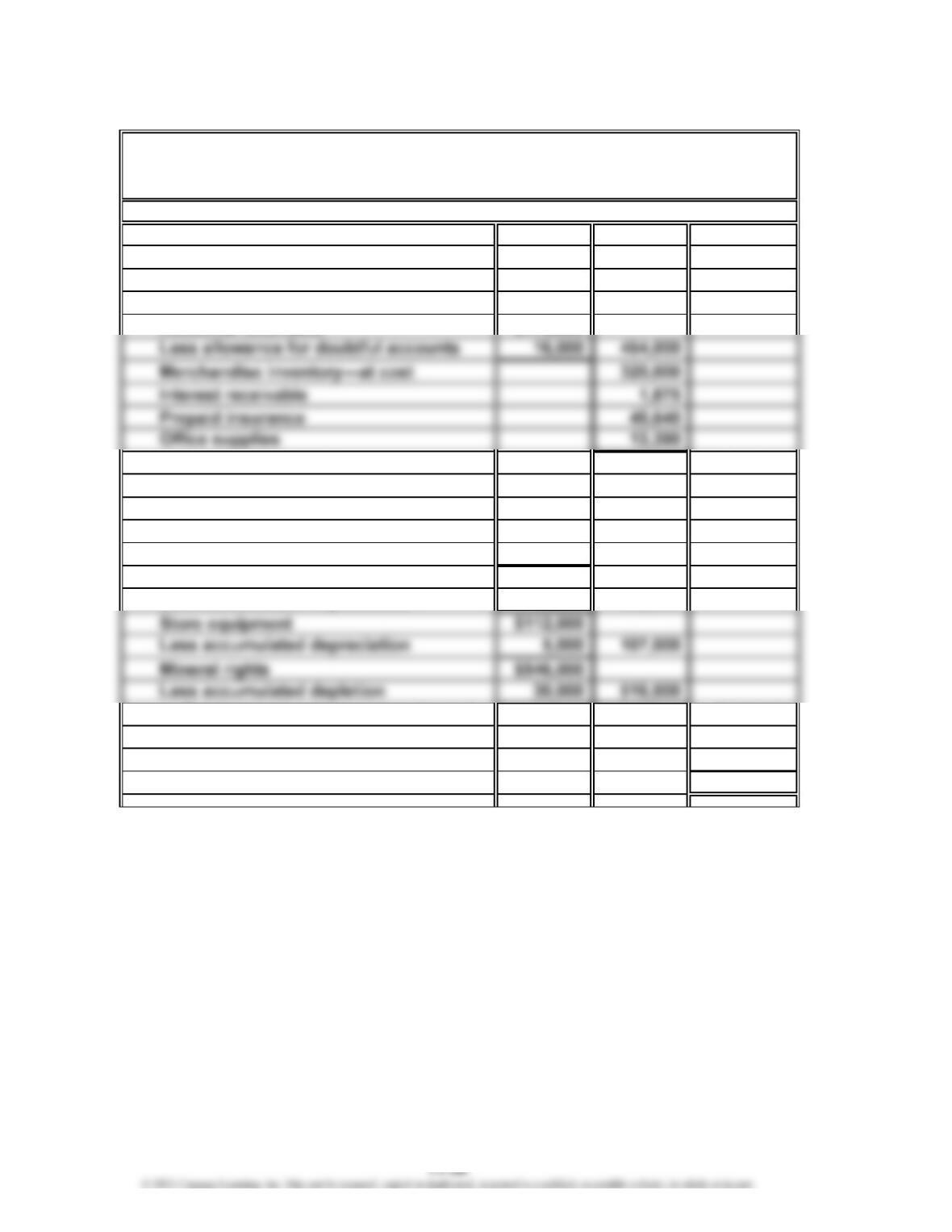

5.

Current assets:

Petty cash $ 4,500

Cash 243,960

Notes receivable 100,000

Total current assets $1,183,365

Property, plant, and equipment:

Land $654,925

Buildings $900,000

Less accumulated depreciation 36,000 864,000

Office equipment $246,000

Less accumulated depreciation 44,000 202,000

Total property, plant, and equipment 2,343,925

Intangible assets:

Patents 42,000

Total assets $3,569,290

Kornett Company

Balance Sheet

December 31, 20Y8

Assets

CHAPTER 11 Current Liabilities and Payroll

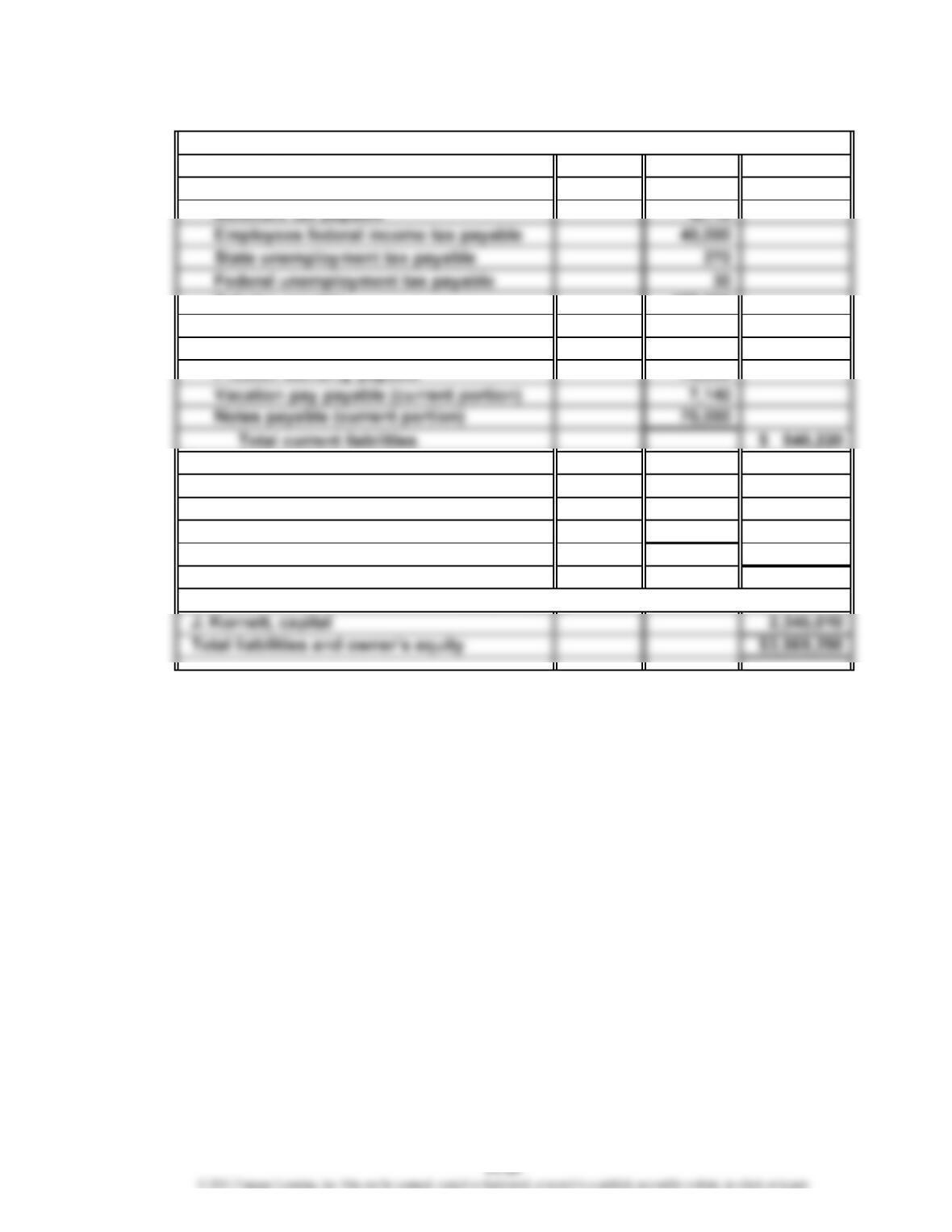

Comp. Prob. 3 (Concluded)

Current liabilities:

Social security tax payable $ 25,470

Salaries payable 157,000

Accounts payable 131,600

Interest payable 28,000

Long-term liabilities:

Vacation pay payable $ 3,360

Unfunded pension liability 50,700

Notes payable 630,000

Total long-term liabilities 684,060

Total liabilities $1,224,280

Liabilities

Owner’s Equity

CHAPTER 11 Current Liabilities and Payroll

CP 11-1

1. Cannally and Kennedy is not obligated to pay a bonus to its employees under any

circumstances. The decision to pay a bonus is discretionary. Companies frequently

2. Tonya Latirno, on the other hand, is behaving unethically. Believing that she is being

cheated, Tonya is attempting to replace the bonus by working overtime that is not

required. This behavior is fraudulent if the overtime is unnecessary, even though

Tonya is present on the job during the overtime hours. Tonya is incorrect in thinking

CP 11-2

1. The so-called “underground economy” hides transactions from IRS scrutiny by

conducting business with cash (not check or credit card, which leaves an audit

trail). The intent in many such transactions is to evade income tax illegally. However,

just because a transaction is in cash does not exempt it from taxation. Tina Song

also appears to perform construction services on a cash basis to evade reporting

2. Marvin should respond that he would rather receive a payroll check as a normal

employee does. As an employee, receiving cash rather than a payroll check

subverts the U.S. tax system. That is, such cash payments do not include

deductions for payroll taxes, as required by law. That is why, for example, cash tips

CASES & PROJECTS

CHAPTER 11 Current Liabilities and Payroll

CP 11-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2018,

follows:

1. $6,040 million. The company’s current liabilities include accounts payable, notes

payable, current portion of long-term debt, accrued liabilities, and income taxes

payable.

2. The company’s current liabilities have increased by $566 million, from $5,474 million

to $6,040 million.

CP 11-4

The purpose of this activity is to familiarize students with retrieving and using IRS forms.

Students should be able to find the three required forms without much difficulty.

Encourage students to retrieve the forms from the IRS website because this is a useful

forms on the web require a PDF reader.

The W-2 form is the Annual Wage and Tax Statement transmitted by the employer to the

IRS. The IRS uses this information to reconcile the taxpayer’s reported income and

withholding taxes with the taxpayer’s tax return. Copies of the W-2 are provided for the

employee’s own records and for submission with state and federal tax returns.

CP 11-5

Memo

To: U. D. Mach III

From: A+ Student

Re: Financial Reporting of Series 3 Shock Absorber Lawsuit

The customer lawsuit filed against WBM Motorworks arising from cracks in Series 3

motorcycle front shock absorbers creates a potential liability for the company. The way

in which this potential liability is reported on the financial statements depends on two

factors: what the likelihood is of losing the lawsuit and whether the amount of the loss

Based on the information that exists at this time, it appears that a loss should be

recorded on the income statement and a liability should be recorded on the balance

sheet. The discovery of a manufacturing defect and the associated recall significantly

increases the likelihood that the company will lose the lawsuit if it is taken to trial.

While a direct link has not been made between the manufacturing defect and the shock

An alternative argument could be made that the uncertainty surrounding the connection

between the manufacturing defect and the cracked shock absorber is too uncertain to

classify the likelihood of losing the lawsuit as probable. Rather, the likelihood of losing

the lawsuit would be classified as reasonably possible. In this case, the lawsuit would be

disclosed in the notes to the financial statements, but no loss or liability would be

reported on the financial statements.

CHAPTER 11 Current Liabilities and Payroll

CP 11-6

Sumana’s interpretation of the pension issue is correct. The employee earns the pension

during the working years. The pension is part of the employee’s compensation that is

deferred until retirement. Thus, Felton should record an expense equal to the amount of

pension benefit earned by the employee for the period. This gives rise to the rather

complex issue of estimating the amount of the pension expense. Francie indicates that

CP 11-7

This activity does not require students to research the contingency notes for Philip

Morris International Inc. (PMI). The contingency disclosure is extensive and complicated.

Rather, the student should identify PMI’s main business and from this information

determine the likely cause of the contingency disclosures.

1. PMI is a holding company for a number of businesses. Thus, PMI’s primary business

is in the manufacture and distribution of tobacco products.