CHAPTER 11 Current Liabilities and Payroll

Prob. 11–3A

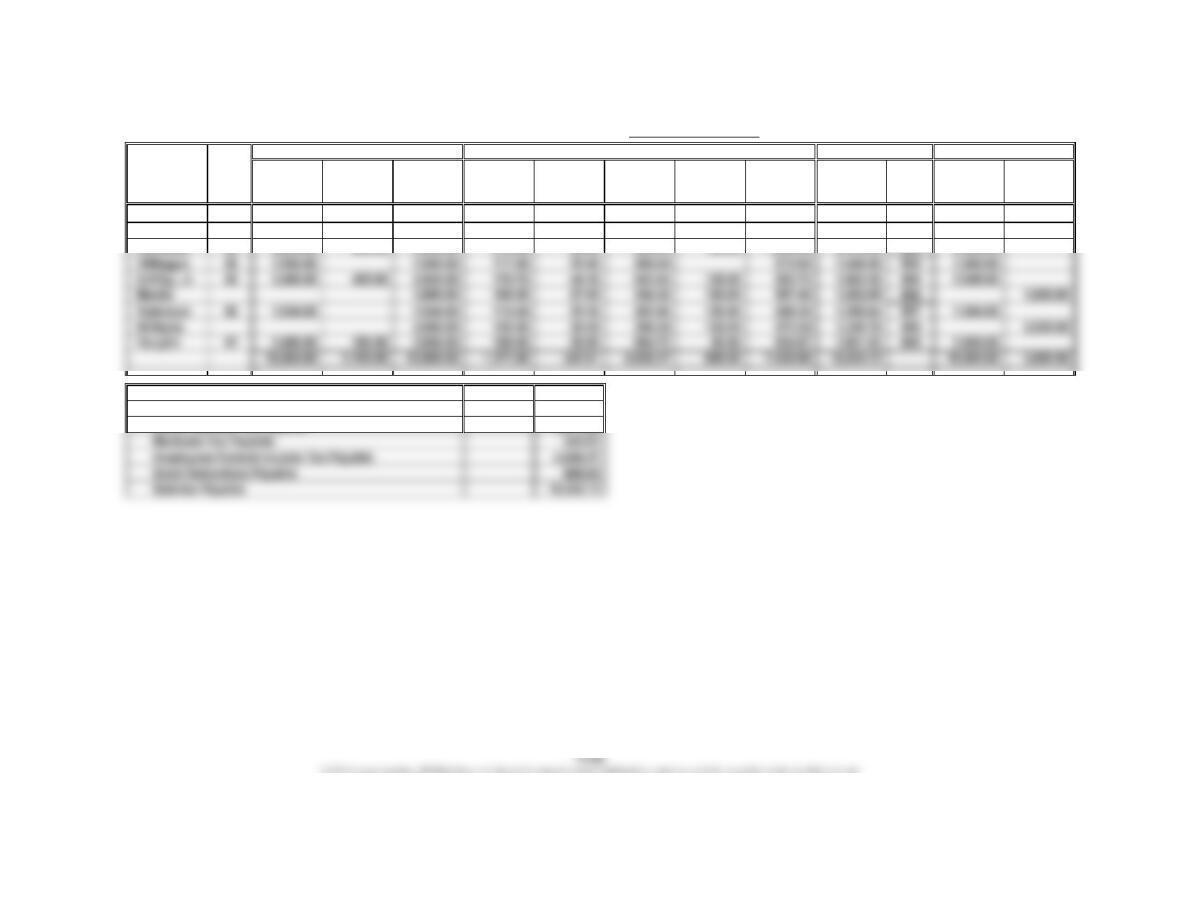

1. Gross Federal Income Social Security Medicare

Earnings Tax Withheld Tax Withheld Tax Withheld

Arnett………

…

$ 8,250.00 $ 1,416.00 $ 495.00 $ 123.75

Cruz…………

…

57,600.00 9,996.00 3,456.00 864.00

Edwards……

…

24,000.00 4,776.00 1,440.00 360.00

2. a. Social security tax paid by employer…………………………………

…

$19,780.80

c. Earnings subject to unemployment compensation tax,

$10,000 for all employees except Arnett, Harvin, and Ward.

Thus, total earnings subject to SUTA and FUTA are

…

Employee

CHAPTER 11 Current Liabilities and Payroll

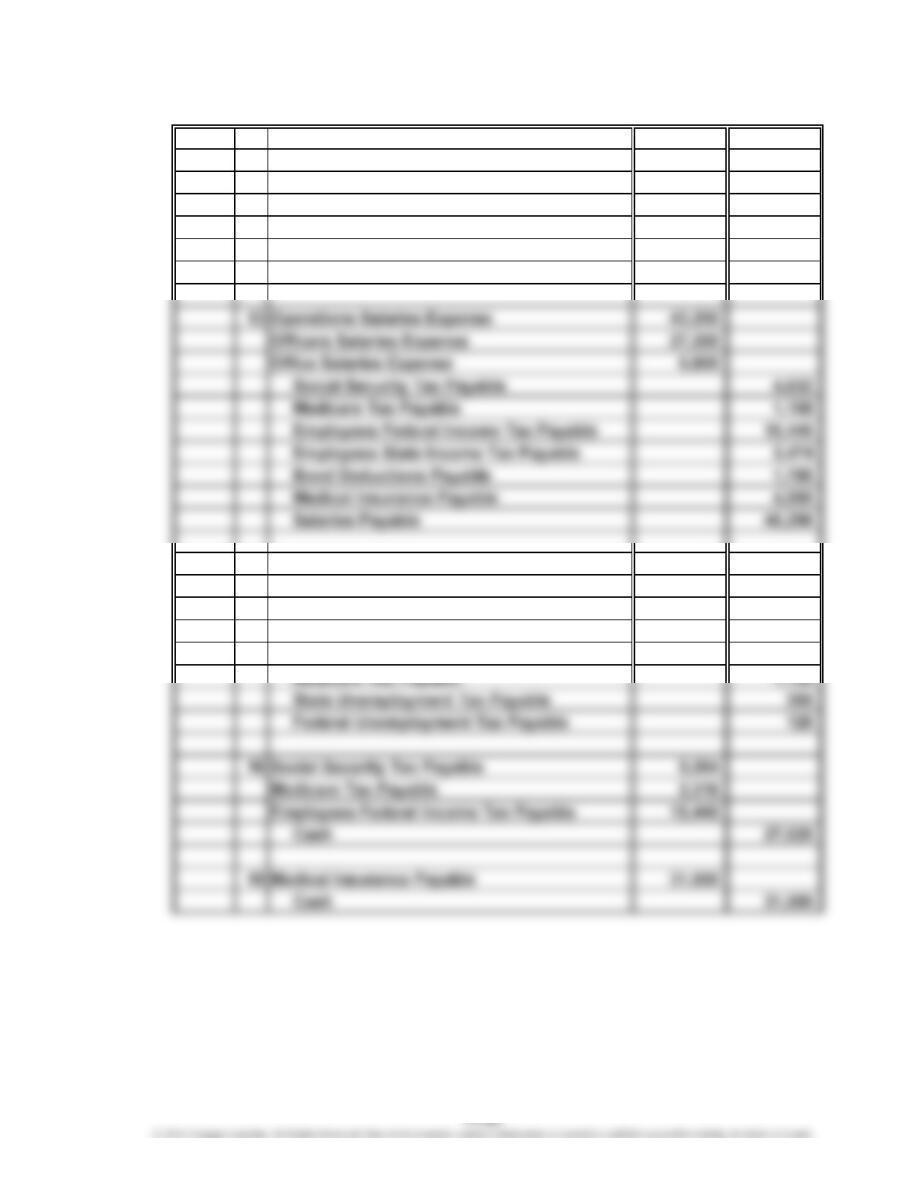

Prob. 11–4A

1.

Social Federal U.S. Sales Office

Total Security Medicare Income Savings Net Ck. Salaries Salaries

Employee Hours Regular Overtime Total Tax Tax Tax Bonds Total Pay No. Expense Expense

Aaron 46 2,720.00 612.00 3,332.00 199.92 49.98 750.20 100.00 1,100.10 2,231.90 901 3,332.00

Cobb 41 2,480.00 93.00 2,573.00 154.38 38.60 537.68 110.00 840.66 1,732.34 902 2,573.00

Clemente 48 2,800.00 840.00 3,640.00 218.40 54.60 832.64 120.00 1,225.64 2,414.36 903 3,640.00

2. Sales Salaries Expense 19,060.00

Office Salaries Expense 3,800.00

Social Security Tax Payable 1,371.60

PAYROLL FOR WEEK ENDING December 9, 2016

EARNINGS DEDUCTIONS PAID ACCOUNT DEBITED

CHAPTER 11 Current Liabilities and Payroll

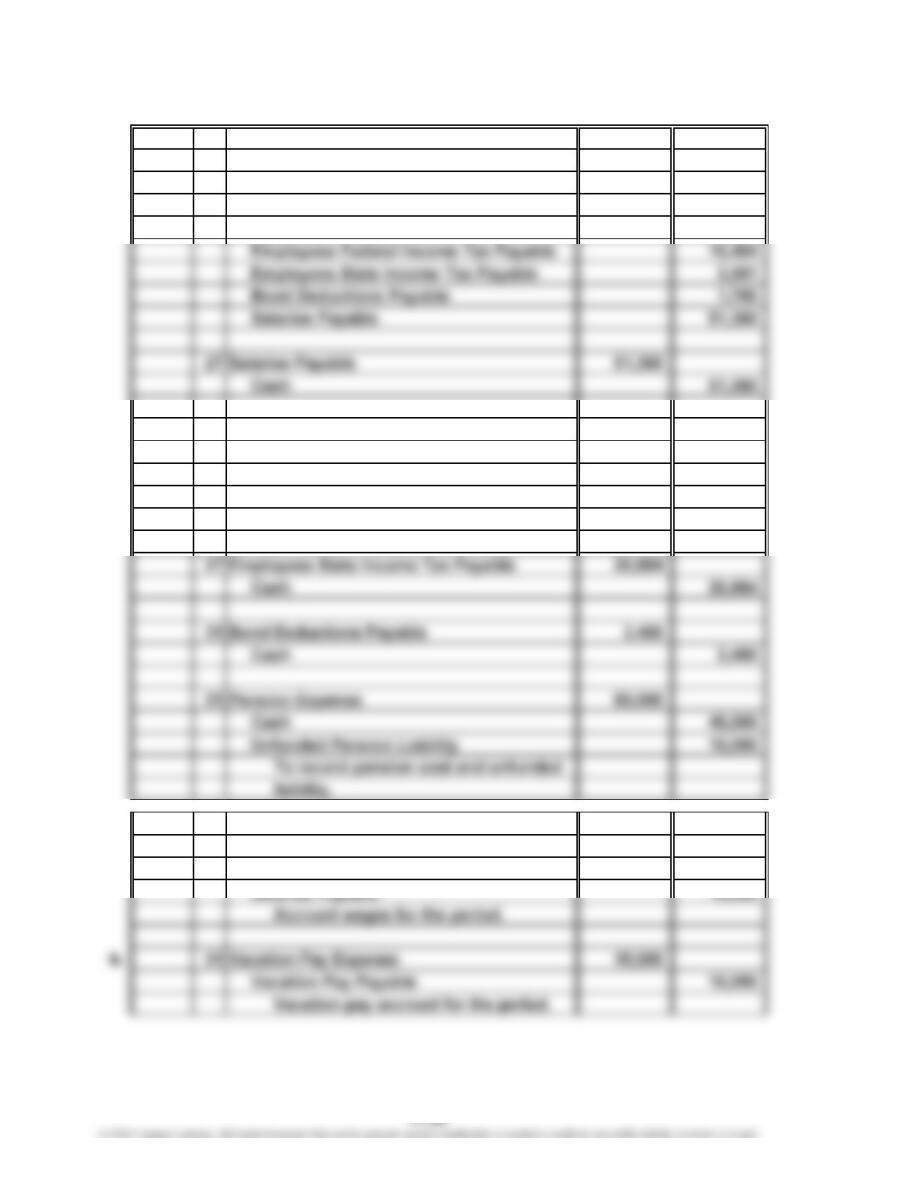

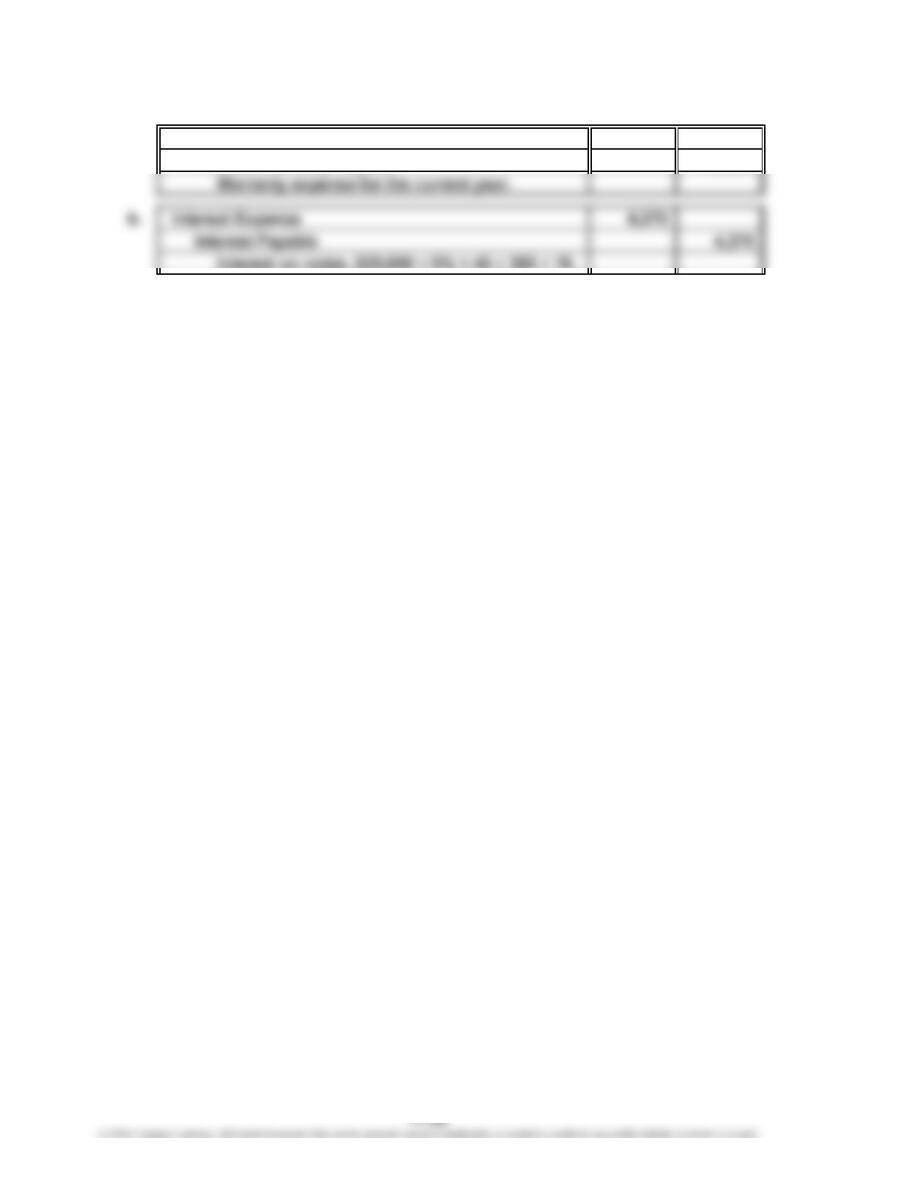

Prob. 11–5A

1. Dec. 2 Bond Deductions Payable 3,400

Cash 3,400

2 Social Security Tax Payable 9,273

Medicare Tax Payable 2,318

Employees Federal Income Tax Payable 15,455

Cash 27,046

13 Salaries Payable 46,296

Cash 46,296

13 Payroll Tax Expense 6,265

Social Security Tax Payable 4,632

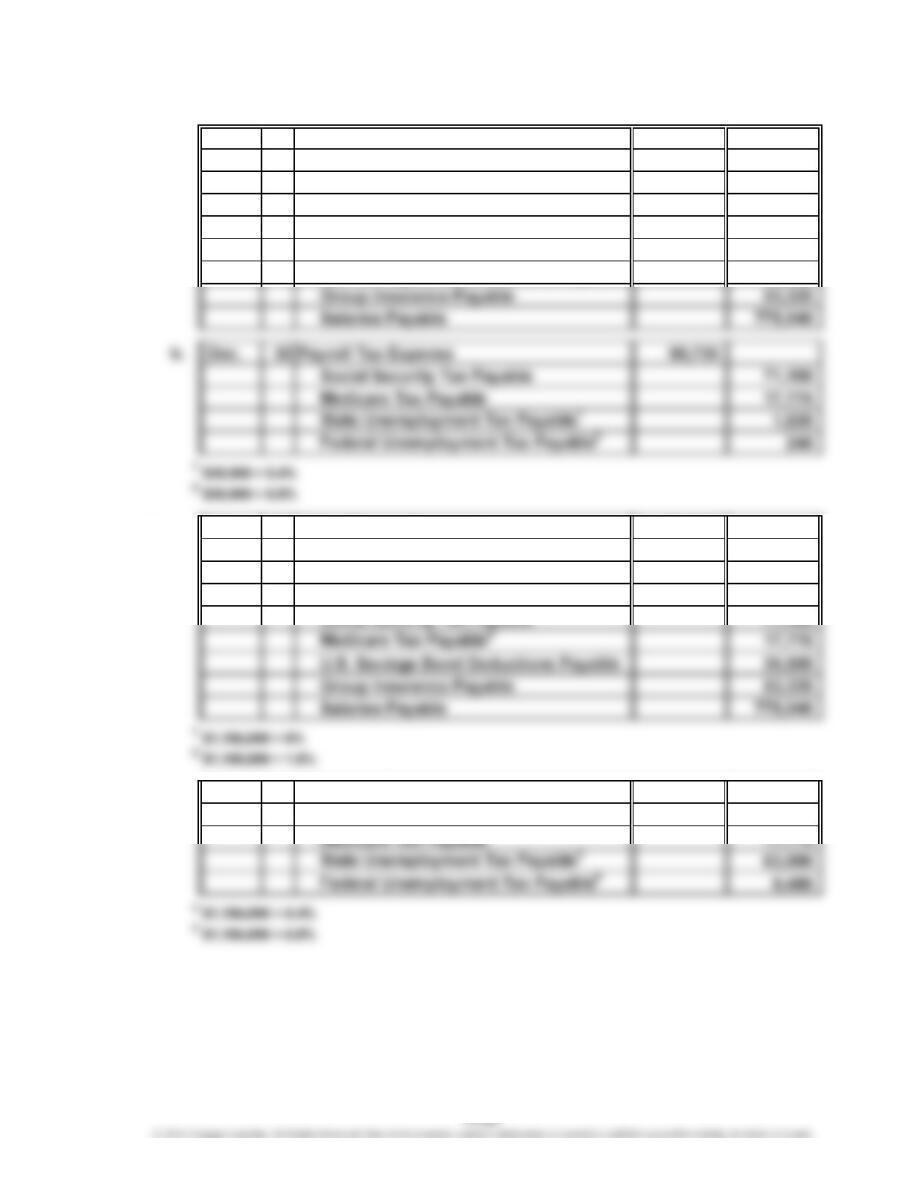

CHAPTER 11 Current Liabilities and Payroll

Prob. 11–5A (Concluded)

Dec. 27 Operations Salaries Expense 42,800

Officers Salaries Expense 28,000

Office Salaries Expense 7,000

Social Security Tax Payable 4,668

Medicare Tax Payable 1,167

27 Payroll Tax Expense 6,135

Social Security Tax Payable 4,668

Medicare Tax Payable 1,167

State Unemployment Tax Payable 225

Federal Unemployment Tax Payable 75

2. a. Dec. 31 Operations Salaries Expense 8,560

Officers Salaries Expense 5,600

Office Salaries Expense 1,400

CHAPTER 11 Current Liabilities and Payroll

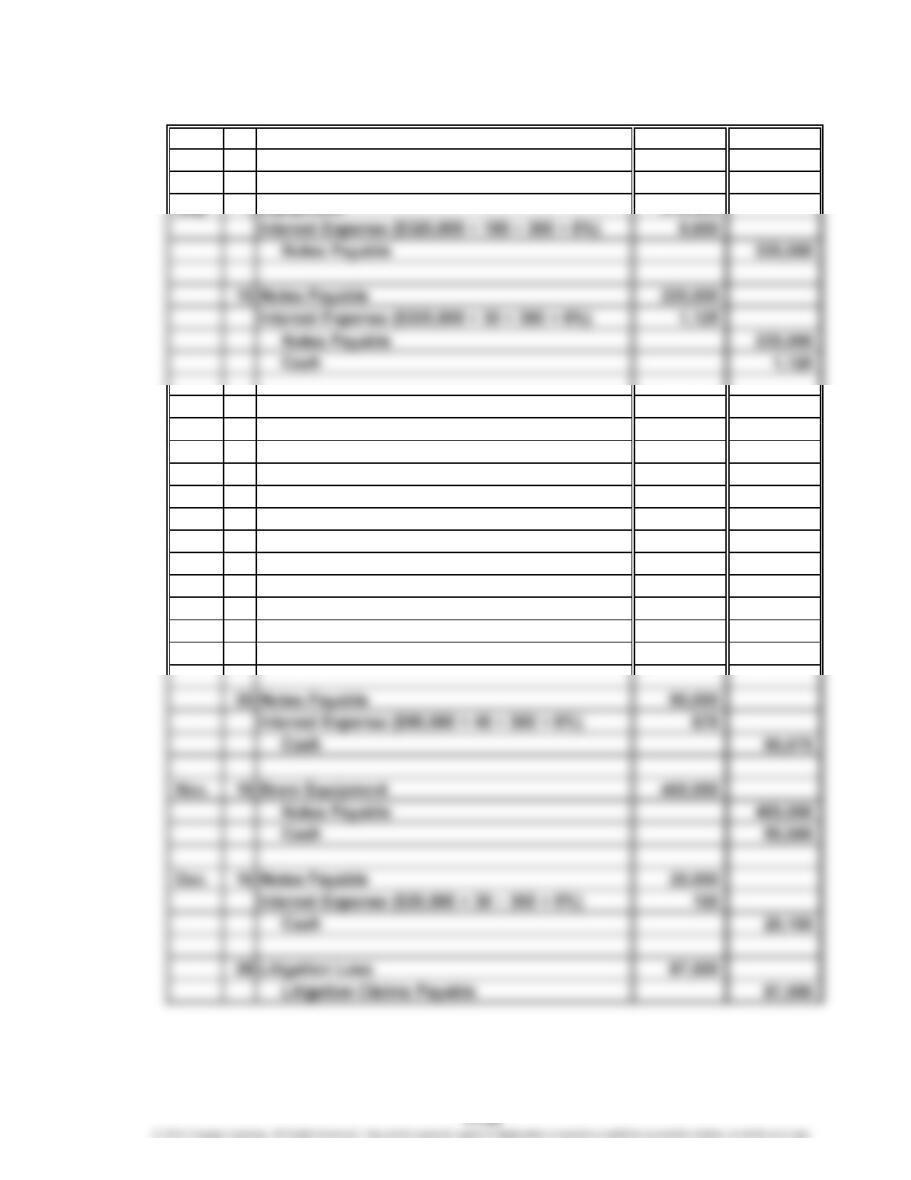

Prob. 11–1B

1. Apr. 15 Cash 225,000

Notes Payable 225,000

May 1 Equipment 310,400

July 14 Notes Payable 225,000

Interest Expense ($225,000 × 60 ÷ 360 × 8%) 3,000

Cash 228,000

Aug. 16 Merchandise Inventory 90,000

Accounts Payable—Exige Co. 90,000

Sept. 15 Accounts Payable—Exige Co. 90,000

Notes Payable 90,000

Oct. 28 Notes Payable 320,000

Cash 320,000

CHAPTER 11 Current Liabilities and Payroll

Prob. 11–1B (Concluded)

2. a. Product Warranty Expense 26,800

Product Warranty Payable 26,800

CHAPTER 11 Current Liabilities and Payroll

Prob. 11–2B

1. a. Dec. 30 Sales Salaries Expense 625,000

Warehouse Salaries Expense 240,000

Office Salaries Expense 320,000

Employees Income Tax Payable 232,260

Social Security Tax Payable 71,100

Medicare Tax Payable 17,775

U.S. Savings Bond Deductions Payable 35,500

2. a. Dec. 30 Sales Salaries Expense 625,000

Warehouse Salaries Expense 240,000

Office Salaries Expense 320,000

Employees Income Tax Payable 232,260

Social Security Tax Payable171,100

b. Jan. 4 Payroll Tax Expense 162,345

Social Security Tax Payable 71,100

CHAPTER 11 Current Liabilities and Payroll

Prob. 11–3B

1. Gross Federal Income Social Security Medicare

Earnings* Tax Withheld Tax Withheld Tax Withheld

Addai………………

…

$44,880 $ 9,372 $ 2,692.80 $ 673.20

Kasay………………

…

25,200 3,731 1,512.00 378.00

McGahee…………

…

67,410 12,999 4,044.60 1,011.15

2. a. Social security tax paid by employer……………………………… $17,163.90

b. Medicare tax paid by employer……………………………………

…

4,290.98

c. Earnings subject to unemployment compensation tax,

$10,000 for all employees except Stewart and Tolbert.

Employee

…

CHAPTER 11 Current Liabilities and Payroll

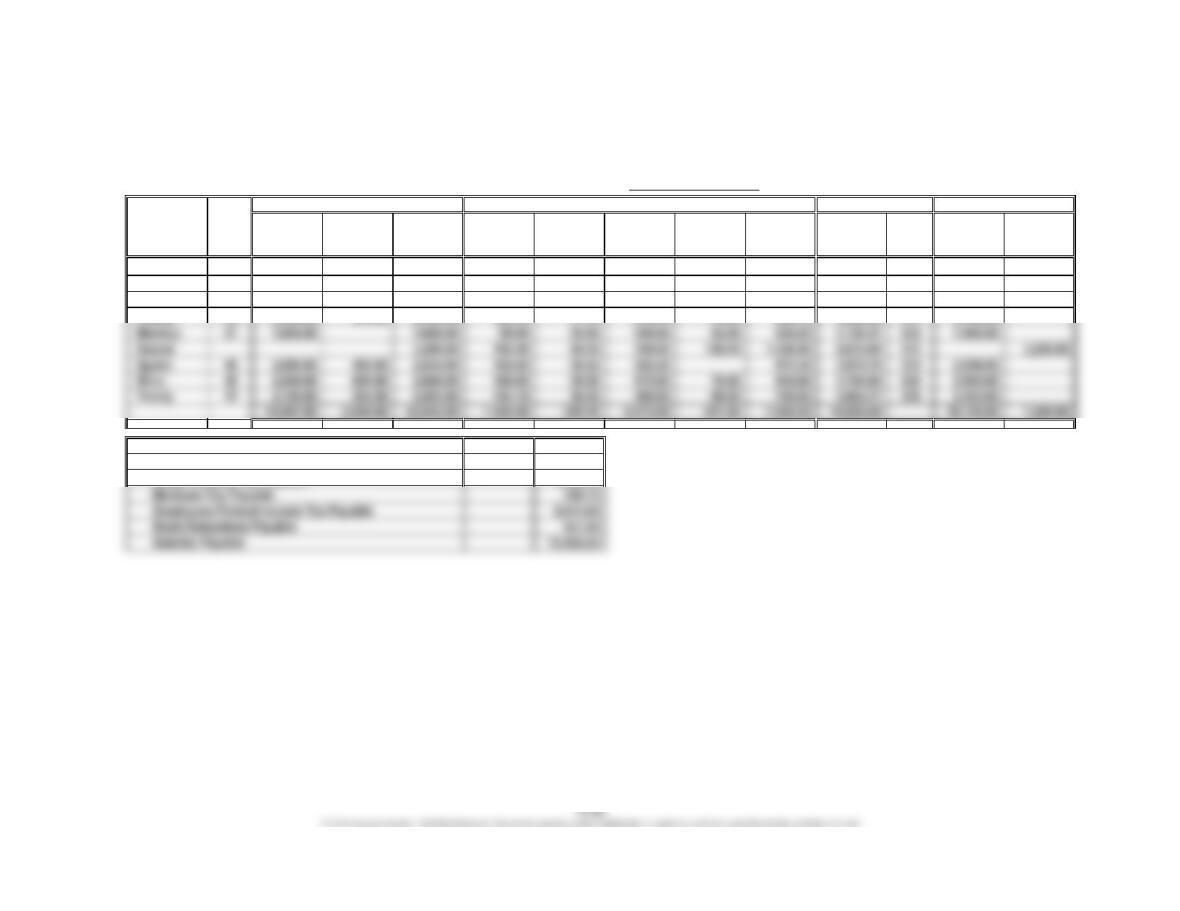

Prob. 11–4B

1.

Social Federal U.S. Sales Office

Total Security Medicare Income Savings Net Ck. Salaries Salaries

Employee Hours Regular Overtime Total Tax Tax Tax Bonds Total Pay No. Expense Expense

Carlton 52 2,000.00 900.00 2,900.00 174.00 43.50 667.00 60.00 944.50 1,955.50 328 2,900.00

Grove 4,000.00 240.00 60.00 860.00 100.00 1,260.00 2,740.00 329 4,000.00

Johnson 36 1,872.00 1,872.00 112.32 28.08 355.68 496.08 1,375.92 330 1,872.00

Koufax 45 2,320.00 435.00 2,755.00 165.30 41.33 578.55 44.00 829.18 1,925.82 331 2,755.00

2. Sales Salaries Expense 16,743.00

Office Salaries Expense 7,200.00

Social Security Tax Payable 1,436.58

PAYROLL FOR WEEK ENDING December 9, 2016

EARNINGS DEDUCTIONS PAID ACCOUNT DEBITED

CHAPTER 11 Current Liabilities and Payroll

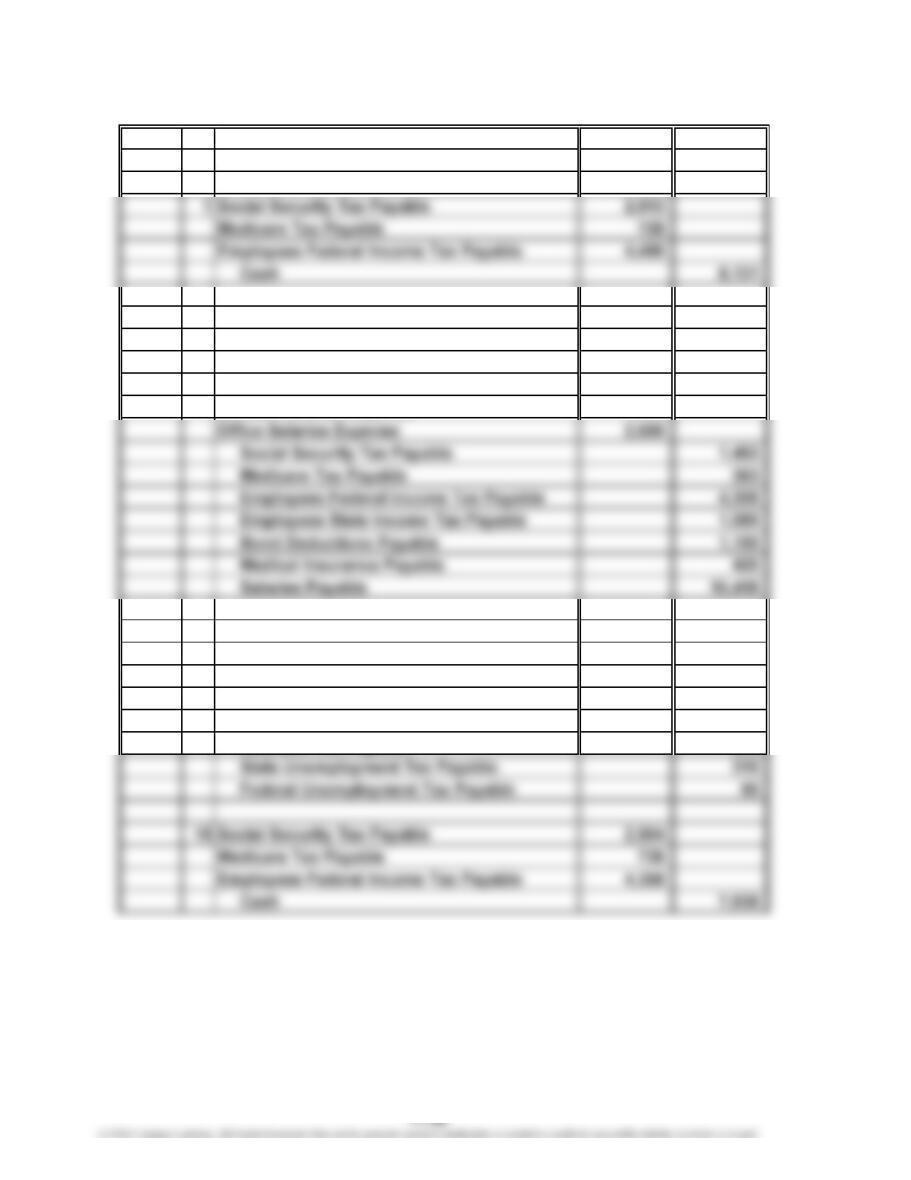

Prob. 11–5B

1. Dec. 1 Medical Insurance Payable 2,520

Cash 2,520

2 Bond Deductions Payable 2,300

Cash 2,300

12 Sales Salaries Expense 14,500

Officers Salaries Expense 7,100

12 Salaries Payable 15,418

Cash 15,418

12 Payroll Tax Expense 2,220

Social Security Tax Payable 1,452

Medicare Tax Payable 363

CHAPTER 11 Current Liabilities and Payroll

Prob. 11–5B (Concluded)

Dec. 26 Sales Salaries Expense 14,250

Officers Salaries Expense 7,250

Office Salaries Expense 2,750

Social Security Tax Payable 1,455

26 Salaries Payable 15,873

Cash 15,873

26 Payroll Tax Expense 2,009

Social Security Tax Payable 1,455

30 Employees State Income Tax Payable 6,258

Cash 6,258

30 Bond Deductions Payable 2,300

Cash 2,300

2. Dec. 31 Sales Salaries Expense 4,275

Officers Salaries Expense 2,175

Office Salaries Expense 825

CHAPTER 11 Current Liabilities and Payroll

1. Jan. 3 Petty Cash 4,500

Cash 4,500

Feb. 26 Office Supplies 1,680

Apr. 14 Merchandise Inventory 31,300

Accounts Payable 31,300

May 13 Accounts Payable 31,300

Cash 31,300

17 Cash 21,200

Aug. 1 Cash 182,400

Notes Receivable 180,000

Interest Revenue 2,400

($180,000 × 8% × 60 ÷ 360 = $2,400).

COMPREHENSIVE PROBLEM 3

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

Sept. 15 Land 654,925

Interest Expense 15,075

Notes Payable 670,000

($670,000 × 90 ÷ 360 × 9%).

30 Payroll Tax Expense 16,229

Social Security Tax Payable 12,735

Medicare Tax Payable 3,184

State Unemployment Tax Payable* 270

Federal Unemployment Tax Payable** 40

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

2.

Balance according to bank statement $283,000

Add deposit in transit, not recorded by bank 29,500

$312,500

Deduct outstanding checks 68,540

3. Miscellaneous Expense 750

4. a. Bad Debt Expense 18,000

Allowance for Doubtful Accounts 18,000

To record estimated uncollectible accounts,

$16,000 + $2,000.

b. Cost of Merchandise Sold 3,300

KORNETT COMPANY

Bank Reconciliation

December 31, 2016

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

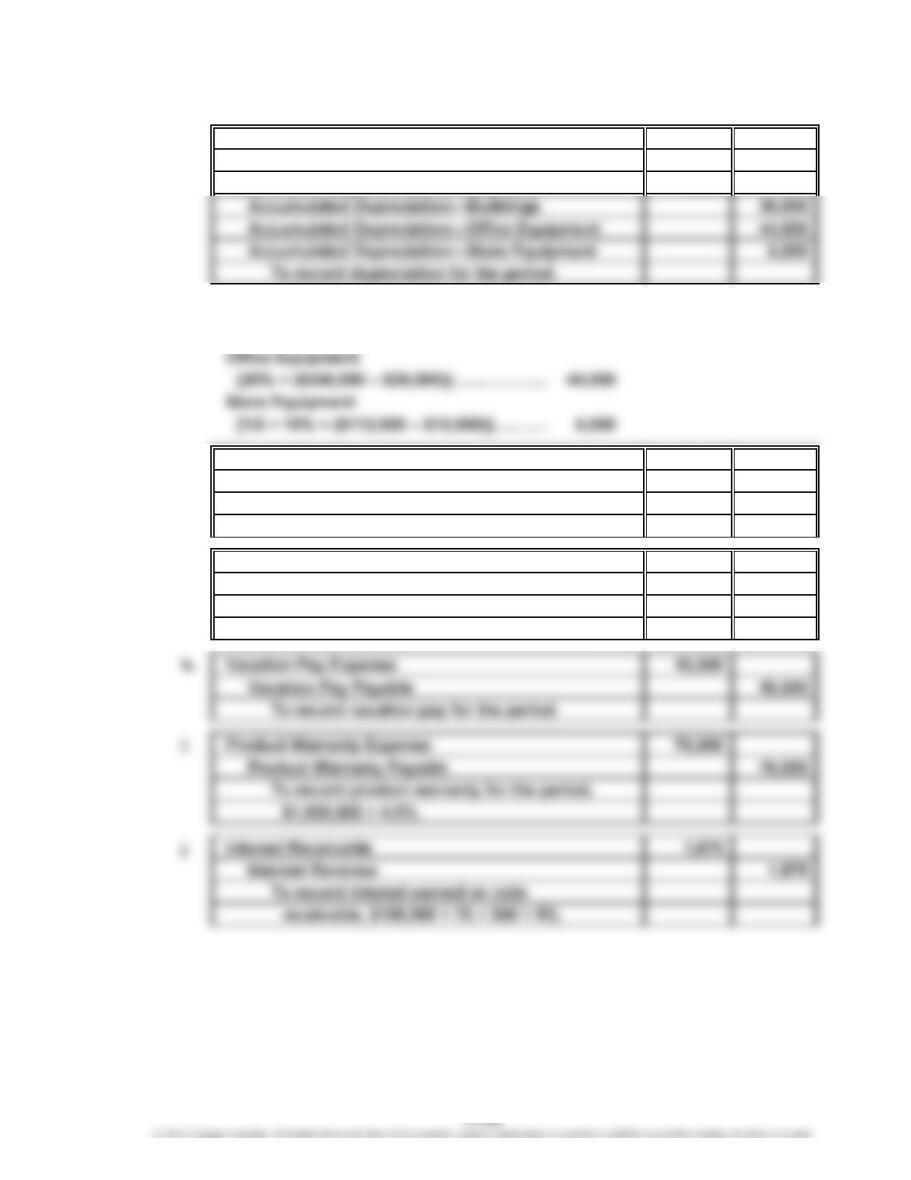

e. Depreciation Expense—Buildings 36,000

Depreciation Expense—Office Equipment 44,000

Depreciation Expense—Store Equipment 5,000

Computations:

Buildings ($900,000 × 4.0%)………………… $36,000

f. Amortization Expense—Patents 6,000

Patents 6,000

To record patent amortization,

$48,000 ÷ 8 years.

g. Depletion Expense 30,000

Accumulated Depletion 30,000

To record depletion,

($546,000 ÷ 910,000 tons) × 50,000 tons.

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Continued)

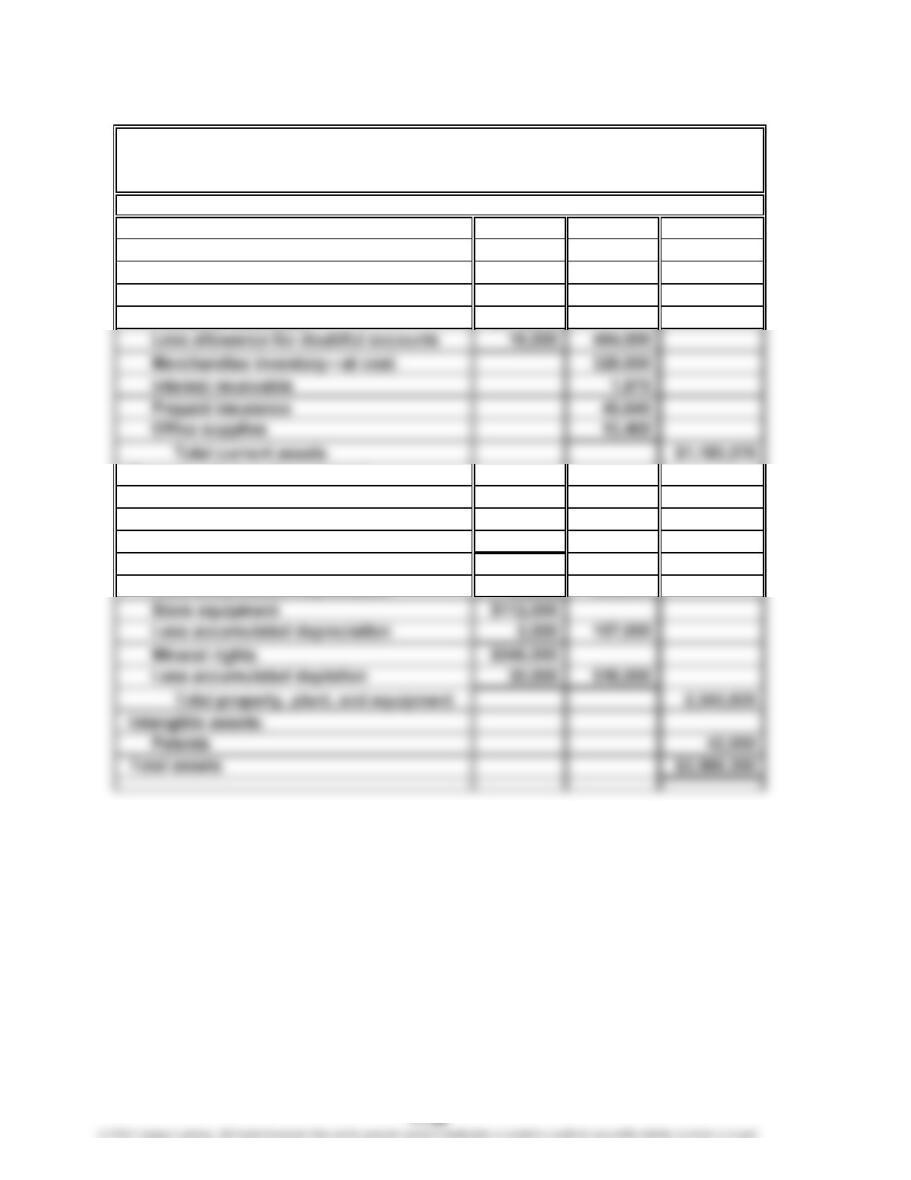

5.

Current assets:

Petty cash $ 4,500

Cash 243,960

Notes receivable 100,000

Accounts receivable $470,000

Property, plant, and equipment:

Land $654,925

Buildings $900,000

Less accumulated depreciation 36,000 864,000

Office equipment $246,000

Less accumulated depreciation 44,000 202,000

KORNETT COMPANY

Balance Sheet

December 31, 2016

Assets

CHAPTER 11 Current Liabilities and Payroll

Comp. Prob. 3 (Concluded)

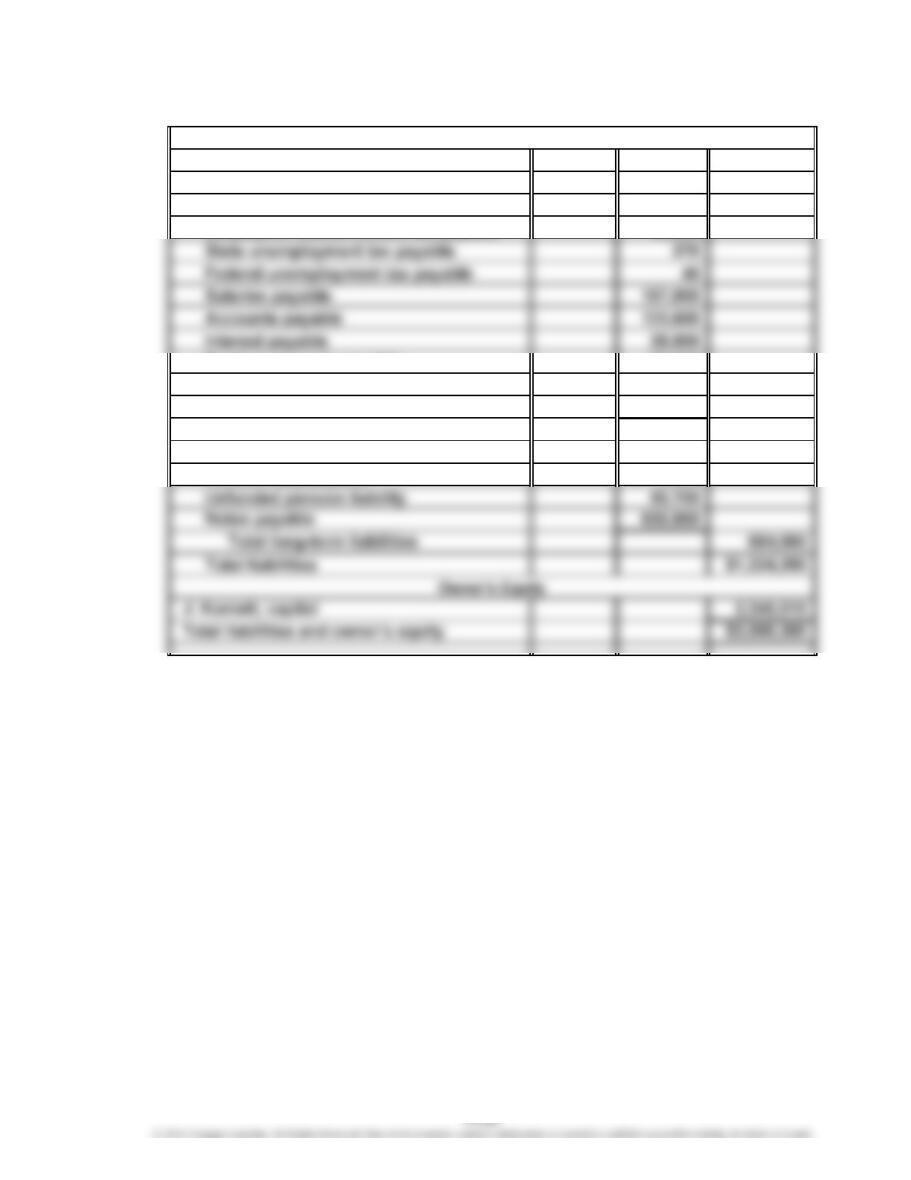

Current liabilities:

Social security tax payable $ 25,470

Medicare tax payable 4,710

Employees federal income tax payable 40,000

Product warranty payable 76,000

Vacation pay payable (current portion) 7,140

Notes payable (current portion) 70,000

Total current liabilities $ 540,230

Long-term liabilities:

Vacation pay payable $ 3,360

Liabilities

CHAPTER 11 Current Liabilities and Payroll

CP 11–1

The firm has no implicit or explicit contract to pay any bonus. The bonus is discretionary,

even if the firm paid a two-week bonus for 10 straight years. The firm is not behaving

unethically for reducing the bonus to one week—regardless of the reason. Tonya Latirno,

on the other hand, has taken things into her own hands. Sensing that she is being

cheated, she tries to rectify the situation to her own advantage by working overtime that

CP 11–2

Sumana’s interpretation of the pension issue is correct. The employee earns the pension

during the working years. The pension is part of the employee’s compensation that is

deferred until retirement. Thus, Felton should record an expense equal to the amount of

pension benefit earned by the employee for the period. This gives rise to the rather

CASES & PROJECTS

CHAPTER 11 Current Liabilities and Payroll

CP 11–3

a. The so-called “underground economy” hides transactions from IRS scrutiny by

conducting business with cash (not check or credit card, which leaves an audit

trail). The intent in many such transactions is to evade income tax illegally. However,

just because a transaction is in cash does not exempt it from taxation. Tina Song

b. Marvin should respond that he would rather receive a payroll check as a normal

employee does. Receiving cash as an employee, rather than a payroll check,

subverts the U.S. tax system. That is, such cash payments do not include

CP 11–4

The purpose of this activity is to familiarize students with retrieving and using IRS forms

Students should be able to find the three required forms without much difficulty.

Encourage students to retrieve the forms from the IRS Web site because this is a useful

source for any IRS form or publication that they might need. IRS Web site forms come in

.pdf format, which means Adobe Acrobat Reader or similar software is necessary to

open and print the file. PDF reader software is available as free plug-ins for most

Internet browsers. However, some students may need to download a full free version in

CP 11–5

This activity does not require the student to research the contingency notes for Altria

Group. The contingency disclosure is extensive and complicated. Rather, the student

should identify Altria Group’s main business, and from this information determine the

likely cause of the contingency disclosures.

a. Altria Group is a holding company for a number of businesses including Philip

Morris. Thus, Altria’s primary business is in the manufacture and distribution of

tobacco products.