CHAPTER 11

CURRENT LIABILITIES AND PAYROLL

ACCOUNTING

LEARNING OBJECTIVES

1. EXPLAIN HOW TO ACCOUNT FOR CURRENT

LIABILITIES.

2. DISCUSS HOW CURRENT LIABILITIES ARE

REPORTED AND ANALYZED.

CHAPTER REVIEW

Current Liabilities

1. (L.O. 1) A current liability is a debt that a company expects to pay within one year or the

operating cycle, whichever is longer. Current liabilities include notes payable, accounts payable,

unearned revenues, and accrued liabilities.

Notes Payable

2. Notes payable are obligations in the form of written notes that usually

require the borrower to pay interest. Notes due for payment within one year of the balance sheet

date are usually classified as current liabilities.

Sales Taxes Payable

4. A sales tax is expressed as a percentage of the sales price on goods sold to customers. The

entry by the selling company to record sales taxes is as follows:

Cash …………………………………………………………………………………… XXXX

Sales Revenue ………………………………………………………………. XXXX

Unearned Revenues

5. Unearned Revenues (advances from customers) are recorded by a debit to Cash and a credit to

a current liability account identifying the source of the unearned revenue. When the revenue is

recognized, an unearned revenue account is debited and a revenue account is credited.

Current Maturities of Long-Term Debt

Statement Presentation and Analysis

7. (L.O. 2) Current liabilities is the first category under liabilities on the balance sheet.

a. Each of the principal types of current liabilities is listed separately.

Contingent Liabilities

9. A contingent liability is a potential liability that may become an actual liability in the future. The

accounting guidelines require that:

a. If the contingency is probable (likely to occur) and the amount can be reasonably estimated,

the liability should be recorded in the accounts.

b. If the contingency is only reasonably possible (could happen), then it needs to be disclosed

Payroll Accounting

11. (L.O. 3) The term payroll pertains to both salaries and wages of employees. Payments made to

professional individuals who are independent contractors are called fees. Government regulations

relating to the payment and reporting of payroll taxes apply only to employees.

Gross Earnings

12. Gross earnings is the total compensation earned by an employee. It consists of wages or

salaries, plus any bonuses and commissions.

a. Total wages are determined by applying the hourly rate of pay to the hours worked.

Payroll Deductions

13. Mandatory payroll deductions consist of FICA taxes and income taxes.

a. These deductions do not result in payroll tax expense to the employer.

b. FICA taxes are designed to provide workers with supplemental retirement, employment

disability, and medical benefits.

c. FICA taxes are also known as Social Security taxes.

Recording the Payroll

17. The employee earnings record provides a cumulative record of each employee’s gross

earnings, deductions, and net pay during the year. This record is used by the employer in:

a. Determining when an employee has earned the maximum earnings subject to FICA taxes.

b. Filing state and federal payroll tax returns.

18. Many companies use a payroll register to accumulate the gross earnings, deductions, and net

pay by employee for each period. In some companies, this record is a journal or book of original

entry.

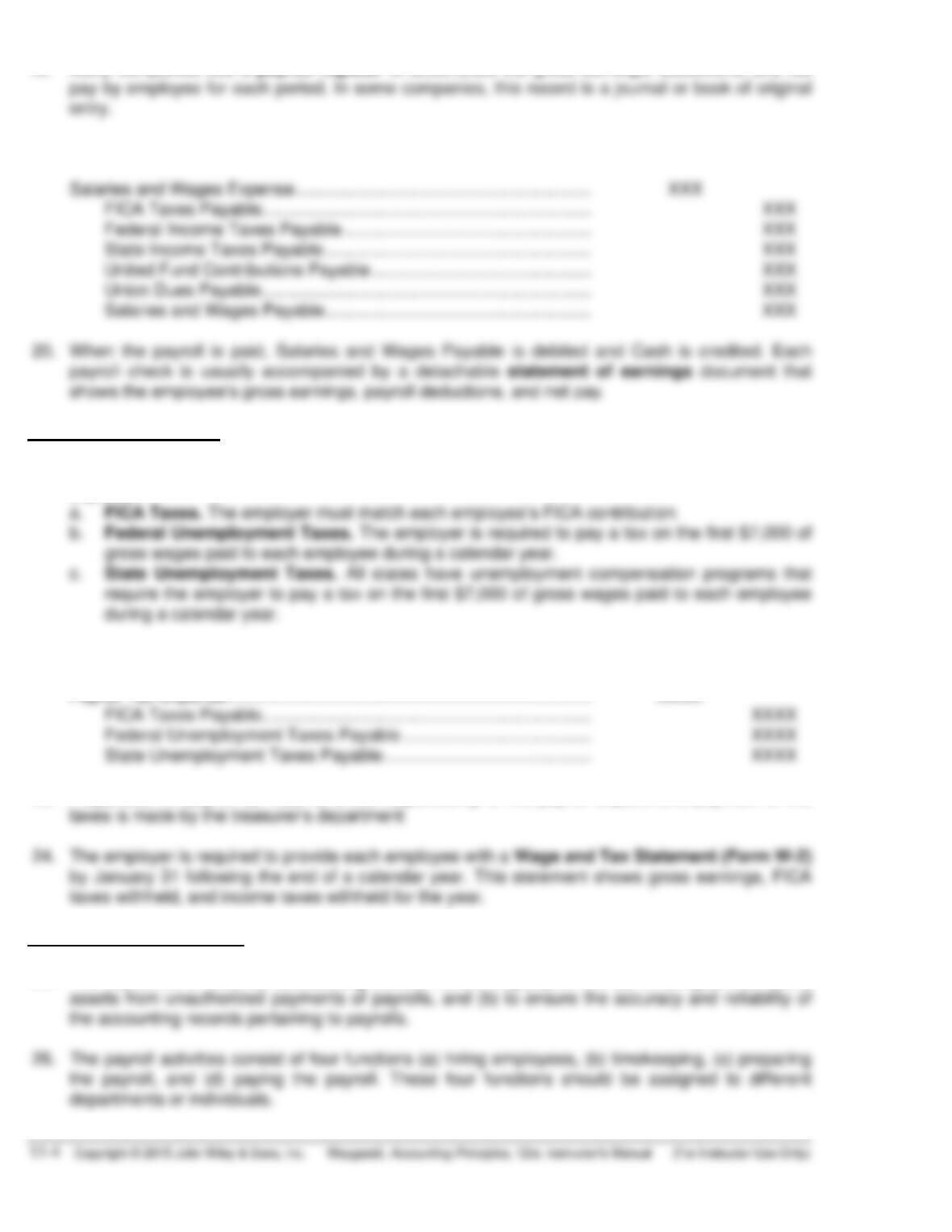

19. The typical journal entry to record a payroll is as follows:

Salaries and Wages Expense ……………………………………………………. XXX

FICA Taxes Payable………………………………………………………….. XXX

Federal Income Taxes Payable …………………………………………… XXX

20. When the payroll is paid, Salaries and Wages Payable is debited and Cash is credited. Each

Employer Payroll Taxes

21. There are three taxes imposed on employers by government agencies that result in payroll tax

expense.

a. FICA Taxes. The employer must match each employee’s FICA contribution.

b. Federal Unemployment Taxes. The employer is required to pay a tax on the first $7,000 of

22. The typical entry for recording payroll tax expense is as follows:

Payroll Tax Expense ………………………………………………………………… XXXX

FICA Taxes Payable………………………………………………………….. XXXX

23. Preparation of payroll tax returns is the responsibility of the payroll department; payment of the

taxes is made by the treasurer’s department.

Internal Control for Payroll

25. The objectives of internal accounting control concerning payroll are (a) to safeguard company

assets from unauthorized payments of payrolls, and (b) to ensure the accuracy and reliability of

the accounting records pertaining to payrolls.

Additional Fringe Benefits

*27. (L.O. 4) When the payment for paid absences (paid vacations, sick pay benefits, and paid

holidays) is probable and the amount can be reasonably estimated, a liability should be accrued.

The entry to record the liability will include a debit to Vacation Benefits Expense and a credit to

Vacation Benefits Payable. When the amount cannot be reasonably estimated, the potential

liability should be disclosed.

*30. A defined-contribution plan defines the contribution an employer will make but not the benefit

that the employee will receive at retirement. A 401(k) plan is an example of a defined-contribution

plan. In a defined-benefit plan, the employer agrees to pay a defined amount to

retirees, based on employees meeting certain eligibility standards.

LECTURE OUTLINE

A. Accounting for Current Liabilities.

1. A current liability is a debt that a company expects to pay within one year

or the operating cycle, whichever is longer.

2. Current liabilities include notes payable, accounts payable, unearned

revenues, and accrued liabilities such as taxes, salaries and wages, and

interest payable.

a. Companies record obligations in the form of written notes as notes

payable. Companies frequently issue notes payable to meet short–

term financing needs. Notes payable usually require the borrower to

pay interest. Notes due for payment within one year of the balance

sheet date are usually classified as current liabilities.

b. Sales taxes are expressed as a percentage of the sales price. The

selling company collects the tax from the customer when the sale

occurs, and periodically (monthly) remits the collections to the state’s

department of revenue.

3. Statement Presentation and Analysis.

a. Companies usually list current liabilities by order of magnitude, with

the largest ones first.

b. As a matter of custom, many companies show notes payable first

and then accounts payable, regardless of amount.

4. A contingent liability is a potential liability that may become an actual liability

in the future.

a. If the contingency is probable (likely to occur) and the amount can be

reasonably estimated, the liability should be recorded in the accounts.

(Both conditions required for recording.)

d. Product warranties are an example of a contingent liability that

companies should record in the accounts. The accounting for warranty

costs is based on the expense recognition principle; therefore,

companies should recognize the estimated cost of honoring product

warranty contracts as an expense in the period in which the sale

occurs.

e. When it is probable that a company will incur a contingent liability but

it cannot reasonably estimate the amount, or when the contingent

liability is only reasonably possible, only disclosure of the contingency

is required.

f. Contingencies that may require disclosures are:

ACCOUNTING ACROSS THE ORGANIZATION

Contingent liabilities abound in the real world. Life and health insurance companies

and their stockholders wonder how big the cost of diabetes, Alzheimer’s, and

AIDS really are and what damage they might do in the future.

Why do you think most companies disclose, but do not record, contingent liabilities?

Answer: In many cases, it is probable that companies have a contingent liability

but the amount of the liability is often difficult to determine. If it cannot

be determined, the company is not required to accrue it as a liability.

B. Payroll Accounting.

1. Payroll accounting involves maintaining payroll records for each

employee, filing and paying payroll taxes, and complying with state and

federal employee compensation tax laws.

C. Gross Earnings.

1. Gross earnings consist of: wages or salaries, plus any bonuses and

commissions.

D. Payroll Deductions and Net Pay.

1. Payroll deductions do not result in payroll tax expense to the employer

because the company is merely a collection agent for the government.

Mandatory deductions are required by law and consist of FICA taxes

and income taxes.

a. FICA taxes are designed to provide workers with supplemental retire-

ment, employment disability, and medical benefits. FICA taxes are

commonly referred to as Social Security taxes.

b. Under the U.S. pay-as-you-go system of federal income taxes, em–

ployers are required to withhold income taxes from employees each

pay period. Three variables determine the amount to be withheld:

(1) The employee’s gross earnings.

2. Employees may voluntarily authorize withholdings for charitable, retirement,

and other purposes. All voluntary deductions from gross earnings should

be authorized in writing by the employee.

E. Maintaining Payroll Department Records.

1. To comply with state and federal laws, an employer must keep a cumulative

record of each employee’s gross earnings, deductions, and net pay during

the year.

3. The employer uses the cumulative payroll data on the earnings record to:

a. Determine when an employee has earned the maximum earnings

subject to FICA taxes.

b. File state and federal payroll tax returns.

F. Employer Payroll Taxes.

1. Payroll tax expense results from three taxes that governmental agencies

levy on employers. These taxes are FICA, federal unemployment tax

(FUTA), and state unemployment tax (SUTA).

2. FICA, FUTA, SUTA, plus items such as paid vacations and pensions are

collectively referred to as fringe benefits.

a. Employers must match each employee’s FICA contribution. Thus, the

employer’s tax is subject to the same rate and maximum earnings

as the employee’s.

3. Companies usually record employer payroll taxes at the same time

they record the payroll. Payroll Tax Expense is debited and the separate

liability accounts are credited because these liabilities are payable to

different taxing authorities at different dates.

G. Internal Control for Payroll.

1. The objectives of internal control for payrolls are:

a. To safeguard company assets against unauthorized payments of

payrolls.

internal control.

3. Posting job openings, screening and interviewing applicants, and hiring

employees are responsibilities of the human resources department.

4. Another area in which internal control is important is timekeeping. Hourly

employees are normally required to record time worked by “punching” a

time clock.

6. The payroll is paid by the treasurer’s department. Payment by check

minimizes the risk of loss from theft, and the endorsed check provides

proof of payment.

*H. Additional Fringe Benefits.

1. Additional fringe benefits associated with wages are paid absences (paid

vacations, sick pay benefits, and paid holidays) and postretirement

benefits (pensions and health care and life insurance).

2. Employees often are given rights to receive compensation for absences

when certain conditions of employment are met.

3. Postretirement benefits are benefits provided by employers to retired

employees for pensions and health care and life insurance.

a. A pension plan is an arrangement whereby an employer provides

benefits (payments) to employees after they retire. In a defined–

contribution 401(K) plan, the plan defines the employer’s

contribution but not the benefit that employee will receive at

retirement.

IFRS

A Look at IFRS

IFRS and GAAP have similar definitions of liabilities. The general recording

procedures for payroll are similar although differences occur depending on the

types of benefits that are provided in different countries. For example, companies

in other countries often have different forms of pensions, unemployment benefits,

welfare payments, and so on.

KEY POINTS

Following are the key similarities and differences between GAAP and IFRS

related to current liabilities and payroll.

• The basic definition of a liability under GAAP and IFRS is very similar. In a

more technical way, liabilities are defined by the IASB as a present

obligation of the entity arising from past events, the settlement of which is

expected to result in an outflow from the entity of resources embodying

economic benefits.

• Under GAAP, some contingent liabilities are recorded in the financial

statements, others are disclosed, and in some cases no disclosure is

required. Unlike GAAP, IFRS reserves the use of the term contingent

liability to refer only to possible obligations that are not recognized in the

financial statements but may be disclosed if certain criteria are met.

• For those items that GAAP would treat as recordable contingent liabilities,

IFRS instead uses the term provisions. Provisions are defined as liabilities

LOOKING TO THE FUTURE

The FASB and IASB are currently involved in two projects, each of which has

implications for the accounting for liabilities. One project is investigating

approaches to differentiate between debt and equity instruments. The other

20 MINUTE QUIZ

Circle the correct answer.

True/False

1. A current liability to the state arises when a business sells an item and collects a state

sales tax on it.

True False

2. An unearned revenue arises when payment is accepted in advance of the goods being

delivered.

True False

3. A refrigerator is sold in year 1, and a repair is made in year 2. The company’s entry upon

making the repair would include a debit to Warranty Liability.

True False

4. The excess of current assets over current liabilities is called the current ratio.

True False

5. Current maturities of long-term debt are identified on the balance sheet as long-term debt

due within one year.

True False

6. With an interest-bearing note, the amount of cash received upon issuance of the note will

be less than the note’s face value.

True False

7. A contingent liability is recorded if it is reasonably possible and the amount can be reasonably

estimated.

True False

8. The separation of the payroll activities of hiring, timekeeping, preparing payroll, and paying

the payroll weakens internal control over the payroll transactions.

True False

9. Net pay is determined by applying the hourly rate of pay to the hours worked less payroll

deductions.

True False

*10. Vacation pay is properly charged as an expense in the month in which the employee

takes the vacation.

True False

Multiple Choice

1. The account Unearned Subscription Revenue

a. is considered a miscellaneous revenue account.

b. has a normal debit balance.

c. is a contra account to Subscription Revenue.

d. is a current liability.

2. Which of the following is not a contingent liability?

a. Product warranties

b. Pending or threatened lawsuits

c. Current maturities of long-term debt

d. Assessment of additional income taxes pending an audit

3. Payroll Tax Expense includes all of the following except

a. federal income tax payable.

b. federal unemployment tax payable.

c. FICA tax payable.

d. state unemployment tax payable.

4. Which of the following is not an estimated liability?

a. Vacation pay

b. Sales taxes

c. Product warranties

d. Income taxes

5. Recording estimated warranty expense in the year of the sale best follows which accounting

principle?

a. Revenue recognition

b. Full disclosure

c. Expense recognition

d. Historical cost

ANSWERS TO QUIZ

True/False

1. True 6. False

2. True 7. False

Multiple Choice

1. d.