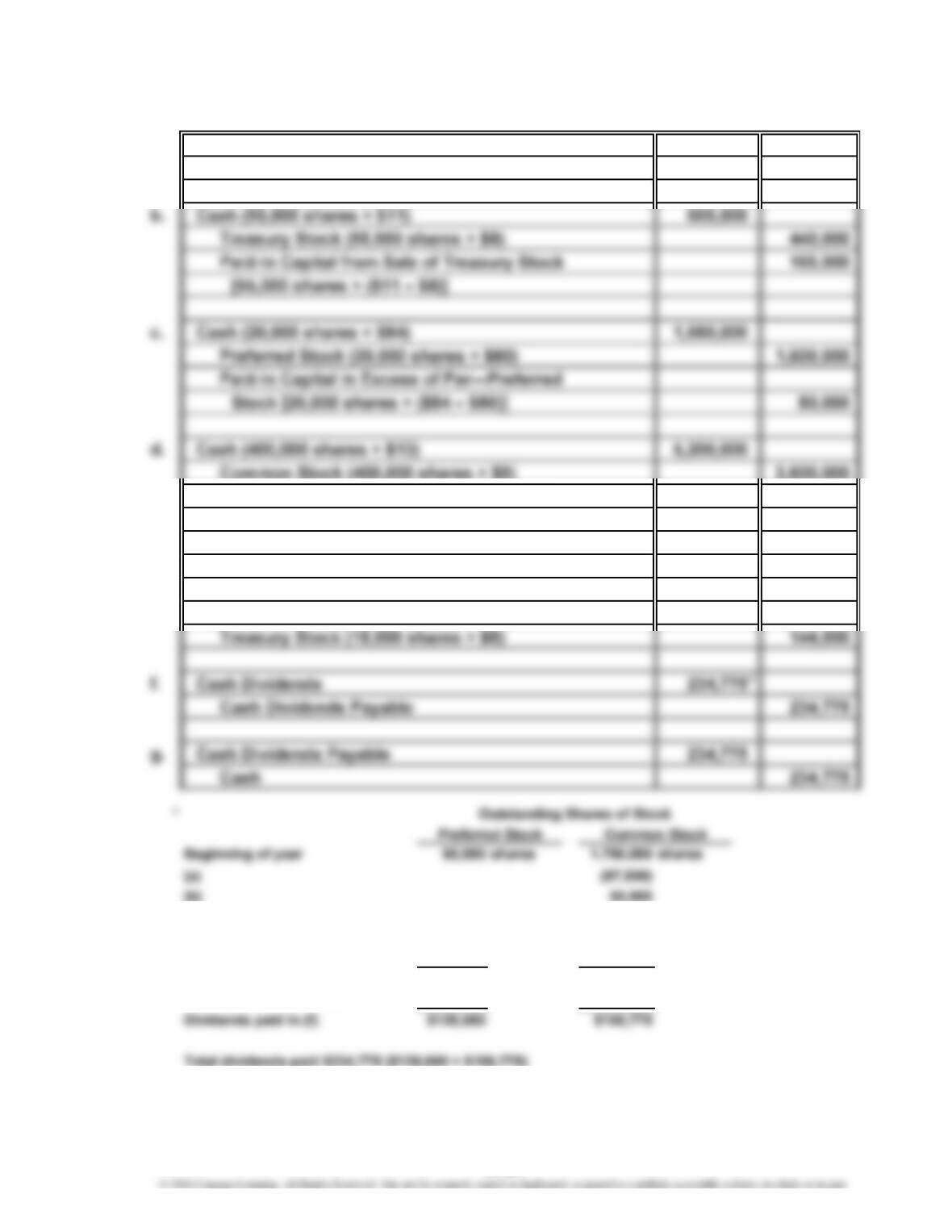

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Ex. 11–25

a. OfficeMax:

$34,894,000 – $2,123,000

85,881,000 shares

Earnings per Share

Net Income – Preferred Dividends

=

Avg. Number of Common Shares Outstanding

=

11-21

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–1A

1.

Total Per Per

Dividends Total Share Total Share

2011…………

…

$ 20,000 $20,000 $0.20 $ 0 $0.00

2012…………

…

36,000 36,000 $0.36 0 0.00

2. Average annual dividend for preferred: $0.30 per share ($1.80 ÷ 6)

Average annual dividend for common: $0.12 per share ($0.72 ÷ 6)

PROBLEMS

Year

Preferred Dividends Common Dividends

11-22

…

…

…

…

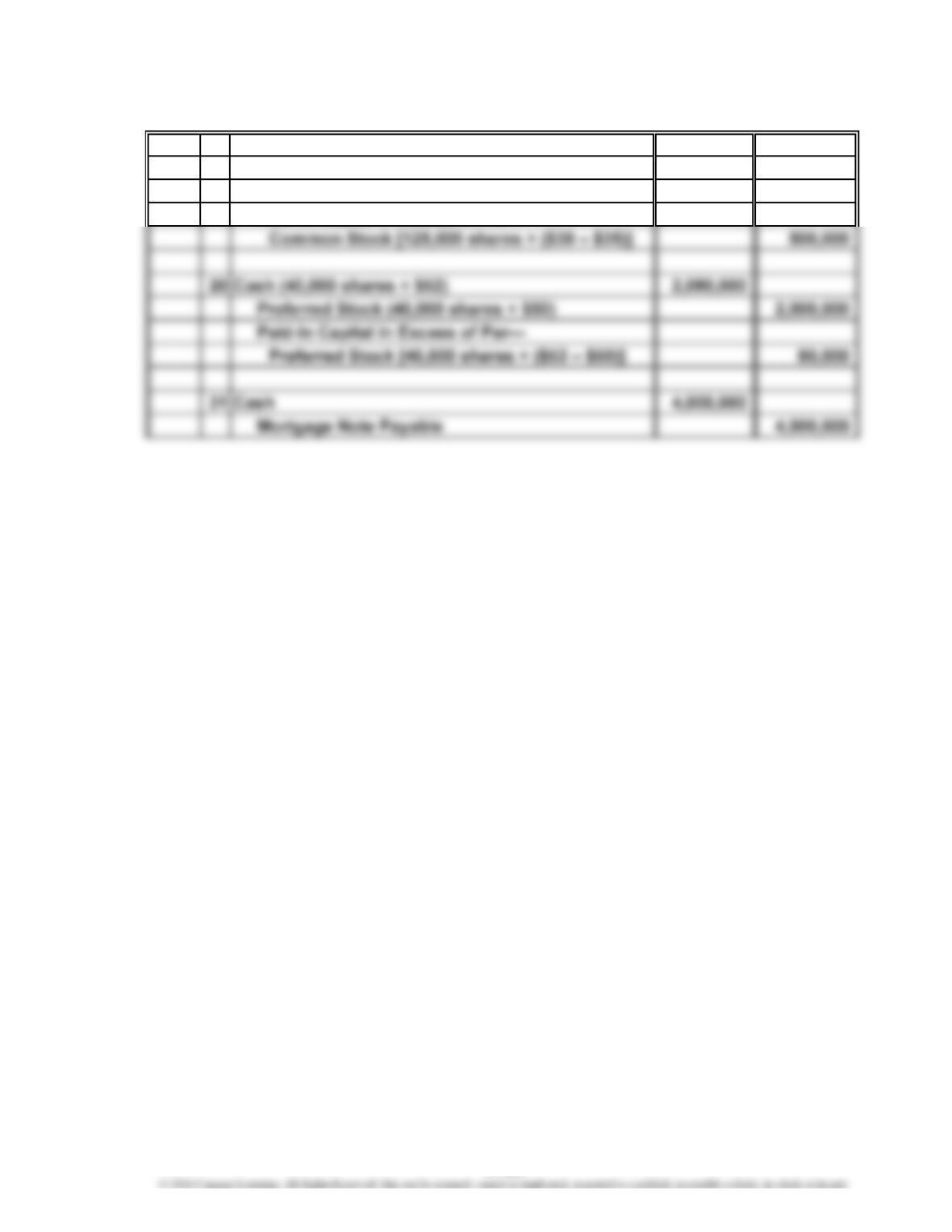

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

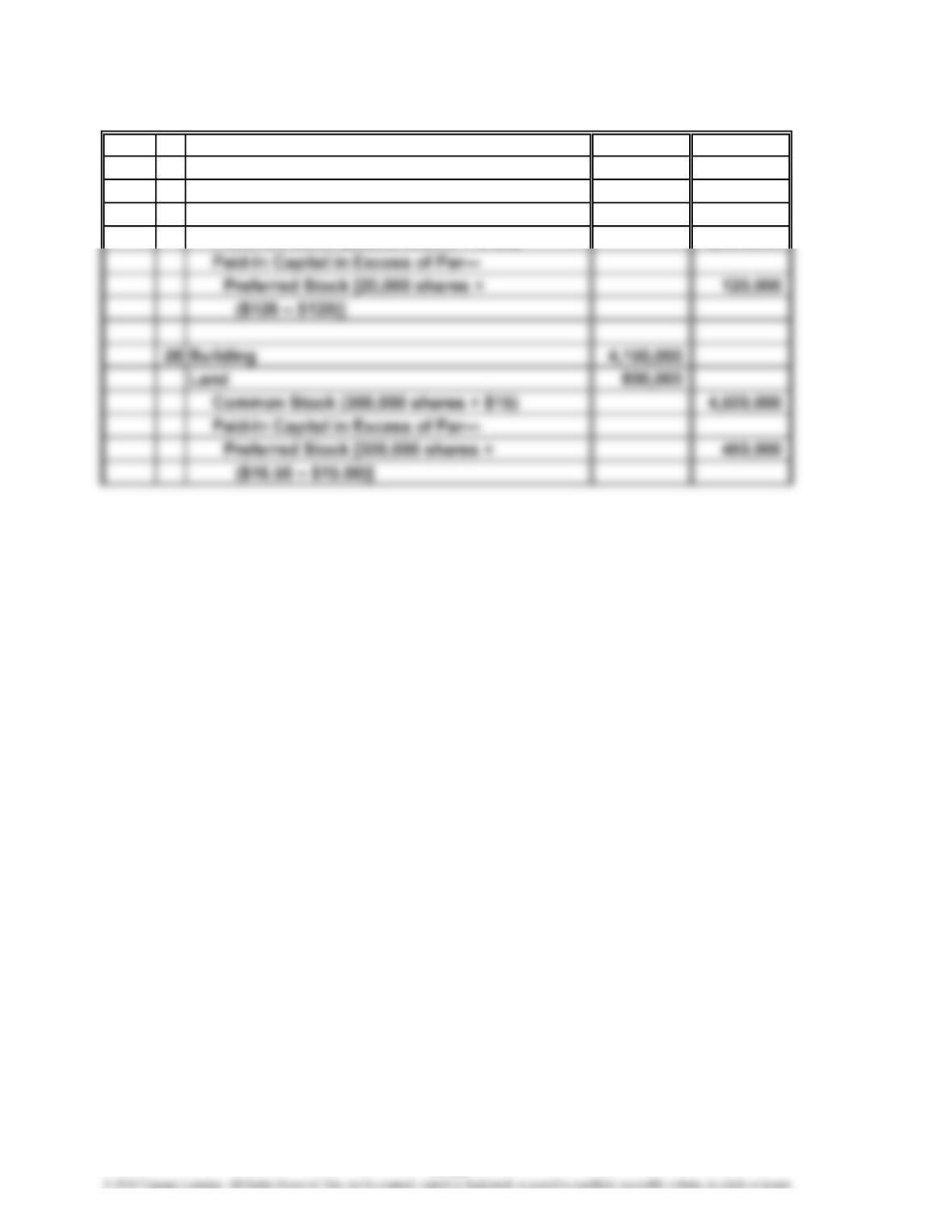

Prob. 11–2A

11 Building 3,375,000

Land 1,500,000

Common Stock (125,000 shares × $35) 4,375,000

Paid-In Capital in Excess of Par—

May

11-23

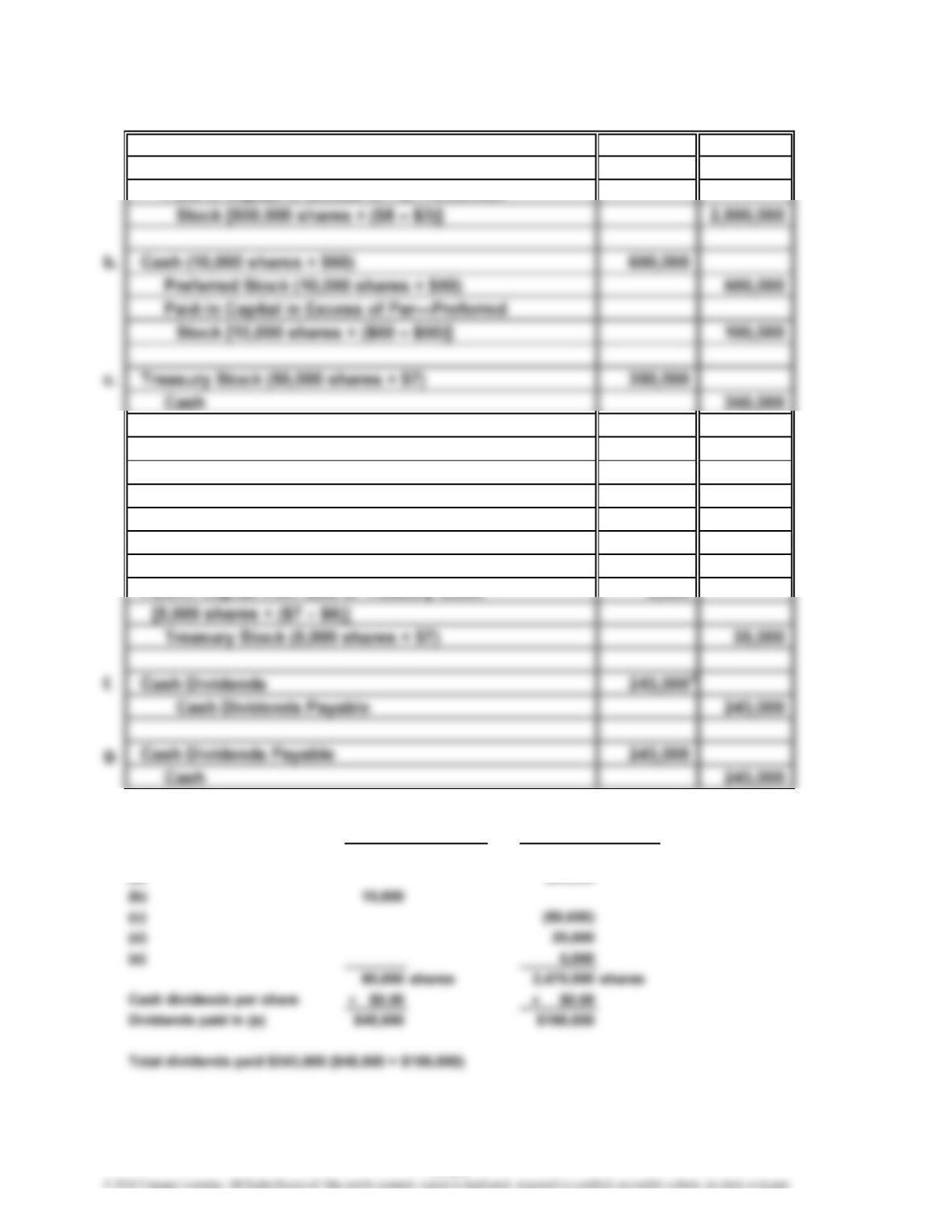

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–3A

a. Cash (500,000 shares × $8)

Common Stock (500,000 shares × $3) 1,500,000

Paid-In Capital in Excess of Par—Common

d. Cash (20,000 shares × $9)

Treasury Stock (20,000 shares × $7) 140,000

Paid-In Capital from Sale of Treasury Stock 40,000

[20,000 shares × ($9 – $7)]

e. Cash (5,000 shares × $6)

Paid-In Capital from Sale of Treasury Stock

*

Beginning of year 80,000 shares 2,000,000 shares

(a) 500,000

Outstanding Shares of Stock

180,000

30,000

5,000

Common StockPreferred Stock

4,000,000

11-24

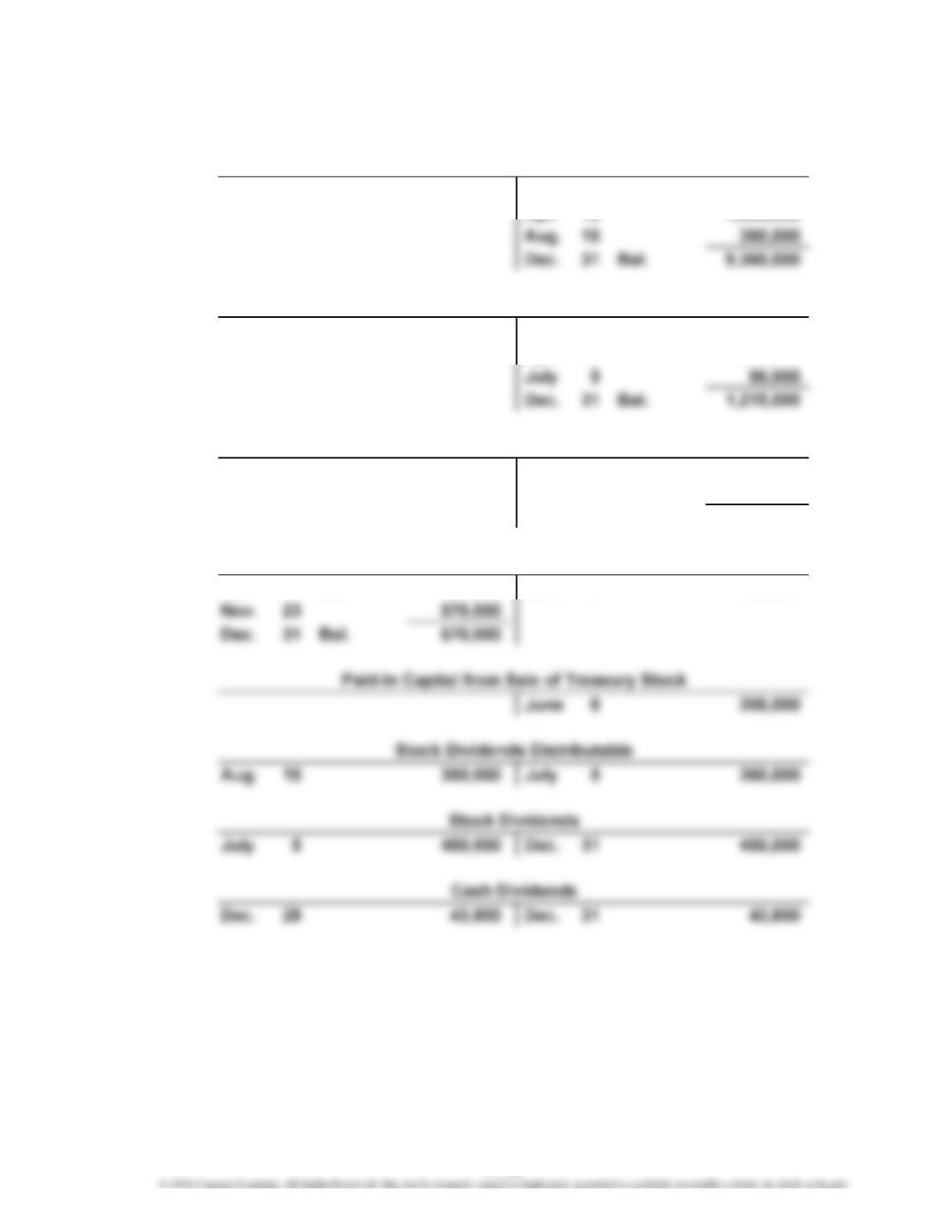

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4A

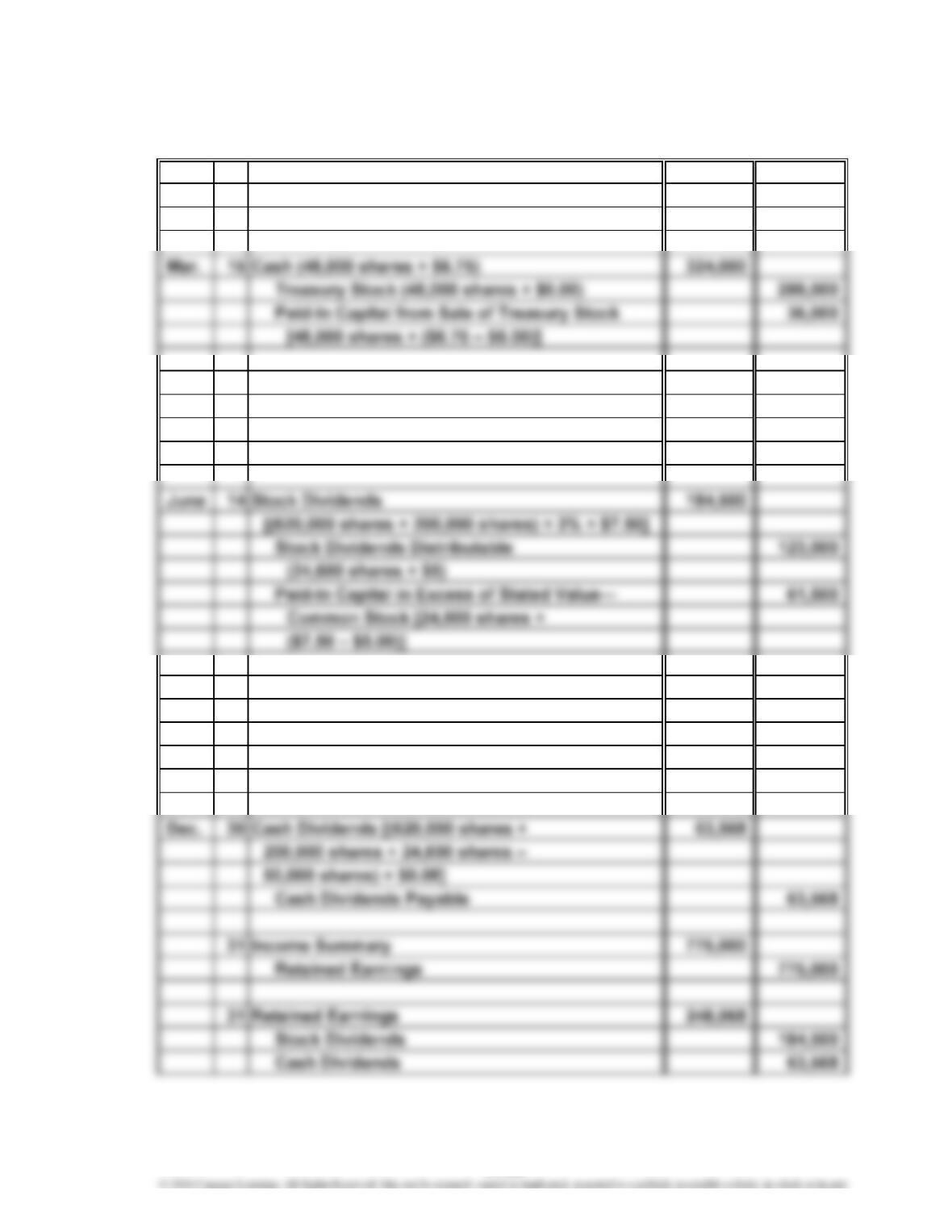

1. and 2.

Jan. 1 Bal. 7,500,000

Apr. 10 1,500,000

Jan. 1 Bal. 825,000

Apr. 10 300,000

Dec. 31 493,800 Jan. 1 Bal. 33,600,000

Dec. 31 1,125,000

Dec. 31 Bal. 34,231,200

Jan. 1 Bal. 450,000 June 6 450,000

Common Stock

Paid-In Capital in Excess of Stated Value—Common Stock

Retained Earnings

Treasury Stock

11-25

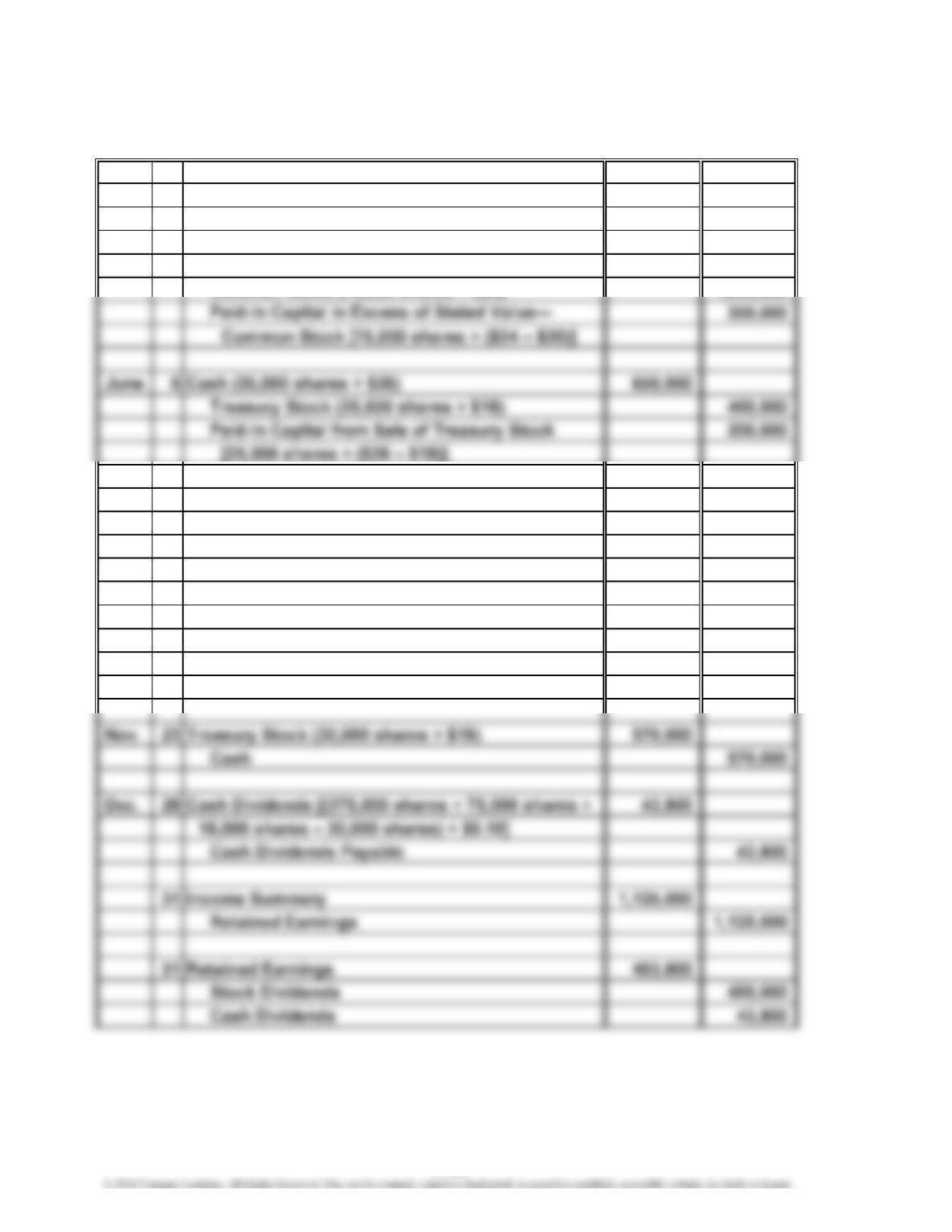

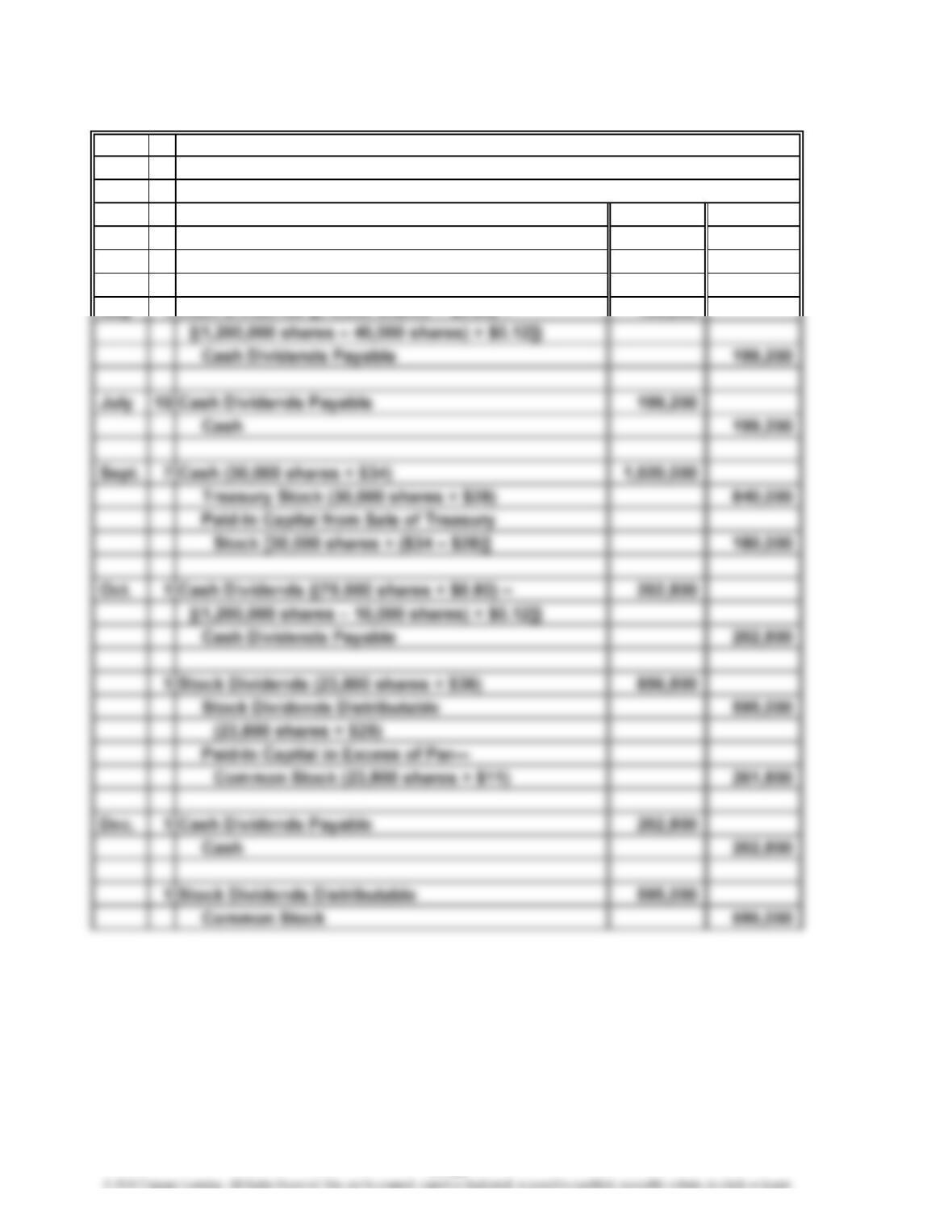

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4A (Continued)

2.

Jan. 22 Cash Dividends Payable 28,000

[(375,000 shares – 25,000 shares) × $0.08]

Cash 28,000

Apr. 10 Cash 1,800,000

Common Stock (75,000 shares × $20) 1,500,000

July 5 Stock Dividends [(375,000 shares + 450,000

75,000 shares) × 4% × $25]

Stock Dividends Distributable 360,000

(18,000 shares × $20)

Paid-In Capital in Excess of Stated Value— 90,000

Common Stock [18,000 shares × ($25 – $20)]

Aug. 15 Stock Dividends Distributable 360,000

Common Stock 360,000

11-26

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4A (Concluded)

3.

Retained earnings, January 1, 2016 $33,600,000

Net income $1,125,000

4.

Paid-in capital:

Common stock, $20 stated value (500,000 shares

authorized, 468,000 shares issued) $9,360,000

Stockholders’ Equity

MORROW ENTERPRISES INC.

Retained Earnings Statement

For the Year Ended December 31, 2016

11-27

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–5A

Jan. 9 No entry required. The stockholders’ ledger would be revised to

record the increased number of shares held by each stockholder

and new par value.

Feb. 28 Treasury Stock (40,000 shares × $28) 1,120,000

Cash 1,120,000

May 1 Cash Dividends {(75,000 shares × $0.80) + 199,200

11-28

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–1B

1.

Total Per Per

Dividends Total Share Total Share

2011………… $ 24,000 $ 24,000 $ 0.96 $0 $0.00

2012………… 10,000 10,000 0.40 0 0.00

*

$101,000 = (2011 dividends in arrears of $11,000) +

3. a. 1.8% ($1.80 ÷ $100)

Year

Preferred Dividends Common Dividends

11-29

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–2B

9 Cash 1,500,000

Mortgage Note Payable 1,500,000

17 Cash (20,000 shares × $126) 2,520,000

Preferred Stock (20,000 shares × $120) 2,400,000

Oct.

11-30

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–3B

a. Treasury Stock (87,500 shares × $8)

Cash 700,000

Paid-In Capital in Excess of Par—Common

Stock [400,000 shares × ($13 – $9)] 1,600,000

e. Cash (18,000 shares × $7.50)

Paid-In Capital from Sale of Treasury Stock

[18,000 shares × ($8.00 – $7.50)]

(c) 20,000

(d) 400,000

(e) 18,000

80,000 shares 2,135,500 shares

Cash dividends per share $1.60 $0.05

700,000

9,000

135,000

××

11-31

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4B

1. and 2.

Jan. 1 Bal. 3,100,000

Apr. 13 1,000,000

Dec. 31 248,068 Jan. 1 Bal. 4,875,000

Dec. 31 775,000

Dec. 31 Bal. 5,401,932

Common Stock

Retained Earnings

11-32

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4B (Continued)

2.

Jan. 15 Cash Dividends Payable 34,320

[(620,000 shares – 48,000 shares) × $0.06]

Cash 34,320

Apr. 13 Cash (200,000 shares × $8) 1,600,000

Common Stock (200,000 shares × $5) 1,000,000

Paid-In Capital in Excess of Stated Value— 600,000

Common Stock [200,000 shares × ($8 – $5)]

July 16 Stock Dividends Distributable 123,000

Common Stock 123,000

Oct. 30 Treasury Stock (50,000 shares × $6) 300,000

Cash 300,000

11-33

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–4B (Concluded)

Retained earnings, January 1, 2016 $4,875,000

Net income $ 775,000

4.

Paid-in capital:

Common stock, $5 stated value (900,000 shares

authorized, 844,600 shares issued) $4,223,000

Excess of issue price over stated value 1,901,500

Stockholders’ Equity

NAV-GO ENTERPRISES INC.

Retained Earnings Statement

For the Year Ended December 31, 2016

11-34

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

Prob. 11–5B

Jan. 15 No entry required. The stockholders’ ledger would be revised to record the

increased number of shares held by each stockholder and new par value.

Mar. 1 Cash Dividends [(100,000 shares × $0.25) + 81,000

(800,000 shares × $0.07)]

Cash Dividends Payable 81,000

Apr. 30 Cash Dividends Payable 81,000

Cash 81,000

11-35

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–1

At the time of this decision, the WorldCom board had come under intense scrutiny.

This was the largest loan by a company to its CEO in history. The SEC began an

investigation into this loan, and Bernie Ebbers was eventually terminated as the

CEO, with this loan being cited as part of the reason. The board indicated that

the decision to lend Ebbers this money was to keep him from selling his stock

and depressing the share price. Thus, it claimed that it was actually helping

Some press comments:

1. When he borrowed money personally, he used his WorldCom stock as

collateral. As these loans came due, he was unwilling to sell at “depressed

2. It was astonishing to read the other day that the board of directors of the

United States’ second-largest telecommunications company claims to have

had its shareholders’ interests in mind when it agreed to grant more than $430

million in low-interest loans to the company’s CEO, mainly to meet margin

CASES & PROJECTS

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–1 (Concluded)

best one by far—at least from the point of view of the shareholders—was to

CP 11–2

Lou and Shirley are behaving in a professional manner as long as full and

CP 11–3

1. This case involves a transaction in which a security has been issued that has

characteristics of both stock and debt. The primary argument for classifying

the issuance of the common stock as debt is that the investors have a legal

right to an amount equal to the purchase price (face value) of the security.

2. In practice, the $25 million stock issuance would probably be classified as

common stock. However, full disclosure should be made of the 5% of sales

and $120 per share payment obligations in the notes to the financial statements.

CP 11–4

a. 500 shares × ($1.12 ÷ 4) = $140

c. 45.2% = ($38.13 – $26.26) ÷ $26.26

CP 11–5

1. Before a cash dividend is declared, there must be sufficient retained earnings

and cash. On December 31, 2016, the retained earnings balance of $4,630,000

is available for use in declaring a dividend. This balance is sufficient for the

payment of the normal quarterly cash dividend of $0.50 per share, which would

3.5:1 ($7,000,000 ÷ $2,000,000) on December 31, 2016. However, after deducting

the $3,000,000 committed to store modernization and product-line expansion,

the ratio drops to 2:1 ($4,000,000 ÷ $2,000,000). If the cash dividend were

2. Given the cash and working capital position of Motion Designs Inc. on

CP 11–5 (Concluded)

a. From the point of view of a stockholder, the declaration of a stock

dividend would continue the dividend declaration trend of Motion Designs

Inc. In addition, although the amount of the stockholders’ equity and

CP 11–6

Note to Instructors: The purpose of this activity is to familiarize students with

1. Google Inc.

3. The following excerpts are taken from Google’s 10-K:

“Google is a global technology leader focused on improving the ways people

connect with information. We aspire to build products that improve the lives

11-39

CHAPTER 11 Corporations: Organization, Stock Transactions, and Dividends

CP 11–6 (Concluded)

4. $93,798,000,000

6. $10,737,000,000

$0.001; no shares issued or outstanding

9,000,000,000 authorized shares of Class A common stock with a par value of

$0.001; outstanding shares of 62,530,474

3,000,000,000 authorized shares of Class C common stock with a par value of

$0.001; no shares issued or outstanding

Classes A, B, and C have the same rights except for voting. Class A stock has

one vote per share; Class B stock has 10 votes per share; Class C stock has no

9. $682.33 – $1,068.00; as of November 29, 2013

10. Google Inc. does not pay cash dividends. In its SEC 10-K filing for the year ending

December 31, 2012, Google states:

“We have never declared or paid any cash dividend on our common stock. We

intend to retain any future earnings and do not expect to pay any cash dividends