CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–20 (FIN MAN); Ex. 11–20 (MAN)

Determine the contribution margin per furnace hour as follows:

Type 5

Type 10

Type 20

Revenues ………………………………….

$ 43,000

$ 49,000

$ 56,500

Variable cost ……………………………..

(34,000)

(28,000)

(26,500)

Contribution margin …………………..

$ 21,000

$ 30,000

Unit contribution margin …………….

$ 4.20

$ 6.00

Unit contribution margin

$ 0.70

$ 0.50

* Calculated as follows:

Type 5:

$1.80 = $0.30 per furnace hour

6hours

$4.20 = $0.70 per furnace hour

6hours

$6.00 = $0.50 per furnace hour

12hours

Emphasize Type 10. In a production-constrained environment, Type 10 generates the

most unit contribution margin per hour of furnace resource and, thus, is the most

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Ex. 25–21 (FIN MAN); Ex. 11–21 (MAN)

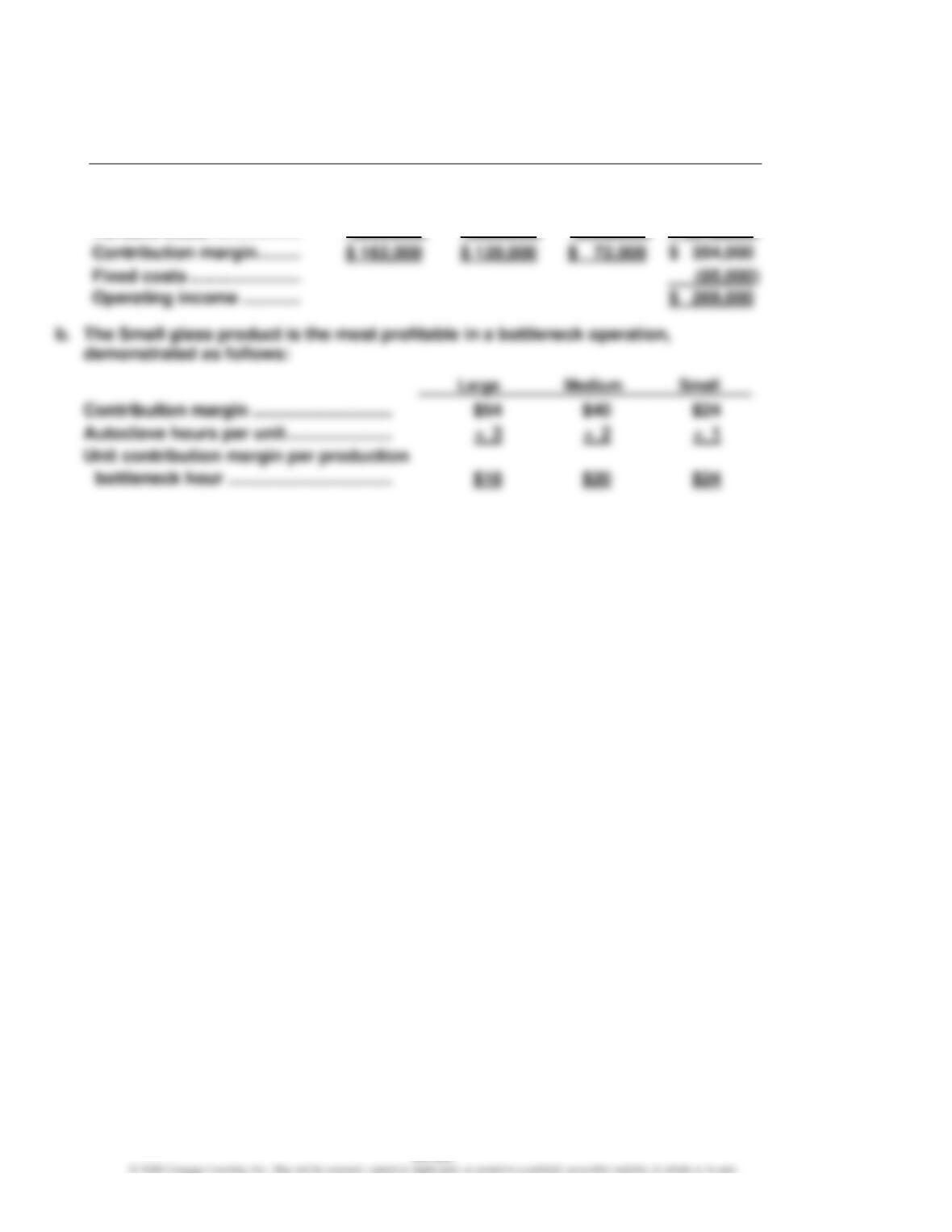

a.

Large

Medium

Small

Total

Units produced ……………..

3,000

3,000

3,000

Revenues ……………………..

$ 552,000

$ 480,000

$ 300,000

$1,332,000

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Ex. 25–22 (FIN MAN); Appendix Ex. 11–22 (MAN)

a.

Total costs:

Variable ($240 × 10,000 units) …………………………………………………

$2,400,000

Fixed ($350,000 + $140,000)…………………………………………………….

490,000

Total ……………………………………………………………………………………

$2,890,000

Cost amount per unit: $2,890,000 ÷ 10,000 units = $289

Appendix Ex. 25–23 (FIN MAN); Appendix Ex. 11–23 (MAN)

a.

Total variable costs: ($240 × 10,000 units) ………………………………………

$2,400,000

Cost amount per unit:: $2,400,000 ÷ 10,000 units = $240

Desired Profit + Total Fixed Costs

Markup Percentage = Total Costs

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

PROBLEMS

Prob. 25–1A (FIN MAN); Prob. 11–1A (MAN)

1.

Differential Analysis

Operate Retail Store (Alt. 1) or Invest in Bonds (Alt. 2)

August 1

Operate

Retail

Store

(Alternative 1)

Invest in

Bonds

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 5,400,0001

$600,0002

$(4,800,000)

Costs:

Costs to operate store

(3,000,000)3

0

3,000,000

Cost of equipment less

0

2. The proposal to operate the retail store should be accepted.

3.

Total estimated revenue from operating store ………….

$ 5,400,000

Total estimated expenses to operate store:

Costs to operate store, excluding depreciation ……

$3,000,000

Cost of store equipment less residual value ………..

(3,950,000)

Total estimated income from operating store* ………….

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–2A (FIN MAN); Prob. 11–2A (MAN)

1.

Differential Analysis

Continue with (Alt. 1) or Replace (Alt. 2) Old Machine

April 30

Continue

with Old

Machine

(Alternative 1)

Replace

Old

Machine

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues:

Proceeds from sale of old machine

$ 0

$ 29,700

$ 29,700

Purchase price

Annual manufacturing costs

$ 10,200

Costs:

1 $23,600 × 6 years

2 $6,900 × 6 years

Note: Revenues and nonmanufacturing operating expenses are not affected by the

Lexigraphic Printing Company should replace the old machine with the new machine.

2. Other factors to be considered include:

a. Are there any improvements in the quality of work turned out by the new machine?

b. What effect does the federal income tax have on the decision?

c. What opportunities are available for the use of the $90,000 of funds ($119,700 less

$29,700 proceeds from the old machine) that are required to purchase the new

machine?

After considering such factors as those listed above, the net cost reduction

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–3A (FIN MAN); Prob. 11–3A (MAN)

1.

Differential Analysis

Promote Moisturizer (Alt. 1) or Promote Perfume (Alt. 2)

November 2

Promote

Moisturizer

(Alternative 1)

Promote

Perfume

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$1,400,0001

$1,650,0002

$ 250,000

Costs:*

1 40,000 units × $35

2 30,000 units × $55

* Costs, except sales promotion, are the costs per unit multiplied by the increase in unit volume

for each cosmetic. Fixed costs are not relevant to the decision, so are not included.

Kanakee Cosmetics should promote perfume.

2. The sales manager’s tentative decision should be opposed. The sales manager

erroneously considered the full unit costs instead of the differential (additional)

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

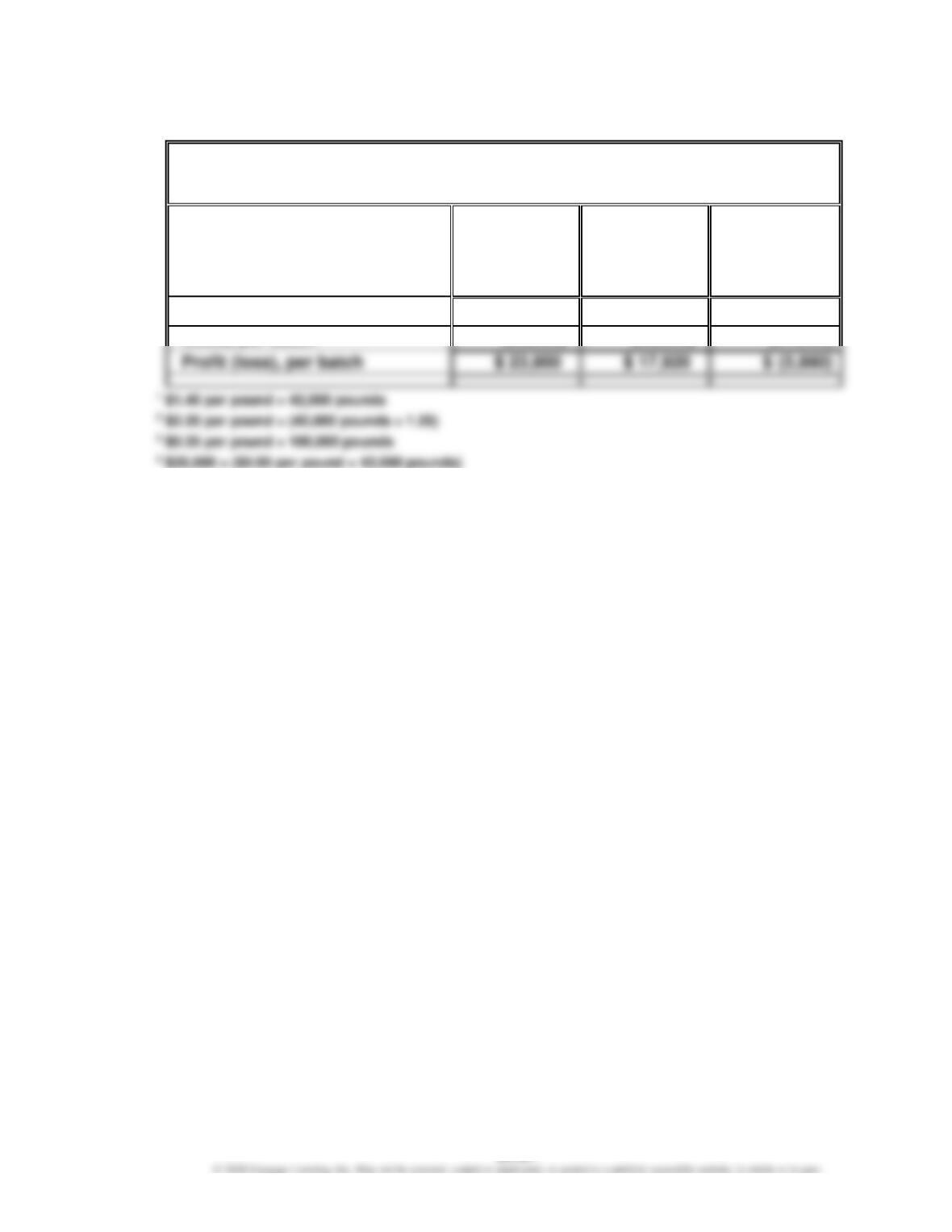

Prob. 25–4A (FIN MAN); Prob. 11–4A (MAN)

1.

Differential Analysis

Sell Raw Sugar (Alt. 1) or Process Further into Refined Sugar (Alt. 2)

March 24

Sell Raw

Sugar

(Alternative 1)

Process

Further into

Refined

Sugar

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues, per batch

$ 58,8001

$ 73,9202

$ 15,120

Costs, per batch

Profit (loss), per batch

2. Dominican Sugar Company should not process raw sugar further to produce refined

sugar because profits would be reduced by $5,880 per batch.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–5A (FIN MAN); Prob. 11–5A (MAN)

1.

High

Grade

Good

Grade

Regular

Grade

Selling price ……………………………………………….

$ 280

$ 270

$ 250

Variable conversion cost per unit ………………..

$(180)*

$(165)**

$(150)***

Direct materials cost per unit ………………………

(90)

(84)

(80)

Total unit costs…………………………………………..

Contribution margin per unit ……………………….

2. The contribution margin per unit may give false signals when an organization has

production bottlenecks. Instead, Hercules should use the contribution margin per

bottleneck hour to determine relative product profitability, as follows:

High

Grade

Good

Grade

Regular

Grade

Contribution margin per unit ……………………….

$ 10

$ 21

$ 20

Furnace (bottleneck) hours per unit …………….

÷ 4

÷ 3

÷ 2.5

Contribution margin per furnace hour ………….

$2.50

$7.00

$8.00

The Good Grade steel has the largest contribution margin per unit ($21); however,

Grade’s $2.50 or Good Grade’s $7.00 contribution margin per furnace hour.

Therefore, the company would want to sell product in the following preference

order:

1. Regular Grade

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6A (FIN MAN); Appendix Prob. 11–6A (MAN)

1. $225,000 ($1,500,000 × 15%)

2.

a.

Total manufacturing costs:

Variable ($200* × 5,000 units) ………………………………………………..

$1,000,000

Fixed factory overhead …………………………………………………………

250,000

Total …………………………………………………………………………………

$1,250,000

Cost amount per unit: $1,250,000 ÷ 5,000 units …………………………...

$ 250

* $120 + $30 + $50

Markup ($250 × 44%) …………………………………………………………………

Selling price ……………………………………………………………………………..

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6A (FIN MAN); Appendix Prob. 11–6A (MAN) (Continued)

3.

a.

Total costs:

Variable ($235 × 5,000 units) …………………………………………………

$1,175,000

Fixed ($250,000 + $150,000) ………………………………………………….

400,000

Total …………………………………………………………………………………

$1,575,000

Cost amount per unit: $1,575,000 ÷ 5,000 units

$ 315

Cost amount per unit ………………………………………………………………..

$315

Markup ($315 × 14.29%) …………………………………………………………….

Selling price ……………………………………………………………………………..

$360

4. a. Variable cost amount per unit: $235

Total variable costs: $235 × 5,000 units = $1,175,000

Desired Profit + Total Fixed Costs

Markup Percentage = Total Variable Costs

c.

Cost amount per unit …………………………………………………………………

$235

Markup ($235 × 53.19%) ……………………………………………………………..

125

Selling price ……………………………………………………………………………..

$360

5. The cost-plus approach price of $360 should be viewed as a general guideline for

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Appendix Prob. 25–6A (FIN MAN); Appendix Prob. 11–6A (MAN) (Concluded)

6. a.

Differential Analysis

Reject (Alt. 1) or Accept (Alt. 2) Order

August 3

Reject

Order

(Alternative 1)

Accept

Order

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$0

$ 180,000

$ 180,000

Costs:

Variable manufacturing costs

$0

b. The proposal should be accepted.

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

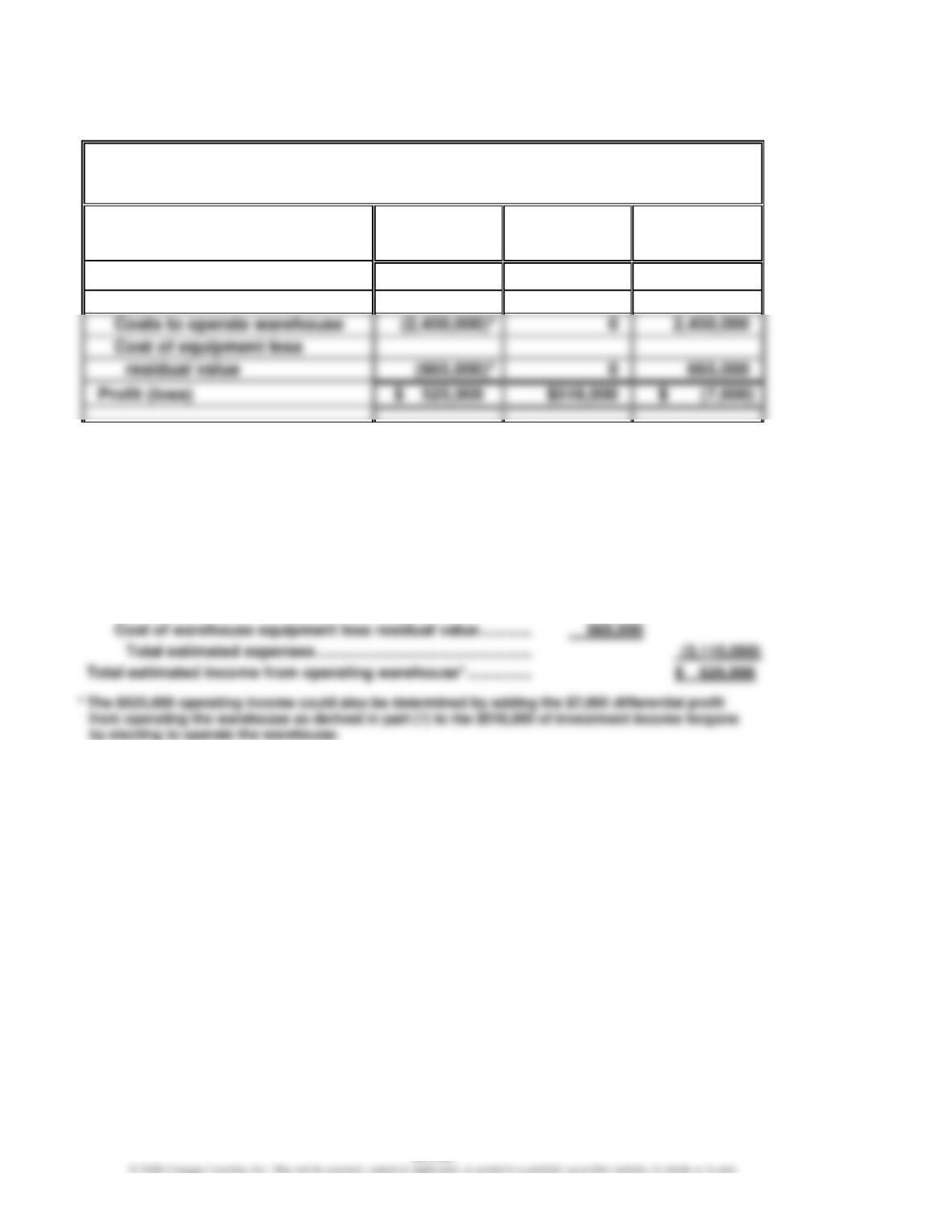

Prob. 25–1B (FIN MAN); Prob. 11–1B (MAN)

1.

Differential Analysis

Operate Warehouse (Alt. 1) or Invest in Bonds (Alt. 2)

July 1

Operate

Warehouse

(Alternative 1)

Invest in

Bonds

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 3,640,0001

$518,0002

$(3,122,000)

Costs:

1 (7 yrs. × $280,000) + (7 yrs. × $240,000)

2 5% × $740,000 × 14 years

3 $175,000 × 14 years

4 $740,000 – $75,000

2. The proposal to operate the warehouse should be accepted.

3.

Total estimated revenue from operating warehouse ……………

$ 3,640,000

Total estimated expenses to operate warehouse:

Costs to operate warehouse, excluding depreciation …….

$2,450,000

Cost of warehouse equipment less residual value …………

Total estimated income from operating warehouse* ……………

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–2B (FIN MAN); Prob. 11–2B (MAN)

1.

Differential Analysis

Continue with (Alt. 1) or Replace (Alt. 2) Old Machine

November 8

Continue

with Old

Machine

(Alternative 1)

Replace

Old

Machine

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues:

Proceeds from sale of old machine

$ 0

$ 12,900

$ 12,900

Costs:

Purchase price

Annual manufacturing costs

1 $12,400 × 6 years

2 $3,400 × 6 years

Note: Revenues and nonmanufacturing operating expenses are not affected by the

2. Other factors to be considered include the following:

a. Are there any improvements in the quality of work turned out by the new machine?

b. What effect does the federal income tax have on the decision?

c. What opportunities are available for the use of the $44,100 of funds ($57,000 less

$12,900 proceeds from the old machine) that are required to purchase the new

machine?

After considering such factors as those listed above, the net cost reduction

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–3B (FIN MAN); Prob. 11–3B (MAN)

1.

Differential Analysis

Promote Tennis (Alt. 1) or Walking (Alt. 2) Shoes

June 19

Promote

Tennis Shoes

(Alternative 1)

Promote

Walking Shoes

(Alternative 2)

Differential

Effects

(Alternative 2)

Revenues

$ 595,0001

$ 700,0002

$105,000

Costs:*

1 7,000 shoes × $85

2 7,000 shoes × $100

* Costs, except sales promotion, are the costs per unit multiplied by the increase in unit volume for each pair of

shoes. Fixed costs are not relevant to the decision so are not included.

Sole Mates Inc. should promote tennis shoes.

2. The sales manager’s tentative decision should be opposed. The sales manager

erroneously considered the full unit costs instead of the differential (additional) revenue

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

Prob. 25–4B (FIN MAN); Prob. 11–4B (MAN)

1.

Differential Analysis

Sell Ingot (Alt. 1) or Process Further into Rolled Aluminum (Alt. 2)

February 5

Sell

Ingot

(Alternative 1)

Process Further

into

Rolled

Aluminum

(Alternative 2)

Differential

Effects

(Alternative 2)

3 $105 per ton × 500 tons

4 $52,500 + ($620 per ton × 80 tons)

2. International Aluminum Co. should decide to process aluminum ingot further, rather

CHAPTER 25 (FIN MAN); CHAPTER 11 (MAN) Differential Analysis and Product Pricing

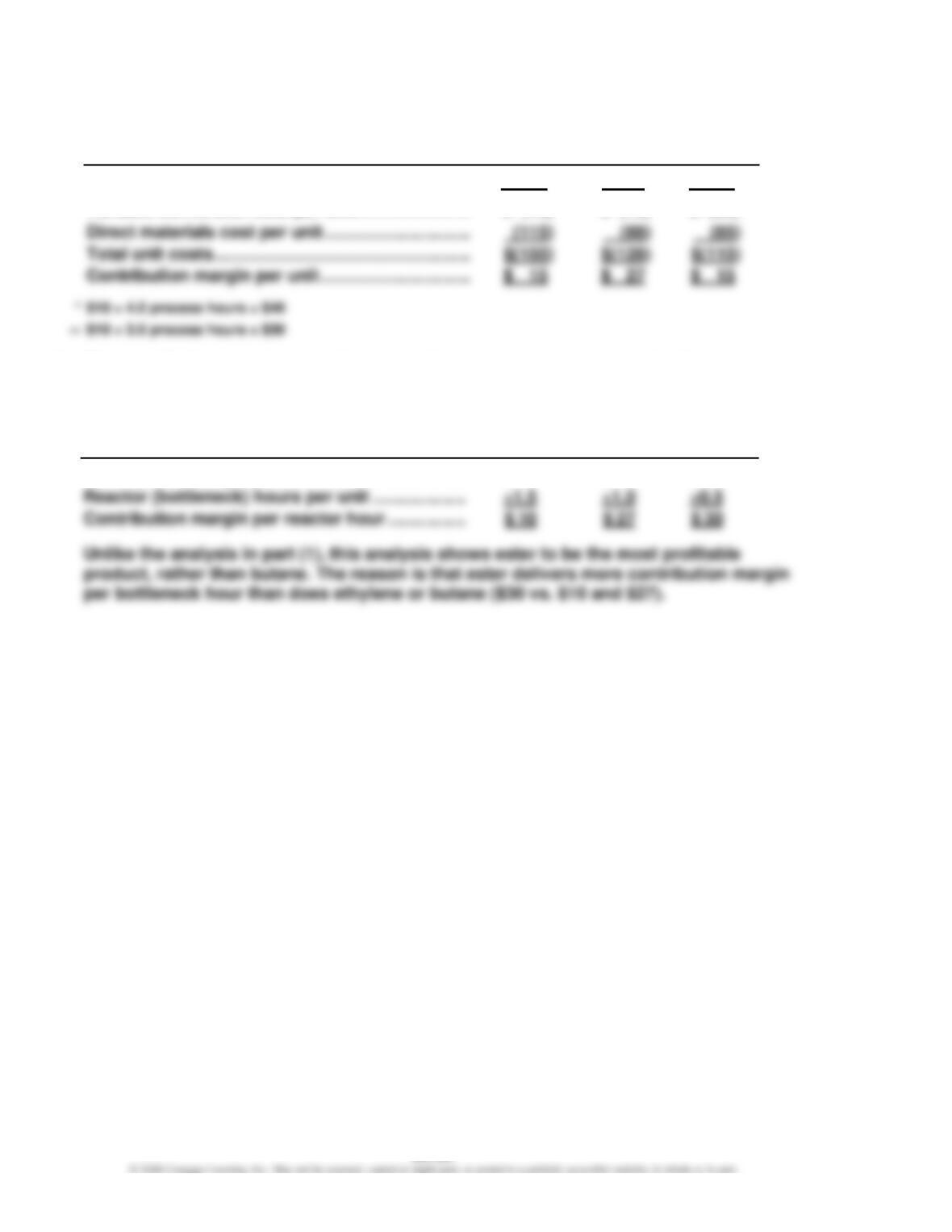

Prob. 25–5B (FIN MAN); Prob. 11–5B (MAN)

1.

Ethylene

Butane

Ester

Selling price ………………………………………………….

$ 170

$ 155

$ 130

2. The contribution margin per unit may give false signals when an organization has

production bottlenecks. Instead, Wilmington Chemical Company should use the

contribution margin per bottleneck hour to determine relative product profitability

as follows:

Ethylene

Butane

Ester

Contribution margin per unit …………………………

$ 15

$ 27

$ 15

Contribution margin per reactor hour …………….