CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN)

DIFFERENTIAL ANALYSIS AND PRODUCT PRICING

DISCUSSION QUESTIONS

1. a. Differential revenue is the amount of increase or decrease in revenue expected from a particular

course of action compared with an alternative.

b. Differential cost is the amount of increase or decrease in cost expected from a particular course

of action compared with an alternative.

c. Differential profit (loss) is the difference between differential revenue and differential cost.

3. If there is demand for the premium-grade product, the differential revenue (premium less commodity)

may exceed the differential cost to process the product to premium grade.

4. A company should only accept business at a special price if the lower price will not contaminate the

regular pricing for other customers or induce other customers to demand the special price. In

addition, the company must be careful not to violate the Robinson-Patman Act, which prohibits

uncompetitive price differences across different markets for the same product within the United

States. Lastly, the company must consider the longer-term ramifications of offering discount

business to a customer that may wish to order in the future.

7. In the long run, the normal selling price must be set high enough to cover all costs (both fixed and variable)

and provide a reasonable amount for profit.

8. In setting prices, managers should also consider such factors as the prices of competing products and

the general economic conditions of the marketplace.

10. The proper measure of product value in a bottlenecked process is the contribution margin per bottleneck

hour.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

BASIC EXERCISES

BE 25–1 (FIN MAN); BE 11–1 (MAN)

Differential Analysis

Lease (Alt. 1) or Sell (Alt. 2) Equipment

August 7

Lease

Equipment

(Alternative 1)

Sell

Equipment

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$320,000

$300,000

$(20,000)

* $300,000 × 4%

Plymouth Company should sell the equipment.

BE 25–2 (FIN MAN); BE 11–2 (MAN)

Differential Analysis

Continue (Alt. 1) or Discontinue (Alt. 2) Product Tango

February 13

Continue

Product Tango

(Alternative 1)

Discontinue

Product Tango

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$1,150,000

$ 0

$(1,150,000)

Costs:

Product Tango should be continued.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

BE 25–3 (FIN MAN); BE 11–3 (MAN)

Differential Analysis

Make (Alt. 1) or Buy (Alt. 2) Bottles

January 25

Make

Bottles

(Alternative 1)

Buy

Bottles

(Alternative 2)

Differential

Effects

(Alternative 2)

Unit costs:

BE 25–4 (FIN MAN); BE 11–4 (MAN)

Differential Analysis

Continue (Alt. 1) or Replace (Alt. 2) Old Machine

April 11

Continue

with Old

Machine

(Alternative 1)

Replace

Old

Machine

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues:

Proceeds from sale of old machine

$ 0

$ 50,500

$ 50,500

Direct labor (5 years)

$(61,500)

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

BE 25–5 (FIN MAN); BE 11–5 (MAN)

Differential Analysis

Sell Product J19 (Alt. 1) or Process Further into Product R33 (Alt. 2)

April 30

Sell

Product J19

(Alternative 1)

Process

Further into

Product R33

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues, per unit

$ 18

$ 24

$ 6

Costs, per unit

Profit (loss), per unit

The company should sell Product J19 without further processing.

BE 25–6 (FIN MAN); BE 11–6 (MAN)

Differential Analysis

Reject (Alt. 1) or Accept (Alt. 2) Order

March 16

Reject

Order

(Alternative 1)

Accept

Order

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues, per unit

$0.00

$ 7.20

$ 7.20

Costs:

(5.00)

(1.08)*

Profit (loss), per unit

$0.00

$ 1.12

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

BE 25–7 (FIN MAN); BE 11–7 (MAN)

Desired Profit + Selling and Admin. Exp.

Markup Percentage on Product Cost : Total Product Cost

$58 + $70 = 80%

$160 *

* $230 – $70

BE 25–8 (FIN MAN); BE 11–8 (MAN)

Product K

Product L

Unit contribution margin …………………………………………………

$120

$100

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

EXERCISES

Ex. 25–1 (FIN MAN); Ex. 11–1 (MAN)

a.

Differential Analysis

Lease (Alt. 1) or Sell (Alt. 2) Machinery

January 15

Lease

Machinery

(Alternative 1)

Sell

Machinery

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

Costs

b. Lease the machinery. The net gain from leasing is $6,400.

Ex. 25–2 (FIN MAN); Ex. 11–2 (MAN)

Note to Instructors: This differential analysis is a “lease or buy” decision, which is from

the user perspective. The “lease or sell” decision is from the perspective of the

equipment owner. Thus, the analysis is similar to the text examples but must be set up

from the user’s, rather than the owner’s, perspective.

Differential Analysis

Lease (Alt. 1) or Buy (Alt. 2) Equipment

March 15

Lease

Equipment

(Alternative 1)

Buy

Equipment

(Alternative 2)

Differential

Effects

(Alternative 2)

Costs:

The company should buy the equipment.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–3 (FIN MAN); Ex. 11–3 (MAN)

a.

Differential Analysis

Continue (Alt. 1) or Discontinue (Alt. 2) Mango Cola

February 29

Continue

Mango Cola

(Alternative 1)

Discontinue

Mango Cola

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$15,000,000

$ 0

$(15,000,000)

Costs:

Variable cost of goods sold

(7,560,000)1

0

7,560,000

Variable operating expenses

(6,000,000)2

0

6,000,000

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

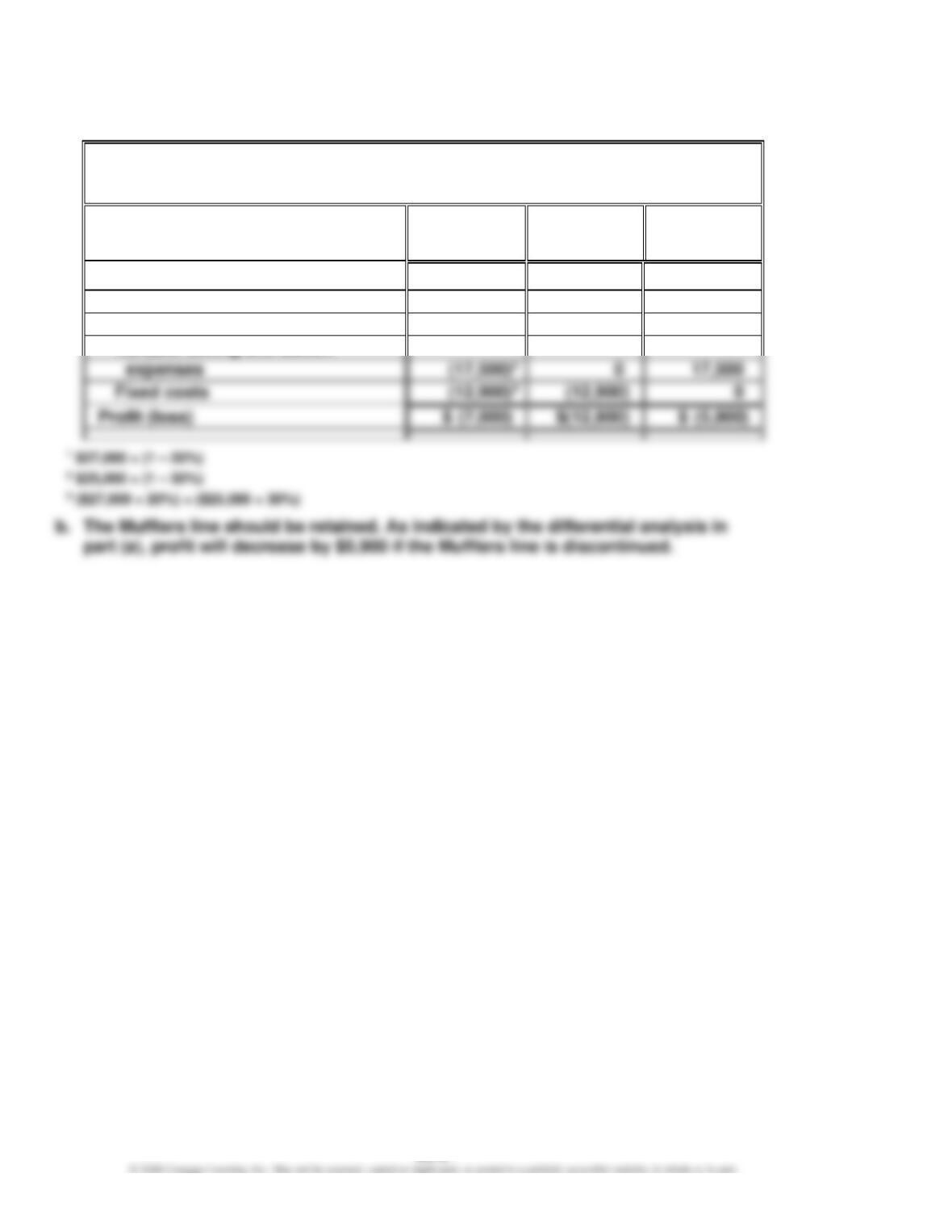

Ex. 25–4 (FIN MAN); Ex. 11–4 (MAN)

a.

Differential Analysis

Continue (Alt. 1) or Discontinue (Alt. 2) Mufflers

October 31

Continue

Mufflers

(Alternative 1)

Discontinue

Mufflers

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 45,000

$ 0

$(45,000)

Costs:

Variable cost of goods sold

(21,600)1

0

21,600

Variable selling and admin.

0

17,500

Fixed costs

(12,900)3

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–5 (FIN MAN); Ex. 11–5 (MAN)

Note to Instructors: Many students may be unfamiliar with the financial services industry.

This exercise provides an opportunity to introduce students to some basic terms and

concepts used within the industry.

a. The Investor Services segment serves the retail customer, you and me. These are

pension plan administrators.

b. Variable costs in the Investor Services segment include:

1. Commissions to brokers

2. Fees paid to exchanges for executing trades

c.

Investor

Services

(in millions)

Advisor

Services

(in millions)

Operating income ……………………………………………….

$2,031

$ 962

Depreciation ……………………………………………………….

180

54

Estimated contribution margin …………………………….

$2,211

$1,016

d. If one assumes that the fixed costs that serve advisor investors (computers, servers,

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–6 (FIN MAN); Ex. 11–6 (MAN)

The flaw in the decision is the failure to focus on the differential revenues and costs, which

indicate that operating income would be reduced by $45,000 if Children’s Shoes were

discontinued. This differential income from sales of Children’s Shoes can be determined

from the following differential analysis:

Differential Analysis

Continue (Alt. 1) or Discontinue (Alt. 2) Children’s Shoes

Continue

Children’s

Shoes

(Alternative 1)

Discontinue

Children’s

Shoes

(Alternative 2)

Differential

Effects

(Alternative 2)

* $45,000 + $30,000

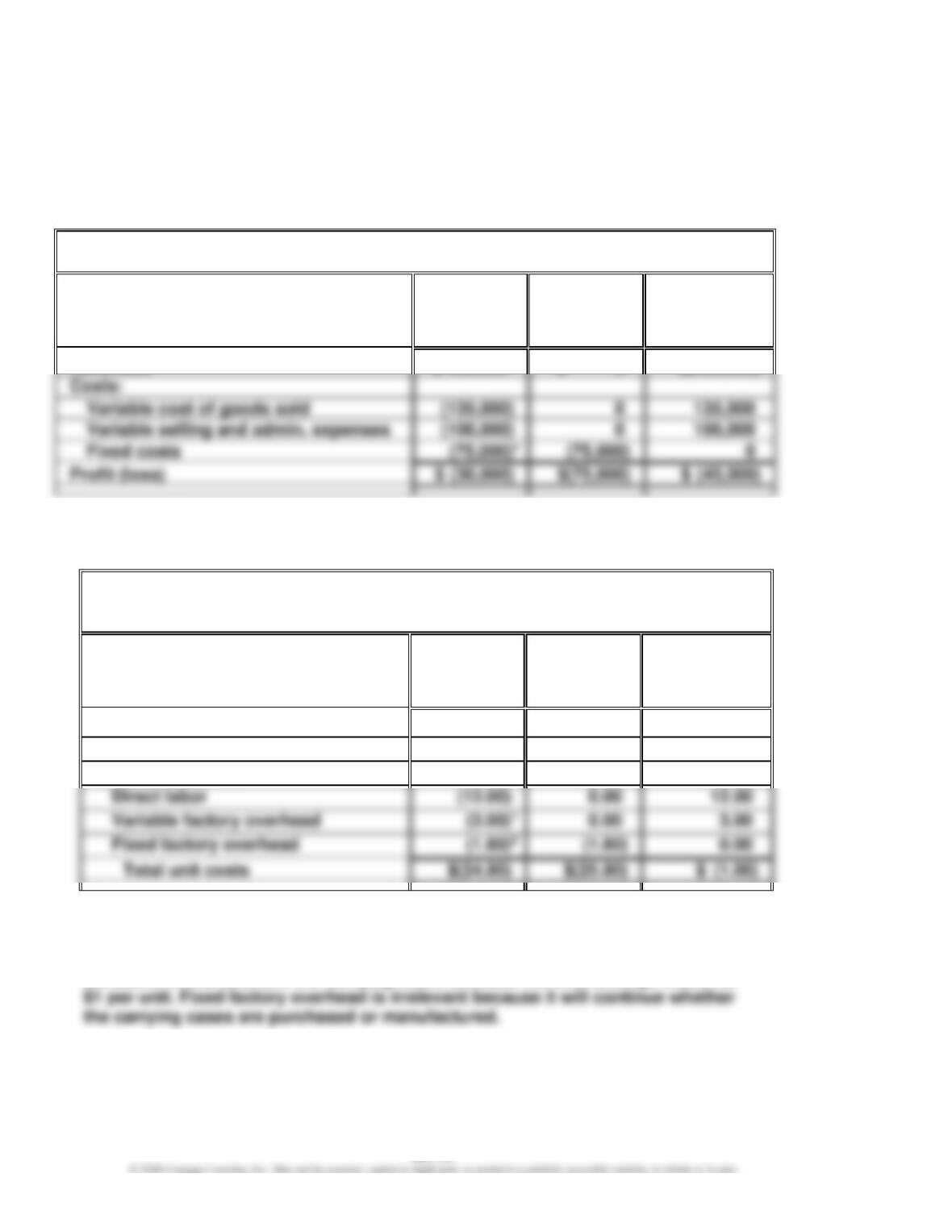

Ex. 25–7 (FIN MAN); Ex. 11–7 (MAN)

a.

Differential Analysis

Make (Alt. 1) or Buy (Alt. 2) Carrying Case

April 30

Make

Carrying

Case

(Alternative 1)

Buy

Carrying

Case

(Alternative 2)

Differential

Effects

(Alternative 2)

Unit costs:

Purchase price

$ 0.00

$(24.00)

$(24.00)

Direct materials

(8.00)

0.00

8.00

Direct labor

0.00

Variable factory overhead

0.00

3.00

1 $12.00 × 25%

2 $4.80 – $3.00

b. Assuming there were no better alternative uses for the spare capacity, it would be

advisable to manufacture the carrying cases because the cost savings would be

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–8 (FIN MAN); Ex. 11–8 (MAN)

a.

Differential Analysis

Lay Out Pages Internally (Alt. 1) or Purchase Layout Services (Alt. 2)

February 22

Lay Out

Pages

Internally

(Alternative 1)

Purchase

Layout

Services

(Alternative 2)

Differential

Effects

(Alternative 2)

Costs:

Purchase price of layout work

$ 0

$312,000*

$ 312,000

Salaries

224,000

0

(224,000)

Benefits

36,000

0

(36,000)

Supplies

21,000

0

(21,000)

Office expenses

39,000

0

(39,000)

Office depreciation

0

Computer depreciation

0

* 24,000 pages × $13 per page

b. The benefit from using an outside service is shown to be $8,000 greater than

performing the layout work internally. The fixed costs (depreciation expenses) in

the budget are irrelevant to the decision. Thus, the work should be purchased

from the outside on a strictly financial basis.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–9 (FIN MAN); Ex. 11–9 (MAN)

a.

Differential Analysis

Continue with (Alt. 1) or Replace (Alt. 2) Old Machine

May 29

Continue

with Old

Machine

(Alternative 1)

Replace

Old

Machine

(Alternative2)

Differential

Effects

(Alternative 2)

Revenues:

$ 250,000

Costs:

Variable production costs (8 years)

Proceeds from sale of old

The company should replace the old machine.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

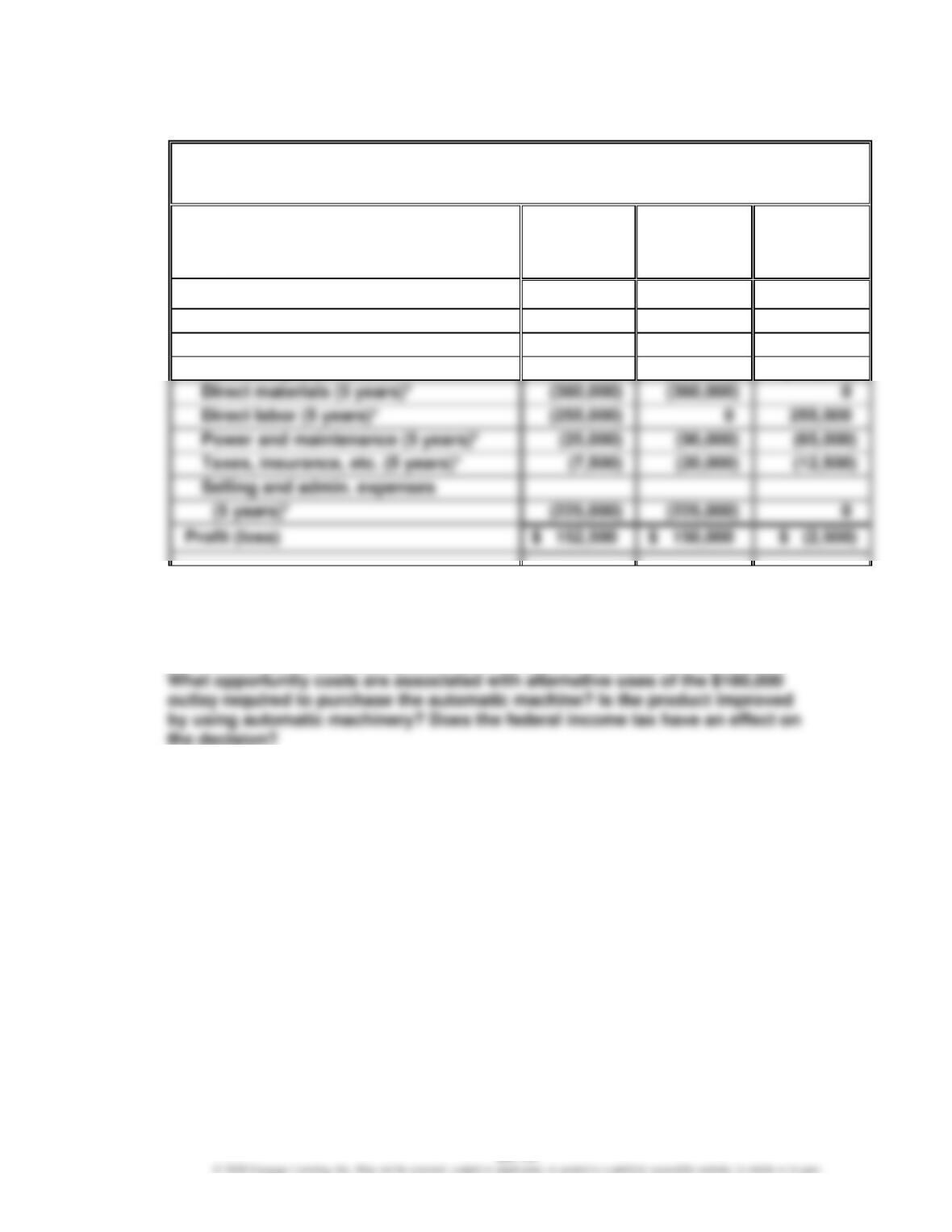

Ex. 25–10 (FIN MAN); Ex. 11–10 (MAN)

a.

Differential Analysis

Continue with (Alt. 1) or Replace (Alt. 2) Old Machine

May 4

Continue

with Old

Machine

(Alternative 1)

Replace Old

Machine

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues:

Sales (5 years)*

$1,025,000

$1,025,000

$ 0

Costs:

Purchase price

0

(180,000)

(180,000)

Direct materials (5 years)*

Direct labor (5 years)*

Power and maintenance (5 years)*

Selling and admin. expenses

(225,000)

* Each annual revenue and cost is multiplied by five years.

b. The proposal should not be accepted.

c. In addition to the factors given, consideration should be given to such factors

as: Do both present and proposed operations provide the same capacity?

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

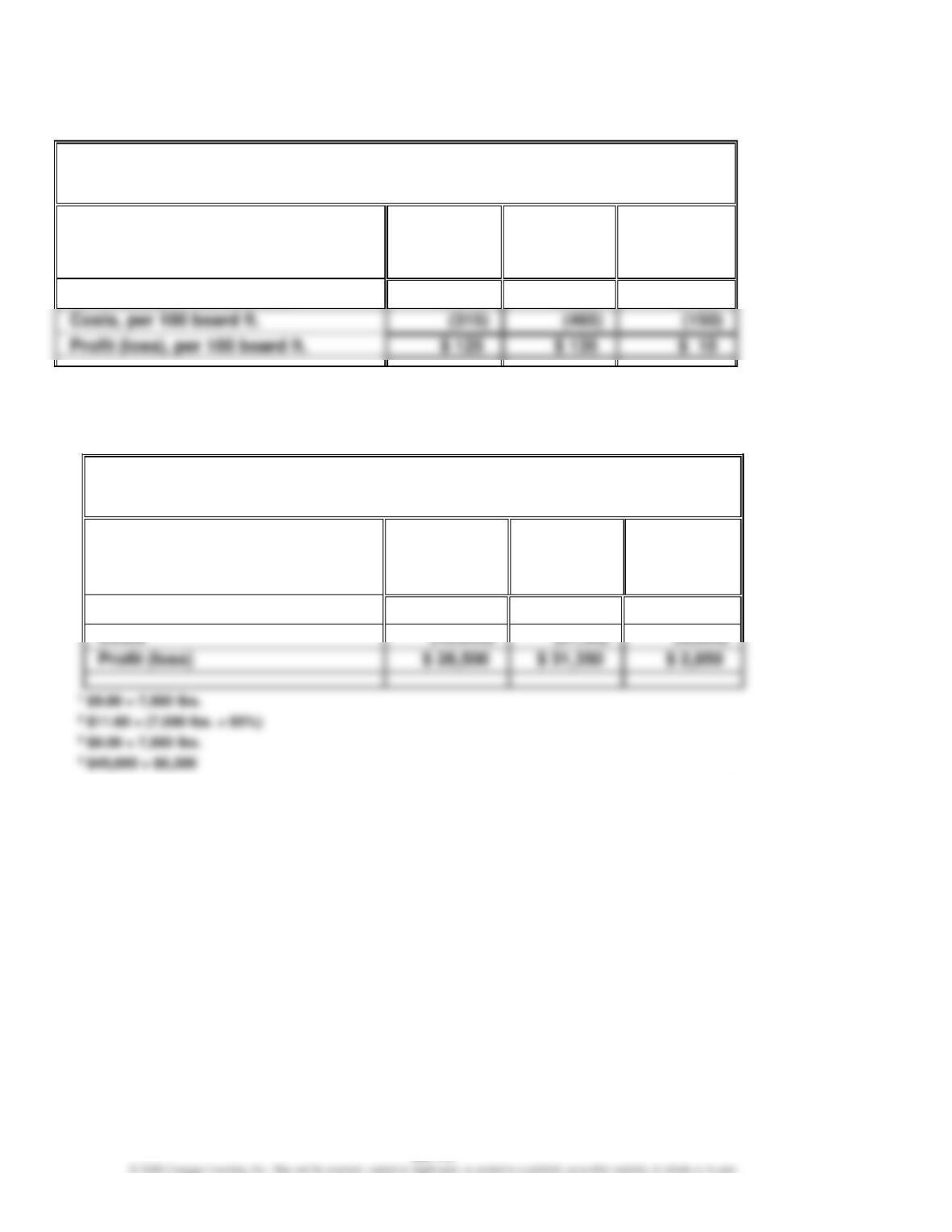

Ex. 25–11 (FIN MAN); Ex. 11–11 (MAN)

Differential Analysis

Sell Rough-Cut (Alt. 1) or Process Further into Finished-Cut (Alt. 2)

March 15

Sell

Rough-Cut

(Alternative 1)

Process

Further into

Finished-Cut

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues, per 100 board ft.

$ 440

$ 600

$ 160

Calgary Lumber Company should process further and sell finished-cut lumber.

Ex. 25–12 (FIN MAN); Ex. 11–12 (MAN)

a

Differential Analysis

Sell Regular (Alt. 1) or Process Further into Decaf (Alt. 2)

December 11

Sell

Regular

(Alternative 1)

Process

Further into

Decaf

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 73,5001

$ 82,6502

$ 9,150

b. The differential revenue from processing further to Decaf Columbian is $2,850. Thus,

Dakota Coffee Company should process further to Decaf Columbian.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–12 (FIN MAN); Ex. 11–12 (MAN) (Concluded)

c. The price of Decaf Columbian would need to decrease from $11.60 to $11.20 per

pound in order for the differential analysis to yield neither an advantage nor a

disadvantage (indifference). This is determined as follows:

The price of Decaf Columbian would need to be $0.40 lower, or $11.20, to yield no net

differential profit or loss. This is verified by the following differential analysis:

Differential Analysis

Sell Regular (Alt. 1) or Process Further into Decaf (Alt. 2)

December 11

Sell

Regular

(Alternative 1)

Process

Further into

Decaf

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 73,500

$ 79,800*

$ 6,300

Costs

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–13 (FIN MAN); Ex. 11–13 (MAN)

a.

Differential Analysis

Reject (Alt. 1) or Accept (Alt. 2) Order

November 12

Reject

Order

(Alternative 1)

Accept

Order

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$0

$ 576,0001

$ 576,000

Costs:

b. The additional units can be sold for $32 each, and because unused capacity is

available, the only costs that would be added if this additional production were

accepted are the variable costs of $29 per unit. The differential revenue is therefore

$32 per unit, and the differential cost is $29 per unit. Thus, the net profit is $3 per unit

× 18,000 units, or $54,000.

Ex. 25–14 (FIN MAN); Ex. 11–14 (MAN)

Total costs …………………………..………………………………………………………

$ 522,000

Fixed costs ………………………………………………………………………………….

(150,000)

Variable cost per unit:

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

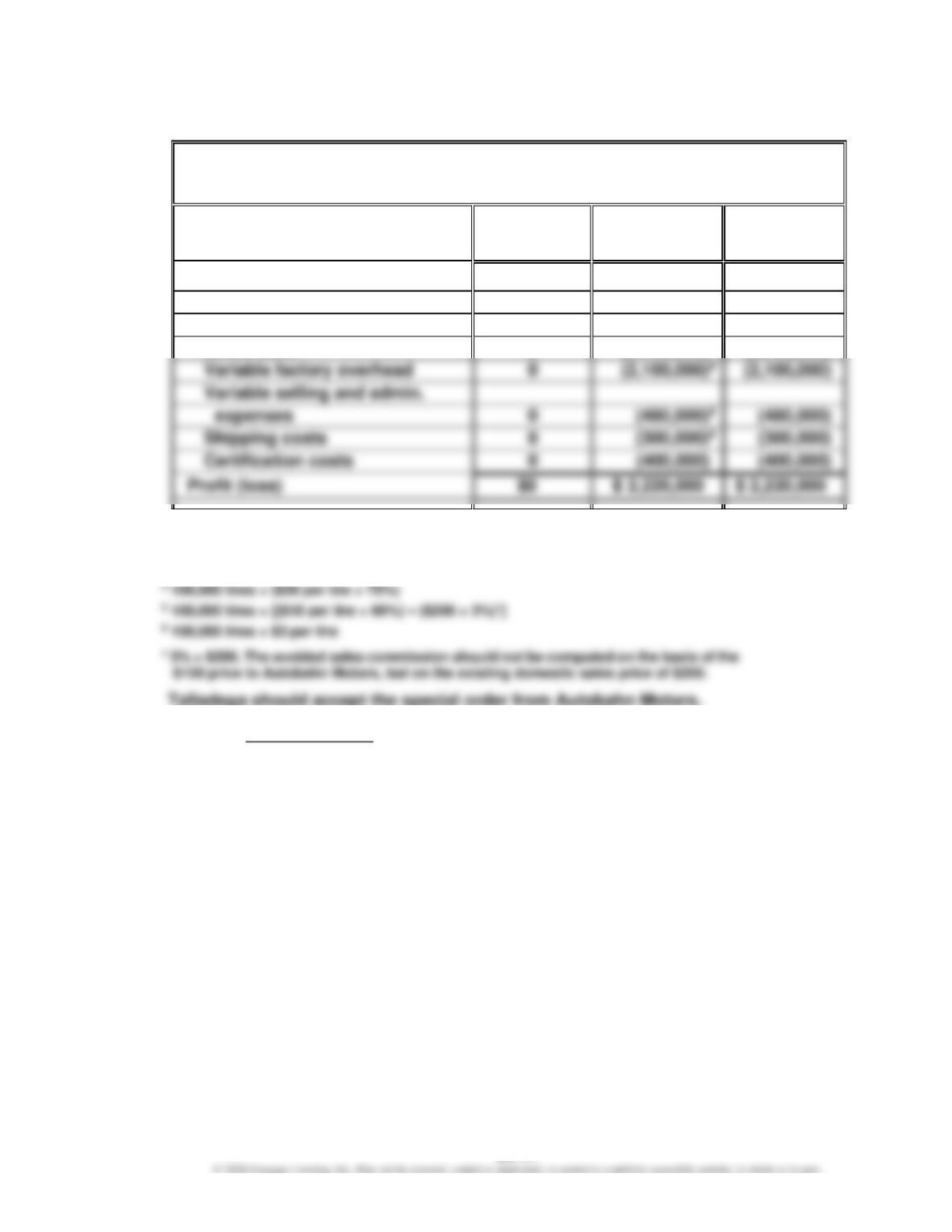

Ex. 25–15 (FIN MAN); Ex. 11–15 (MAN)

a.

Differential Analysis

Reject (Alt. 1) or Accept (Alt. 2) Order

July 31

Reject

Order

(Alternative 1)

Accept

Order

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$0

$15,000,0001

$15,000,000

Costs:

Direct materials

0

(7,500,000)2

(7,500,000)

Variable factory overhead

0

(2,100,000)4

(2,100,000)

Variable selling and admin.

0

Shipping costs

0

Certification costs

0

Direct labor

0

(2,000,000)3

(2,000,000)

1 100,000 tires × $150 per tire

2 100,000 tires × $75 per tire

3 100,000 tires × $20 per tire

Talladega should accept the special order from Autobahn Motors.

b.

$2,220,000

$150 – = $150.00 – $22.20 = $127.80

100,000

This is the price at which the differential profit would be zero.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–16 (FIN MAN); Ex. 11–16 (MAN)

a. Desired profit = $250,000 × 22% = $55,000

b. Cost amount (product cost) per unit: $32,000 ÷ 800 units = $40

d.

Cost amount (product cost) per unit ………………………………………………….

$ 40

Markup ($40 × 225%) …………………………………………………………………………

90

Selling price ……………………………………………………………………………………..

$130

Ex. 25–17 (FIN MAN); Ex. 11–17 (MAN)

a. Desired profit = $1,200,000 × 30% = $360,000

b. Cost amount (product cost) per unit: $2,500,000* ÷ 10,000 units = $250

* ($215 manufacturing variable cost per unit × 10,000 units) + $350,000 manufacturing fixed

cost

d.

Cost amount per unit ……………………………………………………………………….

$250

Markup ($250 × 30%) …………………………..……………………………………………

75

Selling price …………………………………………………………………………………….

$325

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–18 (FIN MAN); Ex. 11–18 (MAN)

b. The required profit margin of 20% of the estimated $27,000 selling price implies a

$21,600 target product cost as follows:

Target Product Cost

=

$27,000 – ($27,000 × 20%)

=

$27,000 – $5,400

=

$21,600

Because the estimated manufacturing cost of $22,500 exceeds the target cost of

$21,600, Toyota must reduce $900 from its total costs in order to maintain

competitive pricing within its profit objectives.

Note to Instructors: Target costing provides pressure to keep costs competitive. The

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–19 (FIN MAN); Ex. 11–19 (MAN)

a.

$460 – $230

Historical markup percentage on product cost : = 100%

$230

or,

$230 = 50% of selling price

$460

price)

b. Required cost reduction: $230 – $200 = $30

c. 1. Direct labor reduction:

$30 × 15 min. =

60 min.

$ 7.50

2. Additional inspection:

$30 × 6 min. =

60 min.

$ (3.00)

Direct material reduction: 20.00 17.00

3. Injection molding productivity improvement: