EXERCISE 11-6

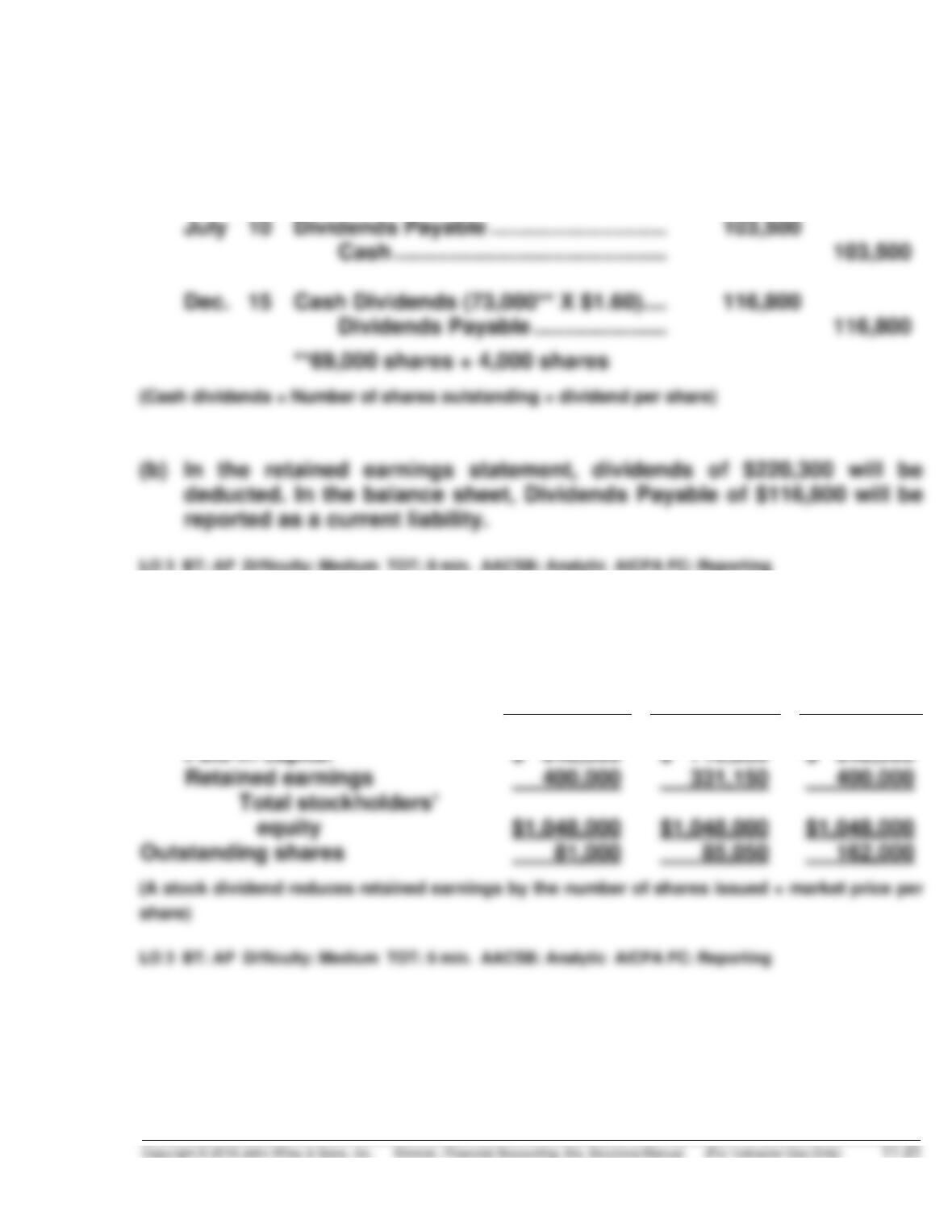

(a) June 15 Cash Dividends (69,000* X $1.50) ….. 103,500

Dividends Payable …………………. 103,500

*60,000 shares + 9,000 shares

EXERCISE 11-7

Before

Action

After Stock

Dividend

After Stock

Split

Stockholders’ equity

Paid-in capital

$ 648,000

Retained earnings

Outstanding shares

EXERCISE 11-8

WELLS FARGO & COMPANY

Partial Balance Sheet

December 31, 2017

(in millions)

Stockholders’ equity

Paid-in capital

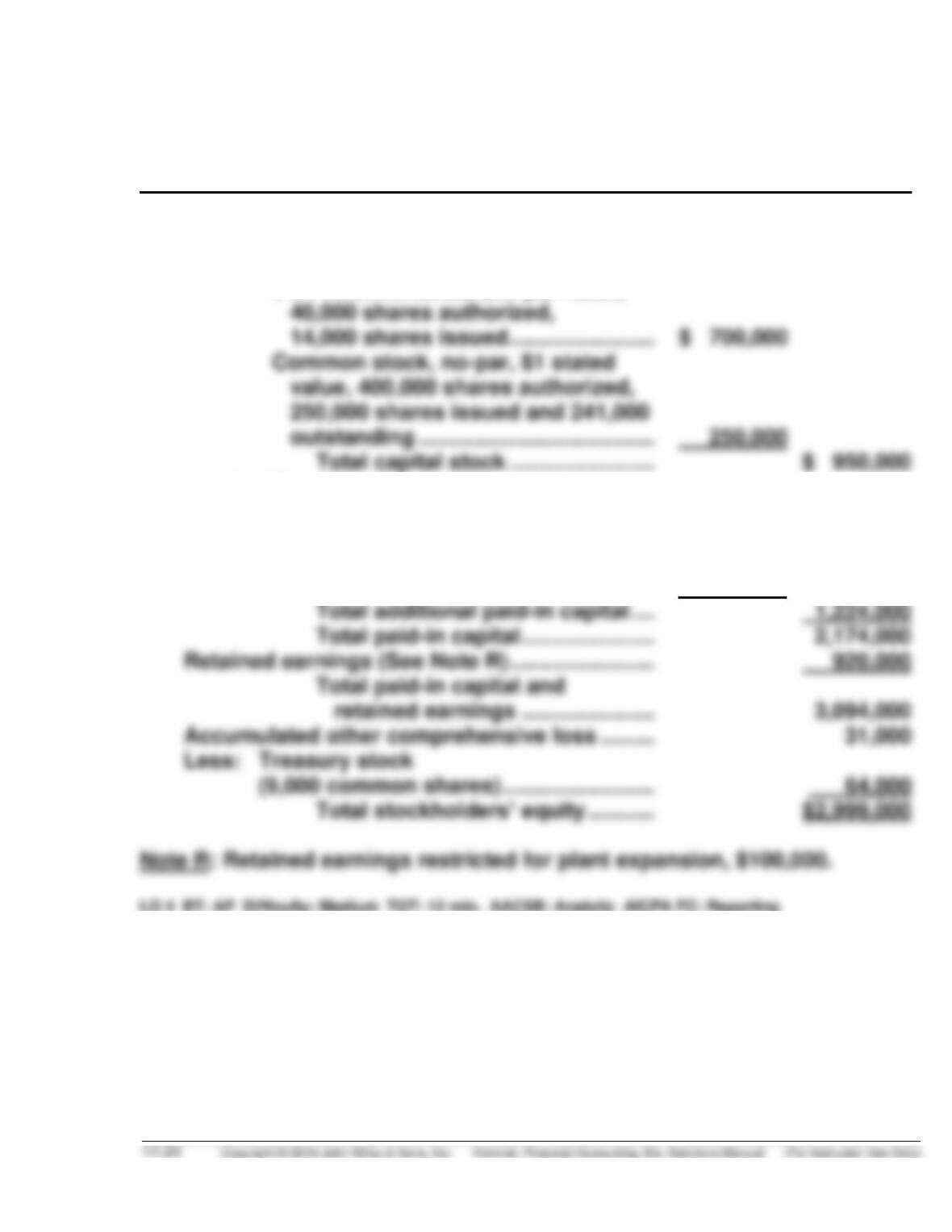

Capital stock

Preferred stock ………………………………………….. $8,485

Common stock,

$1 23

par value,

6 billion shares authorized,

EXERCISE 11-9

RYDER CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100 par

value, noncumulative,

6,000 shares issued ………………………. $ 600,000

Common stock, no par,

EXERCISE 11-10

PAISAN INC.

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $50 par value,

Additional paid-in capital

Paid-in capital in excess of par

value—preferred stock ………………… 24,000

Paid-in capital in excess of stated

value—common stock …………………. 1,200,000

EXERCISE 11-11

2017 2016

Payout ratio

$298

$504 = 59.1%

$611

$555 =110.1%

EXERCISE 11-12

2017 2016

Payout ratio

$471 = 23.5%

$2,006

394 = 18.3%

$2,157

EXERCISE 11-13

(a) 2017:

$182,000–$8,000 = 17.4%

$1,000,000

(b) Kojak Corporation’s net income increased in part because it retired bonds

and eliminated the interest expense associated with the bonds. Such an

(c) 2017:

$200,000 =16.7%

$1,200,000

EXERCISE 11-14

(a)

Plan One

Issue Stock

(b)

Plan Two

Issue Bonds

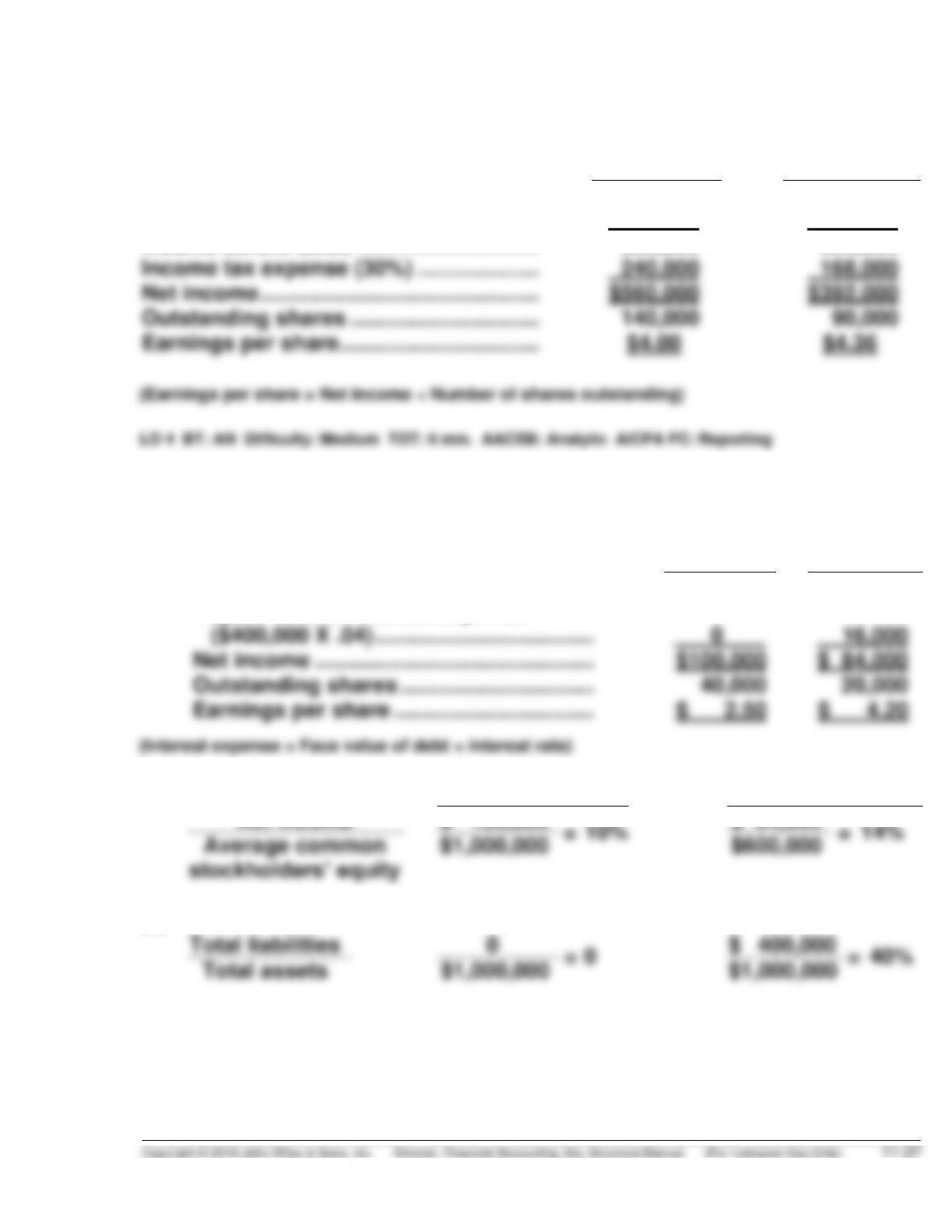

Income before interest and taxes ………

$800,000

$800,000

Interest ($2,000,000 X 12%) ……………….

240,000

Income before taxes …………………………

800,000

560,000

Income tax expense (30%) ………………..

240,000

168,000

Net income ……………………………………….

$560,000

$392,000

Outstanding shares ………………………….

140,000

90,000

Earnings per share …………………………...

EXERCISE 11-15

(a)

2016

2017

Pre-debt net income ………………………….

$100,000

$100,000

Net income ……………………………………….

$100,000

$ 84,000

Outstanding shares …………………………..

40,000

Earnings per share …………………………...

$ 2.50

Adjustment for interest expense

(b)

2016

2017

Net income

(c)

0

$1,000,000

EXERCISE 11-15 (Continued)

(d) The issuance of debt reduced the company’s net income because of

the interest cost that was incurred. However, the debt significantly

increased the company’s earnings per share because it was used to

acquire treasury stock. This reduced the number of outstanding shares,

thus increasing earnings per share.

*EXERCISE 11-16

(a) Stock Dividends (22,500* X $15) ……………………. 337,500

Common Stock Dividends

Distributable (22,500 X $10) …………………. 225,000

Paid-in Capital in Excess of Par Value—

Common Stock (22,500 X $5) ……………….. 112,500

SOLUTIONS TO PROBLEMS

PROBLEM 11-1A

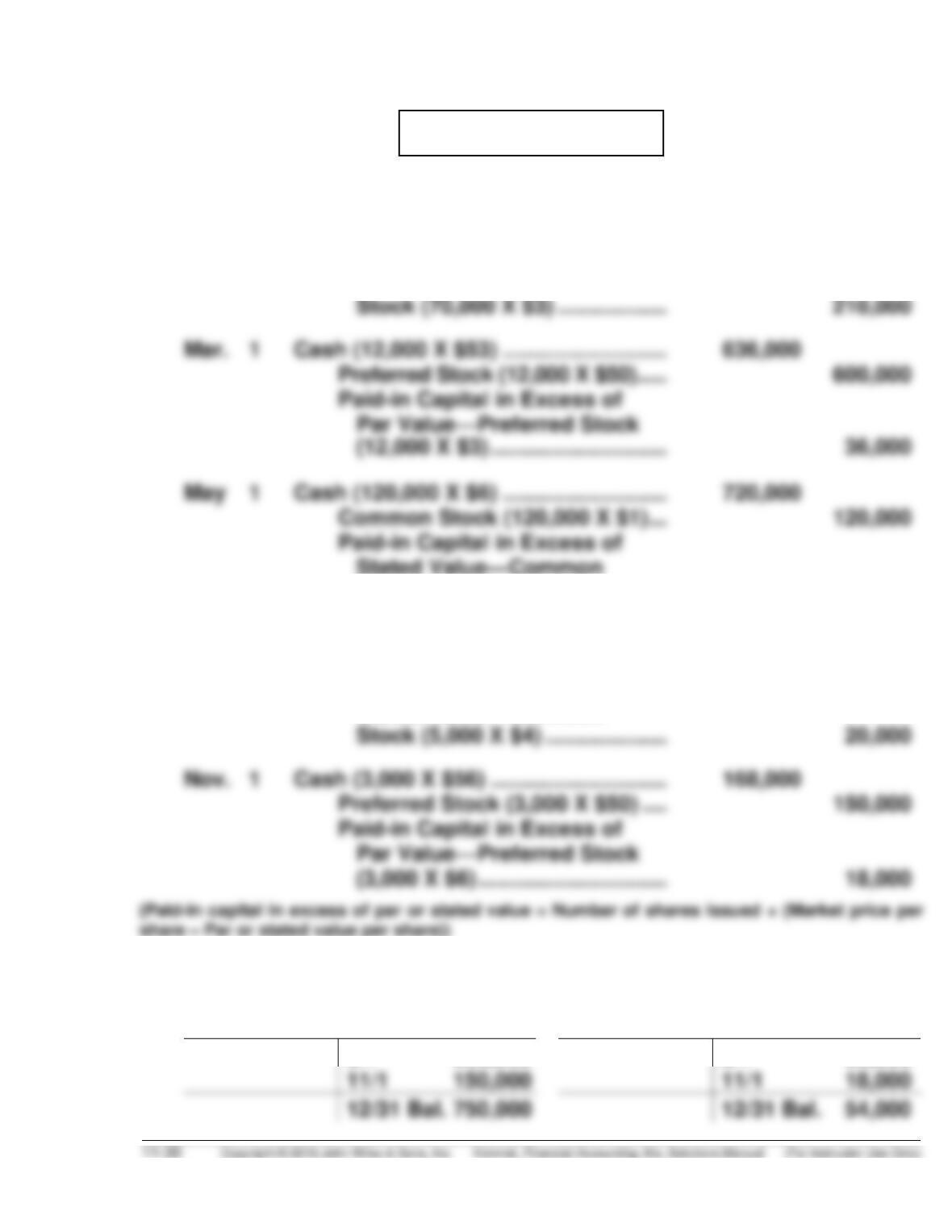

(a) Jan. 10 Cash (70,000 X $4) ……………………….. 280,000

Common Stock (70,000 X $1) ….. 70,000

Paid-in Capital in Excess of

Stated Value—Common

Stock (120,000 X $5) ……………. 600,000

Sept. 1 Cash (5,000 X $5) …………………………. 25,000

Common Stock (5,000 X $1) ……. 5,000

Paid-in Capital in Excess of

Stated Value—Common

(b)

Preferred Stock

Paid-in Capital in Excess of

Par Value—Preferred Stock

3/1 600,000

3/1 36,000

PROBLEM 11-1A (Continued)

Common Stock

Paid-in Capital in Excess of

Stated Value—Common Stock

1/10 70,000

1/10 210,000

5/1 120,000

5/1 600,000

9/1 5,000

9/1 20,000

12/31 Bal. 830,000

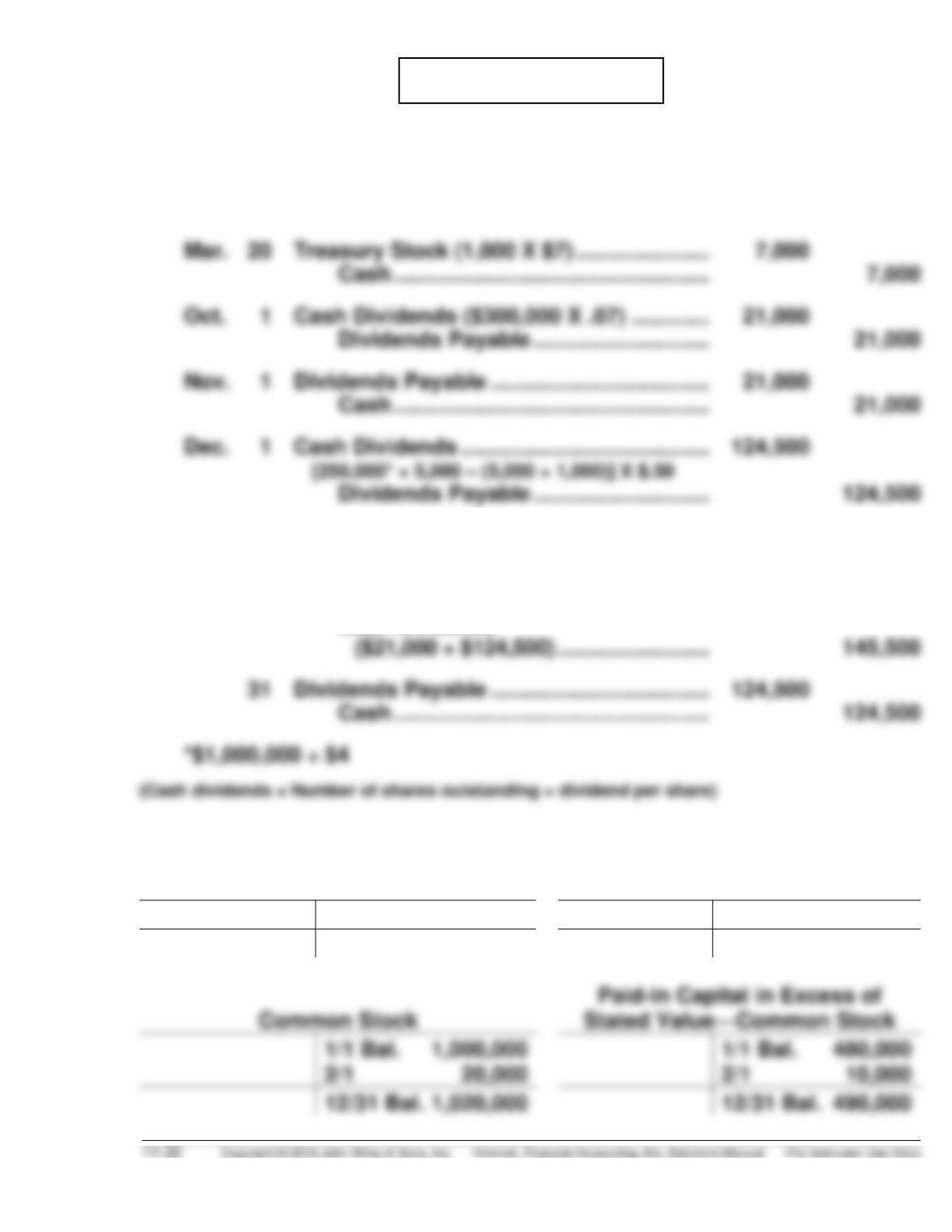

(c) TIDAL CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock, $50 par

value, 20,000 shares

authorized and 15,000

shares issued ………………………… $750,000

Common stock, no-par,

PROBLEM 11-2A

(a) Feb. 1 Cash ………………………………………………….. 30,000

Common Stock (5,000 X $4) ………….. 20,000

Paid-in Capital in Excess of

Stated Value—Common Stock …… 10,000

Dec. 31 Income Summary ……………………………….. 280,000

Retained Earnings ……………………….. 280,000

31 Retained Earnings ……………………………… 145,500

Cash Dividends

(b)

Preferred Stock

Paid-in Capital in Excess of

Par Value—Preferred Stock

1/1 Bal. 300,000

1/1 Bal. 15,000

12/31 Bal. 300,000

12/31 Bal. 15,000

1/1 Bal. 1,000,000

1/1 Bal. 480,000

PROBLEM 11-2A (Continued)

Retained Earnings

Treasury Stock

12/31 145,500

1/1 Bal. 688,000

1/1 Bal. 40,000

12/31 280,000

3/20 7,000

12/31 Bal. 822,500

12/31 Bal. 47,000

10/1 21,000

12/31 145,500

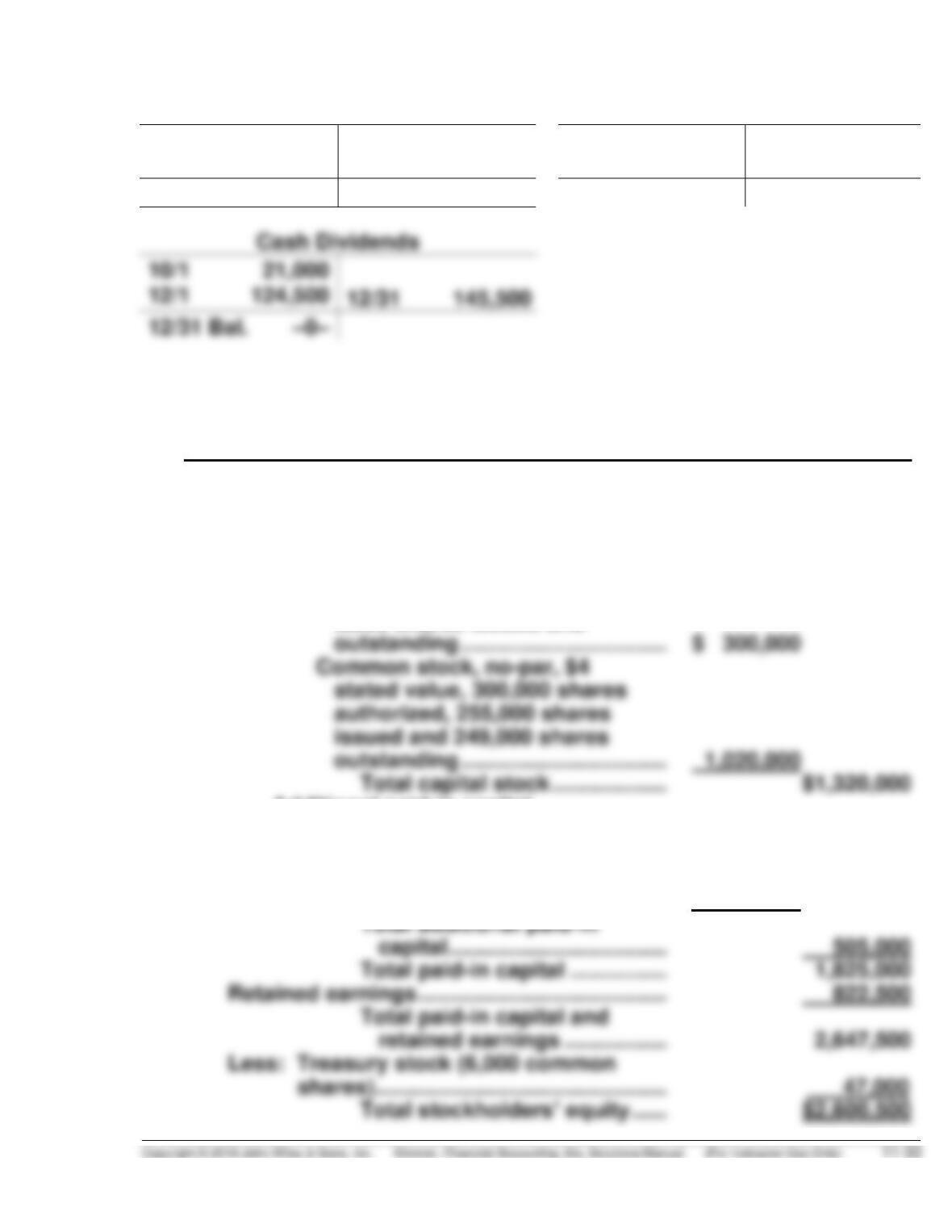

(c) CYRUS CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

7% Preferred stock, $100

par value, noncumulative,

5,000 shares authorized,

3,000 shares issued and

Additional paid-in capital

Paid-in capital in excess of par

value—preferred stock ………….. 15,000

Paid-in capital in excess of stated

value—common stock …………… 490,000

PROBLEM 11-2A (Continued)

(d)

$124,500

Payout ratio = = 44.5%

$280,000

$280,000 – $21,000 $259,000

Earnings per share = = = $1.05

(245,000* + 249,000* *) ÷ 2 247,000

PROBLEM 11-3A

JONS COMPANY

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

9% Preferred stock, $100 par value,

Additional paid-in capital

Paid-in capital in excess of par

value—preferred stock ………………… 840,000

Paid-in capital in excess of par

value—common stock …………………. 1,800,000

Total additional paid-in capital …. 2,640,000

PROBLEM 11-4A

(a)

Retained Earnings

Dec. 31 400,000

Jan. 1 Balance 2,380,000

Dec. 31 Balance 2,860,000

(b) WAITE CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100 par

value, noncumulative,

20,000 shares authorized,

10,000 shares issued and

outstanding ………………………………….. $1,000,000

Common stock, no-par, $5

stated value, 600,000 shares

authorized, 300,000 shares

issued and outstanding ………………… 1,500,000

PROBLEM 11-5A

(a) 1. Cash ……………………………………………………… 170,000

2. Cash ……………………………………………………… 3,520,000

3. Treasury Stock (4,000 X $9) ……………………. 36,000

PROBLEM 11-5A (Continued)

(b) LAYES CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

shares issued, and 396,000

shares outstanding ………………… 2,000,000

Total capital stock ………………. $2,150,000

Additional paid-in capital

Paid-in capital in excess of par

PROBLEM 11-6A

KIMBEL INC.

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Common stock, $1 par value, 2,000,000 shares

authorized, 710,000* shares issued, and

690,000 shares outstanding ……………………………… $ 710,000

Additional paid-in capital

PROBLEM 11-7A

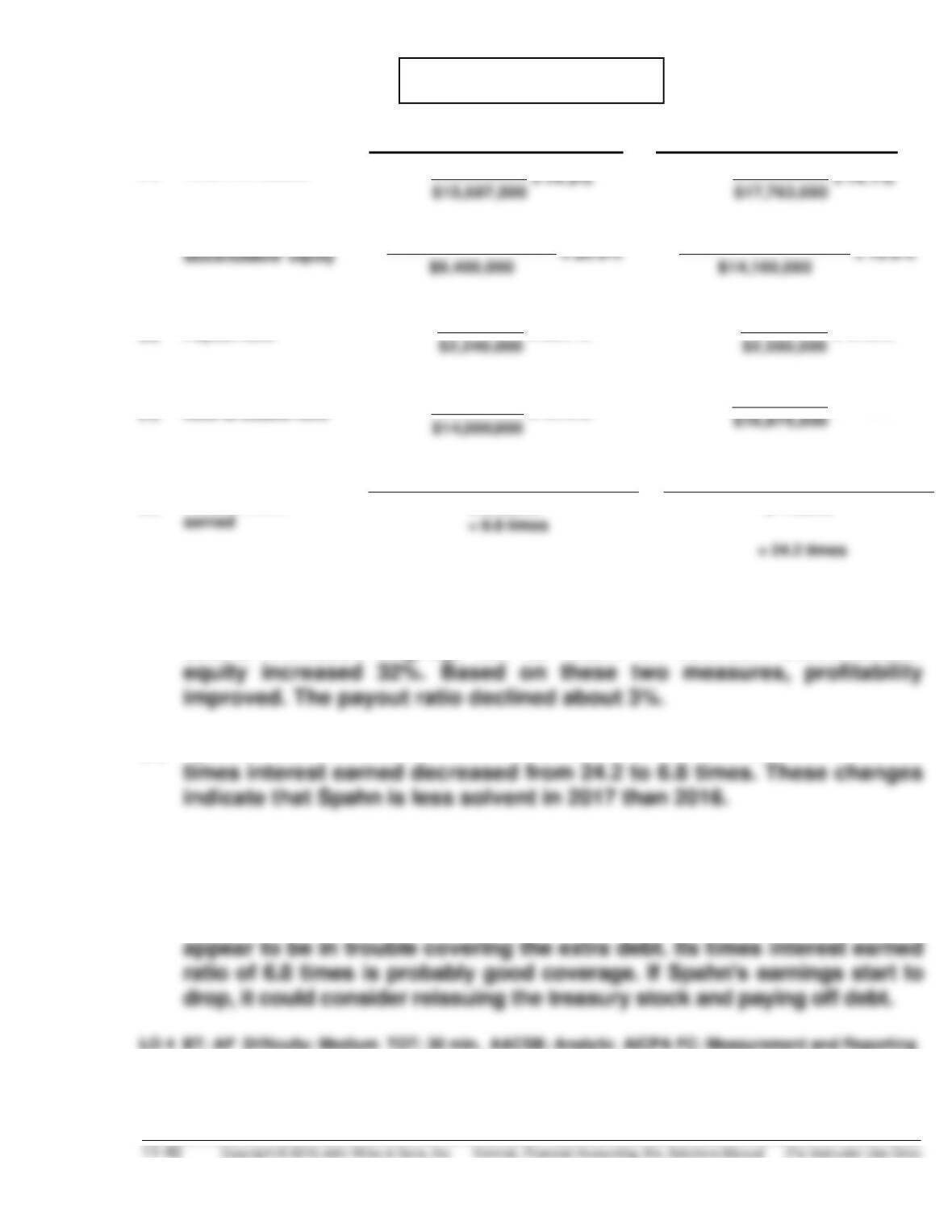

(a) 2017 2016

(1) Return on assets

$2,240,000 = 14.3%

$2,500,000 = 14.1%

(2) Return on common

$2,240,000 – $300,000 = 20.6%

$2,500,000 – $300,000 = 15.6%

(3) Payout ratio

$890,000 = 39.7%

$1,026,000 = 41.0%

(4) Debt to assets ratio

$6,000,000 = 41.4%

$3,000,000 = 17.8%

(5) Times interest

($2,240,000 + $500,000 + $670,000)

$500,000

($2,500,000 + $140,000 + $750,000)

$140,000

(b) Spahn’s net income declined from $2,500,000 to $2,240,000. Its return on

assets increased slightly, but its return on common stockholders’

(c) Spahn’s debt to assets ratio increased from 17.8% to 41.4% and its

(d) It appears that the decision to issue debt to purchase common stock

was wise. Spahn’s 10% interest rate was less than its return on assets of

14.3%. This resulted in the 32% increase in return on common stock-

holders’ equity. Although the solvency ratios declined, Spahn does not