Information provided in the financial statements

Structure of a statement of financial position (balance sheet)

Non-current (fixed) assets

plus

Current assets

minus

Current liabilities

minus

…………………………………..……………..

equals

Ownership Interest

[………..…..……….

…..…………………….]

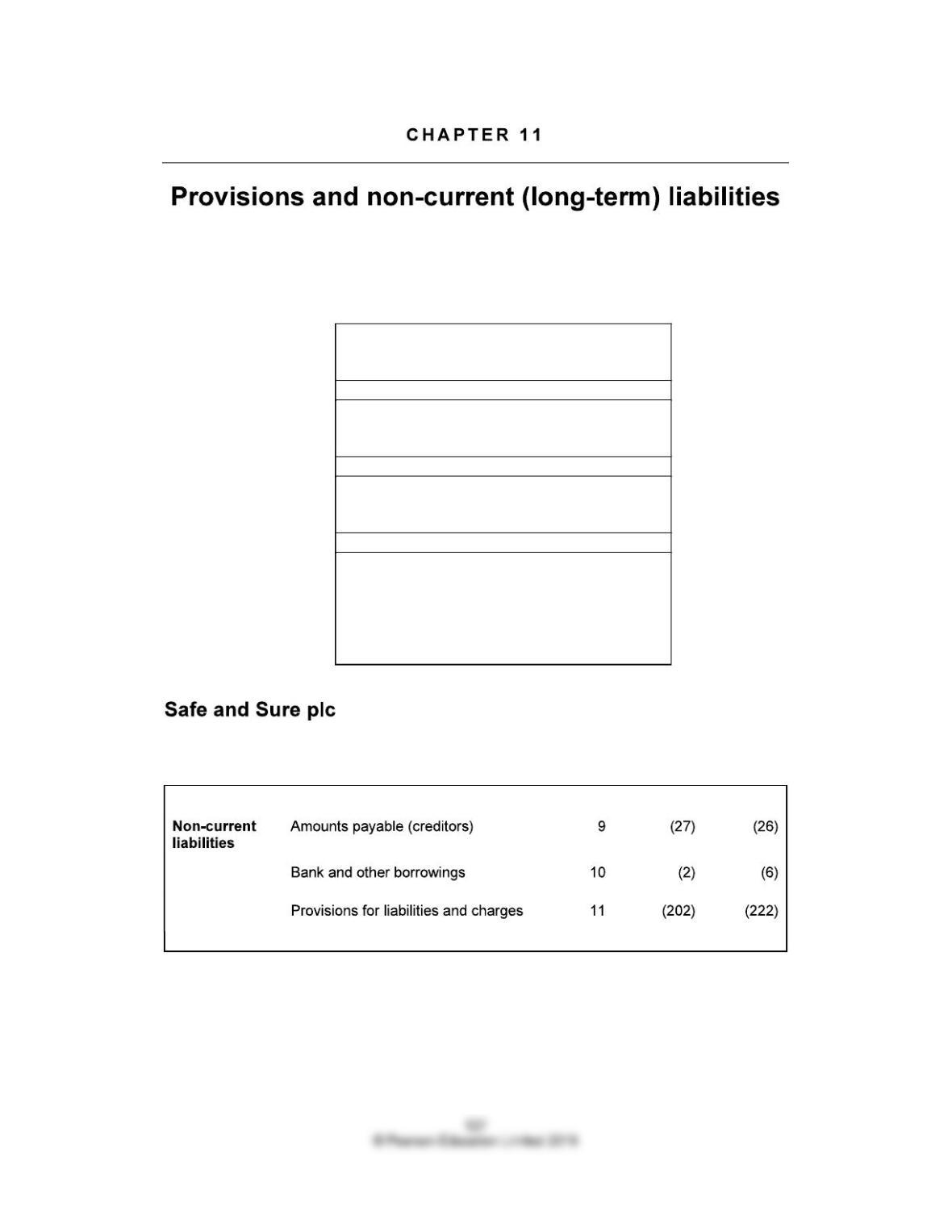

Statement of financial position (balance sheet) (Extract)

Notes Year 7 Year 6

Financial Accounting

A liability is a of the entity to transfer .as a result of

.

A current liability is a liability that satisfies any of the following criteria:

(a) It is expected to be settled in the entitys normal operating cycle.

(b) It is held primarily for the purpose of being traded.

(c) It is due to be settled within 12 months after the financial year-end date.

A non-current liability is any liability that .. meet the definition of a current

liability. Non-current liabilities are also described as .. liabilities.

Loan stock

Debentures

Bonds

Bank borrowing and commercial paper

Debentures: Loan made to the company: packaged in a legal form by which the claims against

the company can be bought and sold. Usually a .. rate of interest.

Bonds (US term) normally indicate that the funds have been borrowed from sources beyond the

UK. May be .. rates of interest.

Funds supplied by banks or other financial institutions (insurance company).

Usually . rate of interest.

How much was (the capital sum)?

How much is ...?

When it is ..?

Financial Accounting

What interest payments .?

Does the lender require .... for the loan?

A provision is a liability of .

Examples of provisions that may be found in the liabilities sections of published accounts are as

follows:

——————-—————————-—————–——————–

—————-—————————————————————–—

—————-—————————————————————–—

—————-—————————————————————–—

—————-—————————————————————–—

—————-—————————————————————–—

The ownership interest is reduced by an .. in the profit and loss account and a

.is created under the name of the provision.

Assets minus Liabilities equals Ownership interest

When the provision is no longer required, it is released to the profit and loss account as an item

of ..,which increases the ownership interest and the .. is reduced.

Assets minus Liabilities equals Ownership interest

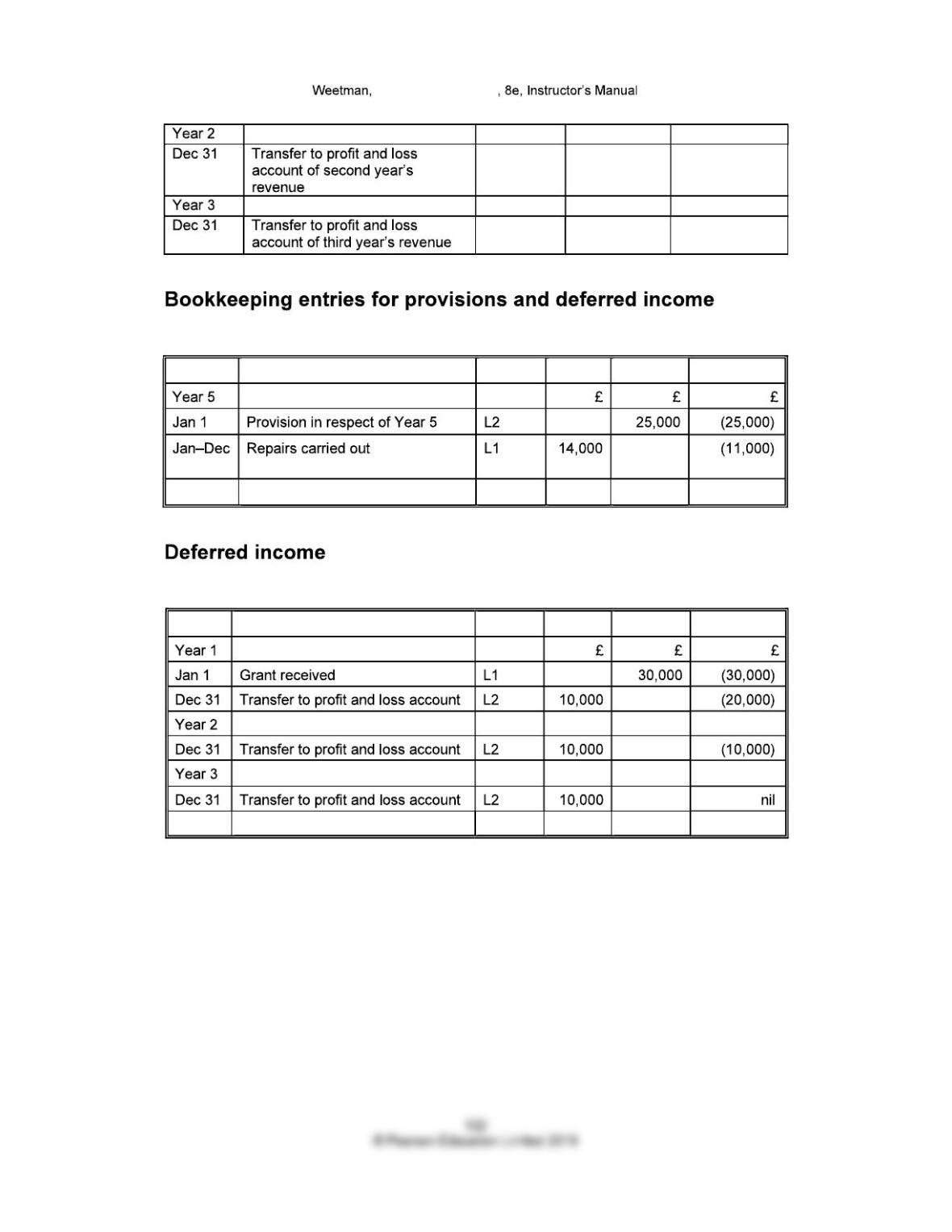

Example

During the year ending 31 December Year 5, a companys sales of manufactured goods

amounted to £1 million. All goods carry a manufacturers warranty to rectify any faults arising

during the first 12 months of ownership. Based on previous experience, a provision of 2½% of

sales was made.

During Year 5, repairs under warranty cost £14,000. Further repair costs incurred are expected

with respect to those items sold part-way through Year 5 whose warranty extends into Year 6.

Provision for warranties £1,000,000 × 2½% = £

When the provision is established:

Financial Accounting

As the repairs under warranty are carried out:

Spreadsheet for analysis of provision for warranty repairs

Date Transaction or event Asset Liability Ownership

interest

Cash Provision Profit and loss

account

Comment: Cost of repairs does not pass through profit and loss account. The provision is not yet

used up because the warranty is for 12 months, and some of the goods sold during Year 1 will

still be under warranty at the year end.

An amount received in a lump sum but related to activities over a .

..: the entity has not fully completed its side of the bargain. Costs still have to be

by the reporting entity. The . concept is

applied.

For example, a government grant to a company intended to help with the cost of training

employees over the next three years.

No, the benefit of the grant will extend over three years, and it would therefore seem appropriate

to spread the revenue over three years to match the cost it is subsidising.

Financial Accounting

Aim of matchingto the

. in the profit and loss account.

When grant received:

Each year covered by the grant, reduce liability and report a portion as income:

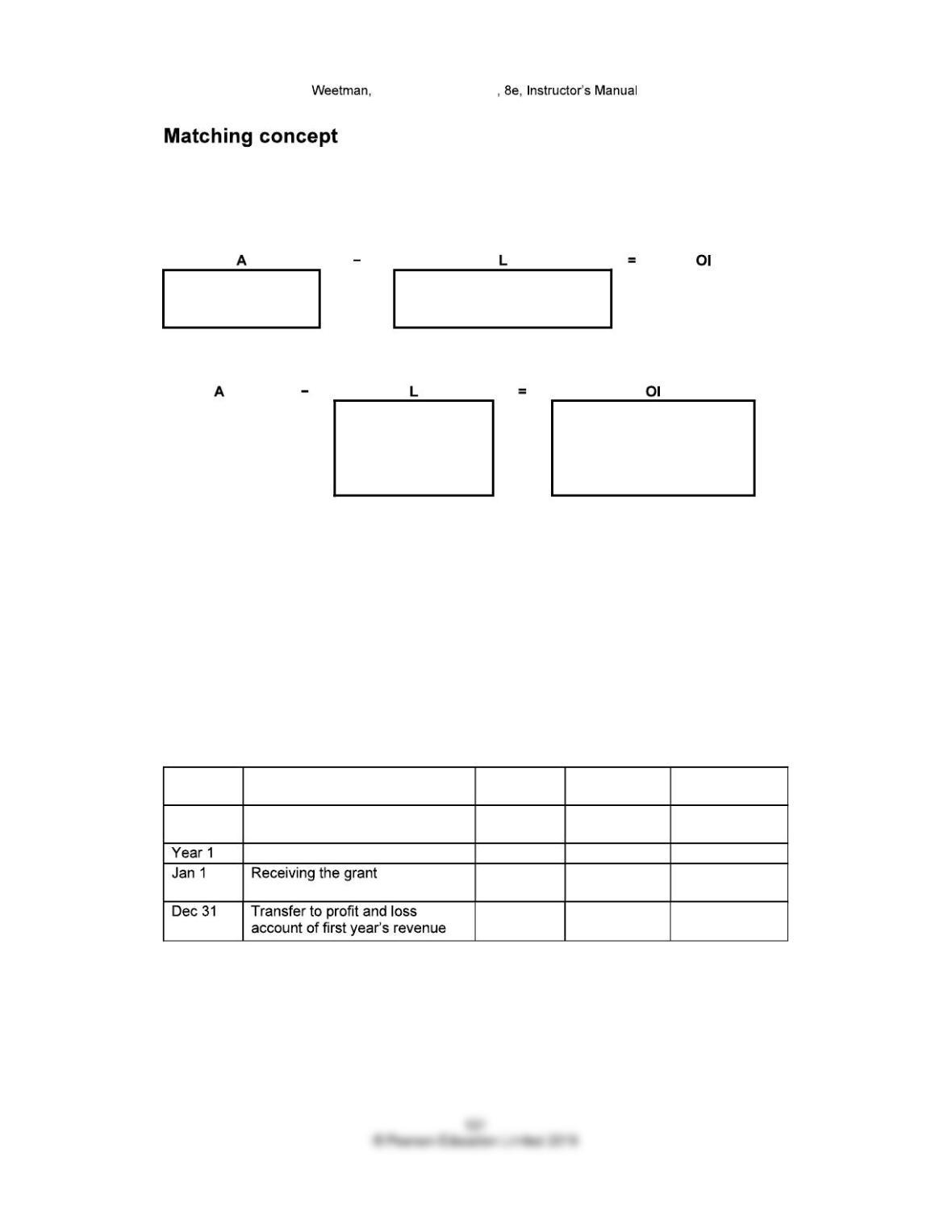

Example

A company receives a grant of £30,000 towards the cost of employee retraining. The retraining

programme will last for three years, and the costs will be spread evenly over the three years.

The aim is to spread the income over three years at a rate of £10,000 each year.

Record the liability of £ at the start and then reduce by £. each

year with transfer to profit and loss account, either as revenue or usually as a reduction in

employee costs.

Recording deferred income and transfer to revenue

Date Transaction or event Asset Liability Ownership

interest

Cash Deferred

income

Revenue

Financial Accounting

L3 Provision for warranty repairs

Date Particulars Page Debit Credit Balance

L3 Deferred income (statement of financial position)(balance sheet)

Date Particulars Page Debit Credit Balance