DATA INPUT

Master Budget Actual Variance

Units sold 5,000 4,800 200 U

Revenue 1,800,000$ 1,728,000$ 72,000$ U

Variable cost 1,140,000 1,170,000 (30,000) U

Contribution margin 660,000$ 558,000$ 102,000$ U

Fixed overhead 270,000 270,000 –

Fixed general and adminstrative cost 180,000 172,500 7,500 F

Operating income 210,000$ 115,500$ 94,500$ U

Unit costs:

Direct material 90$

Direct labor 66$

Variable overhead 54$

Variable selling costs 18$

Total variable costs: 1,170,000$

Direct material 480,000$

Direct labor 288,000$

Variable overhead 264,000$

Variable selling expenes 138,000$

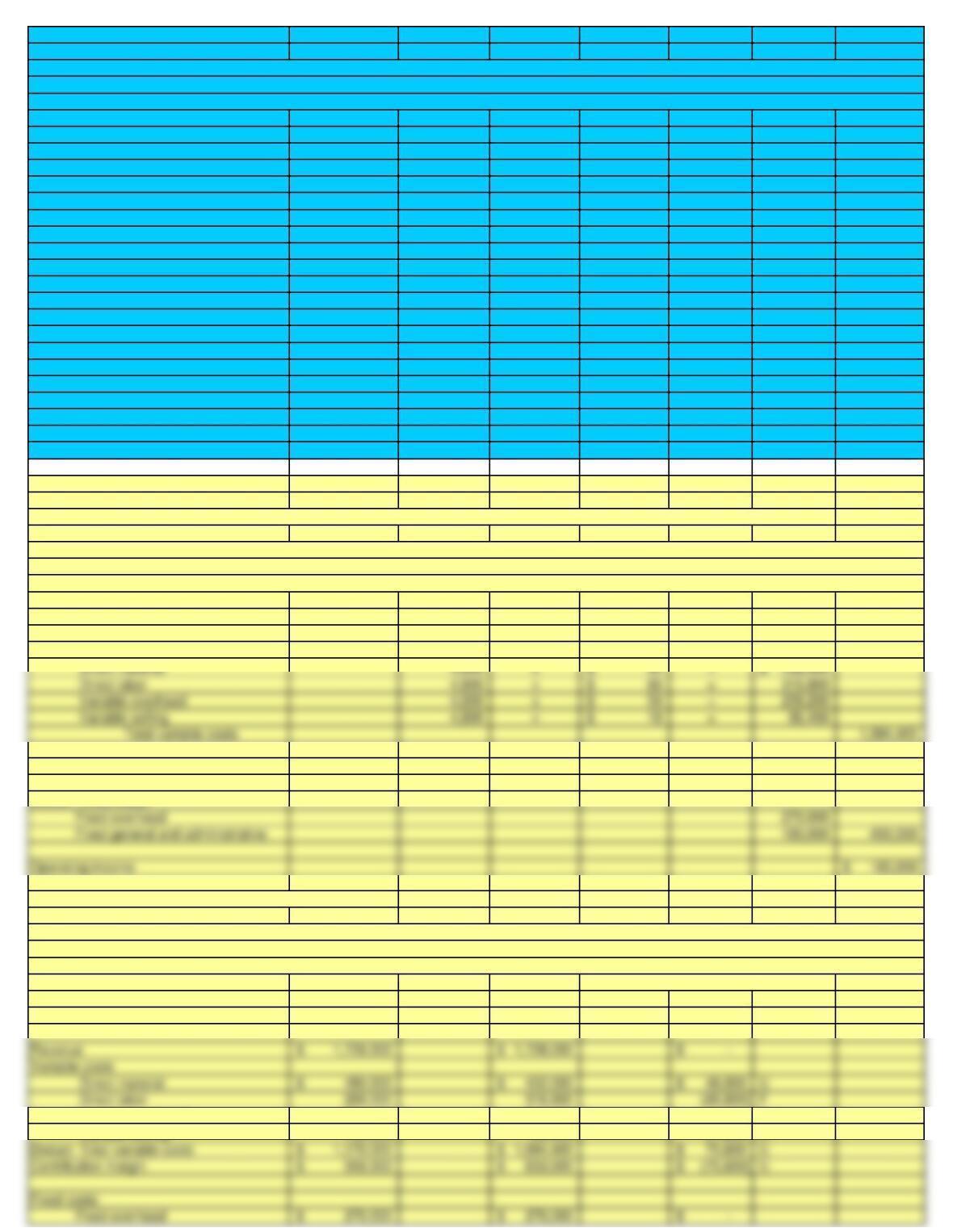

SOLUTION

1. Flexible budget for the month of June, based on 4,800 units, showing separate variable cost budget is as follows:

Revenue 4,800 x 1,800,000$ / 5,000 = 1,728,000$

Deduct: Variable costs:

Contribution margin 633,600$

Deduct: Fixed costs:

2. Flexible-budget variances are as follows:

Flexible Flexible-Budget

Actual Budget Variance

Units 4,800 4,800 –

Variable overhead 264,000 259,200 4,800 U

Variable selling 138,000 86,400 51,600 U

LakeMaster Company

Flexible-Budget Variances

For the Month of June

LakeMaster Company

Operating Results

For the Month of June

LakeMaster Company

Flexible Budget

For the Month of June

Fixed general and administrative 172,500 180,000 (7,500) F